Authored by José Antonio Ocampo, formerly United Nations Under-Secretary-General for Economic and Social Affairs, via Project Syndicate,

This year, the world commemorates the anniversaries of two key events in the development of the global monetary system. The first is the creation of the International Monetary Fund at the Bretton Woods conference 75 years ago. The second is the advent, 50 years ago, of the Special Drawing Right (SDR), the IMF’s global reserve asset.

When it introduced the SDR, the Fund hoped to make it “the principal reserve asset in the international monetary system.” This remains an unfulfilled ambition; indeed, the SDR is one of the most underused instruments of international cooperation. Nonetheless, better late than never: turning the SDR into a true global currency would yield several benefits for the world’s economy and monetary system.

The idea of a global currency is not new. Prior to the Bretton Woods negotiations, John Maynard Keynes suggested the “bancor” as the unit of account of his proposed International Clearing Union. In the 1960s, under the leadership of the Belgian-American economist Robert Triffin, other proposals emerged to address the growing problems created by the dual dollar-gold system that had been established at Bretton Woods. The system finally collapsed in 1971. As a result of those discussions, the IMF approved the SDR in 1967, and included it in its Articles of Agreement two years later.

Although the IMF’s issuance of SDRs resembles the creation of national money by central banks, the SDR fulfills only some of the functions of money. True, SDRs are a reserve asset, and thus a store of value. They are also the IMF’s unit of account. But only central banks – mainly in developing countries, though also in developed economies – and a few international institutions use SDRs as a means of exchange to pay each other.

The SDR has a number of basic advantages, not least that the IMF can use it as an instrument of international monetary policy in a global economic crisis. In 2009, for example, the IMF issued $250 billion in SDRs to help combat the downturn, following a proposal by the G20.

Most importantly, SDRs could also become the basic instrument to finance IMF programs. Until now, the Fund has relied mainly on quota (capital) increases and borrowing from member countries. But quotas have tended to lag behind global economic growth; the last increase was approved in 2010, but the US Congress agreed to it only in 2015. And loans from member countries, the IMF’s main source of new funds (particularly during crises), are not true multilateral instruments.

The best alternative would be to turn the IMF into an institution fully financed and managed in its own global currency – a proposal made several decades ago by Jacques Polak, then the Fund’s leading economist. One simple option would be to consider the SDRs that countries hold but have not used as “deposits” at the IMF, which the Fund can use to finance its lending to countries. This would require a change in the Articles of Agreement, because SDRs currently are not held in regular IMF accounts.

The Fund could then issue SDRs regularly or, better still, during crises, as in 2009. In the long term, the amount issued must be related to the demand for foreign-exchange reserves. Various economists and the IMF itself have estimated that the Fund could issue $200-300 billion in SDRs per year. Moreover, this would spread the financial benefits (seigniorage) of issuing the global currency across all countries. At present, these benefits accrue only to issuers of national or regional currencies that are used internationally – particularly the US dollar and the euro.

More active use of SDRs would also make the international monetary system more independent of US monetary policy. One of the major problems of the global monetary system is that the policy objectives of the US, as the issuer of the world’s main reserve currency, are not always consistent with overall stability in the system.

In any case, different national and regional currencies could continue to circulate alongside growing SDR reserves. And a new IMF “substitution account” would allow central banks to exchange their reserves for SDRs, as the US first proposed back in the 1970s.

SDRs could also potentially be used in private transactions and to denominate national bonds. But, as the IMF pointed out in its report to the Board in 2018, these “market SDRs,” which would turn the unit into fully-fledged money, are not essential for the reforms proposed here. Nor would SDRs need to be used as a unit of account outside the Fund.

The anniversaries of the IMF and the SDR in 2019 are causes for celebration. But they also represent an ideal opportunity to transform the SDR into a true global currency that would strengthen the international monetary system. Policymakers should seize it.

* * *

We are being primed and propagandized to desire this inevitability! Coming just a day after the Saudis threatened to end the Petrodollar, Ocampo’s op-ed is well-timed to say the least.

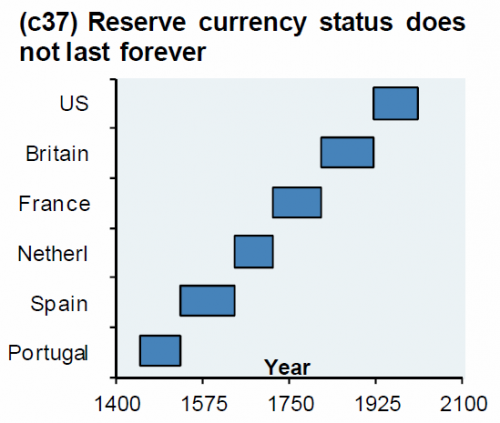

As we noted previously, nothing lasts forever.

via ZeroHedge News http://bit.ly/2UnBu0L Tyler Durden