Authored by Tsvetana Paraskova for Oilprice.com,

For more than ten weeks, portfolio managers have been consistently amassing bullish bets in the most important petroleum futures contracts, as market fundamentals were pointing to OPEC over-delivering on the production cuts, Venezuela’s supply crashing, and potential losses from conflict-torn Libya, amid resilient global oil demand growth.

Last week, oil prices jumped on Monday on the news that the U.S. is ending the sanction waivers for all Iranian oil buyers. And hedge funds continued to bet on higher prices and a tightening oil market.

However, the net long position – the difference between bullish and bearish bets – in WTI and Brent begins to look too stretched to the bullish side, making oil prices vulnerable to declines now if (or rather, when) money managers decide to do some profit taking and liquidate some of their bets on rising oil prices, analysts say.

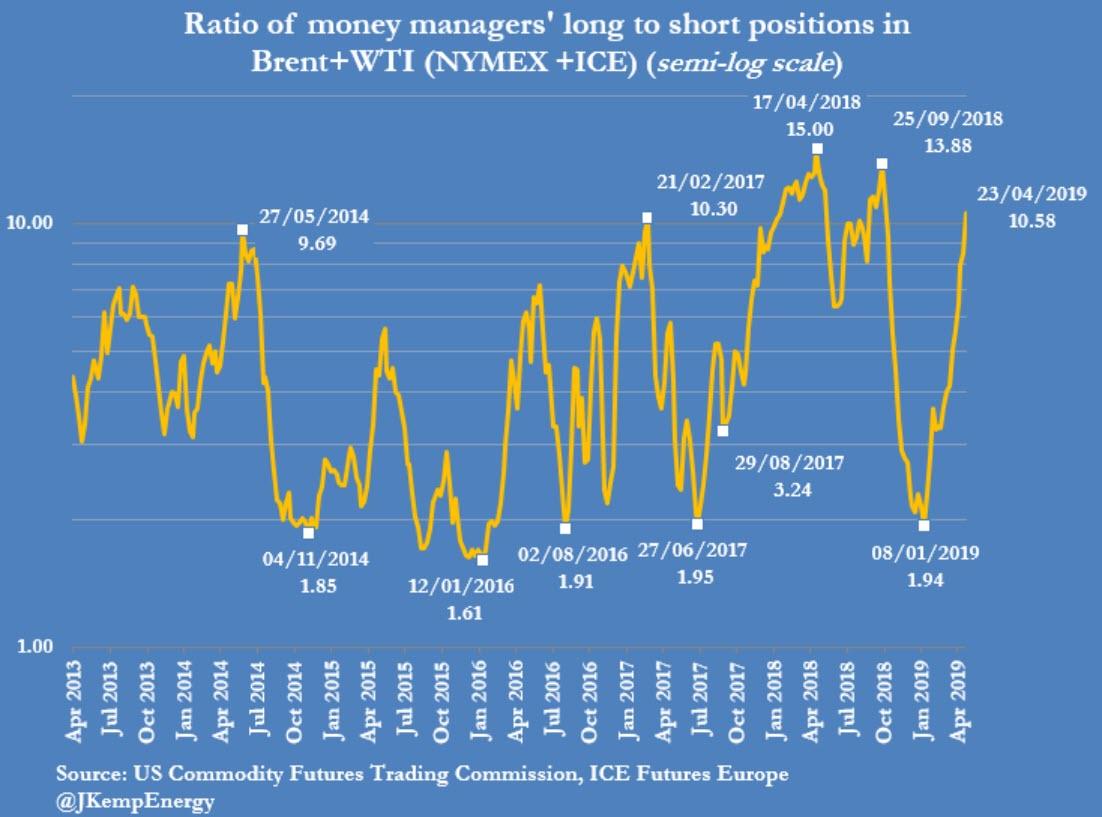

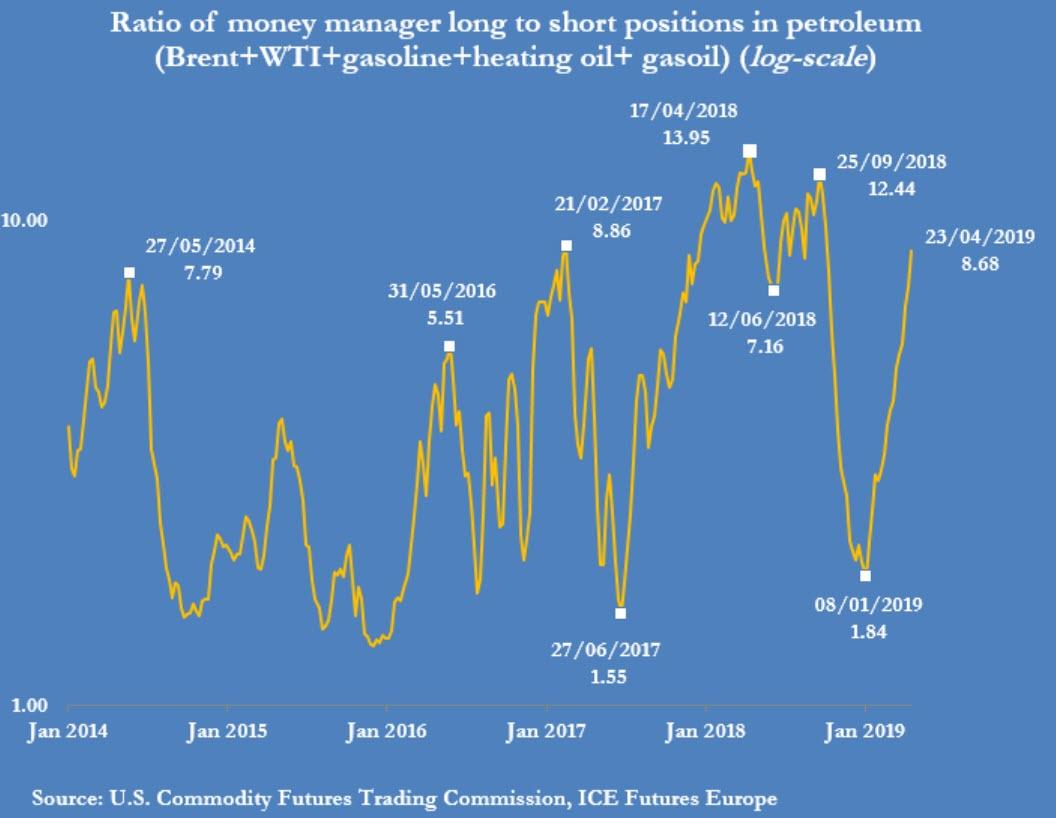

According to data compiled by Reuters market analyst John Kemp, as of April 23, the latest available exchange data, hedge fund and other money managers held long positions in Brent Crude and WTI Crude that outnumbered shorts in a ratio of 11:1—the most lopsided bullish positioning since October 2018, when oil prices started crashing to lose 40 percent until the end of 2018.

Portfolio managers have now closed out nearly all short positions that they had started to open at the end of August last year, Kemp says.

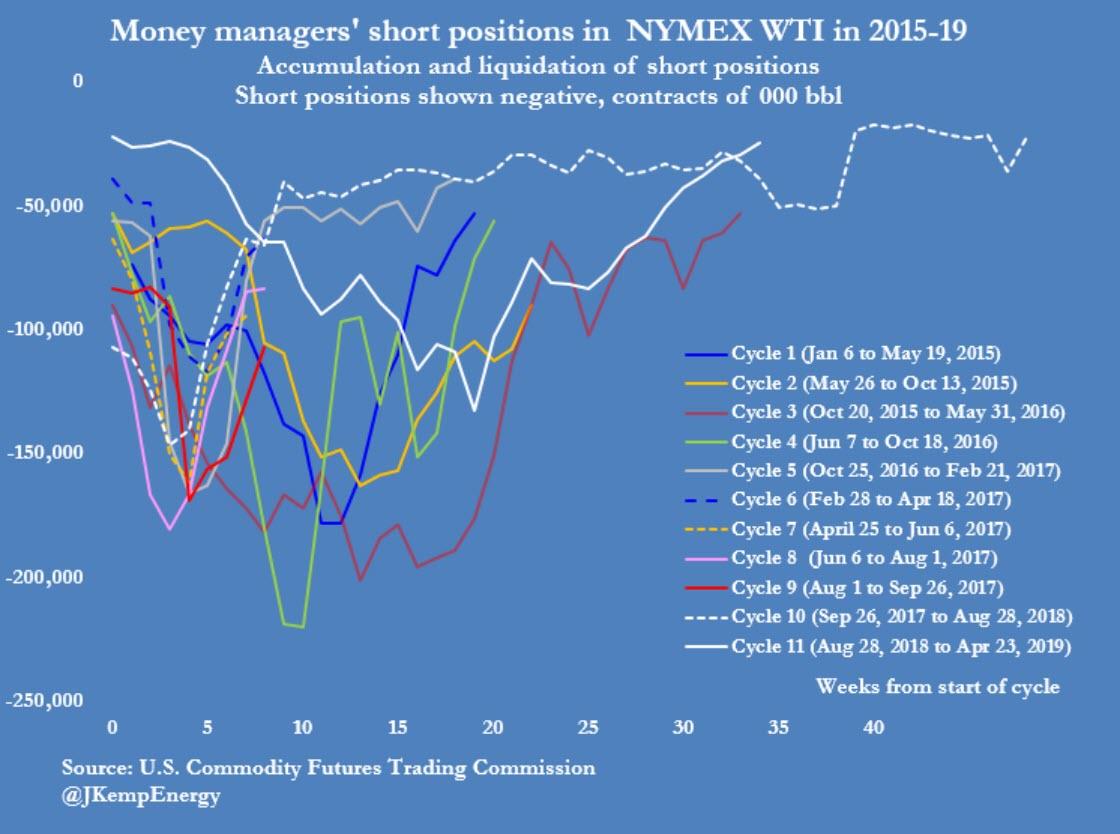

Hedge funds have been continuously amassing bets on rising WTI Crude prices for the past nine weeks, the longest bullish-building trading sentiment since 2006, according to data from the U.S. Commodity Futures Trading Commission compiled by Bloomberg.

The number of long positions in WTI Crude increased by 1.7 percent in the week to April 23, while the number of short positions slumped by 18 percent.

Money managers continue to bet that the market will further tighten, leading to higher prices, but this now overstretched bullishness is setting the scene for a pause in the oil rally, according to analysts.

“There’s been a lot of hedge fund buying, a lot of speculative interest, and we probably need to hit the pause button for now,” Phil Flynn, a senior market analyst with Price Futures Group, told Bloomberg on Monday.

Oil prices already hit the pause button, after jumping to six-month highs at the start of last week when the U.S. took the market by surprise announcing the end to all Iranian sanction waivers.

On Friday, oil prices tanked nearly 3 percent as U.S. President Donald Trump said that he “called up” OPEC and told the cartel that they have to bring gasoline prices down.

“Spoke to Saudi Arabia and others about increasing oil flow. All are in agreement,” President Trump tweeted later on Friday, but neither Saudi Arabia nor anyone else at OPEC appears to have spoken to the U.S. president.

While the U.S. and President Trump seem convinced that Saudi Arabia and other OPEC members will, once again, respond to Trump’s call to “increase oil flow,” the Saudis have been careful in statements about potential future production increases. Unlike last year, the Kingdom will not rush into pre-emptive increase in production unless it sees the actual number of barrels off the market, according to Saudi Energy Minister Khalid al-Falih.

“We are of the view that Saudi Arabia will increase output as soon as May, something they were likely to do anyway in the lead up to summer,” Warren Patterson, Head of Commodities Strategy at ING, said on Monday.

But even if the Kingdom were to raise its production by 500,000 bpd, it would still be complying with the OPEC+ pact because it has been over-complying with its share of the cuts by that amount.

“In the past when the President tweeted about oil, OPEC and its oil cutting co-conspirator Russia dutifully raised output. They won’t do it again. Already they are saying in comments that before they raise output, they want to see a shortage of oil, increased demand or signs that Iranian barrels are coming off. I don’t think the phantom OPEC phone call, or a tweet is going to change that,” Flynn wrote on Monday.

Further reduction of Iranian oil supply, on top of the U.S. sanctions on Venezuela and fears of a supply outage in Libya, where rivaling armies fight for the capital Tripoli, continue to lend support to oil prices. But the already crowded bullish positions of the hedge funds are bearish for oil prices.

via ZeroHedge News http://bit.ly/2J7PcxV Tyler Durden