Authored by Ryan McMaken via The Mises Institute,

This week, CNN reported on how, in spite of all the talk about job growth in recent years, wealth accumulation and incomes have been significantly and negatively impacted for many groups in the United States.

Much of what the article explored has been emphasized ever since the Great Recession started. The impact on younger earners, for example, has long been noted: “people entering the labor market during recessions have lower lifetime earnings.”

What was most interesting about the CNN article, however, was its admission that a persistent low-interest rate policy — one pursued by the central bank since the 2008 financial crisis — brings with it a serious downside. In a section titled “The mixed blessing of low interest rates” author Lydia DePillis discusses how low-interest rates have reduced the standard of living for those on mixed incomes, and has destabilized pension funds. Low rates have also made big firms even bigger at the expense of smaller firms:

But just like taking painkillers for too long can have side effects, the Fed’s monetary policy remedy gave rise to some unintended consequences. For example, low bond yields led the big funds that control trillions in investment to put their money into private equity and hedge funds that paid high rates. As a result, initial public offerings, which allow a wider group of people to benefit from the creation of new businesses, virtually dried up.

Meanwhile, low interest rates have been bad news for pension funds, which mostly depend on bond yields in order to remain solvent. Public pensions’ assets amounted to just 66% of their liabilities in 2016, down from 86% in 2007,according to the Pew Charitable Trusts . For the 100 largest private pensions, that ratio was 87.1% in 2018, according to the actuarial firm Milliman, compared to 105.7% in 2007.

For retirees counting on fixed-income securities like government bonds, low interest rates can also mean a lower standard of living.

“Low interest rates, while they have a lot of benefits, have a lot of costs for society as well,” said

Kevin Kliesen, an economist at the Federal Reserve Bank of St. Louis.

And that’s just short-term rates, which the Fed controls directly. Long-term interest rates were in decline before the financial crisis, and the ensuing recession depressed them even further; Fed officials are now struggling to nudge inflation up to their 2% target.

Those low interest rates may be sapping the economy of its vitality. One study published this year found that they give larger firms a greater incentive to invest than smaller ones. That fuels market concentration and reduces business dynamism — that is, the ability of startups to disrupt incumbents.

“As interest rates go down, they disproportionately favor market leaders as opposed to market followers,” said Atif Mian, a finance professor at Princeton University who coauthored the study. That effect, he found, “is large enough for low interest rates to not have any expansionary effect on the economy any more.”

Thre are three big takeaways here, and it’s surprising CNN has mentioned them.

-

Low interest rates have produced a quest for yield that favors the wealthy over the middle class.

-

Low interest-rate policy hurts regular people who depend on fixed incomes and low-risk sources of interest income.

-

Low interest rates favor large established firms over startups.

In other words, low interest rates favor the rich over the middle class, while widening income gaps.

This won’t be terribly surprising to those who follow the Austrian-school critique of ultra-low-interest and easy money policies.

Although critics of markets and so-called “neoliberalism” insist on ignoring the destructive power of central banks, the fact remains expansionary monetary policy serves to increase income inequality while favoring the already-wealthy. In other words, central banks are the cause of so much that capitalism is blamed for.

How Central Banks Destroy Wealth

Central-bank policy is problematic in a variety of ways. One of them — not mentioned by the CNN report — is the Cantillon effects brought about through the creation of money which is used first by financial institutions closer to the central bank and the easy-money spigots.

A second problem results when a “yield famine” results from low-interest-rate policy, but regular people can’t afford fancy yield-chasing investment products that are available to the wealthy.

Thus, ordinary people are left trying to gain interest income from government bonds, savings accounts, and CDs. In many cases, this strategy may not even allow the investor to keep up with price inflation.

A third problem stems from issues on the production side of the economy.

The CNN story notes a recent report suggesting large firms benefit more from low rates than small firms. The report, titled “Low Interest Rates, Market Power, and Productivity Growth” (by Ernest Liu, Atif Mian, and Amir Sufi) found that “the gap between the leader and follower increases as interest rates decline, making an industry less competitive and more concentrated.” In other words, low interest rates reduce competition and increase monopoly power of a small number of firms.

Moreover, the authors conclude their report

introduces the possibility of low interest rates as the common global “factor” that drives the slowdown in productivity growth. The mechanism that the theory postulates delivers a number of important predictions that are supported by empirical evidence. A reduction in long term interest rates increases market concentration and market power in the model. A fall in the interest rate also makes industry leadership and monopoly power more persistent.

The rise of low-interest-rate-induced monopoly power then stifles innovation, leading to lower productivity, and slower global economic growth. According to Liu, et al, this is not limited to the United States. It can be observed as a result of central-bank policy worldwide.

Last year, analyst Karen Petrou described how low rates have favored large companies.

As our research shows, QE exacerbates inequality because it takes safe assets out of the U.S. financial market, driving investors into equity markets and other financial assets not only to place their funds, but also in search of yields higher than those possible with ultra-low rates. The Fed hoped that soaking up $4.5 trillion in safe assets would stoke lending, and to a limited degree it did. However, new credit largely goes to large companies and other borrowers who have used it for purposes such as margin loans and stock buy-backs, not investment that would support strong employment growth. Growing household indebtedness in the U.S. is principally consumption or high-price housing driven and thus also a cause – not cure – of inequality.

Far from propelling middle class consumers to ever-higher levels of prosperity, low-interest rate policy is leading either to stagnation of losses in wealth.

But these revelations should not be shocking.

After all, Edward Wolff’s 2014 article “Household Wealth Trends in the United States, 1962-2013” suggests that our low-interest-rate world has done little to increase economic well being or counteract the effects of recessions:

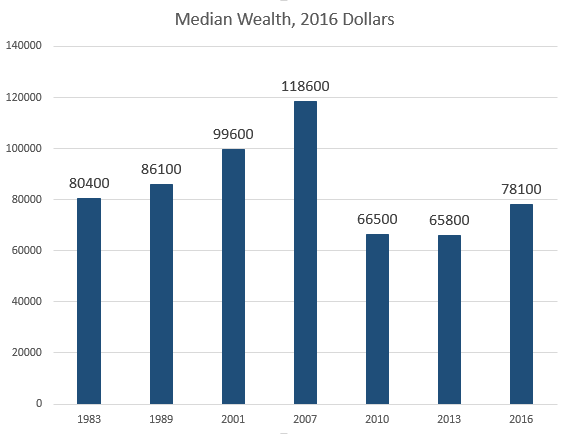

From 2007 to 2010, house prices fell by 24 percent in real terms, stock prices by 26 percent, and median wealth by a staggering 44 percent. Median income also dropped but by a more modest 6.7 percent and median non-home wealth plummeted by 49 percent. The share of households with zero or negative net worth rose sharply from 18.6 to 21.8 percent.

However, from 2010 to 2013, asset prices recovered with stock prices up by 39 percent and house prices by 8 percent. Despite this, both median and mean wealth stagnated, while median income was down by 1.3 percent but mean income rose by 0.9 percent. The percent of households with zero or negative net worth remained unchanged.

According to Wolff in this 2017 follow-up, as of 2016, “median wealth was still down by 34 percent.”

The evidence is mounting against the usual narrative which states that low-interest rate policy has been a clear good because it has stimulated demand and consumption.

On the contrary, there is reason to believe low-interest rate policy has lowered productivity, lessened economic growth, and favored large firms at the expense of small firms and innovation.

Median incomes have also suffered.

But central banks are clearly afraid to do anything but kick the low-interest can down the road. The Fed’s multi-trillion-dollar balance sheet isn’t going anywhere, and the Fed has no appetite for raising rates. But when the next recession hits, it’s likely the Fed and the world’s central banks will dish up more of the same: near-zero rates in the name of recovery and wealth creation. But this strategy’s record of delivering has been questionable at best.

via ZeroHedge News https://ift.tt/2Jgq1rt Tyler Durden