Platts: 6 Commodity Charts To Watch This Week

Via S&P Global Platt’s ‘The Barrel’ blog,

Oil markets are scrutinizing the export and stock balance of OPEC kingpin Saudi Arabia this week, following attacks on critical oil infrastructure. Brazil’s corn exports and the success of Gazprom’s European auction platform are also among our latest pick of energy and commodity market trends.

1. Saudi Arabia looks to plug oil export gap in wake of attacks

![]()

What’s happening? The devastating aerial attacks on Saudi Arabia’s key oil infrastructure last week brought into acute focus the falling crude supply buffer held by the world’s biggest oil exporter to shield against market trauma from upsets to its oil industry. Since OPEC cuts were launched in 2017, Saudi Arabia has been drawing on its crude stocks to help maintain export flows at a time of growing crude domestic demand for its expanding refining capacity. Official figures show Saudi crude stocks have shrunk over 40% since 2015, the majority of which has occurred under OPEC cuts.

What’s next? Oil markets will closely monitor the recovery of damaged Saudi production capacity. Attention will focus on any efforts to fill crude or products supply shortfalls, as Riyadh struggles to meet both its crude exports contracts and meet domestic fuel demand as it diverts some crude away from domestic refining.

2. Gazprom’s European gas sales through online auctions soar

![]()

What’s happening? It is now one year since Gazprom Export held the first auction on its Electronic Sales Platform (ESP), and since then more than 12.6 Bcm of gas has been sold to European buyers. That is almost enough to meet the demand of Austria and Hungary combined, and would outpace the expected production next year of the giant Groningen field in the Netherlands.

What’s next? The ESP has evolved from a simple auction platform to a dynamic sales tool, with Gazprom Export likely to continue to use it to sell surplus gas onto the European market regardless of price as it continues its strategy of prioritizing volume over value.

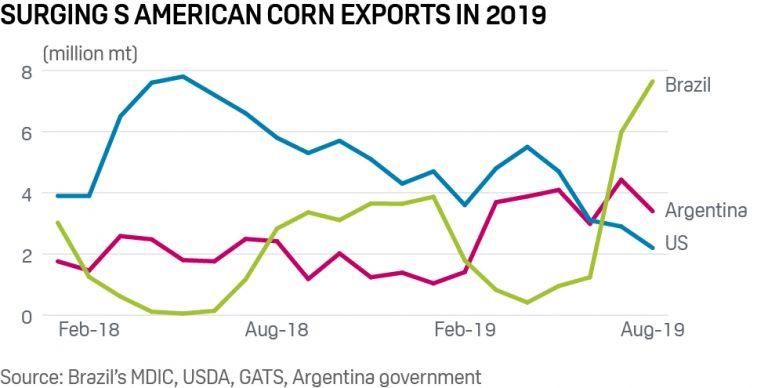

3. Brisk pace of S America corn shipments weigh on US exports

What’s happening? Following a record harvest this year, Brazil has been exporting corn at a brisk pace. Brazil corn production is expected to reach 99.98 million mt in 2018-2019. Corn exports hit a monthly record of 7.6 million mt in August. The US Department of Agriculture expects Brazil to export 38 million mt in 2018-2019 (March 2019-February 2020). Argentina, another major corn producer, is seeing robust export growth, with a jump of 66% on year during March-August this year.

What’s next? Markets will be keenly watching the progress of corn exports from South America, as the fast pace of shipments from Brazil and Argentina keeps US exports under pressure. Moreover, corn harvesting has also started for major producer Ukraine. As the US harvest nears, the price spread between the US and South American corn has narrowed, but US corn prices are still expected to remain uncompetitive through January 2020, according to the USDA.

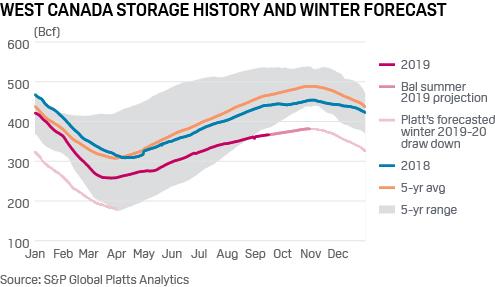

4. West Canada gas stocks on track to end injection season at 13-year low

What’s happening? Although US gas storage levels are near the five-year average as the injection season begins to wind down, inventories above the border in West Canada remain on track to close out the season at a 13-year low. Western Canadian production was down 0.7 Bcf/d summer over summer, and there have been injection curtailments on the NOVA Gas Transmission system. This has led to the region only injecting 67% of the five-year average, according to Platts Analytics.

What’s next? If this injection rate continues, Western Canada will end summer at its lowest volume since 2006. AECO futures for the 2019-2020 winter strip suggest the market is not anticipating these risks. The market could be expecting strong production to help offset low storage, but with the gas-focused rig count stalling near all-time lows, this seems unlikely.

5. Nordic power house in grand shape heading into winter

What’s happening? Sweden’s power exports are booming this year due to a surge in wind farm installations and demand from neighboring Finland. While completion of Finland’s 1.6 GW Olkiluoto-3 nuclear plant enters a tenth year of delay, Sweden has added 2.3 GW of wind this year alone, outpacing stalled onshore wind development in Germany and the UK.

What’s next? A Nordic wind boom means Scandinavia’s vast hydro reservoirs can afford to take stock through the summer ahead of a winter payday. As Nordic links to other markets are built, the region’s generators are increasingly well placed to take advantage of bountiful hydro, and now wind, resource.

6. Coking coal prices diverge on China, India buying behaviour

![]()

What’s happening? Coking coal prices are widening between grades, as global buyers reduce demand on weaker steel demand. China has prioritized buying low-vol coals over premium mid-vols as remaining import volumes under coal quotas shrunk. “Vol” refers to volatile matter – lower volatile matter increases coke production yield. Premium mid vol coking coals typically see regular spot demand in India, which is suffering an economic downturn. Post-monsoon spot buying in India is yet to fortify and inventory has been left to run down, while Europe and Brazil are needing less spot tons. Premium mid vol coking coals, such as Goonyella, Moranbah North and Illawara, are seeing the weakest pricing relative to benchmark Peak Downs and other premium low-vol HCC brands all year.

What’s next? Forward Chinese met coal import demand is facing uncertainty as coking coal volumes are anticipated to reach 2018 totals during September. This potential reduction in quotas for the fourth quarter may cut into demand for premium low-vol HCC, the grade most sought out by Chinese buyers. An extension to coking coal volumes under China’s import quota may be needed to help balance the market.

Tyler Durden

Mon, 09/23/2019 – 11:05

via ZeroHedge News https://ift.tt/2kE2uso Tyler Durden