Towards The Crisis: This Time Truly Is “Different”

Authored by Tuomas Malinen via GnSEconimcs.com,

The world economy has not been in a more precarious situation in over a decade. Growth is faltering everywhere, with the Eurozone flirting with recession, while central banks have returned to monetary easing after just one year of global tightening.

It is imperative to appreciate the exceptionality of the situation. Never before has the world gone into recession with interest rates so low and with the balance sheets of central banks so massive. This time truly is ”different”.

Yet, many seem not to worry about what’s coming. There is a strong sense of denial among the vast majority of analysts and economists—not to mention the general population—that we could be heading into something catastrophic—but we are. There is simply no denying it anymore.

The onset of the crisis may also be much closer than many understand. A fragile, slowing, and over-indebted global economy, inflated asset markets and a weak European banking sector combine forming a highly-explosive mixture, which many fail to acknowledge. Possible trade truce (or a deal) would do very little to solve these issues.

From non-standard to fragile (and beyond)

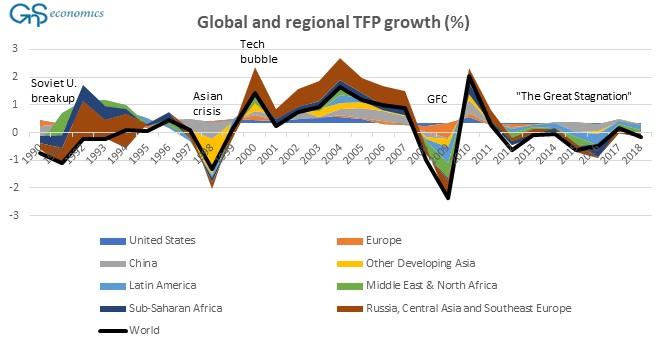

As we have repeatedly warned for several years, the constant meddling by central banks in global bond markets has seriously distorted the price of risk (see, e.g., this, this and this). This has weakened capital markets, but extremely low and negative interest rates have also produced a stagnant and fragile global economy. This is also apparent in the huge growth in the share of zombie corporations as well as in stalling global productivity growth (see Figure 1).

Figure 1. Regional and global growth rates of total factor productivity (TFP) in percentage points. Source: GnS Economics, Conference Board

Last week, Greece sold a 3-month treasury bill with a negative yield. It marks the latest and most preposterous milestone in the relentless hunt for yield across global markets initiated by the asset purchase programs as well as ”ZIRP” and ”NIRP” policies of central banks.

Bond markets were never convinced by the recovery after the 2008 crisis, but now, with negative-yielding debt hovering around $15 trillion, this lack of conviction has reached extreme levels. The massive push towards the safety of bonds sends an ominous signal about prospects for the global economy, but the resulting extreme in fixed-income prices also emphasizes the dangerous nature of inflated bond markets.

Very few seem to consider, what happens to bank collateral, for instance, if corporate and sovereign bond prices fall heavily, which seems likely in a recession.

European banking sector: A crisis waiting to happen

As we explained in our previous post, the European banking sector is in dire straits. Negative rates and QE have wreaked havoc on the profitability of European banks.

Also, while the Tier 1 Capital of European banks has clearly risen since 2009, these institutions are more vulnerable to a crisis in sovereign debt than ever. The “doom-loop” between sovereigns and banks in the Eurozone has actually tightened since 2008/2010 because sovereign debt is higher, especially in the weaker member nations, and the profitability of banks is lower. This is a very serious issue, because the sovereign debt markets in the Eurozone are undeniably in a bubble.

Moreover, “mark-to-fantasy”, the policy which assigns fictitiously high prices to assets that have actually lost their value (such as CDOs), and are currently deteriorating on the balance sheets of European banks, have crippled them for over a decade (since 2008). Along with negative interest rates and QE, impaired balance sheets have helped to zombify both the European banking sector and the economy of the Eurozone.

What will happen to banks when recession arrives in the Eurozone?

Non-performing loans will start to increase from already relatively-high levels and the profits of banks will fall further. It’s painfully obvious that the weak European banking sector will be utterly unable to cope with the resurgence of losses. A new global banking crisis, starting from Europe, is all but guaranteed.

With recession so close, we can prudently inquire: when does the confidence in European banks start to falter? Practically-speaking, it can happen anytime.

Tremors

Ominous signs have started to emerge, again. Recent problems in the ”repo” markets were attributed to regulatory issues and temporary lapses in liquidity. But now, ”emergency” funding by the Fed has been running for three weeks with no end in sight.

What if sudden spikes in repo rates are not caused by a lack of liquidity but rather by the quality of collateral and waning trust, similar to the 2007-2008 banking crisis? No one can say for sure, but the longer the issue persists, the more ominous it gets.

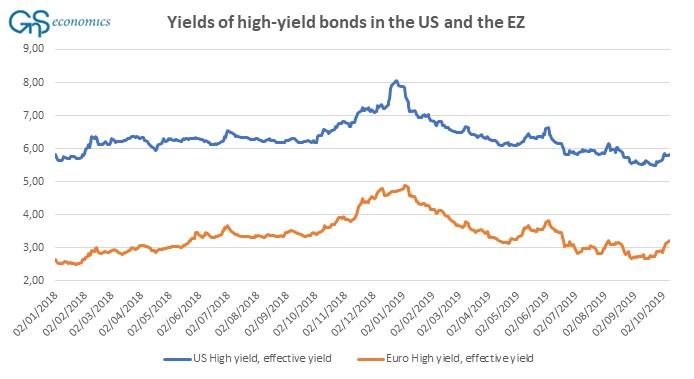

Cracks have also started to appear in the credit markets again. During the 2018/2019 turn-of-the-year panic, credit market almost succumbed (see Figure 2). They were saved by the joint efforts of the People’s Bank of China, which injected huge amounts of liquidity into the markets, and the Fed pivoting, completely, from its year-end projections that promised several interest rate rises in 2019 and an “automated” balance sheet run-off.

Figure 2. The daily effectively yield of junk rated companies in the Eurozone and the US. During the 2008 crisis, high yields topped 22 percent in the US and 25 percent in the Eurozone. Source: GnS Economics, St. Louis Fed

With the ECB once again engaged in QE, and with the Fed starting the “QE-lite” and cutting rates alongside with the PBoC, who will be left to “pivot” to save inflated credit markets this time around, when they finally roll over?

Nobody.

Crisis

By now, a troubling picture of the state of the global economy and markets should be clear for all to see. To ’top the cake’, the US 10y-3mo yield curve has un-inverted due to falling yields of 3-month T-bills. Historically, this has been one of the surest signs that a recession is close.

What happens, when weak European banks start to topple due to recession and the credit markets falter with central banks already fully-engaged in desperate resuscitation measures? There’s likely to be just one word to describe it: mayhem.

Why are people not more worried, then? It’s probably because of a sophisticated façade promoted by central banks and mainstream economists which emphasizes the ability of central banks to control the situation. This is a dangerous fallacy.

No one dares to look at the facts—or if they do, they dismiss them. Denial is a powerful force.

The fact is that monetary policy is running on empty, at least in the Eurozone, and governments can provide only limited fiscal stimulus. We’ve reached the end. There’s nothing left to do than prepare for the crisis and wait. And, to be very afraid.

Tyler Durden

Tue, 10/15/2019 – 15:25

via ZeroHedge News https://ift.tt/32kl8G9 Tyler Durden