Gary Shilling: Why It’s So Hard To Forecast The Economy

Authored by A.Gary Shilling, op-ed via Bloomberg.com,

Normal cyclical patterns have gone missing, and may not be coming back anytime soon…

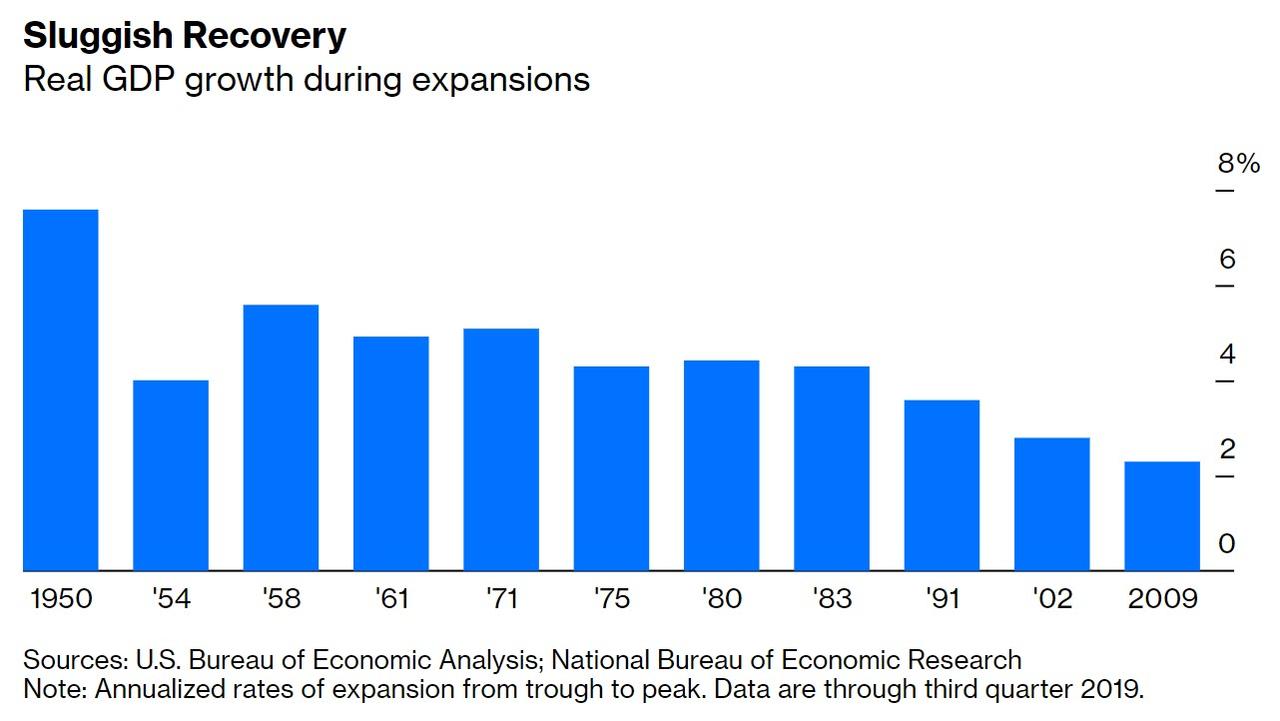

The U.S. economy has experienced its slowest recovery from a recession in the post-World War II era, and the longer it lasts the more evidence there is that normal cyclical patterns are missing. And their absence means market participants shouldn’t rely on them to divine the economy’s future.

Consider the myriad developments that are atypical, or even the reverse of normal economic and financial market behavior. The Federal Reserve shifted from easing credit to tightening following past downturns, with its target federal funds rate normally raised within a year or so of the recession’s trough, eventually precipitating the next economic contraction. This time, the central bank kept its policy rate at the recessionary low of essentially zero until Dec. 2015, 78 months into the recovery. And then, after nine quarter-percentage point increases, it reversed course early this year with three rate cuts.

Far from the Fed’s normal worries about an overheating economy and inflation, the central bank frets that low and even declining consumer prices will spawn deflationary expectations. Buyers will hold off in anticipation of lower prices. Inventories and excess capacity will mount, forcing prices down. The price cuts confirm suspicions and purchases are delayed even further, sparking a deflationary spiral. The glaring example is Japan, with deflation in most years in the past two decades and tiny real GDP annual growth of 1.1%.

Also, despite the plunge in 30-year fixed mortgage rates from 6.8% in July 2006 to the current 3.7%, rate-sensitive single-family housing starts have been muted. They fell from a 1.8 million annual rate in January 2006 to 350,000 in March 2009 as the subprime mortgage market collapsed, but have only recovered to 940,000.

Mortgage lending criteria have tightened and prime-age first-time homebuyers don’t have the necessary downpayments. The net worth of households headed by 18-to-34-year-olds dropped from $120,000 in 2001 to $90,000 in 2016, a 44% decline adjusted for inflation. Also, they learned from the last recession that for the first time since the 1930s, house prices nationwide can fall.

In past business recoveries, the U.S. household saving rate fell as consumer spending grew faster than incomes. In this expansion, it’s the reverse, leaping from 4.9% to 7.9% in November, retarding spending.

Past postwar recessions spawned financial problems, but nothing like the 2008 crisis. The government’s reaction was equally severe with the enactment of the 2010 Dodd-Frank Act and other stringent regulations for financial institutions that are only now being slowly relaxed.

In earlier business upswings, a drop in the unemployment rate of anything like the plunge from 10% in October 2009 to the current 3.5% would have spawned massive wage inflation. This time, real wages are barely growing.

Globalization transported many high-paid manufacturing jobs to China. With the growing “on demand” economy—think Uber Technologies Inc. —many people trade flexibility in working hours for low pay. The payroll jobs that are being created are mostly in low-wage sectors such as retailing and leisure & hospitality.

For years, foreign policy was bipartisan and expanding trade was considered highly desirable. Now, globalists have been overcome by protectionists, spurred by voters upset over stagnant purchasing power and rising income and asset inequality in G-7 countries. Trump’s 2016 election along with the U.K.’s “Brexit” from the European Union are among the results. Then there’s also the demise of global trade deals, which are being replaced by bilateral agreements or no pacts at all.

The U.S.-China trade dispute will no doubt persist because China, with a declining labor force as a result of its earlier one child-per-couple policy, needs Western technologies to grow and achieve its worldwide leadership ambitions. But the U.S. is opposed to the technology transfers China wants.

The dollar’s slide from 1985 until 2007 encouraged U.S. exports, curbed imports and gave U.S. multinationals currency-related boosts to profits. Since then, the dollar index has rallied 33% amid a global demand for haven assets. And it should continue to, given the relatively faster growth of the U.S. economy, its huge, free and open financial markets and the lack of meaningful substitutes for the greenback.

Disinflation has reigned since 1980, but real interest rates were positive until the last decade. But for 10 years now, real 10-year Treasury note yields have been flat at zero (see my Nov. 19, 2018 column, “Zero Real Yields Are Tripping Up Investors”). This and the flat yield curve have pushed state pension funds and other investors far out on the risk curve in search of real returns, bidding up stocks to vulnerable levels.

Earlier, the Fed was run by Ph.D. economists who clung to widely-held theories even though they didn’t work. Fed Chairman Jerome Powell is proving to be much more practical, backing away from rigid Fed policies such as the 2% inflation target and a zero-bound policy rate as well as unsuccessful forward guidance.

In this different economic climate, it’s hard to time the end of the current recovery. Still, it will end, due either to Fed overtightening or a financial crisis, like the 2000 dot-com blow-off or the 2007-2009 subprime mortgage collapse. In the current excess supply-savings glut-deflationary world, it’s likely a recession will unfold due to a shock before the Fed overtightens.

No financial crises are in sight, but there are possibilities such as excess debt in China and among U.S. businesses, a trade war escalation, consumer retrenchment resulting in widespread deflation, and disappointing corporate profits measured against sky-high stock prices. Watch for specific imbalances, not typical past patterns.

Tyler Durden

Wed, 01/01/2020 – 19:00

via ZeroHedge News https://ift.tt/37wA9GX Tyler Durden