If Turkish President Recep Tayyip Erdogan believes he can bully European leaders by provoking a fresh migrant crisis in southern Europe, then he would be well-advised to think again.

Ankara’s announcement that it is once again opening the floodgates to allow millions of refugees from Syria’s brutal civil war to travel to south-eastern Europe in search of refuge has been taken to persuade European leaders to back Turkey’s increasingly desperate situation in Syria.

Having launched an ill-considered military offensive against the Assad regime in northern Syria, Mr Erdogan now finds himself facing the consequences of his action, with regime forces, backed by Russia and Iran, waging a highly effective campaign against the Turks, which has so far resulted in the deaths of scores of Turkish troops.

In addition, Turkey’s decision to deploy thousands of troops to Idlib province in northern Syria has resulted in a fresh wave of refugees fleeing across the border into southern Turkey, where Turkish officials are already struggling to cope with the estimated four million Syrian refugees that have already sought sanctuary in the sprawling refugee camps.

One of the main reasons that Mr Erdogan now finds himself facing this difficult predicament is that he has badly underestimated the nature of his relationship with Russian President Vladimir Putin.

When Turkey took the controversial decision last year to purchase Russia’s state-of-the-art S-400 anti-aircraft missile system, Mr Erdogan calculated that it would herald new era of friendly cooperation with Ankara’s long-standing rival in Moscow even if, by pressing ahead with the deal, the Turks risked jeopardising their relationship with NATO, which bitterly opposed the deal.

There was certainly an expectation in Ankara that improved relations with Moscow would result in better cooperation between the two countries on the post-conflict settlement in Syria, especially regarding Turkey’s desire to establish a safe zone in northern Syria.

Yet, as the recent escalation in fighting has demonstrated, the Russians’ main priority is to support the Assad regime in its attempts to regain control of the last remaining rebel stronghold in northern Syria. Thus the Russians now find themselves in a direct confrontation with Turkish forces in Idlib province, where the Turks are trying to protect a number of Islamist militias committed to overthrowing the Assad regime.

If the current crisis facing Turkey is entirely of Mr Erdogan’s own making, that has not prevented the Turkish president from trying to deflect attention away from his own mishandling of the conflict by seeking to provoke a new migrant crisis in Europe.

Mr Erdogan used this tactic to great effect five years ago when, in response to Turkey’s decision to allow more than a million Syrian refugees to travel to Europe, he succeeded in persuading the European Union to pledge six billion euros to Ankara in return for allowing the refugees to remain on Syrian soil.

Yet, to judge by the initial response from European leaders to Mr Erdogan’s latest attempt to blackmail them, it seems that, this time around, the Turkish leader’s ploy is unlikely to deliver the desired result.

For a start, a meeting of NATO ambassadors called last week to discuss the increasingly vulnerable position of Turkish forces in Syria ended with expressions of sympathy for the Turks, but little else. Other NATO member states are simply not interested in getting involved in a conflict that might result in them being involved in a direct military confrontation with Moscow.

Mr Erdogan is also about to discover that there has been a hardening of attitudes among European leaders about dealing with unwanted migrants since the Turkish leader last used his blackmail tactics five years ago.

At a meeting of EU ambassadors this week to discuss the migrant crisis, officials expressed their outrage at Ankara’s behaviour.

Nor can Mr Erdogan expect any support from Germany, where German Chancellor Angela Merkel responded to the last migrant crisis by opening Germany’s doors to an estimated one million refugees, a decision that seriously undermined her political popularity.

These days, senior politicians in Mrs Merkel’s centre-right Christian Democrats take a more hard-nosed approach to the migrant issue, with one senior party member warning the migrants this week, “There is no point coming to Germany. We cannot take you in.”

Europe might have fallen for Mr Erdogan’s bully-boy tactics in the past. But all the evidence from the latest migrant crisis suggests they are not about to do so again.

The annual Munich Security Conference that took place February 14-16 this year turned out to be an iconic event, drawing comparison with the one held in the same Bavarian city on February 10, 2007, where in a prophetic speech Russian President Vladimir Putin had criticized the world order characterized by the United States’ global hegemony and its “almost uncontained hyper use of force – military force – in international relations.”

If Putin’s 2007 Munich speech was prescient about an incoming new Cold War and the surge of tensions in Russia’s relations with the West, 13 years later, at the event this year, we witnessed that the transatlantic ties that evolved through the two world wars in the last century and blossomed into a full-fledged alliance system have reached a crossroads.

Deep cracks have appeared in the transatlantic relationship. In an extraordinary opening address, German President Frank-Walter Steinmeier, an éminence grise in European diplomacy, accused Washington of rejecting “the very concept of an international community.”

Steinmeier acknowledged that there is no return to the halcyon days of close transatlantic partnership, as Europe and the U.S. are drifting away from each other. He warned, “If the European project fails, the lessons of German history, but perhaps also European history, will be called into question.”

Having said that, Steinmeier did not advocate that Europe could go it alone, either. Rather, “only a Europe that can and wants to protect itself credibly will be able to keep the U.S. in the alliance.”

But he regretted that “Europe is no longer as vital to the U.S. as it used to be. We must guard against the illusion that the United States’ dwindling interest in Europe is solely down to the current administration… For we know that this shift began a while ago, and it will continue even after this administration.”

The theme of European independence—Europe becoming a sovereign, strategic and political power—was also the leitmotif of a speech by French President Emmanuel Macron who brought a rare dynamism into the European debate, fighting spiritedly for a common European foreign and security policy. The German policymakers have signaled broad agreement with Macron’s idea that Europe must take charge of its own destiny.

In contrast, the U.S. Secretary of State Mike Pompeo had earlier insisted that the talk about the demise of the West is “grossly exaggerated,” and, in fact, “the West is winning. We are collectively winning. We are doing it together.”

Meanwhile, two subplots that kept appearing in the discussions were, one, the continued relevance of multilateralism in the international system and, two, deep anxiety over the current global security environment.

Steinmeier framed the concerns sharply, saying, “the idea of international community is not outmoded,” adding that “withdrawing into our national shells leads us into a dead end, into a truly dark age.”

All in all, these sharp exchanges between the Europeans and some of the American delegation confirmed, more than ever, the weakness and disunity of the West. A Politico report on the Munich Security Conference noted, “The two sides aren’t just far apart on the big questions facing the West (threats from Russia, Iran, China), they’re in parallel universes.”

One major issue that divided Munich was China. Neither Pompeo nor Defense Secretary Mark Esper left any doubt that Washington considers China to be a nefarious force in the world, representing a significant long-term threat. But that view is not shared by many countries in the EU. The underlying question is what posture the Western alliance should take toward China, which is a fundamental one with far-reaching consequences. Europe is deeply worried about the consequences that spurning Beijing would have on trade and investment.

It became apparent at the conference that there was no acceptance of Pompeo’s plea that China is the new enemy. His cautioning against the involvement of the Chinese tech company Huawei in the upcoming 5G rollout met with stony silence by European allies. The policy toward China could emerge as the biggest transatlantic divide.

Can the West regain its influence? The crux of the matter is that with the decline in material wealth and the decay of moral values, the capacity to influence has shrunk. And the West’s form of economic organization is no longer as appealing as it once was. Also, with the rise of China, rapid development of India, and the resurgence of Russia, a new dynamic of global power is taking shape.

As these and other emerging powers grow in strength, a dispersion of power and influence is bound to accelerate, and the West is unlikely to regain the preponderant influence it wielded in the post-World War II era.

This drain of influence might slow down if only a “new West” led by Europe that combined power and values reached out to powers such as India or Japan to build global alliances. But a major lacuna lies in the United States’ contempt of multilateralism and a rules-based order.

Equally, Washington’s push for trade-offs to advance its unilateral confrontations—be it with Russia and China or Iran and Venezuela—fails to strike a chord with its top Western partners, the majority of whom are averse to any form of confrontation, least of all with Beijing.

“We cannot be the United States’ junior partner,” said Macron, citing recent failures in the West’s policy of defiance. Clearly, internal divisions afflict the West, and it is hard to see how they can be overcome.

At best, coalitions of the willing may appear within and among the Western states on specific issues. But even then, the West can at best slow down its relative decline but nowhere near reverse it.

The heart of the matter is that the economic center of gravity in the world order and the ensuing global power equation is inexorably shifting away from the West, while on the other hand, there is no longer a “West” that is united behind principles, values, and policies.

Minimum-Wage Blowback – Fast Food Burger-Flipping Robot Works For $3 An Hour

Over the years, we’ve documented the proliferation of artificial intelligence and robots in the workplace would lead to a tidal wave of job losses through 2030.

What peaked our attention several years ago was Miso Robotics, a Pasadena tech company with the focus of developing robots for fast-food restaurants, has seen the price of its burger-flipping robot drop from $100,000 to $10,000 in four years.

“Off-the-shelf robot arms had plunged in price in recent years, from more than $100,000 in 2016, when Miso Robotics first launched, to less than $10,000 today, with cheaper models coming in the near future,” according to the Los Angeles Times.

The burger-flipping robot is now more cost-effective than the average low-skilled employee, which means Miso’s unveiling of a subscription plan for restaurants, of just $2,000 a month, with the choice of a robot that works either the grille or fryer, could be very appealing to restaurant owners or managers across the country who need to drive down labor costs.

“As a result, Miso can offer Flippys to fast-food restaurant owners for an estimated $2,000 per month on a subscription basis, breaking down to about $3 per hour. (The actual cost will depend on customers’ specific needs). A human doing the same job costs $4,000 to $10,000 or more a month, depending on a restaurant’s hours and the local minimum wage. And robots never call in sick,” LA Times adds.

Americans could soon see Flippy or a variant of the robot at a mom and pop restaurant or a major fast-food chain in the early 2020s, the affordability of these robots will entice restaurant operators to drive down labor costs.

On a much broader perspective, Karen Harris, Managing Director of Bain & Company’s Macro Trends Group, presented a fascinating report several years ago titled “Labor 2030: The Collision of Demographics, Automation, and Inequality,” which outlines how automation could eliminate upwards of 40 million jobs by the end of this decade.

Millions of Americans are employed in the fast-food industry; the proliferation of automation could lead to a rapid increase in job losses through the mid to late 2020s. The labor market could see major disruptions from robots in the years ahead, it’s expected this trend could force the government to have the Federal Reserve finance People’s Quantitative Easing, in the form of universal income, etc.

It may seem preposterous to suggest that the outbreak of the new coronavirus, COVID-19, has imperiled the rule of the Communist Party of China (CPC), especially at a time when the government’s aggressive containment efforts seem to be working. But it would be a mistake to underestimate the political implications of China’s biggest public-health crisis in recent history.

According to a New York Times analysis, at least 760 million Chinese, or more than half the country’s population, are under varying degrees of residential lockdown. This has had serious individual and aggregate consequences, from a young boy remaining home alone for days after witnessing his grandfather’s death to a significant economic slowdown. But it seems to have contributed to a dramatic fall in new infections outside Wuhan, where the outbreak began, to low single digits.

Even as China’s leaders tout their progress in containing the virus, they are showing signs of stress. Like elites in other autocracies, they feel the most politically vulnerable during crises. They know that, when popular fear and frustration is elevated, even minor missteps could cost them dearly and lead to severe challenges to their power.

And “frustration” is putting it mildly. The Chinese public is well and truly outraged over the authorities’ early efforts to suppress information about the new virus, including the fact that it can be transmitted among humans. Nowhere was this more apparent than in the uproar over the February 7 announcement that the Wuhan-based doctor Li Wenliang, whom the local authorities accused of “rumor-mongering” when he attempted to warn his colleagues about the coronavirus back in December, had died of it.

With China’s censorship apparatus temporarily weakened – probably because censors had not received clear instructions on how to handle such stories – even official newspapers printed the news of Li’s death on their front pages. And business leaders, a typically apolitical group, have denounced the conduct of the Wuhan authorities and demanded accountability.

There is no doubt that the authorities’ initial mishandling of the outbreak is what enabled it to spread so widely, with health-care professionals – more than 3,000 of whom have been infected so far – being hit particularly hard. And despite the central government’s attempts to scapegoat local authorities – many health officials in Hubei province have been fired – there are likely to be more questions about what Chinese President Xi Jinping knew.

Not surprisingly, Xi has been working hard to repair his image as a strong and competent leader. After the central government ordered the lockdown of Wuhan in late January, Xi appointed Premier Li Keqiang to lead the coronavirus task force. But the fact that it was Li, not Xi, who went to Wuhan seemed to send the wrong message, as Xi realized in the subsequent days.

On February 3, at a Politburo Standing Committee meeting, Xi took an unusually defensive tone in a speech that smacked of damage control. While Xi admitted that he had learned of the outbreak before he sounded the alarm, he emphasized his personal role in leading the fight against the virus.

Moreover, on February 10, Xi made a series of public appearances in Beijing, aimed at reinforcing the impression that he is firmly in command. Three days later, he sacked the party chiefs of Hubei province and Wuhan municipality for their inadequate handling of the crisis. And two days after that, in an unprecedented move, the CPC released the full text of Xi’s internal Politburo Standing Committee speech.

Though Xi has apparently regained his aura as a dominant leader – not least thanks to CPC propagandists, who are working overtime to restore his image – the political fallout is likely to be serious. The profound uproar that marked those fleeting moments of relative cyber-freedom – the two weeks, from late January through early February, when censors lost their grip on the popular narrative – should be deeply worrying to the CPC.

Indeed, the CPC may be highly adept at repressing dissent, but repression is not eradication. Even a momentary lapse can unleash bottled-up anti-regime sentiment. One shudders to think what might happen to the CPC’s hold on power if Chinese were able to speak freely for a few months, not just a couple of weeks.

The most consequential political upshot of the COVID-19 outbreak may well be the erosion of support for the CPC among China’s urban middle class. Not only have their lives been severely disrupted by the epidemic and response; they have been made acutely aware of just how helpless they are under a regime that prizes secrecy and its own power over public health and welfare.

In the post-Mao era, the Chinese people and the CPC have adhered to an implicit social contract: the people tolerate the party’s political monopoly, as long as the party delivers sufficient economic progress and adequate governance.

The CPC’s poor handling of the COVID-19 outbreak threatens this tacit pact. In this sense, China’s one-party regime may well be in a more precarious position than it realizes.

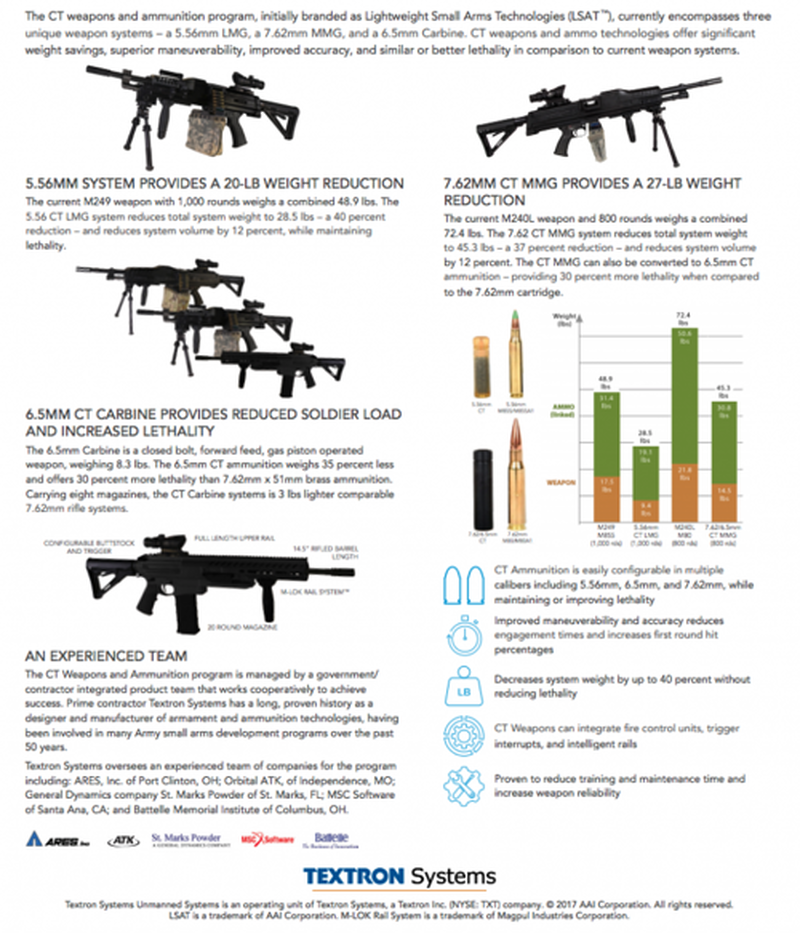

Alton Stewart, a spokesman for the Army’s Program Executive Offices (PEO), said the PSR would replace M107 and M2010 Enhanced Sniper Rifle.

The Tennessee-made PSR, which is produced by Barrett Firearms Manufacturing, is a bolt-action Multi-Role Adaptive Design (MRAD) system and called the Mk 22, which will be chambered in 7.62×51 mm NATO round. The PSR is the next generation of sniper rifles, and it’s lightweight, more accurate, and more reliable than legacy systems.

Task & Purpose said, “the PSR provides the increased probability of hit over the current M2010 [Enhanced Sniper Rifle] configuration at distances up to twelve-hundred (1200) meters and increases range out to fifteen-hundred (1500), which enhances the sniper role in supporting combat operations and improves sniper survivability.”

Army budget documents also said the PSR would include a silencer, thermals, and other advanced optics that will “allow snipers, when supplemented with a clip-on image intensifier or thermal sensor system, to effectively engage enemy snipers, as well as crew-served and indirect fire weapons virtually undetected in any light condition.”

Between fiscal years 2022 and 2025, the Army expects to have 1,516 PSR systems in the field. By 2025, it expects to have an estimated 2,545 at an estimated total cost of $45.5 million.

It’s not just sniper rifles the Army is considering for upgrade. We noted last Sept that the service selected AAI Corporation Textron Systems, General Dynamics Ordnance, and Sig Sauer as the three finalists to test their next-generation assault rifles for the next 27 months.

The Army requested all three manufacturers to each supply 53 rifles, 43 automatic rifles, and 850,000 rounds of ammunition for the 27-month test that will conclude in 1H22 with a winning design.

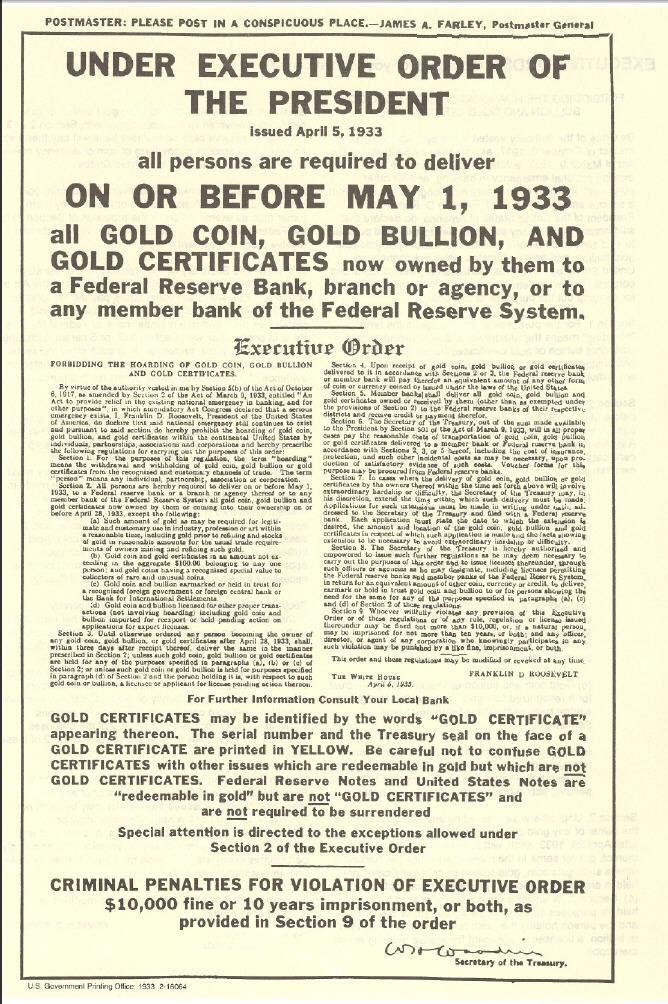

“We Have Never Seen This Before”: The Last Time The Market Did This, FDR Confiscated All The Gold

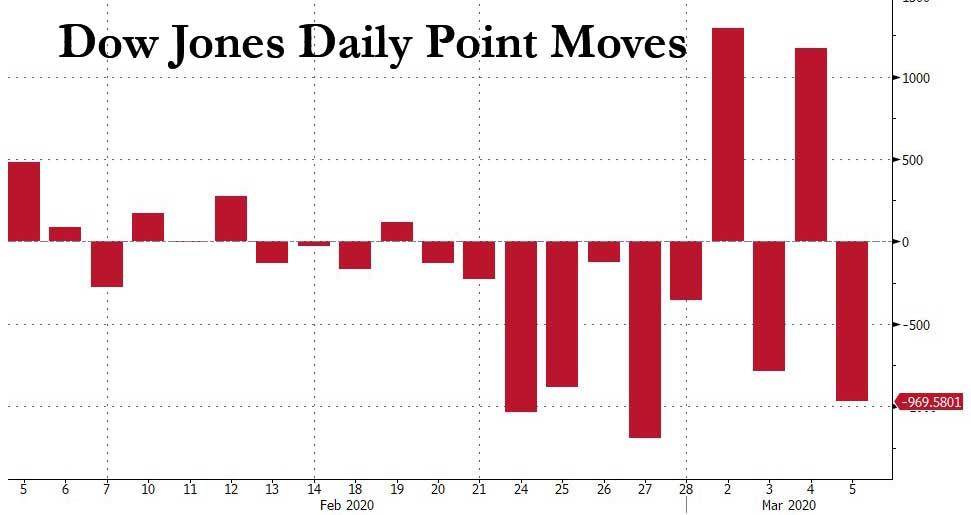

To say that moves in the US stock market have been erratic in the past two weeks would be a prodigious understatement: with the Dow Jones swinging by over 1,000 points on nearly 5 occasions in the past two weeks (today’s 970 point move would have been the fifth)…

… traders – holding on for dear life in a market rollercoaster the likes of which have not been seen in years – have given up trying to make sense, and are just praying they don’t lose all their money. “When you have a 4.5% up day in the market and a 2% down day – what does that mean?” Kathryn Kaminski of AlphaSimplex Group told Bloomberg. “It just means we don’t know what’s going on.”

And while futures continue to slide amid a surge in US coronavirus cases late on Thursday with over 2,000 New Yorkers now having self-quarantined, and emboldening what little is left of the bears – recall that heading into this week, single stock/ETF short interest was at all time lows…

… the bulls, who are rapidly losing faith that even the Fed can prop up this market, are pointing to the recent dramatic rebounds in the stocks most recently on Wednesday when the S&P500 surged back above 3,124 (it is now trading well below 2,990), yet which nobody can fully explain because even though there are several catalysts for the rebound that one could point to, historically speaking none of them are entirely satisfying as explanations, and as Nomura’s Masanari Takada writes in his daily Nomura quant note, “we suspect that more than a few investors (whether bearish or bullish) are feeling paralyzed in the face of such unusual swings in the market.”

However, it is what he says next that struck us as a stark admission that we have crossed the rubicon into a market that nobody, not even grizzled quant veterans, can explain: “We have also been at a loss to predict the market’s movements, and feel painfully reminded of the difficulties involved in drawing a story from nothing more than day-today changes in the market.”

And the punchline: “Even so, what is happening now is like nothing we have seen before.”

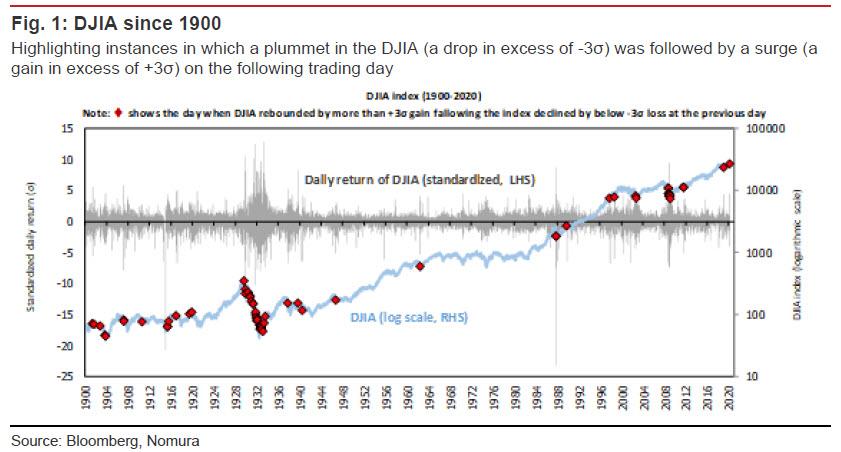

To be sure, here one can counter that maybe “we” simply haven’t been around long enough, and one just needs to extend the time horizon to observe a similar market to the one we have today. And so, indeed, without wandering too far off into the weeds, Nomura picks up on something we highlighted last week, namely that the market’s drawdown to a 10% correction from an all-time high was the fastest since just weeks before the great depression started…

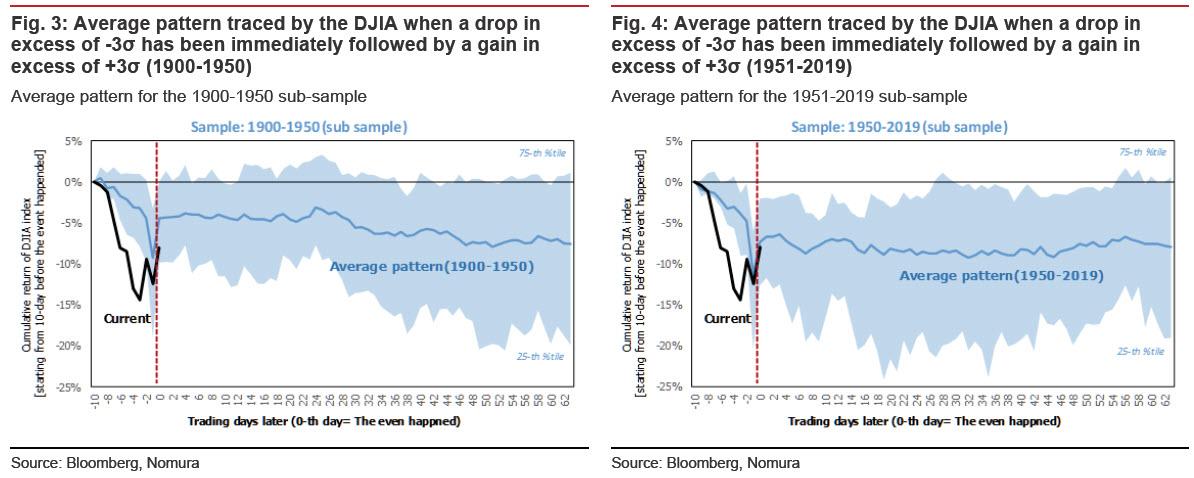

… and observes that there have been only 65 occasions since 1900 in which the DJIA has recorded a daily loss in excess of three standard deviations over the average daily return only to log a gain in excess of three standard deviations on the following trading day, and 70% of those occasions were concentrated in the 1900-1950 span, as happened this week on Tuesday and Wednesday (3 and 4 March), and 70% of those occasions were concentrated in the 1900-1950 span. In percentage terms, this is a frequency of just 0.21%.

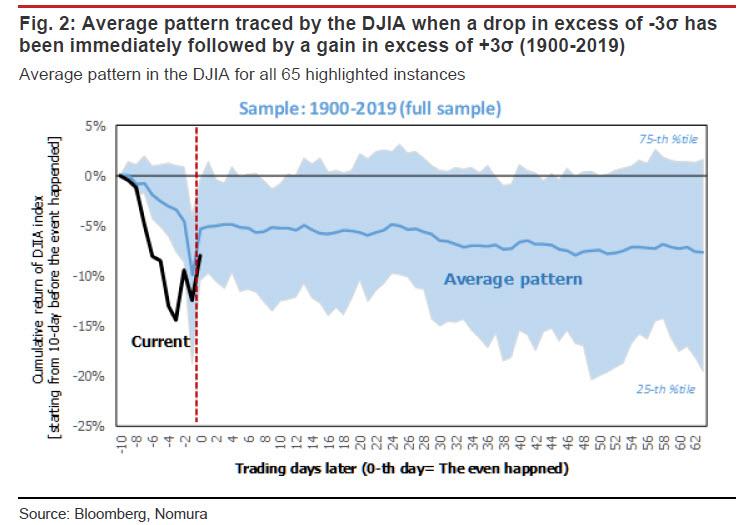

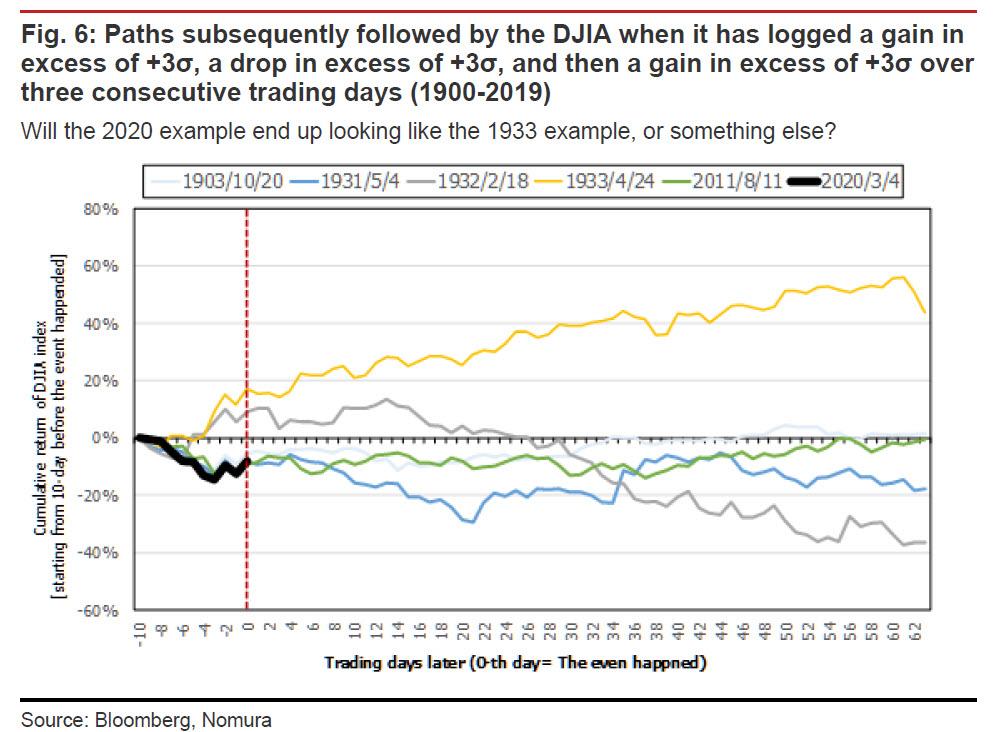

The last time this happened (14 January 2019), the market enjoyed a sustained rally, but the time prior to that (11 August 2011), no such rally ensued. Figure 2 is a plot of the average pattern followed by the market after each of these occasions, using the full sample of 65 instances between 1900 and 2019.

Yet while recent events are an extreme rarity across the entire historical spectrum, there is one distinct point in time when we observe cluster of activity similar to the furious market action noted in recent days (something tells us readers can already figure out which period we are talking about).

But before we get there, Takada writes that “it may be instructive to split this long span of time into two blocks (1900- 1950 and 1951-2019), as the impact of the Great Depression and the two world wars can be cordoned off in the 1900-1950 block. Even when back-testing the data in this fashion, however, we find no evidence that a gain in excess of three standard deviations on the day after a loss in excess of three standard deviations necessarily indicates that a bottom has been marked.

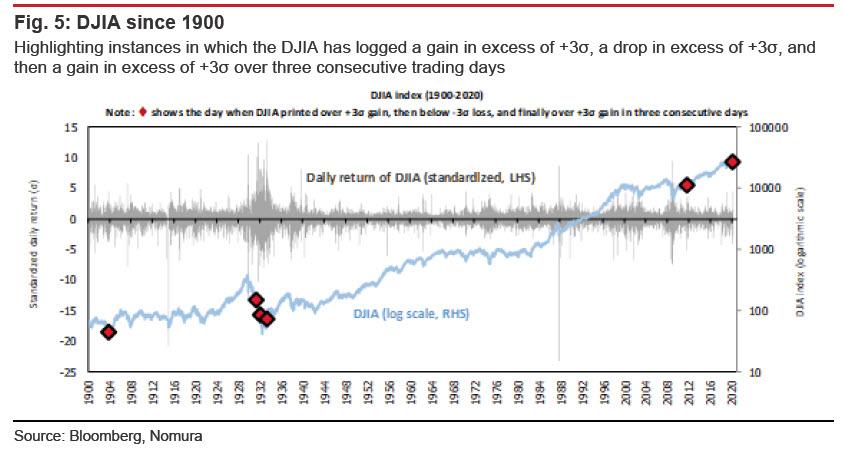

However, where the current market gyrations get even more interesting, is that this time the market logged a gain in excess of three standard deviations (over the average daily return), then a loss in excess of three standard deviations, and then a gain in excess of three standard deviations over the course of three consecutive trading days. This is only the sixth time this phenomenon has occurred since 1900.

And here is the stunning punchline: out of the five historical instances of this pattern (leaving out the present case for obvious reasons), Nomura finds that the only instance that was followed by a sustained market rally was that of April 1933, when the US abandoned the gold standard in the midst of the Great Depression.

Which makes sense: with stocks in freefall for years after the Great Depression started, what some argue stopped the collapse, was the signing of Executive Order 6102 by FDR, which not only ended the gold standard, but also confiscated all gold held by the public, and finally devalued the dollar against gold (Roosevelt changed the statutory price of gold from $20.67 to $35 per ounce, thereby devaluing the U.S. dollar by 40%). Such a historic fiat devaluation against gold was, to many historians, the necessary condition that finally let stocks find a bottom during the great depression, and started the long and painful recovery… the culminated with World War II.

Of course, conditions now are vastly different than they were at the time of each of the five prior instances, with the dollar long ago losing its convertibility into gold (thank Nixon for that) – yet while it would be next to impossible to confiscate gold, a massive dollar devaluation against the yellow metal may be just what the Fed is planning next (as Harley Bassman suggested in 2016) – so Nomura’s dissection of these market patterns is intended only as something that may be of interest from a technical standpoint. That said, this look back at 120 years of market history may be helpful to market observers attempting to assess the sustainability of the rally in US equities…

… and also to spark some thoughts about what events may be necessary to halt the ongoing collapse in risk assets. Our advice: for those who own gold, now is a good time to have an unfortunate boating accident.

Ilhan Omar Tweets “Abortion Is A Constitutional Right”, Accuses Two Supremes Of Being “Sexual Predators”

A day after Senate Minority Leader threatened the Supreme Court (and later apologized for his language), none other than Rep. Ilhan Omar, D-MN, took to Twitter with some very accusatory Tweets.

She suggested two SCOTUS Judges of being “accused sexual predators” and then stated that abortion was a Constitutional right.

Two accused sexual predators should not be deciding whether or not women have access to healthcare in this country. https://t.co/okJE85pwoN

“Two accused sexual predators should not be deciding whether or not women have access to healthcare in this country,” she said.

She is allegedly referring to unproven and false claims against Justices Brett Kavanaugh and Clarence Thomas. Her statements were met with backlash from people around the country.

There’s more evidence that you married your brother to commit immigration fraud than there is for your false claims about Supreme Court Justices.

Just look at some of the responses from people around the country to Omar’s Tweets below.

Ilhan, again, I’m asking you to direct me to Chapter and Verse in the U.S. Constitution, where the Founding Fathers wrote this so called “right” please show me so I can read it myself…..I’m waiting

“Right to life…” is in the Constitution, so, abortion is pretty much the OPPOSITE of constitutional.

Maybe a Civics class or two would help with your glaring lack of knowledge about our nation’s rights.

— Susan [Needs a literary agent] Bagwell (@SweetieWalker) March 4, 2020

I’ll mail you a copy of the Constitution since apparently you have never read it.

— Peni Basse ⭐️⭐️⭐️ Text TRUMP to 88022 (@pmbasse) March 5, 2020

I’m not sure where she read that it was a right but I know for certain that abortion is something our Founding Fathers didn’t include in the Constitution.

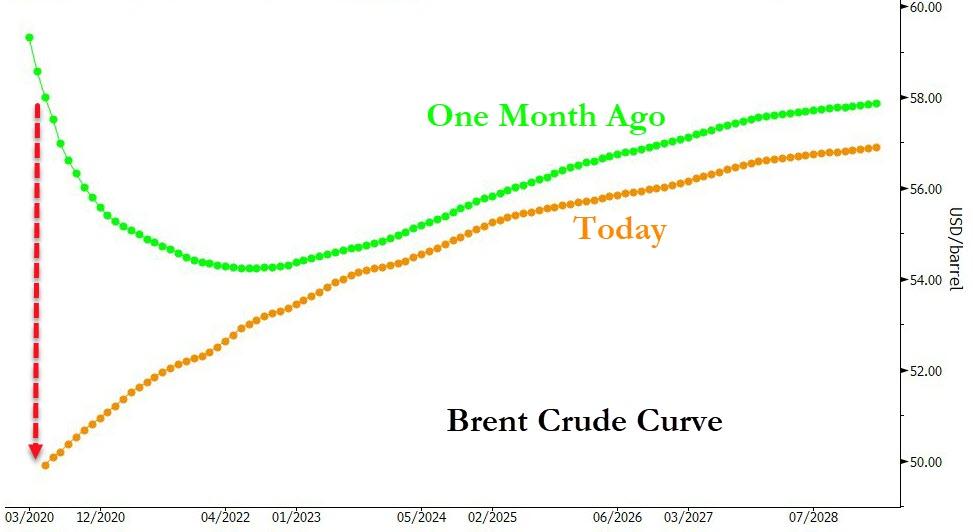

Oil prices have sold off sharply over the past month. Despite a series of bullish events – the killing of Qasem Soleimani by the US, Iran’s retaliation attack on US troops in Iraq, the shutdown of almost the entire Libyan production and the US’ tightening the screws on Venezuela by sanctioning Rosneft and potentially refusing to renew waivers to US companies stating in April – oil prices are now substantially lower than before these events. Brent front month prices peaked at $72/bbl in early January and are now at below $50/bbl (See Exhibit 1).

Moreover, by mid-January, the geopolitical tensions and supply losses had pushed the Brent curve into severe backwardation. June-December 2020 time-spreads for example traded as high as $4.50/bbl just one month ago, reflecting prolonged physical tightness. Those time-spreads are now in contango (see Exhibit 2).

This massive change in sentiment happened as the Coronavirus situation in China unfolded. Importantly, while we do expect a significant impact on Chinese oil demand from the massive travel restrictions in China, that alone would not warrant such a move in the curve in our view. Instead, we think the recent moves in oil prices is reflecting expectations for a significant slowdown in global economic growth. In fact, we think the oil price move is now pricing in a significant probability for a global recession in 2020.

Commodity markets are the only markets which currently reflecting this view. Equity markets, despite the recent sell-off, do not. Importantly, we believe commodity markets are still underpricing the risks to aggregate demand. The question is not longer whether the economic impact from the Coronavirus outbreak will be short-lived or whether it will be more pronounced. The question is whether the economic impact will be pronounced or catastrophic. In our view, energy markets are currently pricing in a pronounced impact with substantial fiscal and monetary stimulus down the road. There is substantial downside risk if that view turns out to be too optimistic.

That said, in either case we expect central banks to return to the 2008 playbook soon. Nominal interest rates will only decline from here and we are likely going to see a reacceleration in quantitative easing. However, in the catastrophic scenario, we believe central banks will quickly realize that the tools they have been using since 2008 will not get them very far this time. Hence, we would expect central banks to become more creative, by deploying something like “helicopter money”. This is not far-fetched. Hong Kong announced a few days ago that it would give every adult citizen HK$10’000, around $1300, in order to combat the economic fallout Coronavirus-crisis. We believe this would push gold prices sharply higher medium term.

How the Coronavirus outbreak changed the oil market outlook

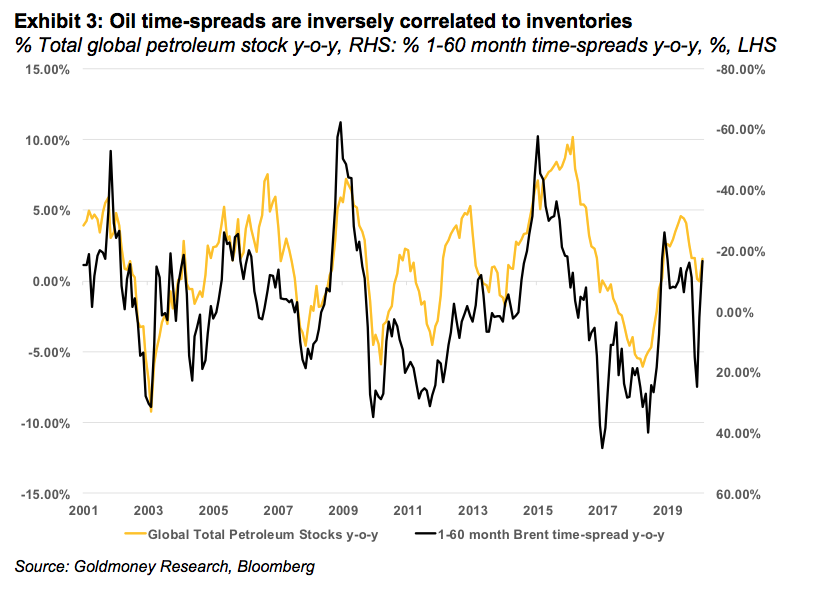

As we have highlighted before, there is a strong correlation between inventories and time-spreads (see Exhibit 3). When inventories are low, the oil curve tends to trade in backwardation (near-dated prices are above deferred prices). When inventories are high, the curve is in contango (near-dated prices are below deferred prices). The reason for this is that when inventories are low, consumers of a commodity are willing to pay a premium for immediate delivery rather than delivery at some point in the future. If oil (or any other commodity) is an input good in the production process, running out of the input good is much more costly than paying the premium as the alternative would be to shut down production. For example, jet fuel is an input good for an airline. Running out of jet fuel is very costly, hence, when inventories are generally low, airlines are willing to pay more for immediate jet fuel deliveries. The curve becomes backwardated. Conversely, when inventories are high, there is no risk of running out of oil, and storing oil is expensive (storage costs, insurance costs, time value of money), hence, consumers would rather have delivery in the future, and the curve is in contango.

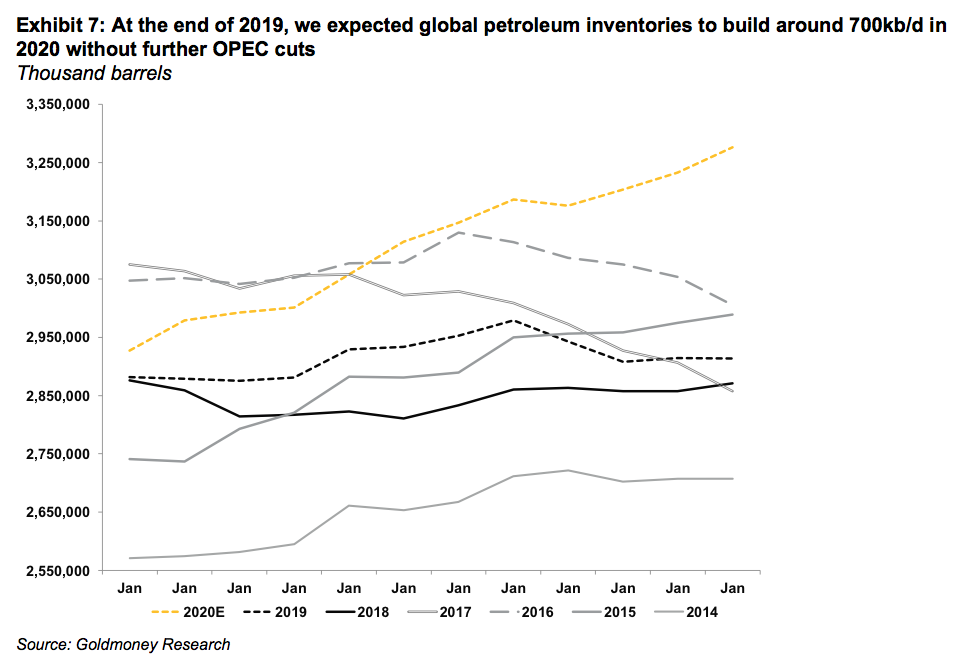

The outlook at the end of 2019

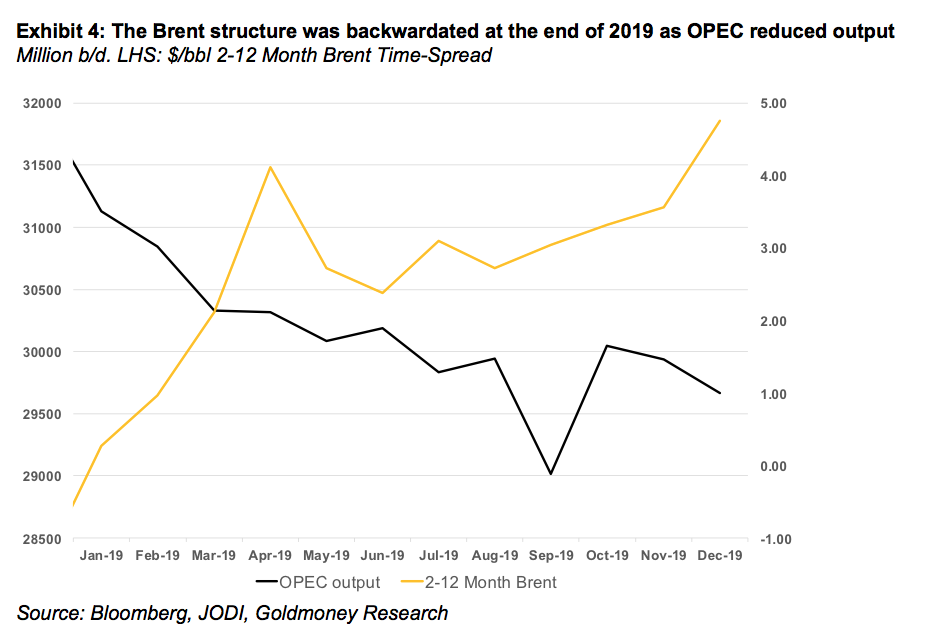

We ended 2019 with relatively low global petroleum inventories, and hence, the Brent curve was backwardated. The low inventory situation came amidst strong US shale production growth and weak global demand. The reason for this is that OPEC production was lower by close to 2mb/d year-over-year on both voluntary (core OPEC+) and involuntary (Iran, Venezuela) production cuts (see Exhibit 4).

However, we expected global balances to change going forward. By the end of 2019, we predicted the global oil balance to be oversupplied by roughly 0.7mb/d in 2020 and by about 1mb/d in 1H2020. Consequently, we expected the curve to become less backwardated and eventually to end up in contango, accompanied by lower front month prices.

Our bearish 2020 balance was driven mostly by strong production forecasts:

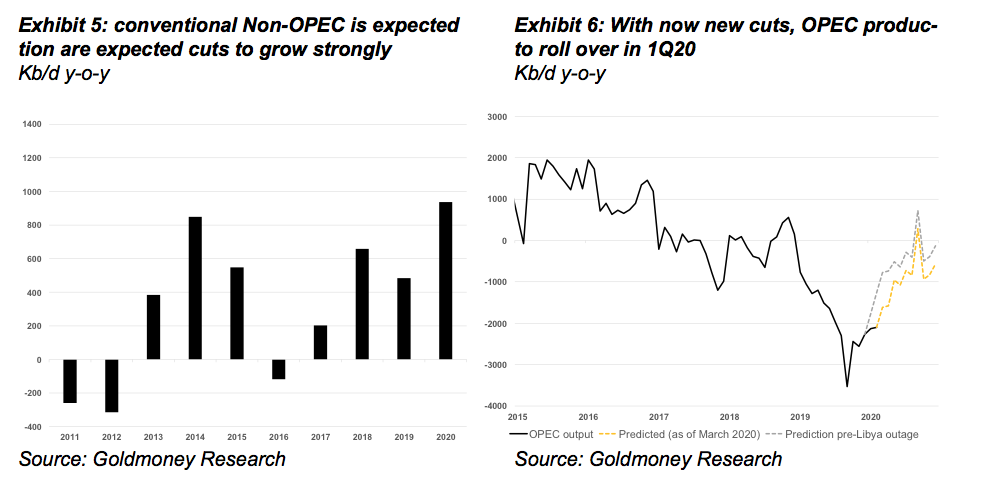

Conventional non-OPEC production was (and still is) expected to grow strongly in 2020 by about 1 mb/d with several major new fields coming online and ramping up.

US shale production, while not growing as quickly as in 2019, was still expected to grow at around 1mb/d (including natural gas liquids NGLs).

On net, we expected non-OPEC production to grow by 2mb/d year-over-year

This strong growth was expected to offset declines of 0.5mb/d year-over-year in OPEC production on the back of the new production cuts decided in December 2019 plus reduced output from Libya (we assume not all Libyan production will remain offline in 2020). The voluntary and involuntary production cuts from early 2019, however, would no longer show up as year-over-year declines.

On net, at the end of 2019 we expected global oil production to grow by around 1.6mb/d in 2020.

These supply growth expectations exceeded demand growth expectations in 2020. Most forecasters, including the International Energy Agency (IEA), predicted demand growth at slightly over 1mb/d. This reflected an expected recovery in global economic growth from 3% in 2019 to 3.4% in 2020. We had a more pessimistic outlook on demand growth of around 800-900kb/d because our calculation showed that demand growth was slowing down sharply in 2H2019, and thus, a minor recovery in economic growth would unlikely lead to the demand growth figures we had been accustomed to over the past years. But even with the more optimistic outlook by the IEA, the global oil balance was poised to be oversupplied.

On net, we expected global petroleum inventories to build by close to 700kb/d in 2020 or about 230 million barrels. The bearish balances where mostly in 1H20 with an oversupply of >1mb/d, while it looked more neutral for the remainder of the year. Our inventory forecast, thus, implied weaker time-spreads and consequently, lower prices in 1H2020.

Shutting off Libyan exports

However, this bearish outlook was suddenly challenged in early January. Firstly, it was reported that Qasem Soleimani, an Iranian General of the revolutionary guards and commander of its Quds Force, was killed in an US airstrike in Iraq. Soleimani was considered the second most powerful man in Iran, in charge of all military operations outside Iran. The news sent oil prices sharply higher as the market began to worry about an escalation of this conflict in the region. Iran had repeatedly threatened to disrupt oil shipments in the Strait of Hormuz, through which about 1/3 of all seaborne oil flows. A few days later, Iran attacked a US base in Iraq with missiles in retribution. The US quickly announced that there weren’t any casualties among the US troops. The market interpreted that the Iranian retribution was an act of saving face rather than the first strike in a prolonged conflict, and prices moved sharply lower on the same day (see Exhibit 8). As suddenly as this conflict emerged, as quickly it was over, without any real impact on oil supplies.

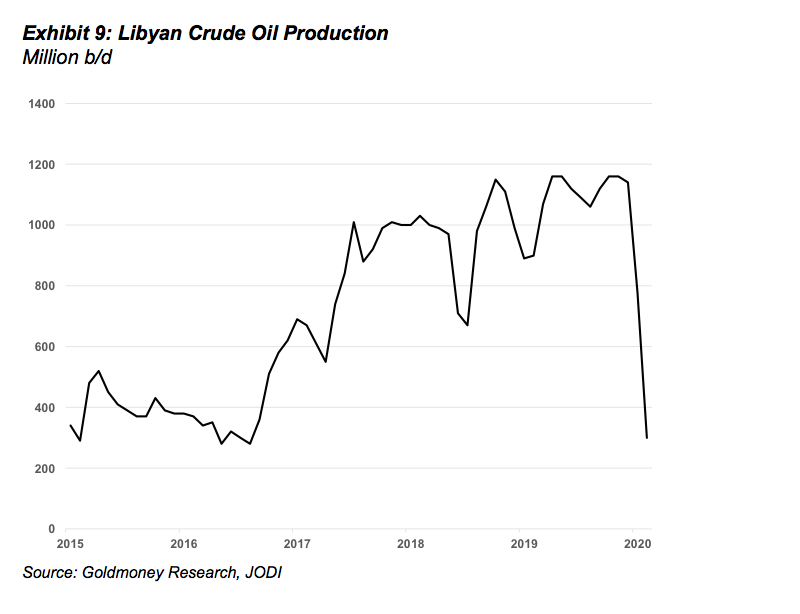

This changed quickly when on January 17, 2020, forces close to Libyan General Haftar closed almost all of Libya’s export ports. Prior to that, Libya had produced around 1.2mb/d of high-quality light sweet crude oil (see Exhibit 9). With the exports gone, the expected global oversupply in 1H2020 almost entirely vanished and 2H2020 now looked quite bullish. At the time, it was quite unclear how long the exports would remain shut-in.

Historically, exports resumed when demands from local groups that blocked exports were met. But this time, the situation is much more complex than just meeting financial demands of a few local interest groups. General Haftar seems to be using the exports as a bargaining chip in the ongoing international peace negotiations. He also seems to have the backing of local tribe leaders (who blocked the ports), which have been complaining about the unfair – or lack of – distribution of the oil revenues for years. Thus, the likelihood for a quick resumption of exports looked low in January (This view has since turned out to be correct. Six weeks into the disruption and a peaceful and quick resolution of the conflict seem very unlikely).

As oil exports could potentially remain offline for months, the Libyan situation turned an oversupply to a shortage overnight. Consequentially, oil prices rallied on these news and time-spreads became more steeply backwardated.

The Coronavirus outbreak starts impacting demand

This bullishness didn’t last long. Since oil prices peaked on the back of the Libyan news six weeks ago, oil prices sold off more than $20/bbl. Moreover, the Brent forward curve went from steep backwardation to contango. This sell-off is entirely driven by the outbreak of the Coronavirus in China. While there is a significant immediate impact on oil demand from the draconian measures taken by the Chinese government to contain the virus, we think the market is now pricing in wider demand destruction on the back of a global economic slowdown or possibly a global recession.

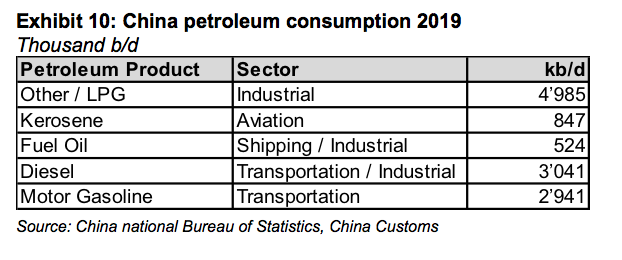

How much is oil demand affected in China? Chinese petroleum demand is roughly 13 mb/d, making it the second largest consumer in the world after the United States (see Exhibit 10). The below table show the breakdown of consumption by product:

We don’t have a lot of information out of China that would allow to directly calculate by how much oil demand is affected. The information we have suggests that air and rail travel and even car travel has decreased sharply, with some cities showing hardly any congestion in the streets. Thus, the hit from the transportation demand alone is most likely 2mb/d or even more as many international flights to and from China are suspended.

On top of that, manufacturing has come to an almost standstill in about 70% of the country. Over the past week, we saw some companies resuming operation, but only at a minority of plants in some regions. A lot of workers who came home from Lunar New Year are still required to stay at home. We estimate the total demand impact currently to be around 3mb/d. While this seems a lot, in our view, this alone cannot explain the dramatic move from backwardation to contango and the $20/bbl price decline in less than 4 weeks. We think the oil market is pricing in a sustained hit to global economic growth, to the point where it’s pricing in a significant probability of a global recession.

How big does the loss in oil demand have to be to warrant such a shift in the curve?

Our inventory-to-time-spread model allows us to back out how much the market is pricing in in terms of inventory builds. Prior to the outbreak of the Coronavirus, prompt prices traded 20% above longer-dated prices (5-year forward). Currently, prompt prices are trading 7% below the forward. In our time-spread to inventory model, such a move is equivalent to a 280-million-barrel build in global inventories. With 3mb/d of demand shut in, it would still take >3 full months of total Chinese lockdown in order to get to such a number, and that requires assuming that once the virus is contained, Chinese companies are not making up any of the lost production (and in turn oil demand). Hence, in our view, the shift in the Brent term structure is not simply reflecting lost Chinese demand, it is reflecting a sharp deterioration in global economic growth.

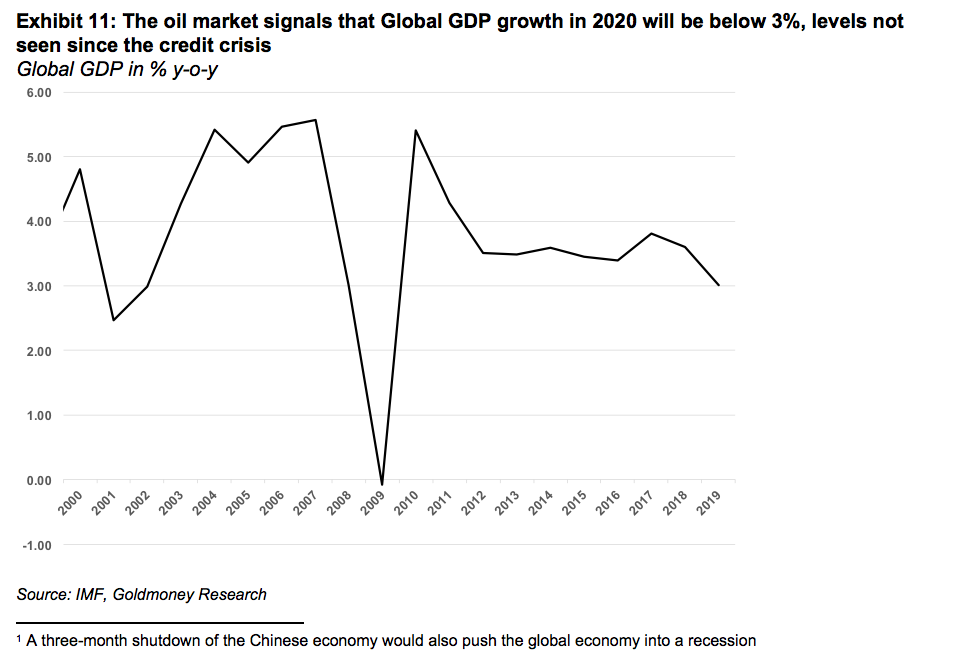

Assuming that lost Chinese demand is closer to 100 million barrels, 160 million barrels of inventory build (450kb/d) would have to come from lower economic growth outside of China. Our global demand model shows that a 1% change in global GDP accounts for 1 million b/d of oil demand. Thus, the market is now pricing in a 0.5% slowdown in global GDP on top of the slowdown in China. In other words, the oil market is pricing in global economic growth well under 3%. According to the IMF, the last time this has happened was during the finical crisis in 2009. Before that, one has to go back to the bursting of the dot.com bubble in 2002 to get to similar numbers.

Interestingly, commodity markets – oil and copper but also LNG and freight – are the only markets that seem to reflect this worldview. Equity markets on the other hand were making new highs even as the viral outbreak unfolded in China. While equities corrected sharply last week, equity markets have declined a lot less than commodities.

We may have already been in a recession before the Coronavirus outbreak

It may come as a surprise, but nobody really has a good handle on global oil demand. One would think that – given the importance of oil for the global economy – there would real-time in-depth data for oil demand across the globe. In reality, all demand data is of very poor quality, reported with a 2-3-month lag and very limited in scope (We only have data for OECD countries, which account for less than half of global demand). Furthermore, the data reported does not actually reflect what real demand is, it’s so called implied demand.

Meaning, the OECD member countries are obliged to report production of oil and petroleum products, changes in stocks as well as imports and exports. From those data points, implied demand is calculated. How much is actually consumed by cars, trucks, jets and heating boilers is unknown. In fact, for most regions, we don’t even know how much gasoline is sold at petrol stations. While some OECD countries report weekly implied demand data, it often comes with heavy revisions a few months later, to the extent that the weekly demand data reports are ignored by the oil market (the market focuses almost entirely on the inventory reports, as those are believed to be the least distorted). Hence, the best estimate we have for OECD demand is typically a few months old, and even that data often tends to be revised years later.

For non-OECD countries, demand data is even harder to obtain. Most non-OECD countries don’t report any data at all. Some do report some data, like China, but part of the data infers such strange results, that calculating implied demand becomes futile. Hence, non-OECD demand is typically just estimated based on economic growth projections. Hence, the global oil demand data that is typically reported and cited is simply a medley of notoriously bad OECD implied demand data and even less reliable estimates based on GDP predictions.

In addition, oil agencies such as the IEA typically publish balances that don’t balance. Meaning, supply minus demand does not equal changes in inventories on a global level. In other words, The IEA does calculate demand as implied demand bottom up for each country but applying the same data for a top down implied demand calculation for the world, leaves a huge error term. The reason typically provided for this error term, is that changes in non-OECD inventories are not part of the balance. However, we do have some inventory data from larger non-OECD economies, and taking those into account does not typically improve those balances, it often makes them worse.

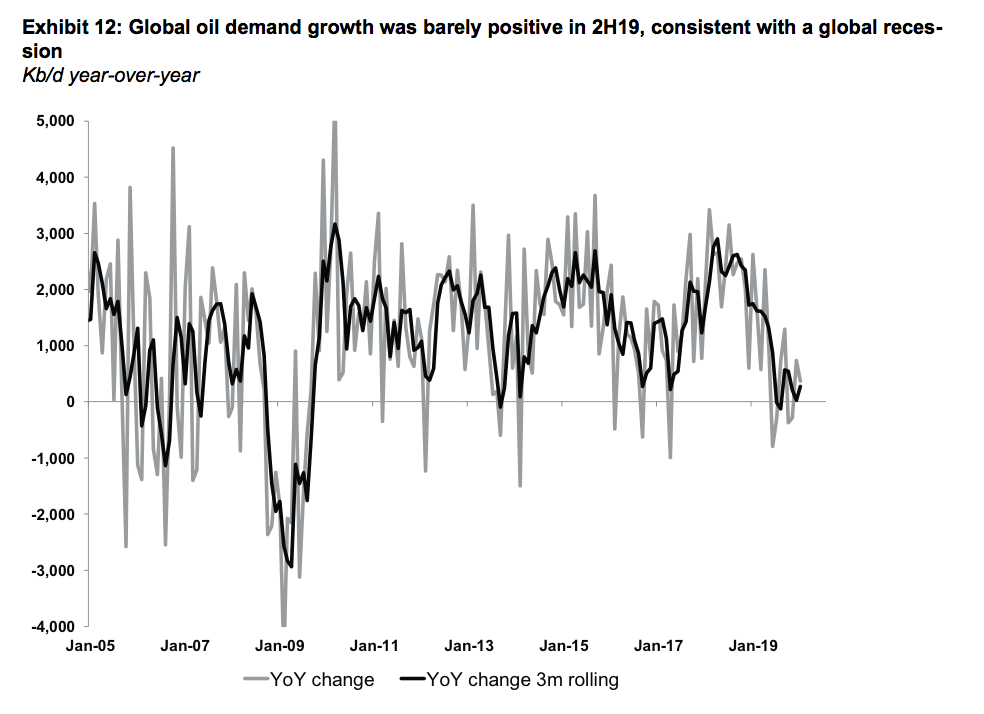

Thus, when trying to get a glimpse of the state of global demand, we calculate top-down implied demand. Meaning, we aggregate changes in global inventories, including oil at sea and add supply, which should add up to global demand. Importantly, our implied demand number for 2019 shows very weak demand of just 0.7mb/d year-over-year. This is below of what most forecast agencies show. Moreover, while implied demand was still healthy in 1H2019, it slowed down dramatically in 2H2019.

The latest numbers suggest that global demand growth in 2H19 was barely positive year-over-year. This would be consistent with global GDP growth at just 2%. While data for the most recent month will likely see some revisions, the latest revision have shown larger inventory builds than previously reported. We see indications for economic weakness in other corners of the petroleum markets as well. Demand from the chemical sector, for example, often an early warning sign for economic slowdown, was very weak in recent months.

Is the oil market bearish enough?

The oil market is one of the few markets that predicts a larger global economic impact from the virus outbreak. However, in our view, what is priced into the current forward curve is still too optimistic. The current 0.5% impact is the bare minimum we expect as a potential fallout on the global economy. This would require:

the draconian measured in China to be lifted over the coming weeks and business going back to normal (with heavy fiscal stimulus in 2H20),

Other governments abstaining from any comparable measures (no wide spread travel bans and lock-downs)

Companies outside China abstaining to close plants and offices and manage to remain productive

The general population largely accepting that they may get the virus eventually and going their business as usual

This scenario seems increasingly unlikely. France reported last week that tourism activity was down 30-40%. By the time this number was reported, the country had only 12 reported cases, so France can’t have been particularly affected by travel cancellations. We can, thus, assume that traveling activity across the world is now heavily impacted. Italy has over 2000 cases now as the virus is spreading in the northern part of the country. South Korea is closing plants and Japan has announced to close all schools until spring break. Global supply chains will no longer be impacted just because Chinese companies can’t deliver, but increasingly because manufacturers from other nations are affected as well. While supply is affected first, we expect demand to suffer going forward. Layoffs mean people will have less disposable income. The hospitality sector will be hit hard, retail as well. Car sales in China have collapsed and there are early indicators that car sales are already slowing down in Europe. We believe that – despite the sell-off – barely any of this to be currently priced into oil markets, still less in other assets such as equities.

Conclusion

Markets became really excited about some better PMI data prior to the Coronavirus outbreak. The IMF predicted a reacceleration in growth from 3% in 2019 to 3.4%. In all likelihood, the impact of the Coronavirus will bring 2020 growth well below 3% even in the “contained” scenario with minimal knock-on effects on other economies, either through supply chain effects or reduced demand for goods (commodities) from China.

However, if economic activity was in fact already much weaker in 2H19 than what is generally assumed, the Coronavirus may be just what it takes to finally push the global economy into a deeper recession.

In such a scenario, we would expect equities to adjust to reality over the coming weeks.

At the same time, this should be very positive for gold. Despite the near-term deflationary effects from lower commodity prices, we expect central banks to quickly return to the financial crisis playbook by slashing rates and deploying some form of Quantitative Easing (QE) or more direct form of stimulation (helicopter money). This would propel gold prices sharply higher over the medium term.

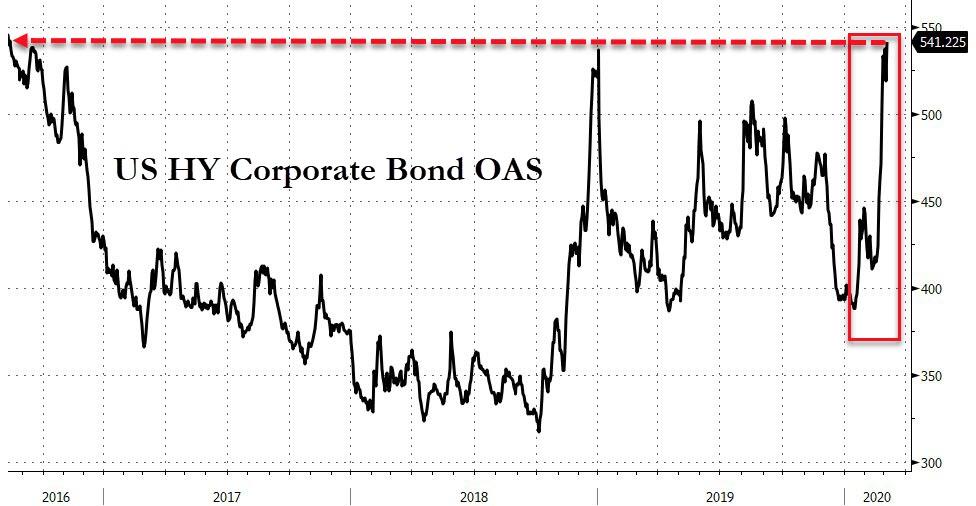

“Gold Is Going A Lot Higher” – DoubleLine’s Gundlach Warns Of “Seizure In The Corporate Bond Market”

“The bond market is rallying because The Fed has reacted the seizure in the corporate bond market – which is not getting enough attention.”

That was the sentence that sparked a chin hitting the table moment for anyone watching DoubleLine CEO’s Jeff Gundlach being interviewed on CNBC today. Until now, amid all this equity market carnage, various talking heads – who clearly are not ‘in’ the bond market – have confidently claimed ‘yeah, but it’s different this time, there’s loads of liquidity and credit markets are not showing any signs of pain’…Well that all changed today as the world was told the truth.

Credit spreads have exploded wider in recent days… “the junk bond market is widening out massively…”

Gundlach noted that Powell’s background in the private equity world – rather than academic economist land – has meant that his reaction function is driven by problems in the corporate bond market as “this will be problematic for the buyback aspect of the stock market.”

The Fed cut rates, he added, “in reaction to even the investment being shutdown for 7 business days.“

So the DoubleLine CEO said that Powell “cutting rates was justified” but didn’t like the way it was done as it signaled “panic.”

The reason for his disdain is clear:

“The Fed in their most recent press conference, took a victory lap, talking about how they had finally reached a stable place in policy and that they could be on hold for the foreseeable future, maybe even the entire world. That we are in a good place. That policy rates were appropriate. And I don’t know, I thought it was a little bit of hubris at this time.”

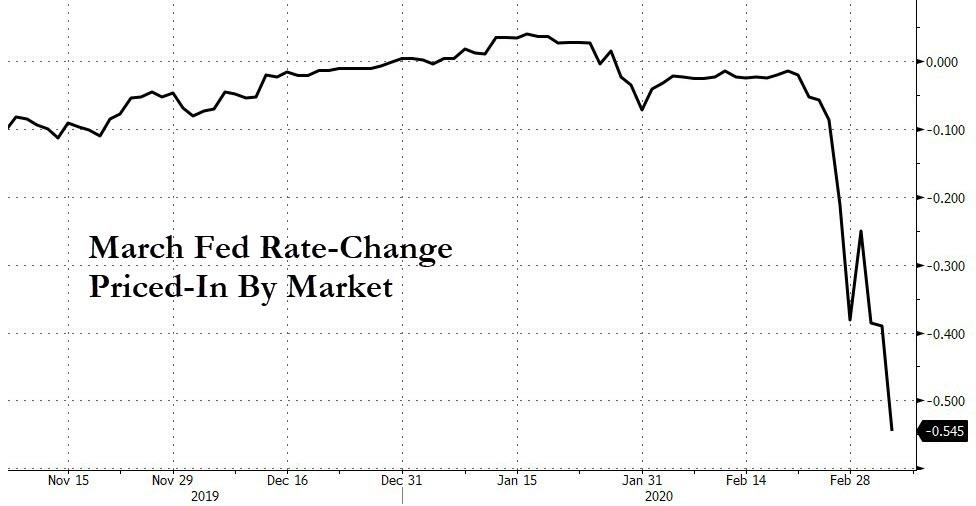

And reminds watchers that historically, “when The Fed has cut 50bps in an emergency intra-meeting such as this, they typically cut pretty quickly after once again.”

And sure enough the market is already pricing in another 50bps cut at the March meeting…

However, unlike Guggeheim’s Scott Minerd – who sees 10Y yields at 25bps – Gundlach believes “we are pretty near the low right now…maybe we get to 80 basis points on the ten year.”

Well we are at 85bps now…

However, while his view is that long-rates are starting to floor, he notes that “short rates are definitely going lower. There is absolutely no upward pressure on short rates.”

Gundlach agrees with Jim Bianco that short-rates are going back to zero, but stopped short of expectations for negative rates:

“I think Jay Powell understands that negative rates are fatal to global financial system. If we go to negative rates, there will be capital destruction en masse.”

But more easing is coming, as Gundlach reflects on those calling for v-shaped recoveries:

“I think it is foolhardy to think anything other than this [pandemic] is going to take a major hit to short-term economic growth.”

His perspective on the financial and societal impact of the Covid-19 pandemic is refreshingly honest on CNBC:

“…obviously, the airlines are in free fall for good reason. And small business activity is going to contract. Maybe grocery store sales will go up on a short-term spike. But all other kind of social activity is grinding to a standstill.”

Warning that “the two sectors that are just falling knives are financials and transports. And I don’t see anything that’s going the reverse that until we get through the other side this valley of this sort of travel shutdown.”

Finally, Gundlach ends on an even more ominous note:

“…the President and the physicians, on top of this coronavirus situation, and they are saying that they might have a vaccine in like a year, year and a half.

So, nobody knows what is happening here. And so, caution is appropriate.“

So no more buy the dip?

As former Dallas Fed President Richard Fisher noted, that means a generation of money-managers are about to losae their security blankets!

And that’s why Gundlach is long gold:

“I turned bullish on gold in the summer of 2018 on my Total Return webcast when it was at 1190. And it just seems to me, as I talked about my Just Markets webcast, which is up on DoubleLine.com on a replay, that the dollar is going to get weaker.

And the dollar getting weaker seems to be a policy. And the Fed cutting rates, slashing rates is clearly going to be dollar negative. And that means that gold is going to go higher.“

The royal family in the UK is having its very foundations shaken by both the controversial departure of Prince Harry and Meghan and now startling new revelations which compromise Prince Andrew even further, since his “car crash” interview with BBC, over his alleged relationship with a sex-trafficked child prostitute working for Jeffrey Epstein.

Andrew had always denied any link whatsoever with the then named Virginia Roberts who was in just 17 when the main allegation – that Epstein flew her to London in March 2001 for her to have sex with the British royal – was brought against him. Central to that allegation was a photo taken by Ghislaine Maxwell in her London home on the same night in question which Andrew claims is fake.

Roberts claims that she was forced into the act by Epstein and Maxwell and has gone on the record to talk about the intimate details of the incident, but her case have been light on witnesses or those who can corroborate her allegations. Until now.

Her shocking claims are that Maxwell and Epstein were running a high class sex trafficking organisation which targeted powerful, influential individuals, which some might speculate was part of a Mossad run ‘honey trap’ – a blackmail ring which made Epstein hugely powerful and in a position to ask from the same targets favours, or for highly valuable information which could support its agenda.

In just a few days in mid February, Prince Andrew already feeble case which he was clinging on to – that he had no link whatsoever with Roberts – was shattered though, which in itself raises a number of questions over who is protecting the British royal. And at what price?

First off came the accusation by a palace security guard in London who has challenged Andrew’s claim to be in another part of the country (far from the capital) on the night of the alleged sexual incident. According to the security officer, Andrew returned to Buckingham Palace in the early hours and shouted at the top of his voice at the palace gates for them to be opened.

But far more damning is the testimony of a telecoms man who was employed by Epstein on his private Caribbean island who a British tabloid interviewed days later, who identifies both Prince Andrew and Roberts being intimate with one another and how she appeared to be like a child “hiding behind an adult” sometime around 2001 or thereafter.

There is nothing quite so powerful in a legal case which Roberts (now Giuffre) is preparing than eye witnesses who can stand in the witness box. And the emergence of Steve Scully will be seen as a massive blow to Andrew’s claims now. The FBI too will find it hard to ignore Scully’s allegations.

Or will it?

The notion supported by conspiracy theorists that Andrew is somehow being protected just got ratcheted up ten fold. The FBI interviewed Scully earlier but Prince Andrew’s name, curiously, was never mentioned.

Given that Epstein and Maxwell were almost certainly being bankrolled by Mossad and that Trump’s relations with Israel are unfathomable one has to ask if there is a deliberate plot in the US to not take Virginia Giuffre’s allegations seriously. Add to that Britain and the US forging stronger links post Brexit with a new trade deal in the air and Trump’s double state visit to the Queen and a reasonable question would be is there a ruse on both sides of the Atlantic to keep Andrew out of an FBI investigation? Or perhaps more worryingly, is Andrew part of a bargaining chip from Trump’s side to nail a more advantageous trade deal which benefits America more, given Trump’s style of blackmailing those he wished to secure deals with, which we have seen with other countries he tackles?

It is hard to imagine how many days left Andrew has as a British royal and a possible heir to the throne, given how tough the Queen was with Meghan and Harry, both stripped of their ‘royal’ titles as they bolt to the US to shamelessly cash in their fame. Andrew may well have to flee the UK and find a Caribbean island himself to escape the reach of both the FBI and Giuffre’s lawyers. But for the moment, he seems secure in the UK, protected by that oh-so special relationship between Trump and Buckingham palace.