Berkshire Says Its Annual Meeting Is A Go For May 2, Despite Coronavirus Outbreak

Berkshire’s Warren Buffett has said that the company’s annual shareholder meeting, scheduled for May 2, is going to take place as planned, despite the coronavirus outbreak in the U.S.

Some of the surrounding events around the meeting may wind up being curtailed, however.

Berkshire posted a brief announcement on its website early this week that simply says:

The Berkshire Hathaway Annual Shareholders Meeting will be held on May 2, 2020 irrespective of conditions at that time. The scope of the meeting and associated activities may be modified by circumstances at the time, but we have no present plans to do so.

Buffett’s shareholder meeting is one of the largest corporate gatherings in America, according to Reuters. And what better way to show your “buy stocks forever” and “America (and its Central Bankers) will prevail” sentiment than to ignore the science behind the coronavirus and get 40,000 or more people into the same meeting rooms and events in Omaha over a three day weekend.

The events include not only the meeting, but a picnic, a 5K run and even a dinner for select attendees at a nearby steakhouse.

For those not interested in contracting coronavirus, the meeting will also be livestreamed by Yahoo Finance, who will allow viewers to watch Buffett’s top lieutenant, Charlie Munger, field incoming questions for hours.

Buffett’s recommendation flies in the face of many U.S. companies that are now restricting travel for employees in response to the outbreak. Buffett said that he “expected” that many of the Chinese visitors who typically make their way to Omaha won’t attend this year.

Beijing Ditan Hospital affiliated to the Capital Medical University said on March 4 that the first patient with novel coronavirus pneumonia complicated with encephalitis was discharged from the hospital on February 25.

Liu Jingyuan, director of the ICU at the Hospital, presided over the treatment of the patient. He reminded that patients with conscious disturbances must consider the possibility that the virus may attack the central nervous system.

At present, patients with new type of coronavirus pneumonia can be combined with multiple organ damages such as severe respiratory distress syndrome (ARDS), myocardial damage, abnormal coagulation function, kidney damage, liver damage, etc. However, no central nervous system involvement has been reported. The case report is the first in the world.

Previous studies on SARS (Severe Acute Respiratory Syndrome) and MERS (Middle East Respiratory Syndrome) have also shown that the coronaviruses that cause these two diseases also cause cases of central nervous system damage.

According to the introduction of Beijing Ditan Hospital, two suspected cases of new-type coronavirus pneumonia have been treated since January 12 this year (confirmed on January 20). As of 7:00 on March 4, the hospital has accumulatively received 150 patients with new-type coronavirus pneumonia, of which the above patient is the only patient with new type of coronavirus pneumonia and encephalitis.

The 56-year-old patient was admitted to the hospital on January 24 with new coronavirus pneumonia, critical illness, and respiratory failure. After admission, he was given a combination of interferon nebulization, antiviral treatment, prevention of bacterial infection, and TCM syndrome differentiation. No improvement, high fever, fatigue, and dyspnea gradually increased.

On January 27 (10th day of onset), a chest CT showed that the range of ground-glass density in both lungs was enlarged, and some of them were consolidating. Short-term nasal high-flow oxygen inhalation, no relief in breathing distress, irritability, breathing 50 breaths per minute, partial oxygen pressure of 85%, intubation in the ICU, mechanical ventilation in accordance with the principle of ARDS breathing ventilation.

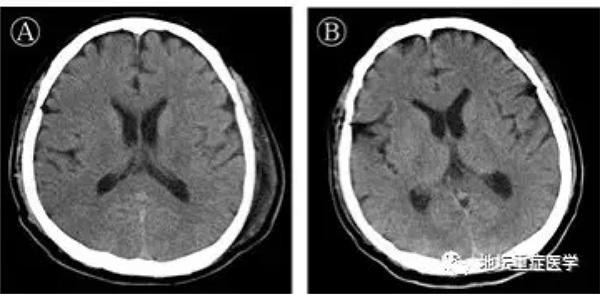

After 96 hours of treatment (day 14 of the onset), the patient developed frequent twitching of the maxillofacial and mouth angles with persistent hiccups.

On examination, the doctor found positive neck resistance, bilateral pupils and other large contours, sluggish light reflection, increased limb muscle tension, bilateral knee reflexes, bilateral Pap sign and ankle clonus, and no intracranial CT scan. Abnormal, the cerebrospinal fluid pressure was greater than 330mmH2O, the appearance of the cerebrospinal fluid was colorless and clear, and the biochemical test was normal.

Beijing Ditan Hospital’s Department of Critical Medicine, Laboratory Medicine, and the China Centers for Disease Control and Prevention’s Infectious Diseases Joint Working Group performed metagenome second-generation sequencing of the collected cerebrospinal fluid specimens and identified possible infectious pathogens. Other pathogens were excluded and a new coronavirus was obtained. Genomic sequence.

Gene sequencing confirmed the existence of a new coronavirus in the cerebrospinal fluid and clinical diagnosis of viral encephalitis.

Subsequently, the medical staff treated the patients with viral encephalitis after 14 days of mechanical ventilation and mannitol to control intracranial pressure, midazolam to control convulsions, gamma globulin, and methylprednisolone anti-inflammatory treatment, and observed the patient’s lung disease imaging gradually. Improved, neurological symptoms disappeared.

On February 10 (day 24 of the onset of illness), the trachea was intubated and the nasal cannula was given oxygen after fully assessing the patient’s respiratory and neural function. On February 18 (the 32nd day after the onset of illness), he was transferred out of the intensive care unit and continued to receive treatment in the new coronavirus ward.

Liu Jingyuan reminded that in clinical observation, there were many cases of cervical resistance, positive pathological signs, sudden disturbance of consciousness and even coma.

He said that in the face of such patients, it is necessary to be vigilant to the new type of coronavirus infection that can affect the central nervous system, timely conduct relevant examinations such as cerebrospinal fluid, and improve the work on SARS-CoV-2 nucleic acid and gene sequencing of cerebrospinal fluid in order to better understand COVID-19. Explore and actively deal with related neurological complications, thereby further reducing the mortality of critically ill patients.

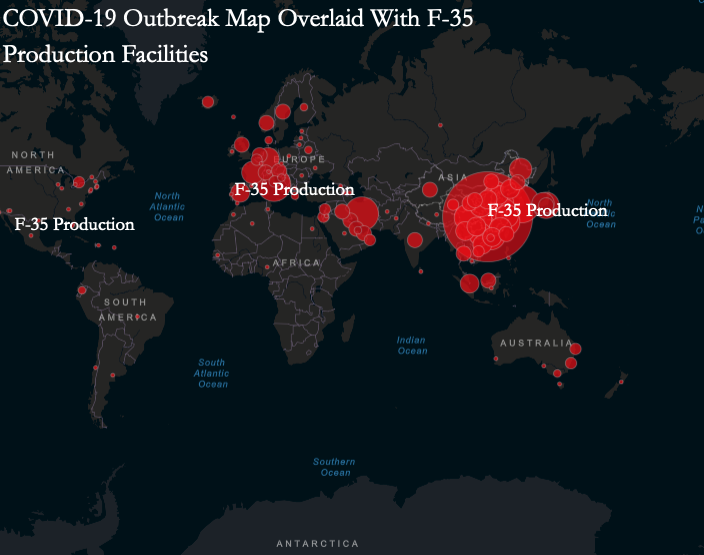

Operations Suspended At F-35 Stealth Jet Factory In Japan Due To Virus Fears

America’s F-35 stealth aircraft factory in Japan shuttered operations for a week due to new concerns over the Covid-19 outbreak, reported Defense News.

This prompted the closure of the F-35 factory in Japan, Ellen Lord, the undersecretary of defense for acquisition and sustainment, told reporters on Wednesday. She said the F-35’s global supply chain has yet to be impacted by the virus.

“In Japan, I believe they shut down the Final Assembly and Check-Out (FACO) for a week,” Lord said.

While much of the F-35 is produced at Lockheed Martin’s factory in Ft. Worth, Texas, Japan has managed to become integrated into the production of the fifth-generation jet.

Still, “right now, it doesn’t look like it is affecting deliveries” of the F-35, Lord said. “Right now, we have not seen any effects.”

With the virus spreading worldwide, South Korea, Italy, Iran, and other countries in Europe, have been hard hit by the virus. Another F-35 factory in Italy has taken precautions to minimize virus spreading, she added.

She said at the F-35 plant in Italy, “Lockheed has directed their employees to work from home.”

Lord said the Assistant Secretary of Defense for Homeland Defense and Global Security has been monitoring the global supply chain of the F-35 and potential virus impacts, including “scenario planning” of supply chain disruptions.

Defense News notes the F-35 program is “the most globally integrated supply chain in military equipment history.”

“Combating the Coronavirus remains a top priority for the department, and Secretary Esper meets weekly with senior leaders to discuss how we’re taking care of our men and women in uniform around the world,” said DoD spokesman Lt. Col. Mike Andrews. “The department remains fully engaged with the defense industrial base on all programs, including the F-35, and stands ready to respond when needed.”

“It’s Getting ‘The Ugly'” – What Can We Really Do About Covid-19?

Submitted by Michael Every of Rabobank

Summary

Covid-19 has broken out of China and become a key global concern: most countries are now preparing for a serious virus epidemic.

All governments are faced with a series of unpalatable options over their next steps – yet all end with serious economic damage.

As a counterweight, we will see a reliance on several types of fiscal and monetary policy response: the conventional, the unconventional, and the ‘unconversational’ – steps that would not even have been talked about until very recently.

“The Conventional” response is already well underway with the RBA cutting rates 25bp to 0.50% and the Fed making an emergency cut of 50bp to takes Fed Funds to 1.25%: this was the first 50bp cut and the first out-of-meeting move since the Global Financial Crisis.

However, conventional policy is arguably of little impact, as initial reactions to the Fed surprise show – and the same is just as true for unconventional policy.

This takes us rapidly towards market conversations about the ‘unconversational’.

“The Bad” scenario was based on the assumption that there would be virus containment within a few weeks within China, with limited spread to other countries. This was already seen as nastier than the market was pricing for, with Chinese 2020 GDP growth reduced by -0.5% to -1.0%, and global GDP by -0.2 percentage points. This was our base case at the time.

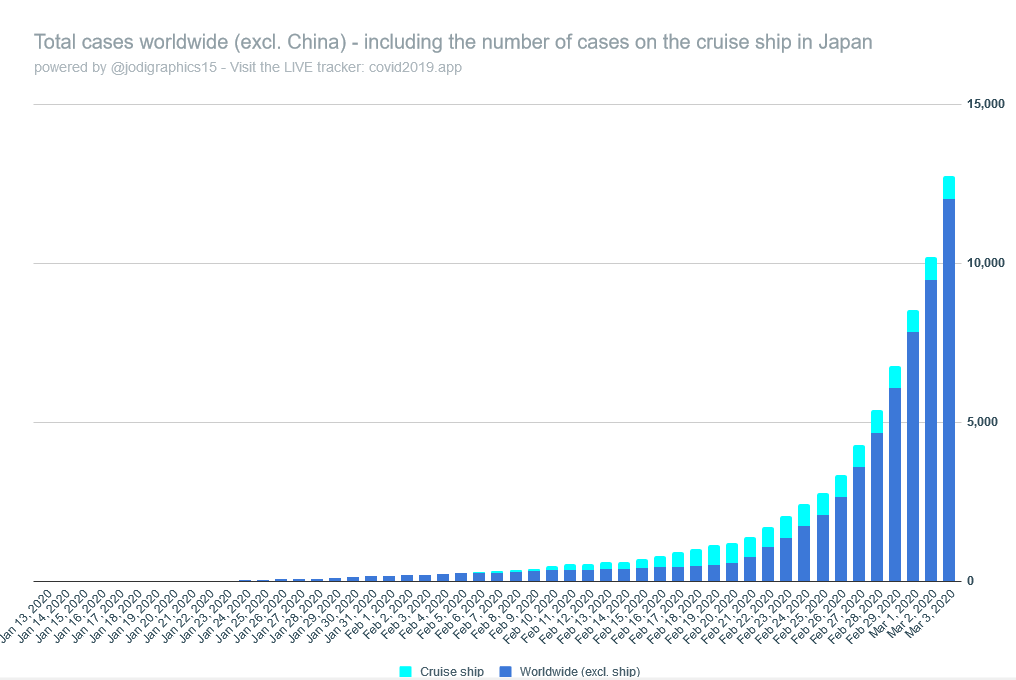

Source: @jodigraphics15

“The Worse” scenario envisaged an ongoing Chinese lockdown and the virus spreading to parts of ASEAN. This would have a larger regional and global impact. Chinese GDP growth was seen grinding to a halt, with a severe slowdown in ASEAN too, and significant global supply-chain disruptions meaning a global recession closer to the likes of 2008/09.

“The Ugly” scenario envisaged that the US, UK, and Europe were infected too. Naturally, this implied a deep global recession.

“The Unthinkable” was a real-life version of a Hollywood movie.

At time of writing, major virus outbreaks in South Korea, Iran, and Italy, as well official warnings from the rest of Europe, the UK, the US, and Australia, show us that we risk entering into “The Ugly” scenario and that a deep global recession may be inevitable. (See Figure 1.)

What is to be done?

As a result, attention is rightly turning to that old Leninist question: what is to be done? Most developed economies have now set up government virus crisis teams (COBRA in the UK, a new unit under Vice-President Pence in the US, for example). The question is, what can they do? The answers are unpalatable. Although the messaging and rhetoric varies in each location, there are logically only three basic options:

Do nothing and tell people all is well.

This option was tried at first in most Western countries – as evidenced by the lack of serious virus preparation until recently. However, Iran–where the total death toll is unclear but the virus appears to have taken a terrible toll already–is a graphic illustration that telling people all is well is not an effective strategy. The Iranian economy, already struggling under sanctions, has understandably suffered another huge blow as people panic and stay at home. As we noted in our previous report, both supply and demand have collapsed in tandem.

Allow business as usual while telling people to prepare

For now this is still the option being pursued by Western countries, with normal movement still allowed – indeed, encouraged. Yes, there are some restrictions in place–France has banned indoor gatherings of more than 5,000 people–but generally people and businesses are free to operate as usual. The problem is that even so many people are nonetheless reacting with fear, cancelling holidays, stopping travel and having meals out, and/or panic buying and hoarding essentials such as pasta and toilet rolls, as well as hand sanitizer and face masks. In short, the economy is already taking a major virus hit anyway – look at airlines as an indicator.

Institute China-style lockdowns.

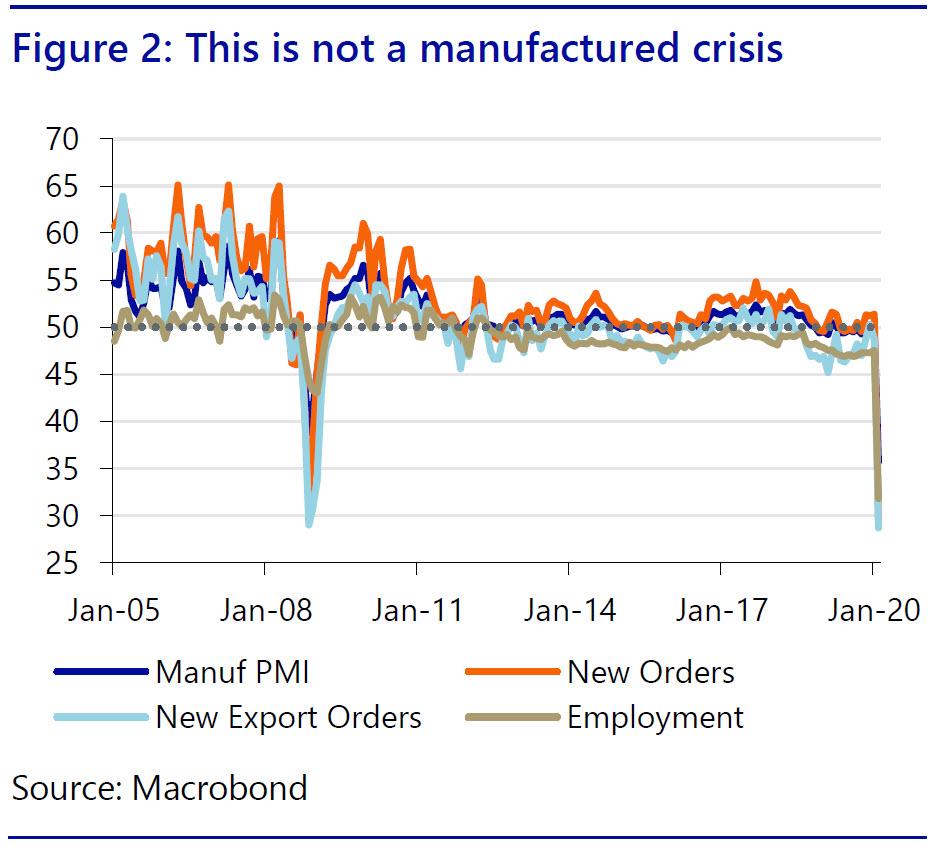

So far these steps have only been taken in specific virus hotspots in developed economies, for example Northern Italy. However, they are clearly ready to be more widely used if needed. Indeed, on 3 March the UK stated draconian action could be seen in its official worst-case scenario involving 1 in 5 of the population being infected and ill, requiring major cities to be locked down, public transport to be stopped, schools to close, workers to be told to work from home, the army on the streets, and the police told only to deal with serious crimes. Naturally, the impact on the economy of such a lockdown would be dramatic – as has been seen in the collapse in the Chinese manufacturing and services PMIs in February, the first real chance we have had to look at relevant official data since Covid-19 broke out. (See Figure 2.) However, there is broad recognition that the steps China took have played a key role in sharply reducing the number of new virus infections being seen in recent weeks. In other words, lockdowns do seem to work – and without them, this would already be a truly global pandemic.

The other key thing to note, however, is that whichever of the three options a government takes, the outcome is major damage to the economy.

Do nothing, and the economy is hit by the virus; act incrementally and a virus outbreak is likely to be larger – and the public to panic anyway, hitting the economy; lockdown the economy and be *guaranteed* a deep downturn.

Moreover, even if the last option were chosen, such action still needs to be coordinated between countries to be effective – yet effective international coordination can be very difficult to achieve, seeing countries resort to unilateral action instead.

For example, there is no use locking down one’s own economy, as in China’s case, if arrivals from another country that has not been taking virus precautions, like Iran, are free to enter and spread infection once again. Tellingly, China, the origin of Covid-19, is now putting travel restrictions in place for visitors from some other countries, such as Iran, after vociferously complaining that its own citizens were discriminated against by other states when it was still seeing the heaviest phase of the virus impact.

Slow burn not V-shape?

One other thing needs to be made clear, but which not many are expressing: at this stage, and regardless of the strategy pursued, there is a real risk that the virus will spread globally. In which case, the best that even quarantine measures can realistically hope to achieve is to spread out the impact of the virus so that not everyone gets sick at once, so reducing the strain on healthcare systems as well as economies. Yet this also means that this cannot be a quickly-resolved “V-shape” issue, but rather a slower burn with longer-lasting economic effects. The British government is now transparently assuming that this will be at least as 12-week cycle, hopefully beginning to be under control properly by June.

It is hard to square such thoughts with Bank of England Governor Carney’s recent message that in the UK Covid-19 will cause economic “disruption and not destruction”. For one, we have to stress that hysteresis is as important as hysteria: the longer the crisis lingers, either because of government actions or regardless of them, the deeper the economic damage that will be done on many fronts: how will many millions of the self-employed and small businesses owners, mortgage holders and credit-card borrowers survive for three months with little or no income. The impact of this crisis, even if managed well, may last well beyond what cynics would usually assume when dismissing panic-filled newspaper headlines.

Moreover, three months is an estimate. Even as UK (and US and European) summer eventually arrives, hopefully reducing the virus’s impact, it will be winter in Latin America and Sub-Saharan Africa, Australia, and New Zealand, all of whom have virus cases already, and the first two of which may not be in a positon to properly monitor or control going forwards. As such, unless economic connectivity between the northern and southern hemispheres is severed, doing even more damage, the risk is that there will be a fresh avenue of potential Covid-19 infection awaiting when summer turns back into autumn again. This is exactly what happened with the Spanish Flu in 1918-19, as we showed in another recent virus special report (“Fear and Trembling”). Slow-burn, not V-shape once again.

Of course, the nearest-term concern is with China as it tries to get hundreds of millions of workers back to work again without seeing a V-shape in virus infections too. Can this be done, or will it illustrate the damned-if-you-do, damned-if-you-don’t nature of this crisis?

So what IS to be done then?

The above is the key question and has been made all the more timely by the fact that 3 March saw an unprecedented gathering of the G7 and major central banks to discuss Covid-19 and the possible coordinated policy response. Expectations were high given how rare such meetings are: the outcome was pure disappointment, with the brief press release stating:

“We, G7 Finance Ministers and Central Bank Governors, are closely monitoring the spread of the coronavirus disease 2019 (COVID-19) and its impact on markets and economic conditions.

Given the potential impacts of COVID-19 on global growth, we reaffirm our commitment to use all appropriate policy tools to achieve strong, sustainable growth and safeguard against downside risks. Alongside strengthening efforts to expand health services, G7 finance ministers are ready to take actions, including fiscal measures where appropriate, to aid in the response to the virus and support the economy during this phase. G7 central banks will continue to fulfill their mandates, thus supporting price stability and economic growth while maintaining the resilience of the financial system.

We welcome that the International Monetary Fund, the World Bank, and other international financial institutions stand ready to help member countries address the human tragedy and economic challenge posed by COVID-19 through the use of their available instruments to the fullest extent possible.

G7 Finance Ministers and Central Bank Governors stand ready to cooperate further on timely and effective measures.”

Measure for measures

So what can the G7 actually do? Arguably, their possible “effective measures” above and beyond direct virus-fighting steps again come down to three broad areas: The Conventional; The Unconventional; and The “Unconversational” – things that were simply unspeakable in official circles until recently. Yet these three options all still sit within the normal axis of fiscal and monetary policy options.

Frisky Fiscal

The G7 statement openly mentioned “fiscal measures, where appropriate”. This suggests that there is no broad agreement on the need for fiscal stimulus right now. The US, with its past Trump tax cuts, and the UK, with its recent shift to a “leveling up” infrastructure budget, have already moved decisively towards larger fiscal deficits – but this can actually limit the extent to which further stimulus can be introduced above and beyond the automatic stabilizer effect that will naturally occur as the economy and tax-take decline in tandem. Moreover, in the Eurozone the room for fiscal maneuver is far more constrained by treaty, in Japan’s case by the government’s insistence on trying to reduce the fiscal deficit (given Covid-19, the timing of Japan’s last sales tax hike could not have been worse!), and in Australia’s case the fiscal constraint is also strong, even if it is entirely self-imposed.

However, there is a more general criticism of fiscal policy: it is slow to take effect, and in the case of the virus is unlikely to be of much short-term use. If consumers are locked away at home, what good does it do to start to build a new railway like High Speed 2 in the UK, for example? In some cases, one can make direct transfers to households or firms, such as the Trump tax cuts – but these would need to be better targeted at lower and middle-income groups and/or SMEs than the tax cuts seen to date in the US. At the same time, if one is bunkered away in fear of a virus, will a few extra dollars in one’s pocket incentivize going out to spend? Unlikely. That said, a liquidity-constrained SME could be hugely grateful for an emergency cash injection, especially if this can be used to pay salaries and prevent a domino effect of unemployment and/or demand destruction.

Naturally, China is taking the lead fiscally. It has already introduced tax cuts to try to offset the effects of Covid-19, and its semi-official Global Times has stated Beijing may be forced to embark on a major stimulus package larger than the CNY4 trillion (USD574bn) infrastructure stimulus package seen back in the 2008 financial crisis–“despite the side effects”–should the economic damage from Covid-19 prove too great. Understand that back in 2008 China’s GDP was USD4.7 trillion vs. USD14.3 trillion today, so if they imply a stimulus package larger as a percentage of GDP, which is not clear, then we are potentially talking about USD2.0 trillion stimulus package.

For China, that kind of thinking, incredibly, is still taken as within the conventional. In developed economies, it would be totally unconventional, as it implies a war-time level of fiscal deficit – but that does not mean that the political winds will not blow in that direction too; healthcare may take precedence over bombs, or over infrastructure, but the economic impact of massive deficit spending would be just as positive for developed economies.

Naturally, when talking of large-scale fiscal packages when public debt and/or fiscal deficits are already very high, we go beyond what was once the conventional and even the unconventional; we enter the realm of the ‘unconversational’, and of fiscal-monetary policy cooperation, or Modern Monetary Theory. We have discussed this several times in recent years (see here for example): might Covid-19 prove the political launch-pad for it outside China?

Mainly Monetary

Mainly Monetary

Central bank governors of course “stand ready”, a message that the Fed, ECB, BOE, and the PBOC, have already made clear to the public and markets. Conventionally, this first means rate cuts, even allowing for the very low level of rates to start with. These are already arriving:

The PBOC got in first, reducing their new benchmark 1-year Loan Prime Rate (LPR) by 10bp to 4.05%, while the fall in 3-month SHIBOR has been even steeper;

Other Asian central banks have been cutting for some time already, with Malaysia cutting 25bp on 3 March, for example. That said, the Bank of Korea (BOK) opted not to cut 25bp as expected last week, even though Korea has been very badly hit by Covid-19, as it did not see lower rates as an effective instrument to fight a virus (a point we shall return to);

The RBA were developed market trend-setters in cutting their overnight cash rate 25bp at their March meeting, taking the OCR to a new record low of just 0.50% – overtly over concerns about the supposedly short-term impact of Covid-19 on the services sector; and

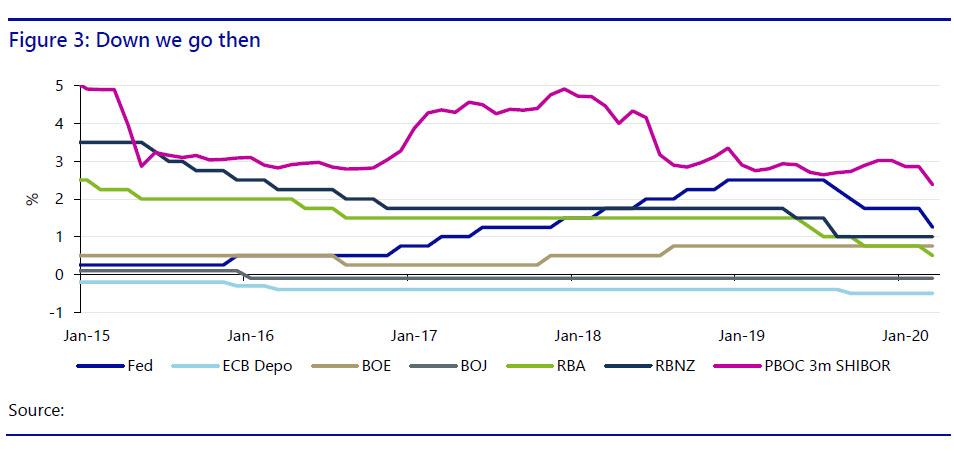

this was then eclipsed by the Fed cutting rates 50bp at an inter-meeting move for the first time since the Global Financial Crisis (See Figure 3.)

With the Fed action in particular, the rates flood gates have now opened even if rates are already close to zero, or below: the BOC, BOE and BOJ, to say nothing of other smaller global central banks, are certain to follow rapidly. Yet as with tax cuts, what use is a lower cost of borrowing if there is no supply and no demand? If you afraid to go and eat in a restaurant for fear of infection and possible illness or even death, then a slightly cheaper mortgage-loan rate will not really change your mind. This is the same fundamental problem that we already see with ultra-low rates and business investment: it’s ultra-cheap to borrow, but why risk it when there is no demand? Tellingly, the immediate market reaction to the Fed’s “bazooka” 50bp cut was to see both equities and yields drop sharply – and at both ends of the curve, with 10-year yields now decisively lower than the psychological and unprecedented 1% level.

So what then? At this point, the conventional must become unconventional. We already know what this “emergency” policy toolkit looks like: central bank asset purchases (i.e., QE) and asset swaps (reverse repos). Both of these are already in large-scale use, and both of them are likely to see even greater escalation in scale and geographical breadth: Australia will join the QE club, for example.

Of course, as we have argued repeatedly in various reports for years, even in a ‘healthy’–if structurally distorted–economy, QE has failed to generate sustainable, equitable growth or inflation. In an economy about to suffer from Covid-19, it will be even less effective. Reverse repo is also just papering over cracks in asset quality rather than addressing fundamentals.

Yet if new QE goes into government bond purchases to fund productive fiscal spending that boosts the economy, so much the better; however, that takes us from the unconventional to the ‘unconversational’.

Purely political

Apart from the fiscal and the monetary, one needs to recall that all governments have a third channel for policy measures that can also be considered very “unconversational” – the Purely Political. We tend to think of real power sitting with central banks and little with our elected officials: this overlooks the fact that the elected officials gave their power away – and can take it back again.

The struggle against Covid-19 is, quite naturally, already being portrayed as a ‘battle’ or a ‘war’, and during wars politics always takes precedence over business (and markets) as usual. If that kind of ‘kitchen sink’ strategy was available for GFC 2008-09, why should it not be with Covid-19?

We have already seen the state impose lockdowns in various regions of various countries, and/or international travel bans totally at odd with traditional freedom of movement: more seem very likely.

In France the government has requisitioned protective masks, and the US is contemplating using Korean-war era legislation to compel the production of anti-virus equipment: again, this is completely normal in present circumstances – and completely opposite to what the Western political-economy trend has been for decades. If the virus outbreak gets worse, one could easily imagine the government acting even more significantly via price controls or rationing of key goods, or by compelling companies to act in certain ways. Temporary nationalizations may even be required. These steps would no doubt be widely supported by the public if it helps prevent profiteering and better health outcomes.

Financially, given the huge blow that airlines and other service-sector firms are likely to suffer, we are also certain to see state aid and/or bailouts to key firms, even if this is technically illegal in some countries currently. We might we also face some temporary quasi-nationalisations once again, as during 2008-09.

Meanwhile, companies will be told to keep paying workers regardless of their cash-flow. In turn, banks will be leaned on to maintain credit lines to businesses and households, or to even extend debt facilities despite it running contrary to usual risk metrics. China is already leading the way here. Indeed, as in China we could also see a possible suspension of mark-to-market pricing for some financial assets or, copying their experience of 2015, a ban on short selling of stocks to try to ensure that this crisis does not become a full-blown financial calamity. It cannot be ruled out.

In short, almost every key part of the economy could, in the worst case, be subject to some form of state interference and prevention of price discovery. That is exactly what happens during wars – which as Von Clausewitz infamously quipped, are an extension of politics by other means.

Again this would likely be popular with much of the public, no doubt, and perhaps even with markets if it saves them from any major downside risks. Yet some will also quote pithy US journalist H L Mencken: “The urge to save humanity is almost always only a false-face for the urge to rule it.” Extricating the state from markets after the virus has passed may prove difficult, especially when the pre-virus economy already had so many pressing socio-economic imbalances to deal with.

But that’s an “unconversation” for another day. Let’s get through Covid-19 safely first.

Apple Issues Warning Over iPhone Replacement Shortage

Apple has warned their retail employees that there may be a shortage of replacement iPhones, in yet another example of a supply chain affected by the coronavirus.

According to Bloomberg, the company recently told tech support staff that heavily damaged devices might not be able to be replaced for as long as two to four weeks, Apple Store employees have said.

The workers, known as Geniuses, were advised in a memo that they can offer to mail replacement iPhones to customers and provide loaner devices to ease delays.

Some Apple stores have also noticed a shortage of individual parts, according to the employees, who asked not to be identified discussing private information. An Apple spokesman did not respond to requests for comment. –Bloomberg

The warning applies to iPhone owners who bring in devices that are too damaged to repair in-store (beyond repair) – which are typically resolved by replacing the entire phone.

Apple’s supply chain woes extend beyond just iPhones, as the company has also experienced shortages of key components for the iPad Pro. Meanwhile, the supply of iPhone 11 models has began to tighten a bit internationally.

Apple has prohibited employees from traveling to China, South Korea and Italy, and has asked that sick employees take leave. It has also encouraged telecommuting whenever possible.

Despite the ongoing virus threat, the company has been re-opening stores in China after temporarily closing all 42 locations. As of Wedensday, 38 locations were open again according to their retail website.

“I will note this, she’s from Hawaii,” King said of Gabbard.

“She’s a congresswoman from Hawaii; American Samoa votes on Super Tuesday. The rules as they now stand, if you get a delegate, you’re back in the debates. As of now. Correct?”

“Yeah, they haven’t, I mean, that’s been the rule for every single debate,” Thompson replied.

“And the DNC has not released their official guidance for the March 15 debate in Phoenix, but it would be very obvious that they are trying to cancel Tulsi, who they’re scared of a third party run, if they then change the rules to prevent her to rejoin the debate stage.”

And indeed, as the smoke clears from the Super Tuesday frenzy, this is precisely what appears to have transpired.

“The Gabbard campaign said it was informed that it would net two delegates from the caucuses in American Samoa, which will allocate a total of six pledged delegates,”The Hillreports today. “However, a report from CNN said that the candidate will receive only one delegate from the territory on Tuesday evening.”

“Tulsi Gabbard may have just qualified for the next Democratic debate thanks to American Samoa,” reads a fresh Business Insider headline. “Under the most recent rules, Rep. Tulsi Gabbard of Hawaii may have qualified for the next televised debate by snagging a delegate in American Samoa’s primary.”

“If Tulsi Gabbard gets a delegate out of American Samoa, as it appears she has done, she will likely qualify for the next Democratic debate,”tweetedWashington Post’s Dave Weigel. “We don’t have new debate rules yet, but party has been inviting any candidate who gets a delegate.”

Rank-and-file supporters of the Hawaii congresswoman enjoyed a brief celebration on social media, before having their hopes dashed minutes later by an announcement from the DNC’s Communications Director Xochitl Hinojosa that “the threshold will go up”.

“We have two more debates — of course the threshold will go up,” tweeted Hinojosa literally minutes after Gabbard was awarded the delegate. “By the time we have the March debate, almost 2,000 delegates will be allocated. The threshold will reflect where we are in the race, as it always has.”

We have two more debates– of course the threshold will go up. By the time we have the March debate, almost 2,000 delegates will be allocated. The threshold will reflect where we are in the race, as it always has.

“DNC wastes no time in announcing they will rig the next debates to exclude Tulsi,” journalist Michael Tracey tweeted in response.

This outcome surprised nobody, least of all Gabbard supporters. The blackout on the Tulsi 2020 campaign has reached such extreme heights this year that you now routinely see pundits saying things like there are no more people of color in the race, or that Elizabeth Warren is the only woman remaining in the primary. They’re not just ignoring her, they’re actually erasing her. They’re weaving a whole alternative reality out of narrative in which she is literally, officially, no longer in the race.

After Gabbard announced her presidential candidacy in January of last year I wrote an article explaining that I was excited about her campaign because she would severely disrupt establishment narratives, and, for the remainder of 2019, that’s exactly what she did. She spoke unauthorized truths about Syria, Afghanistan and Saudi Arabia, she drew attention to the plight of Julian Assange and Edward Snowden and said she’d drop all charges against both men if elected, she destroyed the hawkish, jingoistic positions of fellow candidates on the debate stage and arguably single-handedly destroyed Kamala Harris’ run.

The narrative managers had their hands full with her. The Russia smears were relentless, the fact that she met with Syrian president Bashar al-Assad was brought up at every possible opportunity in every debate and interview, and she was scoffed at and derided at every turn.

Now, in 2020, none of that is happening. There’s a near-total media blackout on the Gabbard campaign, such that I now routinely encounter rank-and-file liberals on social media who tell me they honestly had no idea she’s still running. She’s been completely redacted out of the narrative matrix.

All candidates of color are out. An openly gay married candidate is out. 2 women left. The rest? 70+ old white men fighting for the future of America in 2020. Because of course.

So it’s unsurprising that the DNC felt comfortable striding forward and openly announcing a change in the debate threshold literally the very moment Gabbard crossed it. These people understand narrative control, and they know full well that they have secured enough of it on the Tulsi Problem that they’ll be able to brazenly rig her right off the stage without suffering any meaningful consequences.

The establishment narrative warfare against Gabbard’s campaign dwarfs anything we’ve seen against Sanders, and the loathing and dismissal they’ve been able to generate have severely hamstrung her run. It turns out that a presidential candidate can get away with talking about economic justice and plutocracy when it comes to domestic policy, and some light dissent on matters of foreign policy will be tolerated, but aggressively attacking the heart of the actual bipartisan foreign policy consensus will get you shut down, smeared and shunned like nothing else. This is partly because US presidents have a lot more authority over foreign affairs than domestic, and it’s also because endless war is the glue which holds the empire together.

And now they’re working to install a corrupt, right-wing warmongering dementia patient as the party’s nominee. And from the looks of the numbers I’ve seen from Super Tuesday so far, it looks entirely likely that those manipulations will prove successful.

All this means is that the machine is exposing its mechanics to the view of the mainstream public. Both the Gabbard campaign and the Sanders campaign have been useful primarily in this way; not because the establishment would ever let them actually become president, but because they force the unelected manipulators who really run things in the most powerful government on earth to show the public their box of dirty tricks.

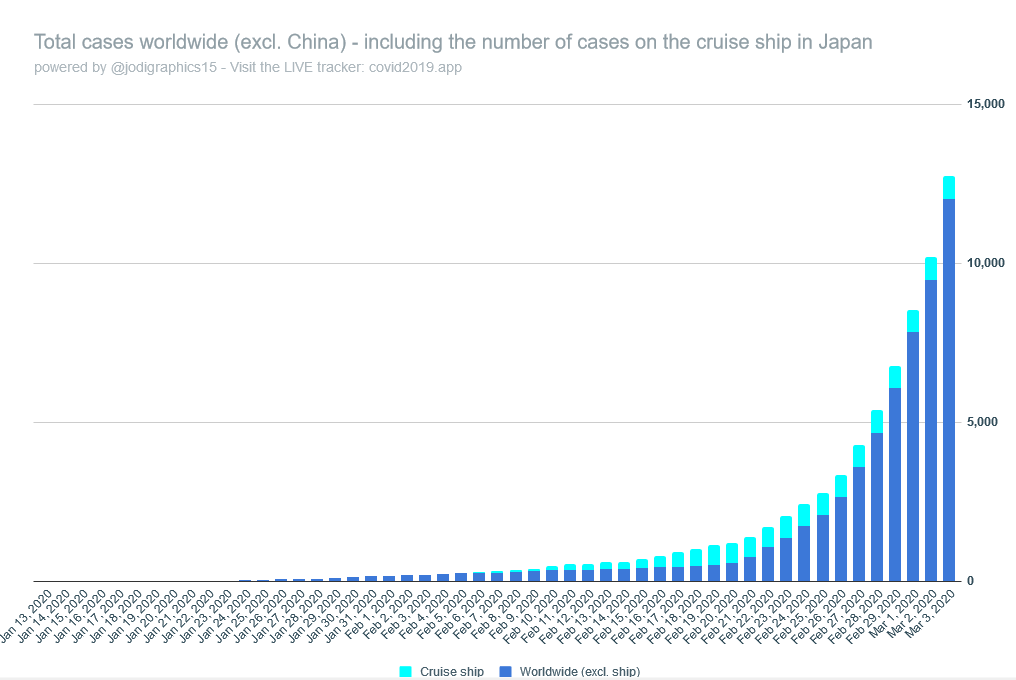

More than 92,300 people have been infected by the virus, which has killed about 3,100 people. Many of the cases are in China, but recent cases ex-China have been surging, especially in South Korea, Iran, Italy, Japan, and in many other countries across Europe.

Airlines have spent the last month canceling flights to China – American Airlines, United Airlines, and Delta Air Lines have suspended service to mainland China and Hong Kong. Reuters provides a full list of canceled flights across the world.

Flights to and from China crashed 80% YoY in February, according to Cirium travel industry data. Global air travel has plunged for the first time since the 2008/09 financial crisis, mostly in the Asia-Pacific region, the International Air Transport Association (IATA) recently said.

Plunging air traffic across the world has resulted in a steep decline in jet fuel. Singapore jet fuel prices have fallen 30% since the start of 2020 and contributed to a 50% collapse in jet fuel crack spreads, now at 2009 lows, Refinitiv data shows.

“It’s indeed an unprecedented fall since the global financial crisis… Jet fuel cracks have fallen to about $8 per barrel and we think it will stabilize around these levels in the next few months before seeing a recovery in the third quarter,” Paravaikkarasu said.

Jet fuel demand will likely remain in a slump for the next several quarters because virus fears will drive a plunge in tourism around the world, eliminate the need for air travel demand as long as the virus spreads. This could suggest the airline industry is headed for turbulence.

“We do see the virus eroding jet fuel demand to some extent in the Western Hemisphere. If the demand erosion develops faster, East-West flows will come under pressure,” Paravaikkarasu said.

Sukrit Vijayakar, director of Indian energy consultancy Trifecta, said people tend to plan their vacations far in advance. This could mean air travel remains depressed for the first half of the year.

The air travel slump suggests immense pain is headed for the global travel and tourism industry, employs roughly 320 million jobs across the world; Restaurants, travel agencies, hotels, amusement parks, casinos, and shopping malls, could be the most heavily impacted businesses to experience job losses if the virus crisis persists.

The grave risks and dangers in the process of worldwide out-sourcing and so-called globalization of the past 30 years or so are becoming starkly clear as the ongoing health emergency across China threatens vital world supply chains from China to the rest of the world. While much attention is focused on the risks to smartphone components or auto manufacture via supplies of key parts from China or to the breakdown of oil deliveries in the last weeks, there is a danger that will soon become alarmingly clear in terms of global health care system.

If the forced shutdown of China manufacture continues for many weeks longer, the world, could begin to experience shortages or lack of vital medicines and medical supplies. The reason is that over the past two decades much of the production of medicines and medical supplies such as surgical masks have been outsourced to China or simply made in China by Chinese companies at far cheaper prices, forcing Western companies out of business.

Sole source China

According to research and US Congressional hearings, something like 80% of present medicines consumed in the United States are produced in China. This includes Chinese companies and foreign drug companies that have outsourced their drug manufacture in joint ventures with Chinese partners. According to Rosemary Gibson of the Hastings Center bioethics research institute, who authored a book in 2018 on the theme, the dependency is more than alarming.

Gibson cites medical newsletters giving the estimate that today some 80% of all pharmaceutical active ingredients in the USA are made in China.

“It’s not just the ingredients. It’s also the chemical precursors, the chemical building blocks used to make the active ingredients. We are dependent on China for the chemical building blocks to make a whole category of antibiotics… known as cephalosporins. They are used in the United States thousands of times every day for people with very serious infections.”

The made in China drugs today include most antibiotics, birth control pills, blood pressure medicines such as valsartan, blood thinners such as heparin, and various cancer drugs. It includes such common medicines as penicillin, ascorbic acid (Vitamin C), and aspirin. The list also includes medications to treat HIV, Alzheimer’s disease, bipolar disorder, schizophrenia, cancer, depression, epilepsy, among others. A recent Department of Commerce study found that 97 percent of all antibiotics in the United States came from China.

Few of these drugs are labeled “made in China” as drug companies in the USA are not required to reveal their sourcing. Rosemary Gibson states that the dependency on China for medicines and other health products is so great that, “…if China shut the door tomorrow, within a couple of months, hospitals in the United States would cease to function.” That may not be so far off.

At the time the outsourcing of US and European drug manufacture to China began no one could imagine the present health catastrophe growing out of Wuhan in a matter of days. The massive China quarantine since late January has shut some 75-80% of all Chinese factories and created an unprecedented domestic China demand for every kind of medical product since the WHO declaration of medical emergency around the coronavirus or COVID-19 events at the end of January. It is unclear how badly deliveries of vital pharmaceuticals including essential antibiotics from China to the USA or Europe or other countries will be affected though anecdotal reports of hospitals beginning to experience delivery problems are surfacing. Even the idea to turn to India, another major global pharmaceutical supplier, only finds that most Indian manufacturers are dependent on China for their active drug ingredients.

Clinton and Outsourcing

The emergence of China in recent years as the global giant in terms of pharmaceutical drugs and products is embedded in the Made in China-2025 national plan as one of the ten priority areas for China to gain world leadership. It has not been simply a random chance development. This in turn, as the present COVID-19 crisis makes starkly clear, is a huge vulnerability for the rest of the world.

How did such a one-sided situation develop? We have to go back to the role of the Clinton Presidency in what was then dubbed globalization, the Davos model of outsourcing any and everything from advanced industrial countries like the USA or Germany to especially China after 2000.

In May 2000 in one of the most far-reaching actions of his Presidency, Bill Clinton, with the strong backing of US multinational companies, succeeded, over the strong objections and warnings of many trade unions, to get Congressional passage of a permanent “most-favored nation” trade status for China and US support for China entry into the World Trade Organization. That gave the green light to corporate America for a flood of overseas investment in cheaper China manufacture known as “out-sourcing.” Major US drug makers were among them. Within two years of the passage of the US free trade agreement with China the US shut its last penicillin fermentation plant in New York State as a result of severe Chinese low-price competition.

In 2008, the Chinese government designated pharmaceutical production as a “high-value-added industry” and bolstered the industry through subsidies and export tax rebates to encourage pharmaceutical companies to export their products. By 2019 China had become by far the world’s largest source for active pharmaceutical ingredients (APIs).

The Achilles Heel of this globalization and sole dependency for vital medicines on one country now becomes alarmingly clear as the future of China as a reliable supplier of needed drugs and other medical supplies has suddenly become a matter of grave concern to the entire world.

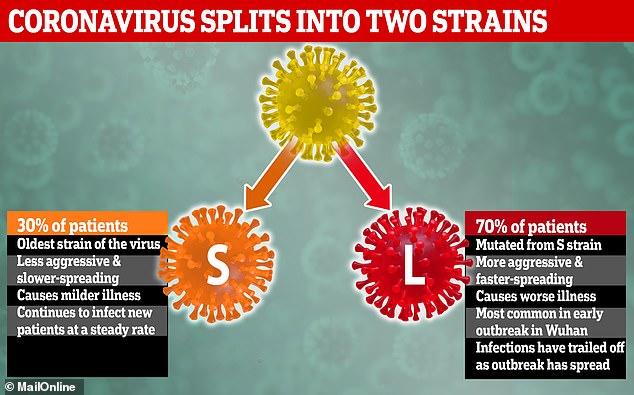

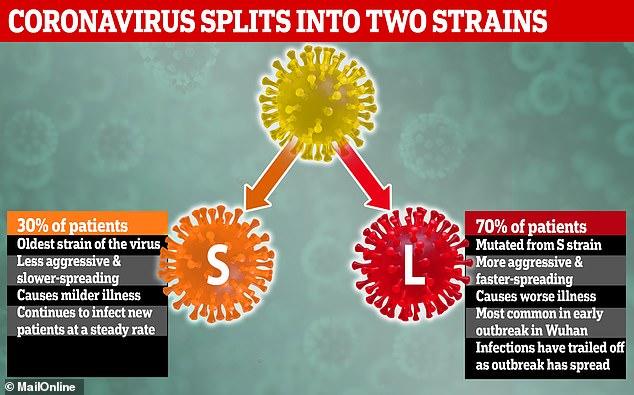

Scientists Discover More Aggressive Strain Of Coronavirus Responsible For 70% Of Current Infections

Chinese scientists studying the new coronavirus have found two new primary strains of the disease – one of which appears to be far more aggressive.

The researchers, from Peking University’s School of Life Sciences, discovered a milder “S-type” strain, and an “L-type” which is highly infectious and currently accounts for around 70% of cases, according to The Telegraph. The researchers cautioned that their preliminary findings looked at a limited number of cases (103), and that follow-up studies with larger data sets are needed to better understand the virus’s evolution.

A genetic analysis of the coronavirus found in a man who tested positive in the United States on January 21 also showed that it’s possible to be infected with both strains.

Coronavirus, which was first detected in December 2018 in Wuhan, China, has infected at least 94,000 people – officially, and killed more than 3,200 as of this writing.

And while there are now two major strains identified, scientist Trevor Bedford of Nextstrain has been tracking 161 strains of SARS-CoV-2 (the virus that causes COVID-19) in patients across the globe.

Bedford writes in a March 2 blog post that “The novel coronavirus which is responsible for the emerging COVID-19 pandemic mutates at an average of about two mutations per month.“

Visualize the virus radiating out from China, mutating as it spreads.

Right: map with different strains color-coded

Left: phylogenetic tree, showing how individual strains mutate and diverge

Here is his latest situation report, and thread on the virus which provides a detailed analysis of what mutations have been found, and where (click the tweet to jump into the thread):

Thus, I believe, similar to the case in Washington State (https://t.co/8wWxtiotE3), we had a situation in which a cluster was identified via intensive screening of travelers, but containment failed shortly thereafter and a sustained transmission chain was initiated. 6/7

The 1978 Humphrey-Hawkins Act requires the Federal Reserve to “promote” stable prices and full employment. Of course, the Fed’s steady erosion of the dollar’s purchasing power has made prices anything but stable, while the boom-and-bust cycle created by the Fed ensures that periods of low unemployment will not last for long. Despite the difficulties the Fed faces fulfilling its “dual mandate,” Federal Reserve Chairman Jerome Powell recently announced a new Fed mandate: to protect the financial system from being destabilized by climate change.

Powell appears to have bought into the propaganda that “the science is settled” regarding the existence, causes, and effects of climate change. But the statement “the science is settled” is itself unscientific. Science is rarely settled as today’s new discoveries disprove yesterday’s consensus. In the case of climate change, many scientists dispute the claim that absent massive expansion of government power a climate apocalypse will soon be at hand.

So far, the Fed’s actions regarding climate change include holding a conference and Chairman Powell indicating the Fed is likely to join the Network for Greening the Financial System. This network is composed in part of central banks from around the world that are attempting to work together to assess the risks of, and plan possible responses to, climate change.

While Powell has not given details regarding other actions the Fed might take to protect the financial system from climate change, there are a number of actions that the Fed could take.

For starters, Powell could signal that the Fed would be willing to increase its purchase of government debt if Congress passes Representative Alexandria Ocasio-Cortez’s Green New Deal. The Fed, since its creation, has been monetizing federal debt, and thus enabling the growth of the welfare-warfare state.

The Fed could implement “Green Quantitative Easing” by purchasing bonds of green energy and other companies whose products fit the environmentalist agenda.

The Fed could also use its monetary and regulatory authority to “encourage” financial institutions to support “environmentally-friendly” businesses.

Whatever policies the Fed adopts to protect the financial system from climate change, the result will be further erosion of the dollar’s purchasing power, increased government control over the economy, lower economic growth, increased crony capitalism, and a reduction in liberty and prosperity.

Ironically, the Fed’s plans to address climate change will harm the environment. History shows that the most effective way to protect the environment is via a system of private property rights and free markets. Private property owners are better stewards of the environment than are government bureaucrats because private property owners have greater incentives to maintain the value of their property. This is why the greatest pollution in history was in the communist countries of the 20th century.

The Fed’s failure to provide any details on how it will carry out its self-imposed climate change mandate is another reason why Congress must rein in the secretive, rogue central bank. A step in restoring a monetary policy that truly promotes prosperity is to pass the Audit the Fed bill so Congress and the people can at last learn the full truth about the Federal Reserve.

{kind=link}

{kind=link}