FOMC Minutes Suggest Fed Will Keep Buying Bonds “For Many Years”, Shuns Yield Curve Control

Tyler Durden

Wed, 07/01/2020 – 14:06

Fed Minutes TL;DR: things can get better, or worse. We have no idea what happens next but everyone agreed we should sound confident and give “forward guidance” as if we know what is coming. Also, we will buy stocks and equity ETFs after the next 20% drop.

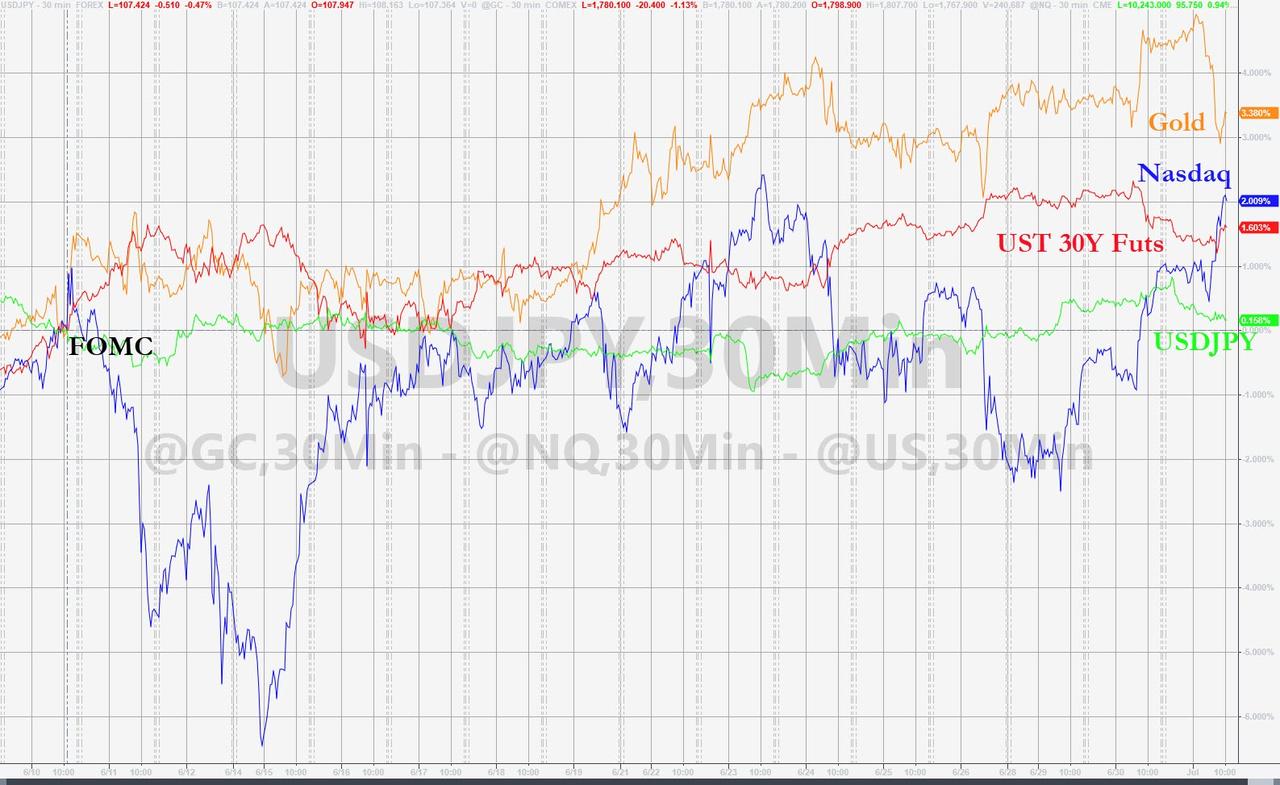

Since The Fed statement on June 10th, gold has outperformed (even beating Nasdaq) as the “lower for… ever” mantra is reinforced…

After moving hawkishly higher after the FOMC meeting, the market has drifted notably dovishly in the last two weeks

As a reminder, the FOMC kept rates unchanged at 0-0.25%, at the June 9-10 meeting, as was expected; it did not announce any enhanced forward guidance, nor did it announce any yield curve control policy but did formalize its QE program. Perhaps most notably, Powell adopted a cautious tone during the press conference and has maintained that stance, until yesterday’s congressional testimony where he suggested that the economy had “entered an important new phase and has done so sooner than expected”, signaling more optimism.

Today’s Minutes are not expected to produce any market-moving comments but Fed-watchers will be listening for discussions of negative rates and yield curve control, and any fears of excess valuations (as noted in The Fed’s semi-annual outlook).

* * *

As expected The Fed’s Minutes show that officials reviewed other options to provide more support for the economy but Fed officials did agree there was no more need to analyze yield curve control (mentioned 15 times in the minutes).

A number of participants commented on additional challenges associated with YCT policies focused on the longer portion of the yield curve, including how these policies might interact with large-scale asset purchase programs and the extent of additional accommodation they would provide in the current environment of very low interest rates.

In their discussion of the foreign and historical experience with YCT policies and the potential role for such policies in the United States, nearly all participants indicated that they had many questions regarding the costs and benefits of such an approach.

“some participants said [YCT could result] in the central bank inadvertently setting yield caps or targets at inappropriate levels. “

This is important as consensus expected some form of YCT policy adjustment in September.

Instead, Fed officials preferred to focus on inflation-based forward guidance:

“That could possibly entail a modest temporary overshooting of the Committee’s longer-run inflation goal but where inflation fluctuations would be centered on 2 percent over time.

“They saw this form of forward guidance as helping reinforce the credibility of the Committee’s symmetric 2 percent inflation objective and potentially preventing a premature withdrawal of monetary policy accommodation.”

On how long they will remain easy…

“The staff presented results from model simulations that suggested that forward guidance and large-scale asset purchases can help support the labor market recovery and the return of inflation to the Committee’s symmetric 2 percent inflation goal.

The simulations suggested that the Committee would have to maintain highly accommodative financial conditions for many years to quicken meaningfully the recovery from the current severe downturn.”

Did The Fed just realize it is obsolete:

“businesses and households might not be as forward looking as assumed in the model simulations, which could reduce the effectiveness of policies that are predicated on influencing expectations about policy several years into the future”

Did The Fed admit QE is no longer working?

“Several participants remarked that declines in the neutral rate of interest and in term premiums over the past decade and prevailing low levels of longer-term yields would likely act as constraints on the effectiveness of asset purchases in the current environment and noted that these constraints were not as acute when the Committee implemented such programs in the wake of the Global Financial Crisis.”

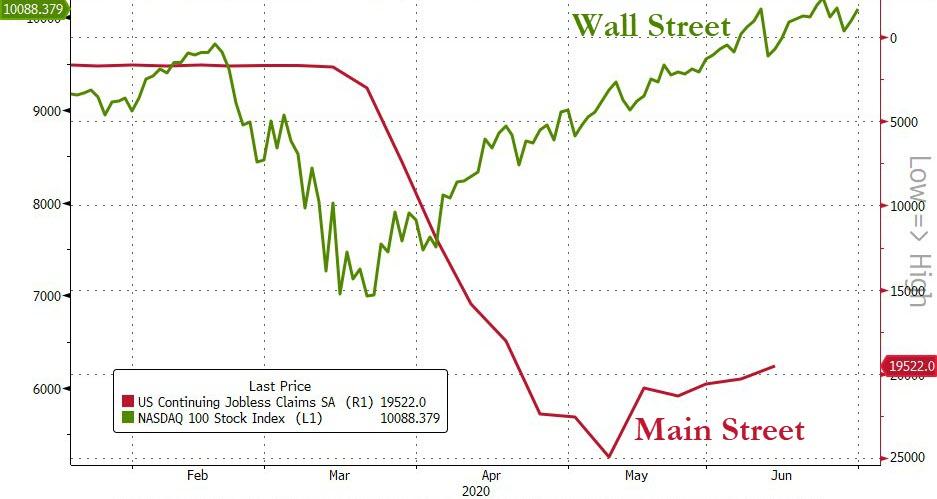

Finally, in the “Developments in Financial Markets and Open Market Operations” section, The Fed admits the market is only higher on optimism and multiple expansion:

“Risk asset prices were buoyed by optimism about the potential for increased economic activity associated with reopenings as parts of the United States and other countries relaxed lockdown restrictions. That optimism was reinforced by high-frequency data suggesting a pickup in economic activity. Market participants also pointed to the suite of U.S. and global policy measures taken since mid-March as laying a foundation for the improvement in risk sentiment. Against this backdrop, staff analysis suggested that equity prices had been supported by expectations for a strong rebound in earnings next year, low risk-free rates and positive risk sentiment. Despite this improvement in risk sentiment, market participants expected weak overall growth in 2020, and elevated uncertainties in the outlook remained.”

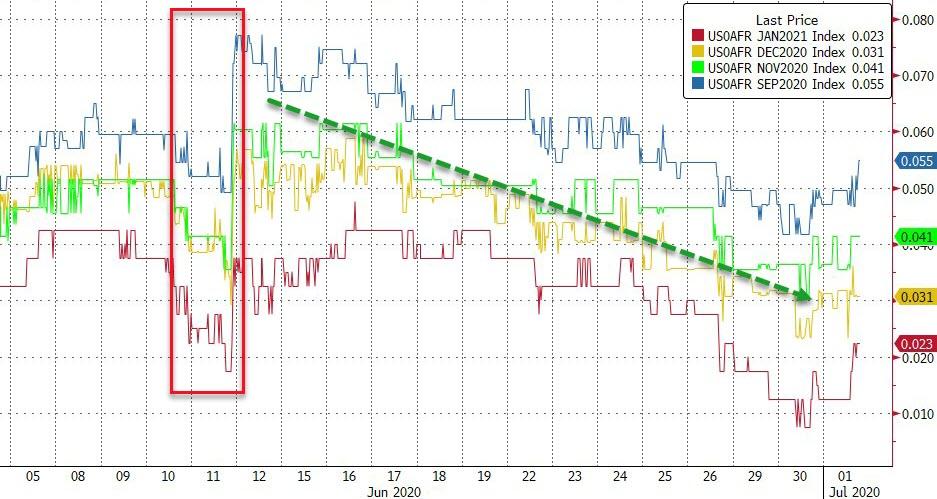

Perhaps Powell should check this chart out before the next FOMC meeting?

Full Minutes Below:

via ZeroHedge News https://ift.tt/2YQWOwl Tyler Durden