The Decade Long Path Ahead To Recovery, Part 1: Debt

Tyler Durden

Wed, 07/01/2020 – 10:45

Authored by Michael Lebowitz and Jack Scott via RealInvestmentAdvice.com,

This article is the first of a four-part series on the vectors driving future economic growth. Forthcoming articles will tackle Depression, Demographics, and De-globalization.

The discussions about economic recovery and the path ahead are ongoing. The shape it will take will defy the simplistic “V”, “W”, and “L” expressions being used by forecasters. One thing, however, is certain. Every bazooka, tank, and A-bomb of stimulus is being used to combat the downturn.

The question, so few seem to ask, is at what cost?

“Additional fiscal support could be costly, but worth it if it helps avoid long-term economic damage and leaves us with a stronger recovery,”

– 5/29/2020 Jerome Powell Peterson Institute of International Economics.

As we will explain, what is best for economic growth and prosperity is not what Powell’s Fed is doing. Power, influence, and intellectual elitism may be winning today’s battle, but they are losing the war. The evidence is compelling.

Yardeni et al.

In a recent Grant’s Current Yield podcast, guest Ed Yardeni, said: “I find too many investors…act like preachers. They judge the Fed, good or bad, a moralistic approach. My approach, as an investment strategist is bullish or bearish.”

Yardeni’s only concern appears to be whether Fed actions are good or bad for his portfolio. Specifically, good or bad for his career.

Like all investors, we also need to understand whether Fed actions are bullish or bearish. However, we have a conscience and care about what is best and right. Yardeni’s comments remind us of the Niemoller prose, “First they came…”.

Yardeni’s view represents the epitome of expedience over principle. His perspective is not a one-off, in fact, far from it. It is a consensus among financial and political insiders. It runs through the veins of Wall Street, Congress, and the White House.

Planning Ahead

The United States is in the midst of an unprecedented third asset bubble in twenty years. The recent crisis is being blamed on COVID. We disagree, COVID is the pin that pricked the bubble.

To help visualize this, we quote from our article The COVID 19 Tripwire:

“There is a popular game called Jenga in which a tower of rectangular blocks is arranged to form a sturdy tower. The objective of the game is to take turns removing blocks without causing the tower to fall. At first, the task is as easy as the structure is stable. However, as more blocks are removed, the structure weakens. At some point, a key block is pulled, and the tower collapses. Yes, the collapse is a direct cause of the last block being removed, but piece by piece the structure became increasingly unstable. The last block was the catalyst, but the turns played leading up to that point had just as much to do with the collapse. It was bound to happen; the only question was, which block would cause the tower to give way?”

The real catalysts include the following:

-

Accumulated leverage

-

Poor use of cash for stock buybacks

-

Fragile financial infrastructure

-

Lack of productive investment

-

Overzealous speculation

-

Unfettered government spending

-

Preference for consumption over savings

In sum, capital has been grossly misallocated towards speculation and away from productive investment. These outcomes are, in large part, a result of prior and current Fed policy.

Like households and corporations, the government also reacts to the “signals” being sent through the market. When interest rates are manipulated, strange things happen and ripple throughout an economy. When that currency is the global reserve currency, the word “strange” takes on a new definition.

Past Experience

In the current set of circumstances, the economy and markets are experiencing a confluence of shocks that are both extreme and unique. Regardless, we can still reflect on past episodes that caused great turmoil and anxiety. Although the analysis does not provide explicit answers, the rigor offers insight and direction.

As James Grant once said, “My goal is to have everyone agree with me, later.”

Foresight with confidence offers early, cheap entry into opportunities that everyone else sees “tomorrow”.

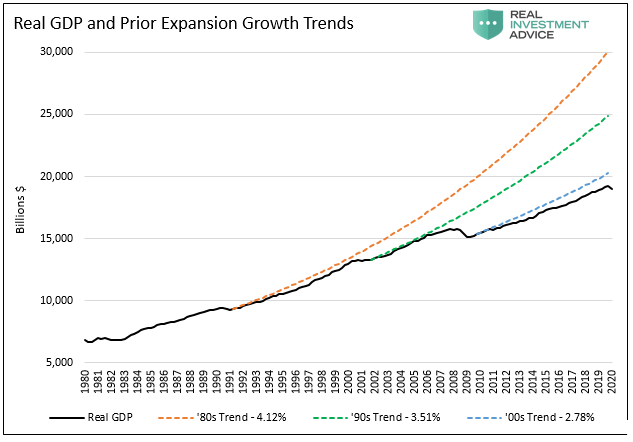

A New Trajectory for U.S. Growth

The chart below offers a substantive context for what has transpired over the past 40 years. The colored lines show what economic activity would have been had the growth rate of the prior expansion held true in the following expansion.

As shown, after each successive bubble, the trajectory of growth, GDP shifts lower. Slow economic growth implies that the time to full recovery is elongated.

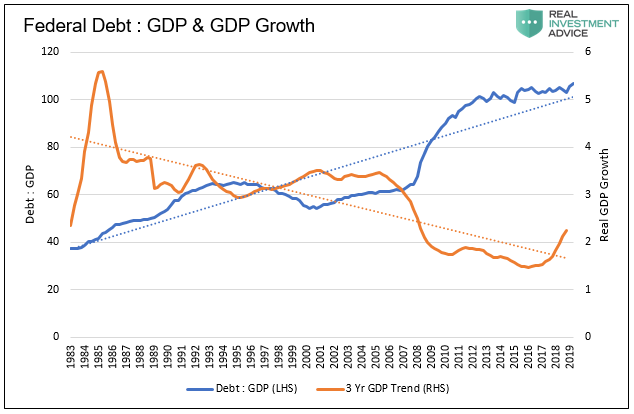

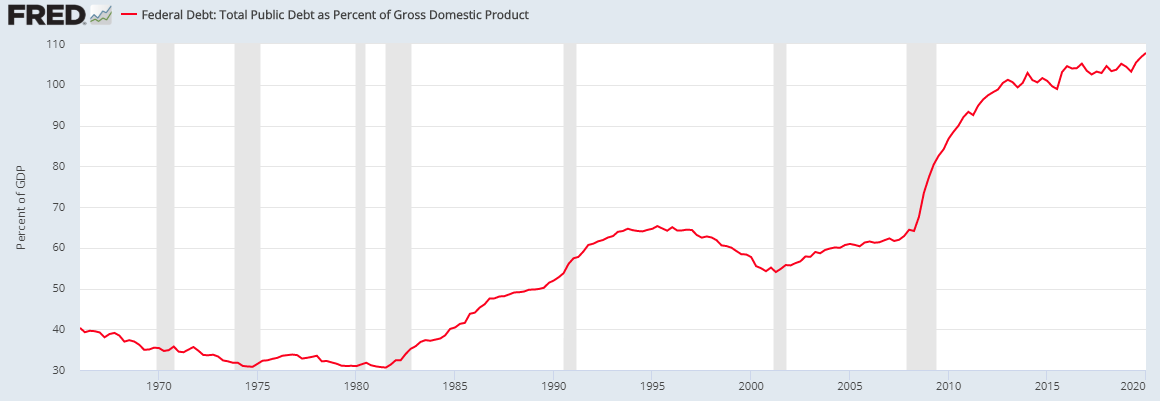

To predict a post-COVID growth trajectory we need only look at the ratio of Federal debt to GDP. As shown below, the trend lines of that ratio to trend economic growth are negatively correlated. Since 1990 the relationship has a very high r-square of .928. Simply, as the ratio of Federal debt to GDP rises, economic growth declines.

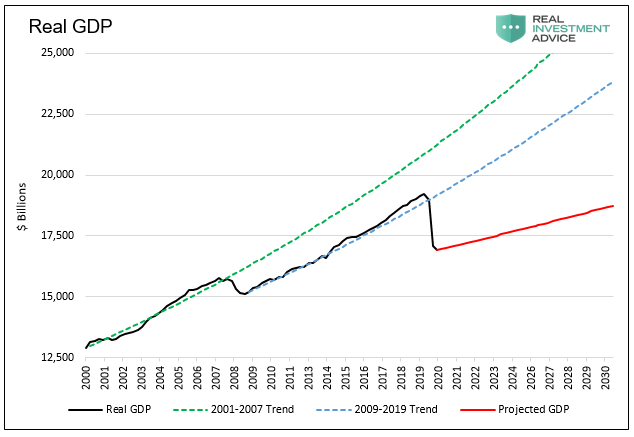

The next graph projects GDP based on the expected ratio of Federal Debt to GDP. For this exercise, we conservatively assume the ratio will be 115% when the economic recovery begins. That compares to 82% in 2009 and 55% in 2002. We also assume economic growth falls by 10% in the second quarter and 1% in the third quarter. GDP then grows at our projected growth rate of 1.07%.

Based on this analysis, the economy will not regain pre-COVID economic levels this decade.

The Culprit

The new paradigm of weak recoveries is due to the Fed’s policy prescription for recessions; debt-fueled consumption. Through lower interest rates they incentivize people, corporations, and the government to borrow. The benefits are here and now as economic recovery ensues. The cost is paid tomorrow.

The debt is increasingly put to unproductive uses, and the obligations grow exponentially larger than income. As we discussed in Why the Recovery Will Fall Short of Forecasts, given the issues facing productivity and demography, this is a troubling outlook.

Recessions are a normal part of the economic cycle. They are a healthy reset that purges weak businesses and encourages productive capital investment for the future, not speculation. The resumption of growth takes time in a recession left to its course. However, improved productivity and prudent use of resources sets the economy on a sustainable path to healthy growth.

The New Order

Modern-day Fed policy encourages speculation over productivity growth. The result is sustained unemployment and low wage growth. The longer people are out of work, the less likely they are to re-assimilate into the productive workforce. This means they require and expect more government assistance, which further raises the debt obligation on the dwindling taxpayer.

Revisiting one of our cornerstone concepts, economic growth hinges upon two key elements:

-

Growth in the labor force

-

Productivity gains

The regressive trajectory of GDP growth reflects that those factors of growth are diminishing.

A Fine Mess

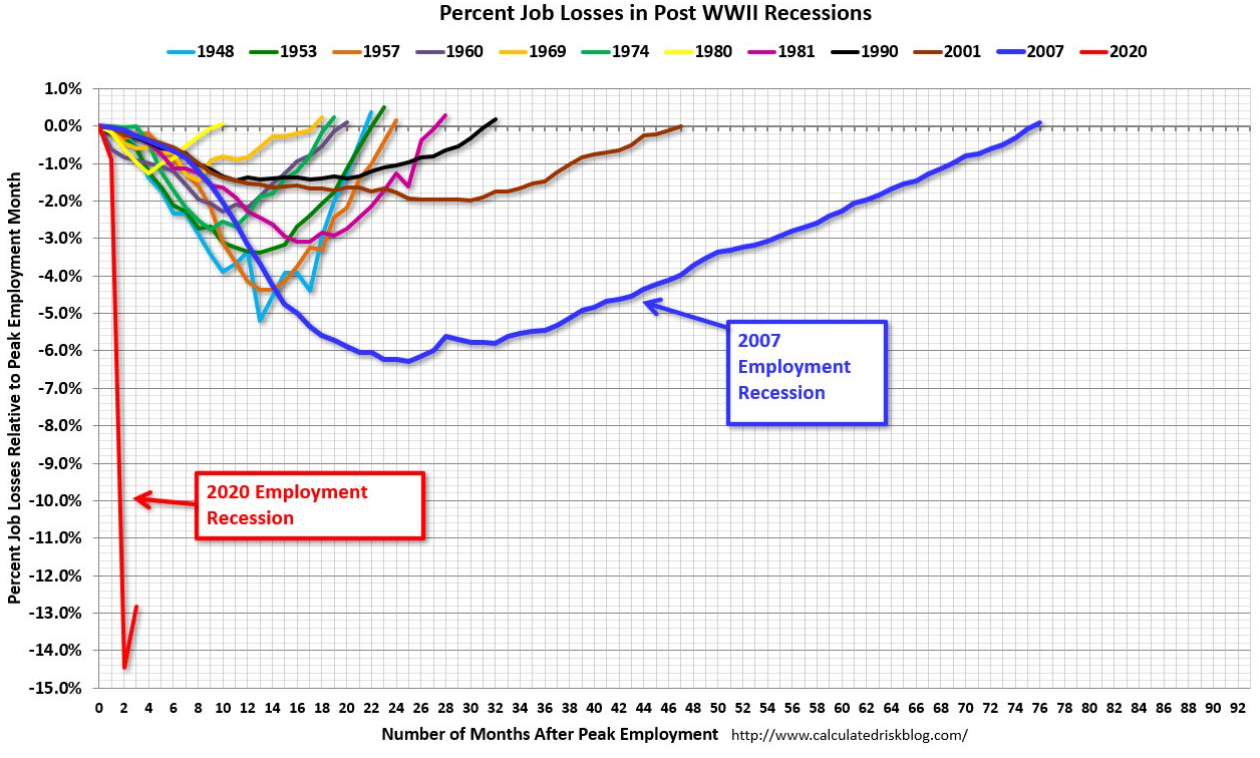

Even after the surprisingly positive payroll report for May 2020, the chart below illustrates the magnitude of our predicament. It also reflects the mischaracterizations being used to discuss the post-COVID19 economic circumstance.

Note that the last four recessions required longer periods consecutively for jobs to recover fully.

The amount of non-productive debt used to combat downturns compounds the pre-existing debt problem. It ensures that the economy will continue to struggle for years to get back to pre-COVID levels of economic activity.

“Much higher public debt levels will become a permanent feature of our economies and will be accompanied by private debt cancellation.”

– Mario Draghi, March 2020, FT

At $6 trillion in December 2001, then $11.5 trillion in June 2009, U.S. government debt has now ballooned to $26 trillion. Tragically, debt continued to pile up over the last decade despite economic recovery. It, in fact, was the economic recovery. Without that expansion of debt, there would have been little to no economic growth.

To characterize it otherwise as Fed and government officials have done is intellectually dishonest. When the debt-to-GDP graph below updates next, the ratio will be close to 120%. The pattern since 1980 is clear.

The Fed is extraordinarily accommodative in both their interest rate posture and their willingness to fund massive federal deficits.

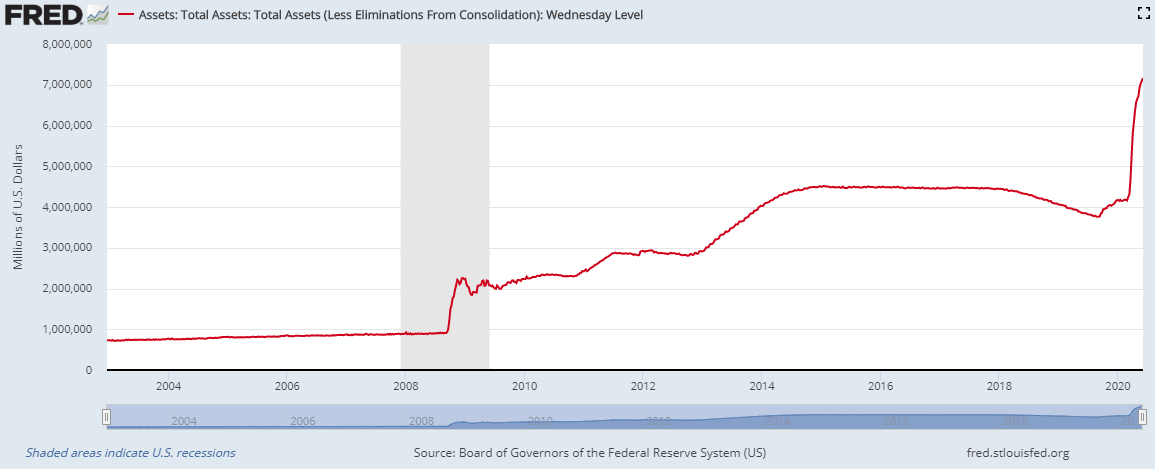

They deliberately encourage everyone to borrow. That occurs with lower rates and expansion of the Fed balance sheet (QE) as shown in the chart below. They have also promised near-zero rates and QE for the foreseeable future. This is, indeed, a fine mess.

Evidence

Despite the information we present, the same talking points justify the same actions. The actions do not serve the best long-term interests of the public. The tools the Fed is employing destroys wealth for all but the top 1%.

The policies incite inflation, much of which is hidden by faulty government reporting. As detailed in a previous article, Two Percent for the One Percent, inflation erodes living standards for the broad population.

Even after years of botched policies that damage the organic economy, no one in Congress challenges the Fed’s counter-factual. Given the evidence from their inability to forecast even one or two quarters ahead, how do they know what they are doing works? How do they know the long-term implications of their policies will not be disastrous? The answer, of course, is they do not know.

Summary

As mentioned, based on this analysis using the trends of the past 40 years, the economy will not regain pre-COVID output levels until sometime in the 2030s. The implications of that scenario are weak GDP growth, poor labor market growth, and high market volatility, among many other unknowns. It might also imply continuing civil unrest and potentially war.

All of those in power appear to be complicit in advancing this agenda. Why not? They are rewarded handsomely for their compliance. That is how politicians and the corporate elite get wealthy from their positions of power.

Meanwhile, the rest of us watch and wait, hoping that someone will show up to represent the community in this injustice.

What the Fed is doing to save today will cause problems tomorrow. We have two choices; we can recognize the problem and force change by electing like-minded legislators. Or, we can stand aside. The latter, of course, only furthers behavior detrimental to our country.

Instead of cheering Fed actions today, consider what they are doing to the future.

If nothing changes, then the problem will eventually take care of itself. It will not be peaceful or pleasant, but it will come to a resolution. The outcome will not be favorable for investors or what was once the greatest economy in history.

via ZeroHedge News https://ift.tt/2ZqCf98 Tyler Durden