Is This Time Different? One Striking Chart Leads To Two Completely Opposite Conclusions On Wall Street

Tyler Durden

Thu, 07/09/2020 – 15:10

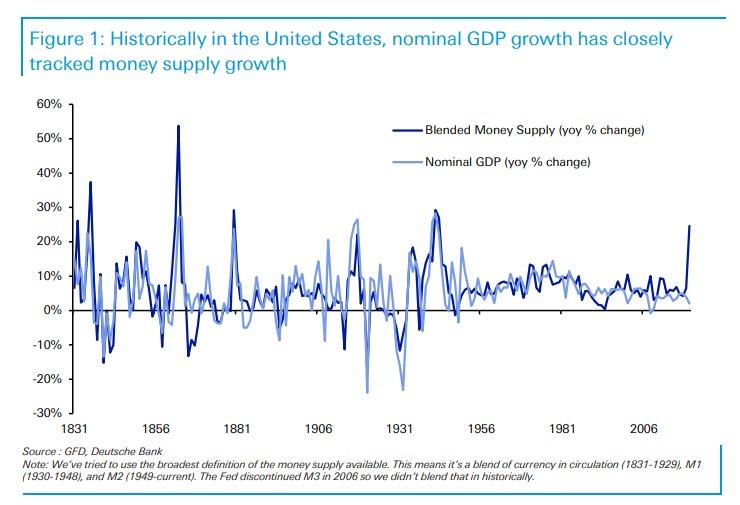

In the past three months, the Fed has unleashed a truly historic amount of liquidity in its attempt to prop up the economy market and avoid a prolonged second great depression, printing trillions in digital money equivalents, with the resulting expansion in the money supply the largest since the Great Depression.

Discussing the chart above, Deutsche Bank’s Jim Reid writes that historically “there’s a decent correlation through history between the annual change in the money supply and nominal GDP growth, as would be implied by the PQ = MV equation/identity. As the chart shows this is only the 10th time that YoY money supply growth has gone above 20% in the US.”

So what happens next? Or rather, what is supposed to happen next? Well, as Reid – who is clearly more in the “inflation is coming” camp – puts it, “on all previous occasions nominal GDP soon moved comfortably into double digits – mostly through inflation.”

The obvious conclusion is be that, if this time is not different, then US inflation is set to explode higher, not just in stocks as this liquidity flood makes its way into risk assets, something we showed back in May…

… but across the broader economy, as all those who have been espousing MMT as the next big thing realize that it has been tried on many prior occasions with catastrophic results.

On the other hand, maybe this time is different. As Jim explains, when he showed the top chart to his colleague, DB’s Chief US Economist Matt Luzzetti convinced this was definitive proof of coming hyperinflation, “he dampened my enthusiasm by suggesting that”:

- in the last few decades the relationship has weakened as the graph shows;

- the pace of the money supply increase will be hard to maintain with the Fed already ratcheting down the pace of purchases over the last month;

- a substantial part of the money supply increase in March was companies drawing on credit lines offsetting lost revenues rather than as an expansionary tool;

- the huge stimulus checks were again offsetting lost income and are unlikely to be repeated to the same scale.

As Reid then rhetorically asks, “maybe this time is different?” although as he adds, “one thing we all agree on in the inflation/deflation debate is that higher inflation will likely require fiscal and monetary policy to be working aggressively together going forward. In the 2010s they tended to move in opposite directions – predominantly aggressive monetary but tighter fiscal. The disinflation believers suggest stimulus will be difficult to maintain and the demand shock from covid will linger. Inflationists are more likely to believe in a regime shift as we move to a more MMT/helicopter money type world and one where the debt burden gives a huge incentive to inflate.”

While the jury is still out on whether the Fed’s latest liquidity flood will be inflationary or deflationary (readers can participate in a survey asking their opinion what the endgame is the following link), in his latest note Albert Edwards – who recently threw in the towel on being Wall Street’s most famous deflationst and is now expecting a “Great melt“, but not before one final, and massive deflationary thrust – picks up on the theme observed by Reid, and asks what if what the Fed has done is not enough.

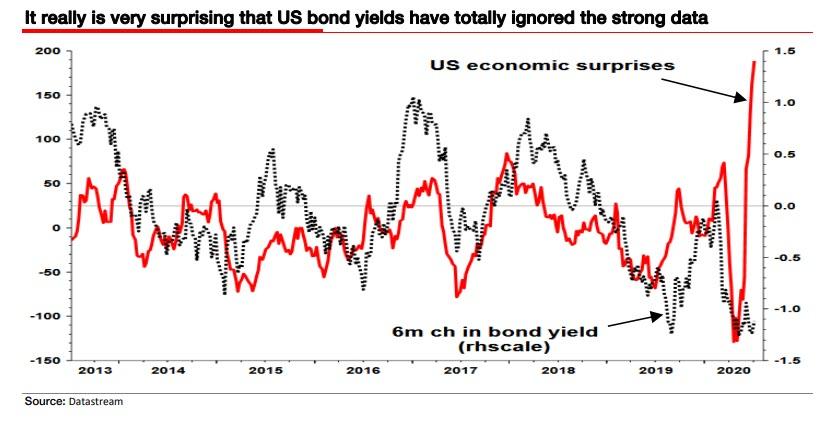

Specifically, Edwards highlights that while the surge in money supply has also unleashed an impressive spike in positive economic surprises as tracked by the Citi econ surprise index (only possible due to the record baseline to expectations after the biggest crash in the US economy on record), it has failed to make even a modest impact on treasury yields, to wit:

used to say if the equity market wont go down on bad news, what do you think will happen when good news comes along?

[My former Kleinwort boss Roger Palmer] used to have a nice turn of phrase for most market situations and one of them has stuck with me. He used to say “if the equity market wont go down on bad news, what do you think will happen when good news comes along?”

I was thinking of that as I was looking at this chart below showing US economic surprises surging to record highs and yet the US 10y yield showing absolutely no inclination to rise, as one would normally expect (see chart below). As Roger would have said if he were still here, if bond yields cant rise on strong data, it beggars the question as to what will happen when the economic surprise indicator begins to turn down again – as it will surely do.

Another way of saying this is that the Fed has literally launched every legal bazooka in its arsenal at the economy market, and with the collaboration of Steve Mnuchin and the Treasury, several quasi illegal ones – such as purchasing corporate bonds under special exemption from section 13(3) – and yet it has succeeded in neither boosting GDP nor yields. Unless, of course, as we have warned previously, the Fed has now terminally broken the bond market’s discounting and signaling capabilities, and instead of reflecting future inflation (or deflation), all the bond prices indicates is the Fed’s willingness and ability to monetize trillions in debt.

So going back to Jim Reid’s question of what happens next, Edwards remains steadfast, “our view is that US bond yields will soon be negative along the whole length of the curve.”

via ZeroHedge News https://ift.tt/2AHzmbw Tyler Durden