Stocks Are Overvalued On 17 Of 20 Metrics; Growth Is A 6-Sigma Outlier To Value

Tyler Durden

Fri, 07/31/2020 – 13:50

With the S&P once again near all time highs even as profits are in freefall, pushing the EV/fwd EBITDA multiple to new all time highs…

… now seems a good time to ask the $64 trillion question: just how overvalued is the market?

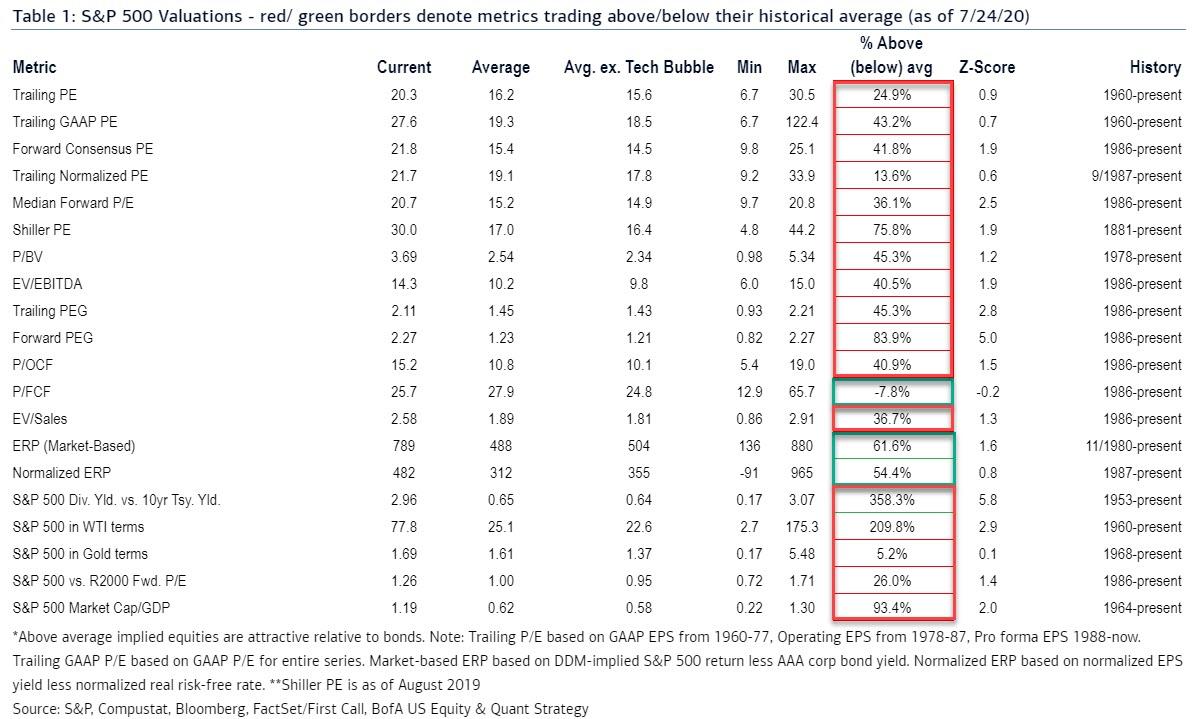

The answer: according to BofA’s Savita Subramanian, the S&P 500 forward PE expanded in July to 21.8x from 21.5x in June, as returns (+4%) have outpaced estimate revisions (+ 2%). The current multiple is two standard deviations above the historical average of 15.4x (since 1986) – the highest since the Tech Bubble.

Stepping back, BofA finds that stocks are trading above average on all but three of the 20 measures its tracks.

Most notably, the forward PEG is at record highs (2.3x) and the median forward PE (20.7x) is in-line with the prior record of 20.8x. Only on the equity risk premium (i.e., relative to bonds) and on free cash flow (artificially depressed from low capex) does the S&P appear statistically inexpensive. Both of those metrics are due to the Fed’s direct purchases of billions in bonds every single day.

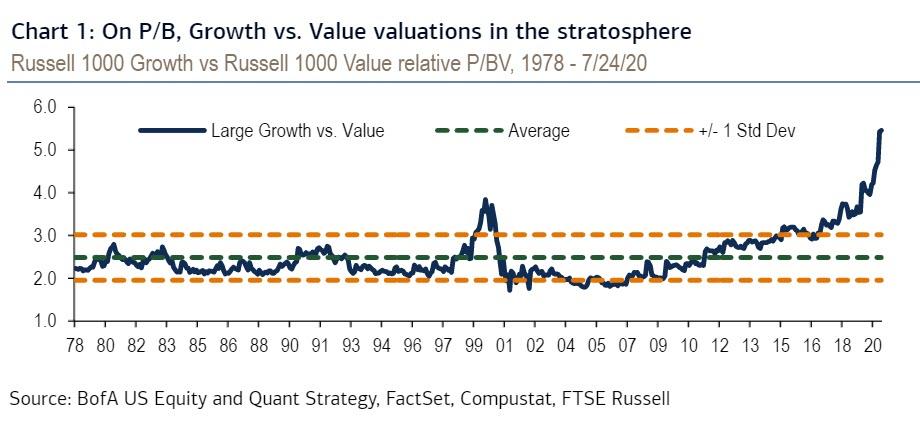

But wait, it gets crazier, because BofA also finds that the “Growth vs. Value” relative price/book value is in the 6-sigma “stratosphere”.

As Subramanian writes, “we have seen increasingly extended relative valuations for Growth and Value stocks, supporting our preference for Value for at least the next few months.” To wit, on some valuation measures, the Russell 1000 Growth index trades at a historical discount to Value index on Price to L/T EPS Growth (PEG), it trades at a premium on other metrics (such as sales or trailing/forward earnings), but nowhere is the distorted valuation more visible than on a Price/Book basis where the relative multiple looks to have gone “vertical”.

In short, value stocks trade at near-record levels of cheapness vs. Momentum (relative forward P/E ~2 standard deviations below average and at lowest levels since Tech Bubble extremes), yet none of this matters as the Fed’s now constant market interventions make growth stocks the consistent winner at the expense of value.

via ZeroHedge News https://ift.tt/2PflwAZ Tyler Durden