Russell Napier: Central Banks Have Become Irrelevant

Tyler Durden

Sat, 08/01/2020 – 14:00

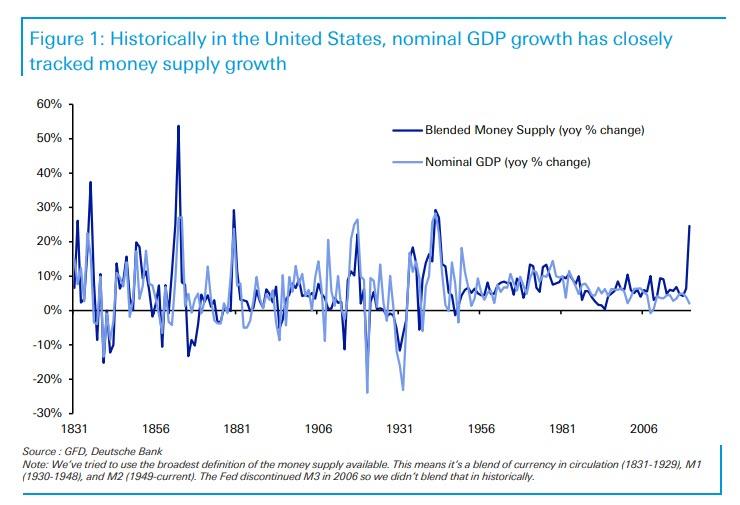

Two weeks ago, we wrote that one by one the world’s legendary deflationists are taking one look at the following chart of the global money supply (as shown most recently by DB’s Jim Reid) and after seeing the clear determination of central banks to spark a global inflationary conflagration, are quietly (and not so quietly) capitulating.

One month ago it was SocGen’s Albert Edwards, who after calling for a deflationary Ice Age for over two decades, finally threw in the towel and conceded that “we are transitioning from The Ice Age to The Great Melt” as “massive monetary stimulus is combining with frenzied fiscal pump-priming in an attempt to paper over the current slump.”

At roughly the same time, “the world’s most bearish hedge fund manager“, Horseman Global’s Russell Clark reached a similar conclusion writing that “all the reasons that made me believe in deflation for nearly 10 years, do not really exist anymore. China looks okay to me, and potentially very good. Commodity supply is getting cut at a rate I have never seen before. The US dollar is strong but will likely weaken from here. And it is clear to me Western governments will only ever attempt fiscal austerity as a last resort, not a first. The conditions for both good and bad inflation are now in place.“

Finally, it is the turn of another iconic deflationist, Russell Napier, who in the latest Solid Ground article on his Electronic Research Interchange (ERIC) writes that “we are living through another deflation shock but [he] believes that by 2021 inflation will be at or near 4%.”

In the lengthy report , Napier wrote that similar to Albert Edwards’ conclusion that MMT, i.e., Helicopter Money, is a gamechanger, “what has just happened is that the control of the supply of money has permanently left the hands of central bankers – the silent revolution.” As a result, “the supply of money will now be set, for the foreseeable future, by democratically elected politicians seeking re-election.” His conclusion: “it is time to embrace the silent revolution and the return of inflation long before such permanency is confirmed.” (read our summary of his full report in the article we published on July 12 “Another Iconic Deflationist Capitulates: According To Russell Napier, “Control Of Money Supply Has Permanently Left The Hands Of Central Bankers.”)

* * *

In a follow up published two days later to clarify his position, Russell sat down with Mark Dittli of the Swiss website TheMarket.ch in which he laid out his reasoning for why investors should prepare for inflation rates of 4% and more by next year. The main reason, as we expounded on previously: central banks have become irrelevant as governments have taken control of the money supply.

The full article is below, courtesy of TheMarket.ch:

Central Banks have Become Irrelevant

In the years following the financial crisis, numerous economists and market observers warned of rising inflation in the face of the unorthodox monetary p0licy by central banks. They were wrong time and again.

Russell Napier was never one of them. The Scottish market strategist has for two decades – correctly – seen disinflation as the dominant theme for financial markets. That is why investors should listen to him when he now warns of rising inflation.

“Politicians have gained control of money supply and they will not give up this instrument anymore”, Napier says. In his view, we are at the beginning of a new era of financial repression, in which politicians will make sure that inflation rates remain consistently above government bond yields for years. This is the only way to reduce the crushing levels of debt, argues Napier.

In an in-depth conversation with The Market/NZZ he explains how investors can protect themselves and why central banks have lost their power.

Mr. Napier, for more than two decades, you have said that investors need to position themselves for disinflation and deflation. Now you warn that we are in a big shift towards inflation. Why, and why now?

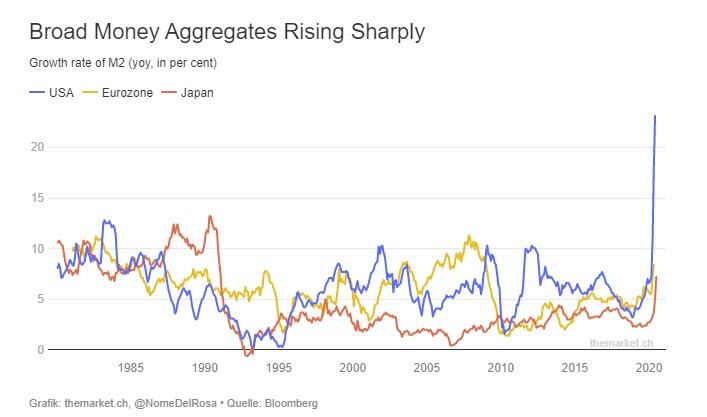

It’s a shift in the way that money is created that has changed the game fundamentally. Most investors just look at the narrow money aggregates and central bank balance sheets. But if you look at broad money, you notice that it has been growing very slowly by historical standards for the past 30 or so years. There were many factors pushing down the rate of inflation over that time, China being the most important, but I do believe that the low level of broad money growth was one of the factors that led to low inflation.

And now this has changed?

Yes, fundamentally. We are currently in the worst recession since World War II, and yet we observe the fastest growth in broad money in at least three decades. In the US, M2, the broadest aggregate available, is growing at more than 23%. You’d have to go back to at least the Civil War to find levels like that. In the Eurozone, M3 is currently growing at 8,9%. It will only be a matter of months before the previous peak of 11.5% which was reached in 2007 will be reached. So I’m not making a forecast, I just observe the data.

Why is this relevant?

This is the big question: Does the growth of broad money matter? Investors don’t think so, as breakeven inflation rates on inflation-linked bonds are at rock bottom. So clearly the market does not believe that this broad money growth matters. The market probably thinks this is just a short-term aberration due to the Covid-19 shock. But I do believe it matters. The key point is the realization who is responsible for this money creation.

In what way?

This broad money growth is created by governments intervening in the commercial banking system. Governments tell commercial banks to grant loans to companies, and they guarantee these loans to the banks. This is money creation in a way that is completely circumventing central banks. So I make two key calls: One, with broad money growth that high, we will get inflation. And more importantly, the control of money supply has moved from central bankers to politicians. Politicians have different goals and incentives than central bankers. They need inflation to get rid of high debt levels. They now have the mechanism to create it, so they will create it.

In the aftermath of the Global Financial Crisis, central banks started their quantitative easing policies. They tried to create inflation, but did not succeed.

QE was a fiasco. All that central banks have achieved over the past ten years is creating a lot of non-bank debt. Their actions kept interest rates low, which inflated asset prices and allowed companies to borrow cheaply through the issuance of bonds. So not only did central banks fail to create money, but they created a lot of debt outside the banking system. This led to the worst of two worlds: No growth in broad money, low nominal GDP growth and high growth in debt. Most money in the world is not created by central banks, but by commercial banks. In the past ten years, central banks never succeeded in triggering commercial banks to create credit and therefore to create money.

If central banks did not succeed in pushing up nominal GDP growth, why will governments succeed?

Governments create broad money through the banking system. By exercising control over the commercial banking system, they can get money into the parts of the economy where central banks can’t get into. Banks are now under the control of the government. Politicians give credit guarantees, so of course the banks will freely give credit. They are now handing out the loans they did not give in the past ten years. This is the start.

What makes you think that this is not just a one-off extraordinary measure to fight the economic effects of the pandemic?

Politicians will realize that they have a very powerful tool in their hands. We saw a very nice example two weeks ago: The Spanish government increased their €100bn bank guarantee program to €150bn. Just like that. So there will be mission creep. There will be another one and another one, for example to finance all sorts of green projects. Also, these loans have a very long duration. The credit pulse is in the system, a pulse of money that doesn’t come back for years. And then there will be a new one, and another one. Companies won’t have any incentive to pay back these cheap loans prematurely.

So basically what you’re saying is that central banks in the past ten years never succeeded in getting commercial banks to lend. This is why governments are taking over, and they won’t let go of that tool anymore?

Exactly. Don’t forget: These are politicians. We know what mess most of the global economy is in today. Debt to GDP levels in most of the industrialized world are way too high, even before the effects of Covid-19. We know debt will have to go down. For a politician, inflation is the cheapest way out of this mess. They have found a way to gain control of the money supply and to create inflation. Remember, a credit guarantee is not fiscal spending, it’s not on the balance sheet of the state, as it’s only a contingent liability. So if you are an elected politician, you have found a cheap way of funding an economic recovery and then green projects. Politically, this is incredibly powerful.

A gift that will keep on giving?

Yes. Theresa May made a famous speech a few years ago where she said there is no magic money tree. Well, they just found it. As an economic historian and investor, I absolutely know that this is a long-term disaster. But for a politician, this is the magic money tree.

But part of that magic money tree is that governments keep control over their commercial banking system, correct?

Yes. I wrote a big report in 2016 titled «Capital management in the age of financial repression». It said the final move into financial repression will be triggered by the next crisis. So Covid-19 is just the trigger to start an aggressive financial repression.

Are you expecting a repeat of the financial repression that dominated the decades after World War Two?

Yes. Look at the tools that were used in Europe back then. They were all in place for an emergency called World War II. And most countries just didn’t lift them until the 1980s. So it’s often an emergency that gives governments these extreme powers. Total debt to GDP levels were already way too high even before Covid-19. Our governments just know these debt levels have to come down.

And the best way to do that is through financial repression, i.e. achieving a higher nominal GDP growth than the growth in debt?

That’s what we have learned in the decades after World War II: Achieve higher nominal GDP growth through higher rates of inflation. The problem is just that most active investors today have had their formative years after 1980, so they don’t know how financial repression works.

Which countries will choose that path in the coming years?

Basically the entire developed world. The US, the UK, the Eurozone, Japan. I see very few exceptions. Switzerland probably won’t have to financially repress, but only because its banking system is not in the kind of mess it was in in 2008. Government debt to GDP in Switzerland is very low. Private sector debt is high, but that is mainly because of your unique treatment of taxation for debt on residential property. So Switzerland won’t have to repress, neither will Singapore. If Germany and Austria weren’t part of the Eurozone, they wouldn’t have to repress either. Of course there is one catch: If the Swiss are not going to financially repress, you will have the same problem you had for a long time, namely far too much money trying to get into the Swiss Franc.

So we will see more upward pressure on the Franc?

Yes. But financial repression has to include capital controls at some stage. Switzerland will have to do more to avoid getting all these capital inflows. At the same time, other countries would have to introduce capital controls to stop money from getting out.

The cornerstones of the last period of financial repression after World War II were capital controls and the forcing of domestic savings institutions to buy domestic government bonds. Do you expect both of these measures to be introduced again?

Yes. Domestic savings institutions like pension funds can easily be forced to buy domestic government bonds at low interest rates.

Are capital controls really feasible in today’s open financial world?

Sure. There are two countries in the Eurozone that have had capital controls in recent history: Greece and Cyprus. They were both rather successful. Iceland had capital controls after the financial crisis, many emerging economies use them. If you can do it in Greece and Cyprus, which are members of the European Monetary Union, you can do it anywhere. Whenever a financial institution transfers money from one currency to another, it is heavily regulated.

What’s the timeline for your call on rising inflation?

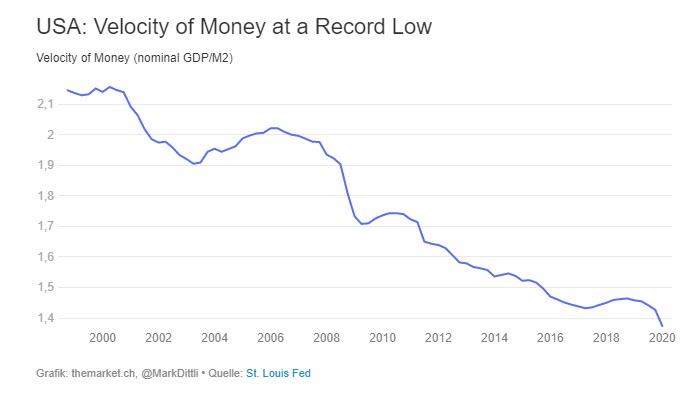

I see 4% inflation in the US and most of the developed world by 2021. This is primarily based on my expectation of a normalization of the velocity of money. Velocity in the US is probably at around 0.8 right now. The lowest recorded number before that was 1.4 in December 2019, which was at the end of a multi-year downward trend. Quantitative easing was an important factor in that shrinking velocity, because central banks handed money to savings institutions in return for their Treasury securities. And all the savings institutions could do was buy financial assets. They couldn’t buy goods and services, so that money couldn’t really affect nominal GDP.

What will cause velocity to rise?

The money banks are handing out today is going straight to businesses and consumers. They are not spending it right now, but as lockdowns lift, this will have an impact. My guess is that velocity will normalize back to around 1.4 some time next year. Given the money supply we have already seen, that would give you an inflation rate of 4%. Plus, there is no reason velocity should stop at 1.4, it could easily rise above 1.7 again. There is one additional issue, and that is China: For the last three decades, China was a major source of deflation. But I think we are at the beginning of a new Cold War with China, which will mean higher prices for many things.

Most economists say there is such a huge output gap, inflation won’t be an issue for the next three years or so.

I don’t get that at all. You can point to the 1970s, where we had high unemployment and high inflation. It’s a matter of historical record that you can create inflation with high unemployment. We have done it before.

The yield on ten year US Treasury Notes is currently at around 60 basis points. What will happen to bond yields once markets realize that we are heading into an inflationary world?

Bond yields will go up sharply. They will rise because markets start to realize who is controlling the supply of money now, i.e. not central banks, but politicians. That will be the big shock.

For a successful financial repression, governments and central banks will need to stop bond yields from rising, won’t they?

Yes, and they will. But let me be precise: It will be governments who will act to stop bond yields from going up. They will force their domestic savings institutions to buy government bonds to keep yields down. The bit of your statement I disagree with is that central banks will put a cap on bond yields. They won’t be able to.

Why not? Even the Fed is toying with the idea of Yield Curve Control, an instrument they successfully used between 1942 and 1951, when they capped yields at 2.5%.

I think this is a bad parallel, because from 1942 to 1951, we also had rationing, price controls and credit controls. With that in place, it was easy for the Fed to cap Treasury yields. Yield Curve Control is easy when everyone is expecting deflation, which the current policy of the Bank of Japan shows. But once market participants start to expect inflation, they will all want to sell their bonds. The balance sheet of the central banks will just balloon to the sky. They would be spreading fuel on the fire, given that their balance sheets would expand with rising inflation expectations. Yield Curve Control in an environment of rising inflation expectations is not going to happen.

You are saying that governments now control the supply of money, and it will be governments who will make sure policies of financial repression are successfully implemented. What will be the future role of central banks?

They will be sidelined. They will become more a regulatory than a monetary organization. The next few years will be fascinating. Imagine, you and I are running a central bank and we have a 2% inflation target. And we see our own government print money with a growth rate of 12%. What are we going to do to fulfill our mandate of price stability? We would have to threaten higher interest rates. We would have to ride a full-blown attack on our democratically elected government. Would we do that?

Paul Volcker did in the early 80s.

Yes. But Paul Volcker had courage. I don’t think any of today’s central bankers will have the guts to do that. After all, governments will argue that there is still an emergency given the shocks of Covid-19. There is a good parallel to the 1960s, when the Fed did nothing about rising inflation, because the US was fighting a war in Vietnam, and the administration of Lyndon B. Johnson had launched the Great Society Project to get America more equal. Against that background of massive fiscal spending, the Fed didn’t have the guts to run a tighter monetary policy. I can see that’s exactly where we are today.

So central banks will be mostly irrelevant?

Yes. It’s ironic: Most investors believe in the seemingly unlimited power of today’s central banks. But in fact, they are the least powerful they have ever been since 1977.

As an investor, how do I protect myself?

European inflation-linked bonds are pretty attractive now, because they are pricing in such low levels of inflation. Gold is obviously a go-to asset for the long term. In the next couple of years, equities will probably do well. A bit more inflation and more nominal growth is a good environment for equities. I particularly like Japanese equities. Obviously you wouldn’t buy government bonds under any condition.

How about commodities?

In a normal inflationary cycle, I’d recommend to buy commodities. There is just one complicating factor with China. If we really enter into a new Cold War with China, that will mean big disturbances in commodities markets.

You wrote in the past that there is a sweet spot for equities up to an inflation rate of 4%, before they tip over. Is this still valid?

Yes, this playbook is still in place. But once governments truly force their savings institutions to buy more government bonds, they will obviously have to sell something. And that something will be equities. Historically, inflation above 4% hasn’t been too good for equities.

How high do you see inflation going?

If we’re taking the next 10 years, I see inflation between 4 and 8%, somewhere around that. Compounded over ten years, combined with low interest rates, this will be hugely effective in bringing down debt to GDP levels.

In which country do you see it happening first? Who will lead?

The one I worry about the most is the UK. It has a significant current account deficit, it has to sell lots of government bonds to foreigners. I never really understood why foreigners buy them. I wouldn’t. Now we have Brexit coming up, which could still go badly. I don’t think it will, but it could. So we would see a spike in bond yields in the UK.

What will it take for an investor to successfully navigate the coming years?

First, we have to realize that this is a long term phenomenon. Everyone is so caught up in the current crisis, they miss the long term shift. This will be with us for decades, not just a couple of years. The financial system is a very different place now. And it’s a very dangerous place for savers. Most of the skills we have learned in the past 40 years are probably redundant, because we have lived through a 40 year disinflationary period. It was a period where markets became more important and governments less important. Now we are reversing that. That’s why I recommend to my clients that they promote the people from their emerging markets departments to run their developed world departments. Emerging markets investors know how to deal with higher levels of inflation, government interference and capital controls. This will be our future.

via ZeroHedge News https://ift.tt/2Phj0Kw Tyler Durden