Knock On Wood: Blackstone, Balyasny And About Ten Other Managers Bought ARKK Puts In Q1

If you had a sneaking suspicion that Wall Street was starting to bet against the “untouchable” Cathie Wood, as we did over the last couple months, you were right.

Today it was revealed that “about two dozen investment advisers” that included Balyasny Asset Management and a unit of Blackstone bought put options on ARK’s Innovation ETF during the first quarter. Blackstone bought puts on 1.3 million ARKK shares and Balyasny acquired puts on 436,500 shares.

The managers saw Wood’s fund as a “alternative to buffer against a slump in stocks that surged during the pandemic,” that buying puts on an index, the report said. In other words, the asset managers were so confident in Wood’s ability to handpick stocks that would lose value during a pull back, they took the inverse of her “expertise” instead of just getting short a tech or small cap index (or both).

And so far, that strategy likely provided outsized returns as a hedge: ARKK is down about 30% from its highs, while the QQQ ETF is down just about 0.7% from its February peak.

Chris Murphy, co-head of derivatives strategy at Susquehanna International Group, said: “If you were sitting on some serious gains heading into this year and you want to protect those gains, it was an effective strategy.”

Deer Park Road Management Co. bought puts on 2.15 million ARKK shares with a notional value of about $258 million. Deer Park Chief Investment Officer Scott Burg said: “As rates have been going up, the tech stocks have been getting crushed. You could see that in the first quarter.”

Efrem Kamen, the head of New York-based Pura Vida Investments, said: “The Ark Innovation fund had a tremendous run over the course of 2020 and early 2021. However, the level of fund flows into the ETF appeared to be extreme.” Kamen’s fund bought puts on 622,500 ARKK shares with a notional value of about $75 million.

“Volatility on Ark Innovation ETF was an efficient way to hedge some of the factor risk in our portfolio,” Kamen continued.

Eric Balchunas, an ETF analyst for Bloomberg Intelligence concluded: “Sometimes hedge funds look at Tesla and Ark, and think ‘This is just way too much and I can make a killing here.’”

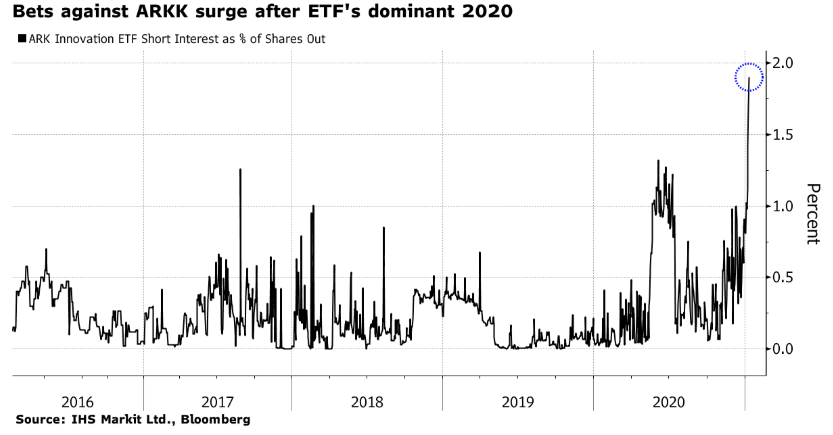

Recall, at the beginning of 2021, we noted that short interest in Wood’s funds had “exploded” amidst their rise in 2020.

And while shorts may have been paid modestly in 2021 so far, with ARKK about 30% off its highs, Wood’s ARK hasn’t sank just yet. Days ago we wrote that Wood’s strategy of selling liquid tech names in order to rotate into smaller, more “speculative” names has miraculously held up, so far, in 2021.

Despite selling some of her largest holdings, ARK “no longer holds a stake bigger than 20% in any stock,” Bloomberg reported this week. The firm’s largest holding, formerly 21.3% in Compugen, is now down to 17.2%.

Nikko Asset Management has a minority stake in ARK and the number of stocks where the two asset managers own more than 20% has fallen to 8 names, from 10.

Tom Essaye, a former Merrill Lynch trader, told Bloomberg: “This is an evolution a bit — Ark accepting it’s a large fund-family now. It makes sense that especially in some of the smaller cap names they are reducing that concentration. How much money you put to work in the smaller names can alter the risk-reward calculation.”

ARK’s flagship “Innovation” fund is down more than 32% from its peak on February 12, but outflows haven’t yet been rushed. This has allowed Wood the time for “an orderly adjustment of positions”.

Todd Rosenbluth, head of ETF & mutual fund research at CFRA Research, commented: “My fear was that investors that were relatively new to the strategy would see weak performance and then pull out just as management had increasingly favored some of these smaller companies. But because investors have stayed relatively loyal, they have not had to make changes to the portfolio to meet client redemptions.”

Tyler Durden

Thu, 05/27/2021 – 15:00

via ZeroHedge News https://ift.tt/3oW7ntg Tyler Durden