The Short And Long-Term Bull Cases For Ethereum

![]()

OVERVIEW

Thesis

-

Long term: sustainable growth, huge TAM, superior products, scale economics shared, underappreciated due to complexity, and mispriced as a “young bitcoin”.

-

Short term: Upcoming gross supply/demand mismatch given structural outflows of supply enforced by the London fork (EIP1559) and the phased Ethereum 2.0 rollout. Short term (18 months) upside on flows alone.

Big questions

Can it scale to facilitate many, frequent, complex transactions?

- Yes, Eth2.0 plus rollups cuts gas fees to viable levels where cost/Stx outcompetes payment processors and computation cost/byte will compete around 2022 with software and infrastructure providers when a premium is afforded to verification. Transaction size, latency, and frequency out-competes existing payment players.

Will it be better than existing alternatives (blockchain and not)?

- Yes, block-chain P2P is a superior model with a lower cost base, better security, better ecosystem incentives, equivalent or better transacwbility, and its interoperabilixy enables more innovation across a wider TAM.

Key risks

-

London/Eth2.0 forks do not get passed.

-

Short-term sell pressure forces downward volatility, liquidating existing players and preventing narrative adoption.

-

Regulators cripple fiat onramp chokepoints.

-

Strong competition from other Layer 1’s.

* * *

This report originally began as a slide deck. If you’d prefer it in that (far messier) format, here we are:

Monopolies with Growth – Ethereum

There is already copious Ethereum literature out there; my work leans heavily on it. This essay is intended as a summary of existing theses and a primer on key concepts, more than a particularly novel standalone. A disclaimer, my background is in law and finance, there are bound to be several technical issues below. If you notice them, please point them out to me. Please see the deck for sources and references. If I’ve left anyone out and have used your work, please let me know on twitter and I’ll link you ASAP.

The layout of the essay is as follows:

-

The Pitch: A Quality Company

-

The Pitch: A Special Situation

-

The Basics

-

DeFi, NFTs and DAOs

-

The Real World (scaling is discussed here)

-

Valuation

-

Parting Thoughts

The Pitch: A Quality Company

Ethereum is somewhat like a high quality “company” with a win-win ecosystem, which is trading at a pessimistic valuation. It’s deeply resilient, carries sizeable optionality, and – with the upcoming forks in August and December/early 2022 – it also presents a “special situation” with expected upside volatility.

As a 10 second primer (we’ll review the basics later), Ethereum is the protocol that underpins the decentralised finance (DeFi) movement, where users transact peer-2-peer without 3rd parties like banks. It also underpins the non-fungible token (NFT) movement, which creates digital scarcity for objects like art and certificates, and the decentralised, autonomous organisation (DAO) movement, which enables groups to join up in new ways to achieve certain preset goals.

Source: VanEck

Same page? Cool. Back to The Pitch.

Quality is a subjective metric. Usually agreed requirements are talented management, favourable unit economics, and a sustainable advantage over competitors. It gets even better when that company has provable innovation in their product and adapts to continually find the best product-market fit.

In the wake of Big Tech’s earnings, I’ve seen several tweets about “increasing returns to scale” and how “good companies surprise to the upside”. This essay will hopefully convince you that Ethereum – like any good company – exists well within that scale-advantaged world and has historically (often) surprised to the upside.

While Vitalik Buterin is the founder and face of Ethereum, the core development team exists worldwide in these decentralised clusters. Some of the smartest and most driven people I know are now working in crypto.

Blockchains are now sucking in top-tier Silicon Valley tech talent faster than any boom since the Internet.

— Naval (@naval) March 6, 2018

The “company” also has platform-like unit economics, with a hyper lean cost structure (post the Proof-of-Stake merge) where most participants are well-incentivized owner-operators. One of the key differentiators of a quality company is a win-win ecosystem. Both the dynamics of the ETH token and the dynamics of a scale-economics-shared platform mean that Ethereum is one of the least zero-sum ecosystems out there.

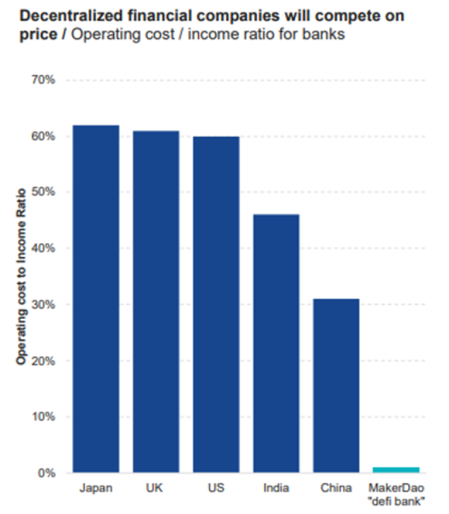

With an operating cost-to-income ratio around 20x lower than traditional banks, the lower legacy costs in Ethereum mean that there are hefty cost savings passed on to the end user. Add to this that as users and developers usually hold ETH themselves, they accrue value like shareholders. It’s like AWS, but you pay and get paid in Amazon stock for using it.

Ethereum has a far lower (and decreasing) take rate than many internet companies, has grown at several times the pace, and is trading at a similar forward price-to-sales, and a PEG of 0.03, compared to the software/finance average of around 2.5.

Source: VanEck and Aswath Damodaran

Roughly 80% of all decentralized apps (dApps) are being built on the Ethereum protocol, all of which are built to interoperate with each other. The more of these dApps that are built, and the more they interact with each other, the more entrenched Ethereum’s network becomes. Add to this the multi-year track record of Ethereum developers upgrading their product, and the hefty amount of innovation being built by non-Ethereum developers on the protocol, and you have a highly adaptive ecosystem.

In Greek mythology, Hercules faces down and slays the Hydra – a nine-headed water-snake-like beast. For every head of the Hydra Hercules cut off, the beast grew several in its place. The Hydra is a perfectly anti-fragile animal. Each time it is damaged, it becomes more dangerous. Like the Hydra, the Ethereum protocol has proven to be highly anti-fragile. Each time a protocol was hacked, a bug exposed or a dApp blew up, several more grew in its place. In this essay, Anthony Bertolino makes the case for this exact analogy.

Ethereum’s innovation, anti-fragility, and widespread network effects are the foundation for its optionality in future dApp developments. Its product is superior to blockchain peers and traditional finance, and is increasingly competitive with compute providers. This is the foundation for its resilience.

As a technology, Ethereum faces stiff competition from the likes of Terra, DFINITY, Binance Smart Chain, Polkadot, Cardano… the list goes on. Each competitor usually has one or two things they do better than Ethereum (usually lower transaction costs or higher transactions per second). These teams are all rapidly growing, highly innovative, strongly motivated and cash flush. And none of them come close to Ethereum’s network. The technical advantages these protocols have usually come as a result of the centralisation of a particular process, but they are building off a far less adopted base and (some of them) have far higher node costs. The likelihood of any one of these protocols displacing Ethereum is low, given the network effects and the amount of innovation currently on the latter’s platform, while the likelihood of Ethereum continuing its trend of lowering costs, decreasing take rates and improving throughput via Layer 2 solutions is tough to bet against.

Source: VanEck

So how superior is it to non-blockchain alternatives? I’ll get into the benefits of decentralisation, P2P, the “ultrasound money” meme, and the individual value-adds of DeFi, NFTs, DAOs and other dApps later. Off the bat though, the big question facing Ethereum is its ability to scale in competition with off-chain payment infrastructure, and off-chain compute providers.

Source: David Hoffman

Currently, it’s not great. Costly gas fees prohibit frequent transactions and complex code. To make Ethereum viable, throughput needs to increase, and transaction costs need to compete with other software development platforms. Beyond this, decentralisation and security are just two features in a stack of many that are needed. A thriving digital economy has many other equally important requirements (ease of use, real-world integration, utility-cost platforms, stability and predictability, state-adoption, etc.). While Ethereum is gaining these rapidly, existing alternatives already have these in spades. A large percentage of non-crypto-native adoption rests on how well Ethereum competes on these factors, not how decentralized or secure it is.

To get to the point quickly: The rollout of Ethereum 2.0 and the scaling solutions being built will get Ethereum to a competitive level within the next 12-18 months. Ethereum currently outcompetes all alternatives on interoperability, and cost per transaction when the transaction requires absolute validity (such as for payments and value-transfer).

It is possible folk will pay a premium for the decentralisation and data privacy, but even with Eth2.0 and the scaling solutions, it will still be around 10x more expensive than centralized, off-chain alternatives for computation. Speculatively, future scaling may solve this. Notably, Ethereum will likely never be competitive as a storage platform. It may one-day compete by outsourcing storage to side-chains, but that is speculative for now.

As we go through the essay, I’ll unpack much of what has been briefly outlined above. However, it is my view that the mental model many investors have been using to view Ethereum – as a young Bitcoin, lumped together with the rest of this “crypto crap” – is misinformed. So far, I’ve suggested a secondary model – a company – through which to filter Ethereum. However, this does not do it much justice either.

In his excellent essay, A New Model For Money, David Hoffman makes the case that Ether is a “triple point asset”. It serves as a consumable (like oil), a capital asset (stocks), and a store of value (gold) simultaneously. It is this dynamic that enables the second “special situation” part of The Pitch: that Ether will be hit by an unprecedented supply squeeze.

The Pitch: A Special Situation

This part is really just a summary of Nikhil Shamapant’s work. I highly recommend reading it firsthand.

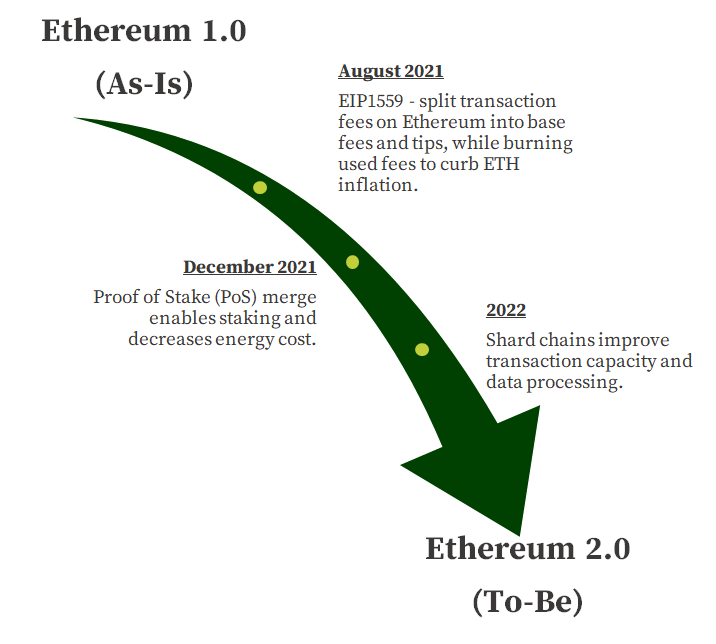

Below are the key forks coming to the Ethereum protocol. The August fork (EIP1559) is known as the “London” fork, and the Proof-of-Stake is the “merge”. Both are expected to notably improve the transaction costs and decrease supply.

Source: Finematics

In a nutshell, the base of the supply squeeze comes from the combination of EIP1559 & the Proof-of-Stake (PoS) merge. In a staking-based chain there would be:

-

A decrease in miner sell-pressure (estimated to be around 22 300 ETH/day), as miners are no longer required to validate transactions, and no longer have to recoup energy costs,

-

plus a decline in supply (~2% per annum) caused by burned gas fees,

-

plus a structural outflow of supply as more ETH holders stake their ETH for yield (from roughly 12% of ETH currently staked, to >30% of ETH staked post merge).

The selling pressure is estimated to fall to roughly 2 600 ETH/day, a ~90% decrease from current levels. Combine this with the decreased float (as a result of the structural staking/DeFi supply outflow) and it’s almost inevitable ETH will become more volatile. Why this volatility is likely to be to the upside is because:

-

Current demand pressure will likely exceed future sell pressure when sell pressure drops.

-

Demand inelasticity comes from passive inflows via upcoming ETFs.

-

Price appreciation leads retail narrative adoption of “internet money”+ staking yields.

-

There are increasing retail onramps (Visa, PayPal).

-

Institutions are already familiar with BTC.

Two addendums to this thesis are that groups like Lido facilitate the creation of a liquid derivative market for staked Ether (you give Lido ETH, they stake it, they mint a stETH token, you can trade or lock up your stETH in DeFi protocols). This allows for more ETH to be staked, while allowing those who wish to monetize their staked Ether to do so without having to unstake the asset. It also makes staking one’s ETH a lot easier.

Quick dive into the mechanics: Taking the place of miners, staked ETH is awarded a yield by the protocol for securing the protocol – by validating transactions and “staking” your Ether on the fact that that your validation is accurate and true. This yield means staked ETH (or, stETH) is worth more than unstaked ETH as it is essentially ETH + a capital yield.

The interplay between these derivatives means there are arbitrage opportunities to make sure ETH and stETH never deviate too far from their relative value. However, the fact that stETH offers yield means that most rational actors will swap their ETH for stETH, and then swap/sell/lock-up that stETH for a yield-on-yield. The incentives here make it likely the original stETH yield (offered by Lido/the Ethereum protocol) will trend lower over time. Staking yields of <2% are the minimum, which would only occur when 90% of ETH is staked.

The benefit of the ETH/stETH dynamic means that institutions – who were previously pretty locked out of illiquid situations – will be able to take advantage of ETH as they come to understand the economics. It also means that folk in need of liquidity now no longer have much of a justifiable reason not to stake their ETH. The result? More staked ETH.

Sidebar: if you are wondering where all this Ponzi-like yield is coming from, it’s really just the regular value created by liquidity provision to regular markets. Only, it is now accruing to users, rather than being absorbed by the legacy costs of the banking system.

Turning to the final part of The Pitch, the valuation, you’ll find ETH pretty tough to value properly. Analyst estimates range anywhere from $5 700/ETH (using the stock-to-flow model popularized by Bitcoin), to over $150 000/ETH which Nikhil reckons is an achievable price target during peak reflexive mania caused by the supply squeeze above.

To summarize: Buying ETH in the next 18 months is a special situation. Staking ETH for the long term is a quality asset at a pessimistic valuation.

The Basics

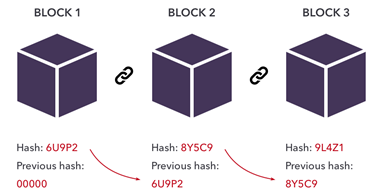

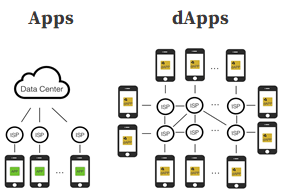

To understand Ethereum, you need to first understand decentralised computing and what Bitcoin was created for. As a rough definition, decentralized computing is a computer application, which creates some useful result for its users, can be run simultaneously on many computers around the world rather than on just one central server, and the network of computers can work together to run the application in a way that avoids trusting the honesty or integrity of any one computer or its administrators.

Bitcoin was the first successful application of this. Within Bitcoin, three core innovations were embedded:

-

Peer-to-Peer networking. Nothing new here – think BitTorrent,

-

Blockchains. A fairly novel way of storing data (new, but not revolutionary),

-

Consensus mechanisms. This was the game-changer. Bitcoin relied on a proof-of-work system as the mechanism through which networked computers agree on and record changes to a shared set of data.

It was the Proof-of-Work consensus mechanism that enabled Bitcoin to ensure agreement across the blockchain: As miners must pay for energy costs, they are incentivized not to waste energy validating transactions nobody else will agree with. The chains which have the most validations are definitionally the longest chains. Each linked block represents the work done to verify those transactions. The longest chains are the most valid, thus agreement is arrived at by proof of work done.

Decentralized computing was designed by Satoshi Nakamoto to solve the value-transfer layer of the internet. In the wake of 2008, Satoshi believed that the current value transfer protocols, which require trusting 3rd party authentication and incur unnecessary fees, are insufficient for transacting during the Internet Age. Hence Bitcoin was originally digital, peer-to-peer cash. The protocol doubled however as an identity verification mechanism, albeit one that verified the identity of bitcoin (small “b”, the output and medium of exchange for Bitcoin the protocol).

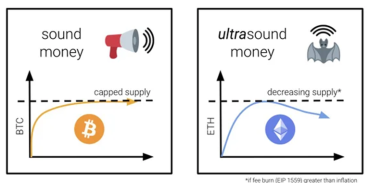

It is this second mechanism – the ability for transparent, publicly-owned identity data verification – that has become the focus of the 2nd generation blockchains (of which Ethereum is the foremost). Currently, the main use case for blockchain tech is speculation. The next main use case is for value storage – the “sound money” and “ultrasound money” memes which people use to argue for Bitcoin and Ethereum respectively. Increasing numbers of folk believe crypto has a better value proposition here than gold or fiat.

Ideologically, Bitcoiners tend towards a libertarian view, espousing Mises, Rothbard, Spitznagel, and Hayek. The belief here is fundamentally that decentralisation enables politically neutral individual sovereignty, which is a worthwhile pursuit. They usually hold that Bitcoin’s simplicity makes it superior at storing and transferring value, and little else. The base layer is minimal by design, having lower barriers to access running a node and rather scaling through Layer 2’s like the Lightening Network. Thus, Bitcoin’s path dependency, security, decentralisation and its Lindy-ness as a cryptocurrency make it the best (and only, if you’re a maximalist) option among cryptocurrencies.

Source: Notboring

However, stepping past the digital cash/store of value argument for a second, fringe use cases of decentralised computing include a growing replacement to the traditional finance system – DeFi, and the growing community around digitally scarce goods – NFTs. These are almost exclusively built on Ethereum.

Like Bitcoin, Ethereum is an open-source network and is built to validate transactions. Unlike Bitcoin, Ethereum is Turing complete. This means that, where the whole point of the Bitcoin protocol is to validate transfer of Bitcoins and to produce little bitcoins as reward for those validators, the whole point of Ethereum is far broader. Ethereum is designed to enable folk to build on top of it, and is capable of validating any kind of transaction or set of transactions (called smart contracts). It’s programmable. If Bitcoin is the HP-35, Ethereum is Microsoft Excel.

Excel is just one of several useful analogies for understanding Ethereum. It’s also like: a bunch of distributed and online vending machines, digital oil, communally-owned AWS, the TCP/IP of Web3.0, and like contract and property law found a Bloomberg terminal.

Source: VanEck

So how does Ethereum work? Before we get there we need to unpack smart contracts. These are the auto-executing and immutable agreements that underpin the Ethereum ecosystem. Think of them as a bunch of If-Then instructions. Developers code smart contracts using Ethereum’s programming language (Solidity) and upload it to the Ethereum system (the Ethereum Virtual Machine). Everyone running the application as a verifier (called a “node”) gets a copy of that code. When users transact using those contracts, all nodes must verify the outcome per contract rules. This verification process is the computation that blockchain relies on.

Each miner/staker is continually validating blocks of transactions. Valid blocks are added to the chain. “The chain” is the history (and current state) of all transactions and smart contracts. To stop people from overclocking the compute systems, users must pay gas fees as computational credit. Gas is purchased using Ether (also denoted ETH). Under Eth1.0, miners are paid in gas fees and protocol-issued ETH to validate and tipped when users want their transactions processed first. Under Eth2.0, those gas fees will be burned (like a share buyback) and tips will accrue to people who are staking their ETH. For a nuanced take on this model, here is a good essay by Joel Monegro.

Source: EthHub via Lyn Alden

Ethereum’s monetary policy is a pretty complex topic, having been hard forked (crypto-speak for “changed”) roughly 10 times before. At the moment there’s a roughly 0.2% issuance/inflation rate. These newly minted ETH are given to miners. After the London fork (EIP1559) and Eth2.0’s rollout, the issuance rate will be determined by a Staked Ether/Total Ether algorithm, incentivizing the added security where needed with higher staking yields (issuance rates). Theoretically, the net effect will be a rules-based, deflationary, throughput-enhancing policy.

“If crypto succeeds, it is not because it empowers better people. It’s because it empowers better institutions.” This is one of my favorite quotes from the founder of Ethereum, Vitalik Buterin. Ethereum’s programmability is its defining trait. Its transactions are faster and cheaper than Bitcoin, and its network is more secure and decentralised than alternatives. It is highly energy efficient, has seen an absurd amount of innovation in the last 24 months, and has the widest variety of applications built atop it – including some by multiple central banks. However, one could say AWS ticks most of those boxes too. AWS doesn’t falter, latency is minimal, innovation is high, data transactions are cheap and abounding. The difference? AWS isn’t decentralised. And AWS doesn’t align incentives nearly like Ethereum.

Source: VanEck

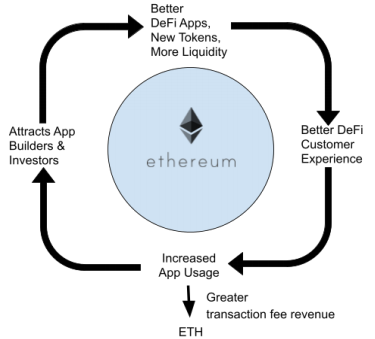

With gas fees being mandatorily paid in ETH (cf. economic abstraction for why ETH and not something else), developers and users alike must own ETH. This means they benefit from token appreciation. Beyond this, it also means that the more ETH is worth, the harder the network is to attack. While no dev practically thinks “let me HODL ETH so my project is secure”, they almost certainly think “let me encourage people to look into building dApps on Ethereum so the ecosystem grows”. For every dApp that is built on Ethereum, more gas fees are paid, more interoperability opens up, and the more the network is secured, increasing the attractiveness of building on Ethereum. This is the core positive feedback loop in the Ethereum protocol.

However, if too many teams join too quickly, gas fees surge, preventing hyper-adoption. This negative feedback loop governs the protocol, as hyper-adoption would likely see an equivalent surge in rapidly released code, rife with bugs and poor UX, hogging scarce network space from the more useful, resilient dApps. Together, these positive and negative feedback loops govern both the growth of the ecosystem, and the trajectory of value accrual. Historically, we’ve seen far more value creation at the app/platform level (like Google/Maps) than we have at the infrastructure level (HTML/GPS). The dynamics I’ve just outlined ensure the Ethereum protocol will always have to be worth more than the dApps built upon it, lest the protocol face a 51% attack purely to rob the dApps of their value.

Beyond being gas fees and the staking asset, ETH is also used in DeFi as a reserve asset, as collateral, for financing, and as a medium of exchange. Certain retailers accept ETH, and ETH is the default unit of account for digitally scarce goods (NFTs/on-chain in-game items). The combination of all of these means ETH is currently a highly transactable asset, unlike Bitcoin which is predominantly just HODL’ed.

Whether folk will want to transact a rapidly appreciating token is a curious concept. In BTC’s case the culture has decided “No. Not until we’ve monetized the new financial system”. In ETH’s case, people are seemingly deciding “Yes. If we believe what we are buying is worth more than the token”. But, what they are currently buying (NFTs, DAO governance tokens, DeFi swaps etc.) is all caught up in a wave of higher-ETH-higher-NFT-prices, and is also all serving to push the ETH price higher through ecosystem growth and gas fee demand.

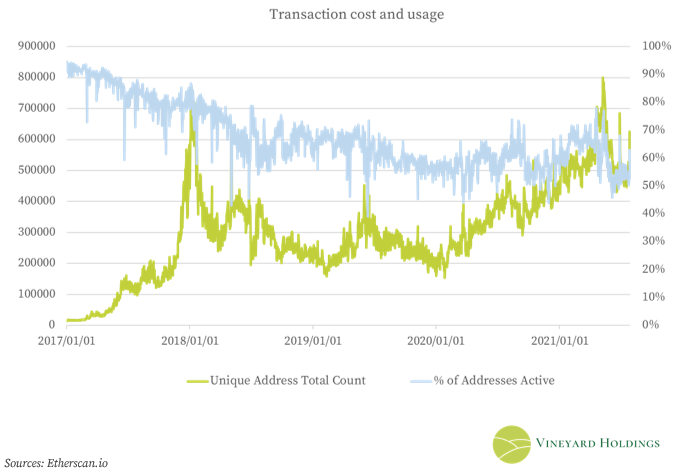

The above picture can mean one of several things. It could mean ETH is being seen increasingly as a store of value, or a speculative instrument by HODLers. It could mean that more users are transacting on centralised exchanges. Or it could just mean that there were a bunch of people who emptied their accounts of ETH over the years and there are now a stack of unused wallets. It is tough however, to see the number of unique addresses up nearly 40x since the start of 2017 and say Ethereum’s network is not growing.

I’m partial to Allen Farrington‘s posed question: “What would it seem like if it did seem like a global, digital, sound, open source, programmable money was monetizing from absolute zero?“. I’d ask similarly what it would look like were an entire financial ecosystem to monetize from the ground up. The flow of value which makes ETH number go up makes sense to me:

-

Growth in Ethereum ecosystem → more transactions → more demand for gas fees → more demand for ETH.

-

Adoption of Ether (or BTC on Ethereum) as money/store of value → more demand for ETH.

-

Users stake ETH → less supply.

-

Staked ETH generates yield as it’s a share of the Ethereum network and a claim to Ethereum’s fees → more people buy ETH to stake.

What is less clear is what the real-world use cases of this technology are. In a classic response to an interviewer, Steve Jobs opined that “… you’ve got to start with the customer experience. You can’t start with the technology and try to figure out where you’ll try and sell it.” Herein lies my biggest conundrum with Ethereum: the customer experience is, while improving, still pretty shoddy. My Mom is never going to go through the KYC for Binance, open a MetaMask wallet, send some ETH she purchased on Binance to the wallet, stake the ETH on Lido, and start liquidity mining on Curve. She doesn’t want to know about gas fees, stock-to-flow ratios, or protocols. This is all exciting technology, but the use cases are so far from customer-centric that it’s still a long way off from mainstream adoption.

DeFi, NFTs and DAOs

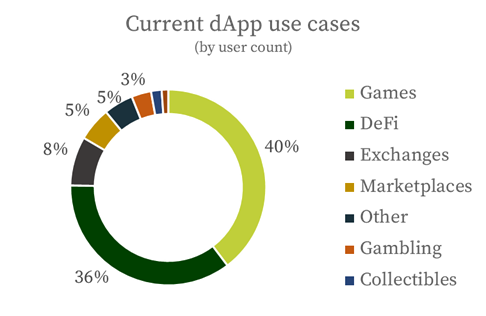

“The Ethereum ecosystem has to expand beyond just making tokens that help with trading tokens.” – another fantastic quote from Vitalik. Today, the bulk of crypto exists in traders swapping one token for another on exchanges in circular bouts of zero-sum speculation and inter-currency arbitrage. By USD volume transacted, DeFi accounts for 99% of the ecosystem value. Yet in total number of transactions made, gaming makes up 81%. Similarly, NFTs have been accused of being speculative art bubbles and much of the media around 2021 crypto has centered on these odd-looking digitised pictures.

DeFi, NFTs, DAOs, these are all example use cases for decentralised applications (dApps). DeFi is an ecosystem is made up of a collection of finance-like dApps, NFTs are on-chain strings of code which are bought, sold, minted, and owned using dApps, and DAOs are organisations usually governed by, operating through, and interacting with dApps.

Essentially a set of smart contracts, dApps are currently limited to relatively simple use cases (a structural result of the high gas fees incurred with more complex code and computation).

This is arguably the key limitation in distributed computing: since the state management system is – by definition – in more places than its centralised counterpart, computation costs will inevitably be higher. Since each action a dApp takes on-chain (minting NFTs, transacting, interfacing) incurs gas fees, the cost of computation increases exponentially with code complexity.

This problem is well known in the Ethereum community. Ultimately, it seems the community has opted to follow the scale-through-technical-solutions approach, optimising for decentralisation, programmability, and interoperability over low-cost fees. The rationale here is that the former are either built at the base, or they are non-existent. So the fee solutions? Improve technical second-layer building blocks and lower transaction fees through supply/demand mechanics to the point where they, like gasoline for your car, are materially negligible.

Crypto enthusiasts will tell you that DeFi may one day allow folk to pay, send remittances, buy and sell things, apply for loans and mortgages, crowdfund startups, and everything the existing financial system does. NFTs will theoretically bring all certification on-chain. From digitised IDs, title deeds, state documents, multi-game digital goods, and IP protection to security infrastructure, data storage, supply chain optimisation and censorship-resistant social media, crypto may seem a little Shangri La-esque in its promises. While the potential for this is all there, it’s good to temper the hope with a little objectivity.

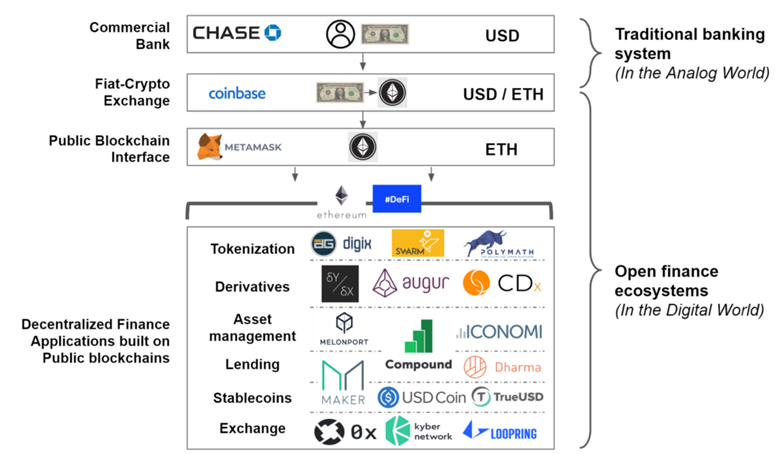

DeFi

Decentralized Finance (DeFi) is a developing ecosystem of financial dApps aiming to displace the existing financial system with one not reliant on trusted intermediaries like banks. A common crypto meme is that DeFi is Money Legos composing pieces of the financial system together.

Source: Andrew W.

Roughly 80% of DeFi occurs on the Ethereum blockchain and uses ETH as the reserve asset. The core mechanisms here are that users must lock up ETH and another asset in liquidity pools to provide the ecosystem with liquidity. Folk who want to swap one token for another must put their ETH in the pool and get to take out the other token. For this privilege of swapping, they pay fees. These fees accrue to the liquidity providers.

Sometimes folk want a non-ETH token because they like what a particular project is doing, and would like some say in that project’s governance (these projects are called DAOs, and DAOs are governed by token holders in a similar way to public companies and shareholders). Other times, they just want the other token because they think they can trade it at a profit elsewhere. While this all seems wildly speculative, remember that this is very similar to what the big banks do with debt and derivatives normally.

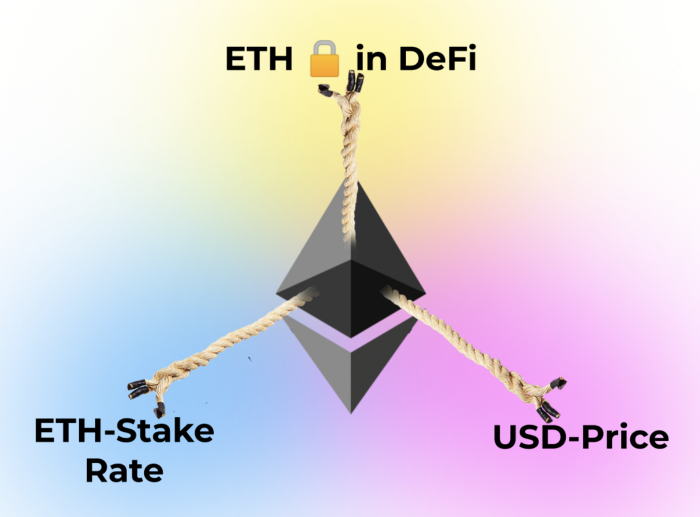

Locking something up in DeFi is different to staking your ETH to secure the Ethereum protocol. The ETH stake rate offers the “risk-free rate” for DeFi. The more ETH locked in DeFi, the more the Ethereum protocol recognizes the need for security (via the Value Staked/Total Value function) and increases ETH stake rate. The inverse is true too. The more ETH staked, the higher the cost of liquidity in DeFi, so folk are willing to pay higher fees and increase the yield of liquidity pools.

Alden and Pfeffer have questioned whether Ethereum protocol adoption causes ETH token appreciation. As ETH (protocol and/or asset) are adopted in DeFi, the provision of tokens (LP or ETH) both transacts on-chain (incurring gas fees) and reduces staked ETH (causing the ETH stake-rate to rise). The net effect of this is more demand for ETH (in addition to the fees) in the same way a rising treasury yield attracts investors. If these investors are pulled from DeFi (unlikely, as yields there are better), then the protocol adoption may not cause ETH appreciation. If they are pulled from outside crypto, it’s more likely ETH will rise as adoption is then not zero-sum. David Hoffman and Anthony Sassano describe this dynamic in more detail in their respective essays.

Source: David Hoffman

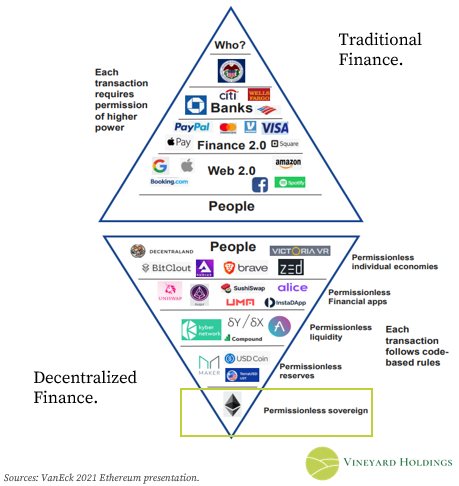

So what does DeFi offer that the traditional world doesn’t?

Firstly, it’s permissionless. Theoretically what this means is that there is no difference between a Jeff Bezos and a homeless man in Cape Town. Because there is no KYC/AML, there are no limits on who can participate. In practice, what this means is that you currently need a working Internet connection, the time and willingness to spend a good week or more familiarising yourself with the various risks, platforms, and projects, and you need sufficient money that a couple trial-swaps won’t cost your life savings. Good for the developed world, but still a work-in-progress for “the unbanked”.

Self-custody and control will also theoretically disperse the effects of a systemic failure (ala 2008 or LTCM’s blow-up). The phrase “not your keys, not your coins” is thrown around a lot in crypto, but in reality, not many non-crypto-native folk want to think about custody. They’d rather, say, keep their money in a bank which their friends tell them is safe. For crypto to move mainstream, it needs to shed the “we are hackable, make sure you look after yourself here” stigma, and begin to ingrain the non-custodial tech within a better UX.

Thirdly, it’s interoperable. Although my Mom may not want to, I can stake my ETH on Lido, lock up my stETH in a Curve liquidity pool, then use my liquidity tokens (the things that let me reclaim my stETH) as collateral on MakerDAO and buy little in-game animals in Axie Infinity, the on-chain game which rewards me in AXS for playing. AXS, in turn, are swappable for ETH. And the cycle begins again.

If this sounds wild to you you’re not alone. Right now, this kind of interoperability looks gimmicky and Ponzi-like, but it doesn’t take much imagination to see the kind of innovation that can come from this kind of open platform.

DeFi is also inherently higher-yield. The current narrative is “high yields for early adopters”. While it is unlikely high double digit yields on blue-chip tokens are sustainable, users should not be anchored to the non-crypto yields in traditional finance, which must cover legacy costs and rent-seeking. The combination of permissionlessness and interoperability means there’s likely to be several opportunities for new business models, financial products, and ways of working.

Source: VanEck

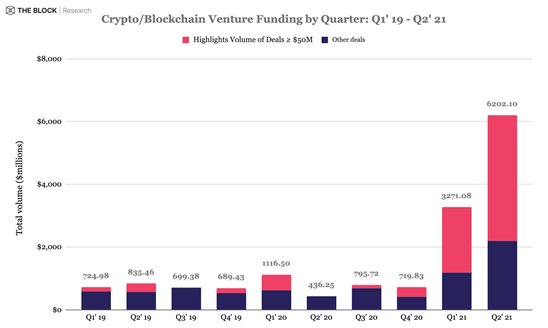

As the Hydra and AWS-but-you-get-paid-in-Amazon-stock analogies hopefully showed, DeFi is also highly antifragile and has far better incentive alignment. In recent months, stablecoins (which enable more real-world interfacing) have made regulatory headway and are spurring adoption. Lastly, the ecosystem is cash and talent flush with highly motivated developers and users, and venture funding has surged in recent quarters.

Source: VanEck

Economically, a surplus of cash means incremental capital allocated to that industry carries lower ROIC than alternatives. This essay is not pitching allocation to any particular project – many crypto startups are at heady valuations. However, because the bulk of the value is captured at the protocol level, and because of the long runway for growth that DeFi contains, Ethereum remains a high ROIC bet on indexing this industry.

Two current causes for concern in the DeFi space revolve around the limited real world use cases, and (ironically) the centralisation of many of the dApps. Many of the dApps are reliant on 3rd party node-aggregators (like Infura) who often run nodes via existing cloud servers like AWS. This is because the time, money, and storage cost of running a node that transacts can be too high for small-time developers. These chokepoints are vulnerabilities in the ecosystem.

Regarding actual use cases, the major one today is yield-farming and KYC-avoidance. Real world utility (like insurance, mortgages, stable deposits, uncollateralized loans etc.) should come with time. However, many of these would require a form of digital identity (like DIDs) and possibly a synching with the existing legal system. In the meantime, improving onboarding UX and developing solutions to code-bugs and lost admin keys would go a long way.

NFTs & DAOs

For a more in-depth look a each, I recommend reading through a16z’s collection on NFTs and Packy McCormick’s The DAO of DAOs .

Non-Fungible Tokens (NFTs) are the tokenisation of digital assets onto a blockchain – they make previously copyable things, scarce. If DeFi is money Legos, NFTs are media Legos. The bulk of current use cases are in-game items and digital art, but there are a number of start-ups focusing on the tokenisation of legal items like ownership certificates and IDs. Legally, NFTs are a gray area at best of times – can one really own a snapshot of a historic event? Yet, with the advent of concepts like the metaverse and the creator economy blooming in search trends, the law will likely play catch up shortly.

NFTs have skyrocketed in adoption over the past year. Setting aside speculative future use cases, right now NFTs offer fundamentally better economics for creators. In his canonical 2008 essay, A Thousand True Fans, Kevin Kelly outlined why the Internet would change the dynamics for creatives: it would allow them to find, monetise, and connect with the extremely dedicated few in their fanbase, rather than keeping them tied to appealing to their entire audience – many of whom will only ever be mildly interested. While some of Kelly’s vision was realised in social media and Insta-celebrities, monetisation was generally limited to clunky adverts and inefficient sponsorships. One of the reasons why NFTs have blown up so much in the creator space is because NFTs enable creatives to focus on the fat tails.

Source: Taylor Pearson

While digital assets are usually downloadable, this does not damage the value of an NFT. Think of a photo for instance: in the same way a meme is only a meme when lots of people know about it, your ownership becomes more valuable the more people know about the original. Unlike the music industry where the pleasure comes from listening to a song, a bulk of pleasure of art comes from owning it. It is currently for this pleasure and the ability to resell that NFTs exist. In the art world, for instance, the concept of provenance – validating an artwork’s authenticity, origin, and history – is a costly and essential part of the art market. With NFTs, that entire process is automated and infallible.

While many NFT creators and buyers are crypto-native, companies like Momint are enabling creators to mint, buy, and display NFTs without needing to understand the back-end. This is a crucial step in bringing NFTs mainstream. The focus here is a good UX, no-fees, and an appeal to a wider fanbase through non-crypto influencers and personalities.

Two more great things about NFTs: they allow granular pricing, and they (like DeFi) remove rent-seeking from intermediaries and orthodox distributors who usually carry substantial legacy costs. More money to the creator, more ownership to the fans. Creatives can price NFTs individually, selling originals, limited editions, and other copies all at different prices and in different mediums. They may not need to take sponsorships, or rely on Patreon-like support, and the possibilities for new business models opens up. One of these models is the sale of an NFT which accrues royalties in perpetuity as a percentage of future sales or sales of derived similar NFTs.

Source: Chris Dixon

And what about DAOS? These are a little complicated – basically, DAOs are algorithmically governed groups of stakeholders who come together to achieve a particular goal or set of goals. The rules of the organisation are set out on the blockchain, with smart contracts governing everything from the flow of funds throughout the organisation to the incremental tasks allocated to stakeholders or processes, depending on how the DAO is structured.

The value adds of DAOs over orthodox organisations are their transparency, accessibility and, in many cases, automated decision-making. As the governing rules are transparent on the blockchain, anyone can view tasks and task rewards, examine the financials, and understand the incentives. Because DAOs are usually global, they are not a constrained by border controls, have lower barriers to entry, and have lower switching costs than existing organisations. If a DAO is not meeting member needs, or is evolving too slowly, members can disband quickly and form/join other organisations. Finally, DAOs, by virtue of their rules-based nature are a step towards AI-driven organisations. Whether this is a good or a bad thing is up for debate, but an immediate benefit is the hardcoded impartiality.

Source: Linda Xie

Crypto receives a disproportionate amount of hype, and many proselytisers would have you believe it is a “solve everything” type of asset. It is not even a single asset at all. I expect that over time the definitions of Ethereum, Bitcoin, and their peers will both separate from each other and crystalise into their own various use cases. Definitions will narrow, use cases will emerge, and the technology underpinning the hype will come to the fore. Until then, examining blockchains for their real world applications will hopefully prove useful. In doing this, three of the leading technologies coming off the Ethereum platform are DeFi, NFTs and DAOs. All three face growing adoption, and all three are built on a platform that – should that adoption continue – will keep bumping up against the limits of its capability.

The Real World

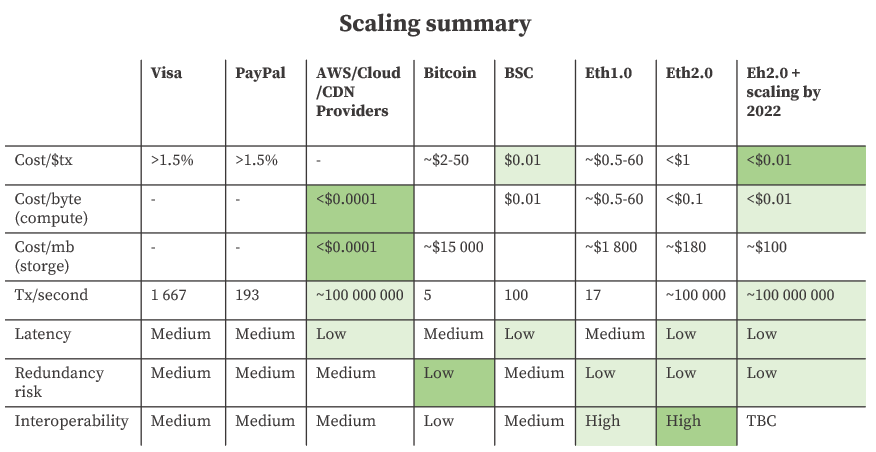

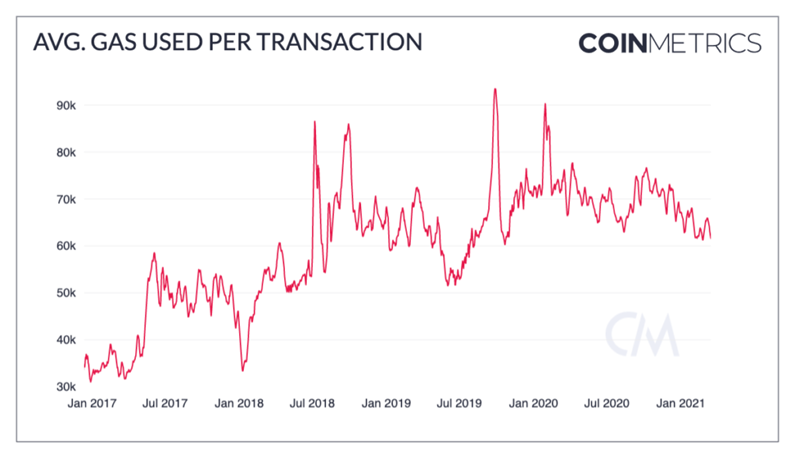

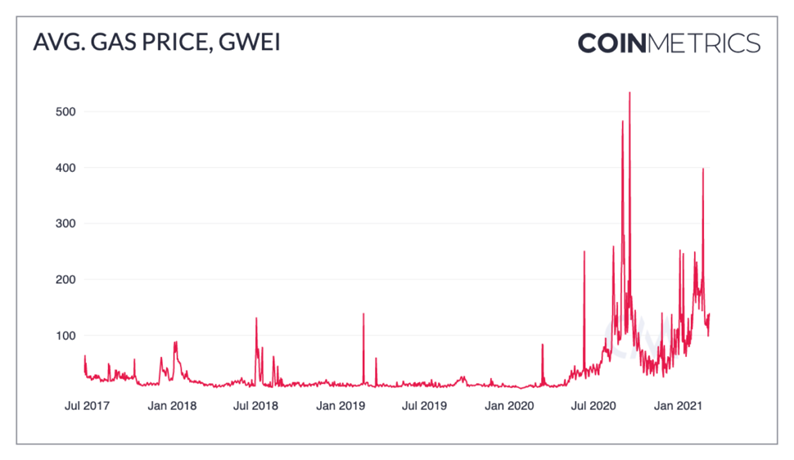

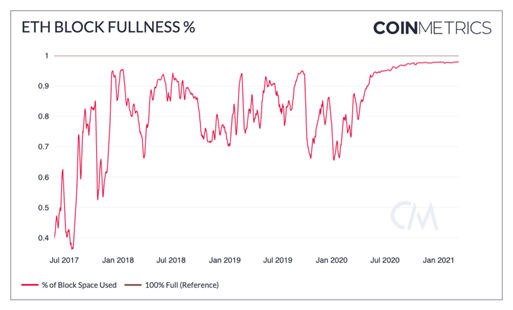

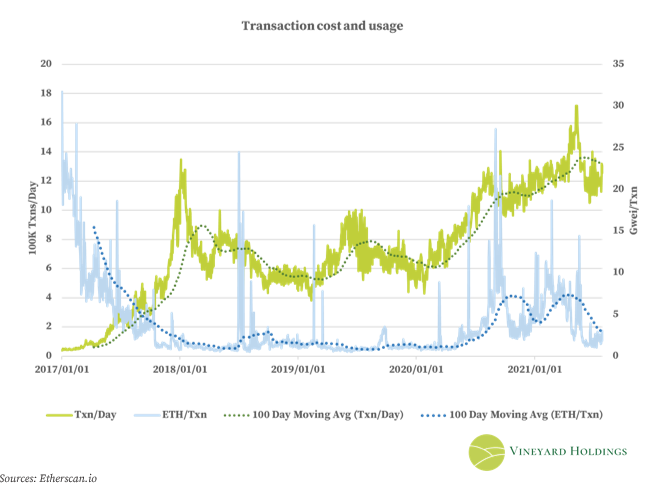

The main problems of Ethereum 1.0 are it’s inhibitively high gas fees (transaction cost), slow transaction time (time taken to complete a transaction), and low transaction throughput (amount of transactions per second). Any scaling attempt needs to balance the scalability, with staying secure and decentralized – the scalability trilemma.

The Scalability Trilemma

To compete with centralized alternatives, Ethereum needs to at least be as fast, as cheap, and able to handle as much data. Already Ethereum competes with existing payment providers on cost/txn size. However, Ethereum cannot yet compete with non-financial network providers and software companies (like CDNs and cloud providers) on cost/byte. Decentralized databases inherently require higher cost per transaction than centralized alternatives, because the number of “places” where the ledger state needs to be changed/maintained are greater. Where the transaction fee is a small percent of total transactions, this is no problem. But it is very costly to run complex smart contracts in series, where data (not money) is being transacted.

Source: CoinMetrics

Source: CoinMetrics

Source: CoinMetrics

Because DeFi is built on the idea of composability and interoperability (“Money Legos”), it’s vital that scaling solutions do not inhibit the innovation that these attributes bring. The two main ways of scaling are: improving the Layer 1 (Ethereum2.0) and building Layer 2s (like zk-rollups).

Currently, Ethereum1.0 lags several of the more centralised Layer 1’s (the base protocols upon which dApps are built). Eth2.0 however will likely outcompete many of them, and when Layer 2 (L2) scaling solutions are added it will be tough for the less developed chains to rival Ethereum without sacrificing decentralisation or interoperability.

Sources: SinoGlobal, Notboring, Bitinfocharts

I’ll take this time to note that while it’s likely Bitcoin and Ethereum stay around for a long while (the former as money and the latter as the platform), the future of blockchain is very likely multi-chain. Protocols like Solana and Polygon are already building crucial “bridges” between chains. This is both excellent for the ecosystem as a whole and for Ethereum in particular.

Source: Polygon

The more Ethereum can integrate with alternatives, the more it will lower gas fees and increase thoughput. This incentivizes building of dApps on chains which only interact with Ethereum when absolutely necessary. While in the short run this sacrifices gas fee revenue, it builds in resilience and key dependency on Ethereum for the long run. If every app interfaces with Ethereum at some point, even if minimally, then new developers will have little choice but to do the same or risk losing their interoperability.

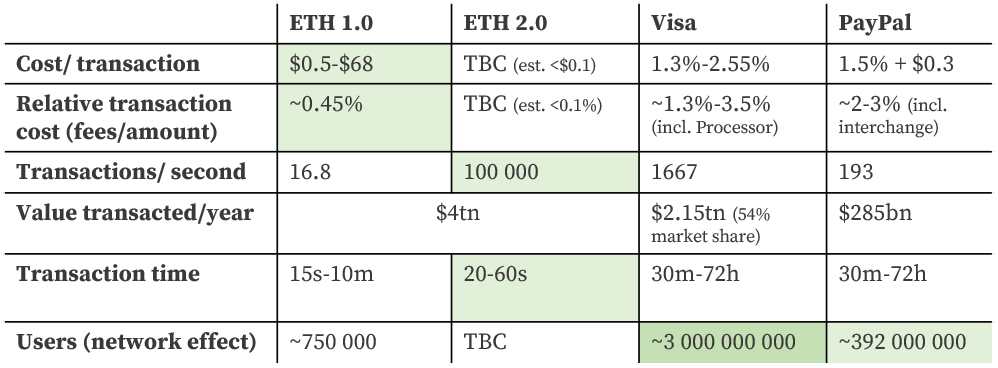

However, Ethereum needs to outcompete not only Layer 1’s but real world payment systems too. As a value transferal protocol, Etherum1.0 is only cheaper than Visa or PayPal. It is arguably more secure too, but with the incumbents security is only a risk at the systemic level. To compete Ethereum needs to process more transactions, at roughly one-tenth of the cost and time, and must be accepted by a roughly equal amount of people. With the rollout of Eth2.0 and where transactions are of more than, say $25, Ethereum is the clear technical winner. However, its network effect still severely lags the payment giants.

Sources: company financials, VanEck, Messari. 2021E used for Eth1.0 at $18bn revenue/$4tn transaction value, creditcards.com

For Ethereum to grow its network to a rival base, it will compete with the payment processes not just on technical ability, but on:

-

UX

-

Financial system integration (especially with the likes of Stripe, and B2B integrators)

-

Accurately forecastable cost, transaction value, transaction time

-

Public sentiment (merchant acceptance, asset credibility), and

-

Payment providers offering fraud protection, KYC/AML and having better legal protection.

While necessary for adoption, these elements are ancillary, and arguably far easier to build on top of a technically superior base.

If, as per Evan McFarland, “The meta purpose of blockchain is to be a decentralized internet. And the only way you do that is by replacing the cloud”, then Ethereum’s biggest challenge will be against scaled providers of compute infrastructure.

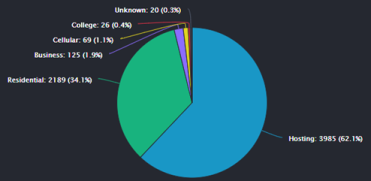

Currently, Around 60% of Ethereum nodes are run on either AWS, AliCloud and GCP, as the set-up costs for full scale nodes are expensive for individual users. Further, Most devices/browsers/app-stores run on MacOS, Windows, or Android, and with Facebook, Apple, and Google’s push into wearables, they are the leading players in home IoT as well.

Sources: ethernodes.org

To compete, Ethereum needs to beat Big Tech on compute, storage, and interoperability. It is well on track with the latter. With sharding and rollups, Ethereum may be able to compete on computation costs within 1-2 years, although this is still largely speculative.

Household compute is essentially a utility. Between CDN providers and cloud IaaS (like AliCloud, fastly or AWS) computation costs for centralised compute is virtually negligible relative to paying ETH gas fees. It’s possible that completely decentralized computation being at a premium to censorable/centralized compute might be a reasonable tradeoff for some developers, but if Ethereum hopes to become a genuine “world computer” then it will need to bring computation costs down accordingly.

On the storage front, Ethereum falls quite a bit further short with historic storage costs reaching ~$1.8k/MB of data stored, compared to CDNs or AWS which are virtually negligible (<$0.001). This is because the Ethereum blockchain was never intended to be a storage facility. In fact, making the protocol more storage friendly was one of the proposed forks that never achieved consensus. Were everyone to store every byte of data on-chain, nodes would require enormous capacity just to function. This would put the price of decentralisation well out of reach for many node operators – something untenable with the core of the value proposition. The solution here is to store packaged, encrypted and vital data on-chain and the rest in side-chains. This is safe, given that the off-chain data requires on-chain data for operation, so it is still decentralised.

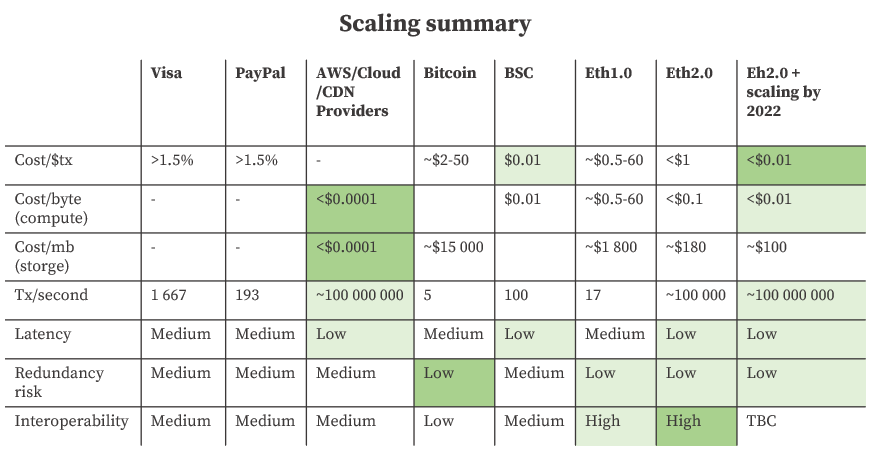

To recap the scaling summary picture (you’ve probably forgotten it by now) – Ethereum currently outcompetes all alternatives on interoperability, and cost/transaction when the transaction requires absolute validity. Ethereum will be competitive when used as a computation platform when a premium is afforded data privacy and decentralisation but will still be around 10x more expensive than centralized, off-chain alternatives for developers not willing to pay the premium. Speculatively, future scaling may solve this. Ethereum will likely never be competitive as a storage platform. It may one-day compete by outsourcing storage to side-chains, but that is speculative for now.

Sources: see slide deck, Amaznog.com, Ethereum.org

While Layer 1 and 2 scaling solutions can massively improve transaction times, lower gas fees, and expand throughput capacity, they bring their own problems. Without an interoperable “L2 bridge” layer like Polygon, L2 solutions can fragment liquidity and create excess friction when swapping between the different L2s thereby limiting interoperability.

Here is Vitalik’s take on the problems facing scalability:

“There are two ways to try to scale a blockchain: fundamental technical improvements, and simply increasing the parameters. Increasing the parameters sounds very attractive at first: if you do the math on a napkin, it is easy to convince yourself that a consumer laptop can process thousands of transactions per second, no ZK-SNARKs or rollups or sharding required. Unfortunately, there are many subtle reasons why this approach is fundamentally flawed.

Computers running blockchain nodes cannot spend 100% of CPU power validating the chain; they need a large safety margin to resist unexpected DoS attacks, they need spare capacity for tasks like processing transactions in the mempool, and you don’t want running a node on a computer to make that computer unusable for any other applications at the same time. Bandwidth similarly has overhead: a 10 MB/s connection does NOT mean you can have a 10 megabyte block every second! A 1-5 megabyte block every 12 seconds, maybe. And it is the same with storage. Increasing hardware requirements for running a node and limiting node-running to specialized actors is not a solution. For a blockchain to be decentralized, it’s crucially important for regular users to be able to run a node, and to have a culture where running nodes is a common activity.

Fundamental technical improvements, on the other hand, can work. Currently, the main bottleneck in Ethereum is storage size, and statelessness and state expiry can fix this and allow an increase of perhaps up to ~3x – but not more, as we want running a node to become easier than it is today. Sharded blockchains can scale much further, because no single node in a sharded blockchain needs to process every transaction. But even there, there are limits to capacity: as capacity goes up, the minimum safe user count goes up, and the cost of archiving the chain (and the risk that data is lost if no one bothers to archive the chain) goes up. But we don’t have to worry too much: those limits are high enough that we can probably process over a million transactions per second with the full security of a blockchain. But it’s going to take work to do this without sacrificing the decentralization that makes blockchains so valuable.“

Currently, the proposed scaling solutions improving the Layer 1 are Ethereum2.0 and EIP1559. The former will divide the chain into shards, each randomly served by dedicated nodes. This will reduce network congestion and increase transactions per second by creating what is effectively coordinated, new chains.

![]()

Source: Vitalik.ca

The second Layer 1 solution, EIP1559, will not directly enable better throughput or lower costs, but allows for more accurate demand/supply pricing with algorithmically variable fees optimising for throughput. This makes gas fees more certain, and lets developers budget better – hopefully also reducing congestion.

The Layer 2 solutions are generally protocols that collect transactions and batch them before putting them on the main chain. These include:

-

Rollups, which computes off-chain, but stores the outputs on-chain. These are still decentralised as the cryptographic output (which is needed to make sense of the data) is stored on-chain. Roughly, these are expected to constitute a ~10-100x scalability improvement.

-

State Channels are where participants “stake” ETH on-chain, opening up a separate off-chain channel wherein they transact freely and frequently. When the transaction(s) are finished, final data is stored on-chain and the ETH staked is reimbursed.

-

Side Chains are other blockchains (technically L1s) which are purpose-built to interoperate with Ethereum, and use “bridges” to port final data across. These are usually less decentralized and have alt. consensus mechanisms.

-

Plasma, which are mini “child” chains anchored to the Ethereum mainnet which can be checked by the mainchain for fraud. These chains don’t facilitate general computation, but can be used for more basic, preset activities (like token swaps and such) thereby taking some of the “grunt” work off the mainnet.

All considered, scaling is a focal point for many Ethereum developers with numerous independent projects working on solving the issue. There is a long way to go, and if Ethereum wants to hold its decentralisation as critical, none of the solutions will come easily. The optimistic news, is that while usage and capacity for transactions has been increasing, cost per transaction has remained relatively steady.

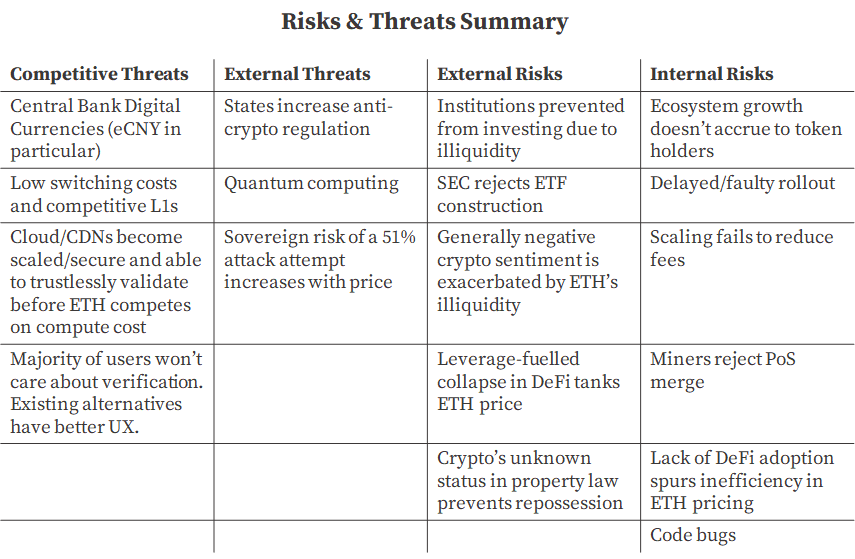

Risks & Threats

“… Speculators should understand that the base layer of Ethereum is still in alpha development, with rapid change in terms of its security model, monetary policy, and addressable market, at a time when competition in the smart contract industry is not insignificant.” – Lyn Alden

Thus far, this essay has tried to be as realistic and fact-based as possible. This segment is intended to be a brief overview of some of the major competitive, internal, and external risks and threats facing Ethereum presently.

Atop the list are central bank digital currencies (e.g. PBoC’s DCEP/eCNY). These are central bank issued tokens designed to serve as legal tender. Generally, they will be backed by the reserves the central bank holds and their public fiduciary duty – similar to fiat cash. These make sense for central banks on several grounds, including cost, efficiency, payment stability, information flow, economic monitoring, protection of sovereignty, and transmission of monetary/fiscal policies. One big hinderance to CBDCs is that they risk disintermediating the banking sector within a country, as many folk may believe their savings are better stored in a (possibly interest yielding) CBDC than in a bank. This would deprive the state of much of the leverage they have in affecting monetary policy.

Currently, China likely leads the CBDC development with their digital Yuan. This is rumored to be unveiled publicly at the 2022 Beijing winter Olympics. To quote from Goldman Sachs’ recent report:

“The DC/EP’s primary goal is to supplement or replace traditional physical cash; it will therefore not pay interest. The PBOC plans to adopt two-tier issuance—the PBOC will issue digital currency to commercial banks and require 100% reserves. If individuals or companies want to use digital currency, they must request a commercial bank or qualified payment provider to open up a digital currency wallet on their behalf, with authentication by the PBOC. From a technology standpoint, DC/EP will be based on a centralized ledger operated by the PBOC, in contrast to cryptocurrencies, which rely on a decentralized ledger.“

The threat that CBDCs hold to decentralised cryptocurrencies is more as cash than as a platform or computation-provider. While the eCNY may compete directly with Bitcoin, it is unlikely to be as programmable or as interoperable as Ethereum, thus unlikely to have as sophisticated an ecosystem develop atop it.

Three more brief competitive considerations are the relatively low switching cost for utility protocols, the disinterest of the masses in “verifying” blockchain code or transactions, and the price decentralisation incurs.

We’ve covered the cost of decentralisation ad nauseum, but to summarize: It is possible companies won’t want to develop on-chain, simply because the compute cost of doing so is higher than the cloud/CDN alternative. If this is widespread enough, the use case for crypto become limited exclusively to value transfer. However, to believe this, you have to believe that innovation in the crypto community will not continue finding ways to lower gas fees, and that the use cases for NFTs, DAOs and DeFi are either unnecessary, or replicable through big tech.

The low switching costs are increasingly offset by the interoperability requirements of Layer 1s and 2s, but will likely continue to be a threat to Ethereum as long as the bulk of on-chain transactions are simple token swaps or trades.

One of the most common memes in crypto culture is “Don’t trust. Verify”. Unfortunately this is unrealistic. Most people won’t read code, and “the unbanked” certainly won’t verify. Trust – of code, or people – is an inevitable part of a world with division of labour. However, people are oddly willing to trust a great UX, especially when they don’t have to pay much and see adverts for the product coming from billboards and celebrities. This is counter to the average Linux-using, anti-consumerist Etherean, but is likely the fastest route to mass adoption at a public level.

Externally, Ethereum faces many of the same risks as other cryptocurrencies. Arguably the most realistic one is a clampdown on the fiat-crypto gateway by states. Decentralised exchanges like LocalCryptos.com would likely be fine, but centralised exchanges provide chokepoints, and the bulk of onramps would face severe headwinds. Additionally, states could hamper the dApp portals, or prevent regulated entities from interacting with Ethereum-based dApps. VPNs could circumvent this, but the increased user friction and associated stigma would curtail adoption. However, with numerous large institutions adopting L1s as investments this is unlikely to happen in the West. Instead, countries like India are slowly embracing Ethereum as a state-assistance tool.

As with the CBDCs, China is again the anti-crypto lead. Besides an authoritarian state, the primary difference China has is the closed systems of Tencent and Alibaba. Digital payments are incredibly user friendly and are integrated with every other element of consumer life via WeChat and AliPay. If you are keen on reading more about the Chinese tech behemoths, I wrote another article over here.

While the Federal Reserve could not really mandate Facebook to us “Fedcoin” as the medium of exchange for WhatsApp Pay, the CCP has no such constraint. Given current geopolitics, it’s pretty unlikely either WeChat or the eCNY would be used much in the Western world. This tension arguably helps the politically agnostic crypto market. It also, however, means that a hostile nation would be more predisposed to launch an attempted 51% attack on Ethereum if it believed it could both drain the protocol of its value and hamper the flow of value in its national rival. This is a pretty late stage risk though, as neither China nor the US has widespread Ethereum adoption. Fortunately, as Ethereum improves and grows in value it becomes more costly to attack.

The last major state related risk is the murky link between Ethereum and property law. While the whole self-custody thing means that abrogation of property rights is borderline impossible, the flipside of the coin is that 90% of the legal system is in very muddy waters. A common legal phrase is “possession is nine-tenths of the law”, meaning ownership is far easier to settle when you possess the thing in dispute. Here again the self-custody element is hammered home. While the legality of crypto varies by jurisdiction, many judiciaries are behind in adapting precedent. ETH owners should get comfortable with the risk that they may not be able to reclaim their lost crypto.

One threat that comes up a lot is quantum computing. In theory, quantum computing could easily crack the encryptions Ethereum relies on, threatening not just future Ethereum projects, but all history stored on-chain too. Fortunately, this is a well-known problem within the community. For all the bits of the Ethereum protocol that are susceptible to quantum (ECDSA, BLS signatures etc.), there are already well-known and in-development alternatives that are quantum proof. Several proposed alternatives would require an EIP (a hard fork which improves the base Ethereum protocol), but others are Layer 2. For a good discussion of them I recommend this paper by Marcos Allende et. al. These alternatives are less efficient at processing (even w/the sharding). As compute and our technical capabilities improve, these will become more efficient to the point where they’re comparable with the current protocol stack. Here’s Vitalik talking about it.

Volatility is accepted as a law of nature in crypto. Laws of nature are usually derived from certain causes though, and this holds true for crypto too. One of the reasons why Apple is such a low-vol equity is because so much of it is traded per day. The liquidity ensures there’s a constant buyer for every seller and vice versa. When you have an asset like Bitcoin, with its strong HODL culture, or Ethereum with its staking model to-be, the float of tokens available for trade is structurally limited. This thin float means every incremental purchase or sale affects an increasingly large price swing. Volatility is structural because of the illiquidity.

This means two things: firstly, The Pitch’s “special situation” is more at risk of a sentiment change than it may appear. If ETH is priced in line with Bitcoin, and Bitcoin sentiment flips, ETH post-Eth2 will suffer markedly more downside volatility than token holders may be used to. Secondly, institutions require liquidity. Overcapitalised buyers need to trade material amounts of Ethereum for it to make sense for them. If the system is not able to accommodate these flows without rocking the price, institutions will hang back until it can. stETH fixes this.

Mario Laul recently wrote an essay on mitigating systemic risk in DeFi. It’s a great read, and you should definitely check it out. The basis of his essay is that DeFi has, as a community, an opportunity to build in a resilience that traditional finance does not have. Much like how early insurers spurred on fire-proof design in clustered houses, the various teams building DeFi protocols need to build with an awareness of the possibility of a rampant “fire-spread”. The leverage implicit in liquidity mining creates one such possibility. The illiquidity of Eth2.0, combined with the inter-linked liquidity provision and automatic liquidation of margined positions means that a flash crash could wreak sizeable havoc on an ecosystem as nascent as DeFi. As DeFi provides the liquidity for the rest of the blockchain, this can impact the staking rate for Ethereum, rippling across the ecosystem. Crypto is reflexive.

Several risks have a stack of literature on them already. Most of these are relatively unlikely, but good to take note of. To name a few:

-

The Eth2.0 rollout could be delayed or contain a faulty upgrade.

-

The ecosystem adoption may fail to spur token price. Transaction fees could be too low after scaling for fee burn to have an impact on price or Ethereum’s high-throughput, low-take-rate approach may render it a utility which doesn’t accrue enough value to token holders.

Source: Finematics

-

Scaling could fail to reduce fees, although this is unlikely as many protocols are already showing 100x improvements on computation costs.

-

Code bugs are always a concern. There have been several bugs allowing exploit or contract failure. In Ethereum, the DAO hack was the most well known. However, given the auditing and extensive research on Ethereum’s core protocol, this seems unlikely. Bugs are more likely to occur in L2s and products built atop Ethereum.

-

DeFi could fail to gain sufficient adoption, making Ethereum’s pricing system highly inefficient.

Beyond these more technical risks, there are concerns raised by many non-crypto-native investors. These range from ethical to game theoretic, legal and sociological. They are often nuanced, well-thought out critiques, and there is not space in this already-long essay to address all of them. Here are some of the more common ones:

“Bitcoin’s Gini coefficient is estimated at 0.88 & up, making Bitcoinlandia more unequal than any other human society, including North Korea, which enjoys a comparatively liberal Gini coefficient of 0.86”

Hypocritical crypto billionaires pretending to care about world poverty

— Nouriel Roubini (@Nouriel) May 11, 2018

The basis for the Gini coefficient mention usually comes from claims by media that the enormous bulk of Bitcoins/Ethereum are owned by an elite minority of addresses. A common rebuttal is that this is misapplied address analysis. Many addresses will be empty by design, many will represent millions of owners. A longitudinal study of clustered addresses would be more accurate. However, even these studies suggest unusually high levels of inequality. Ethereum is similar.

Vitalik recently wrote an excellent article against overuse of the Gini coefficient (Pardon the Vitalik spam in here, but he really is an excellent communicator). The essence of the article is summed up here:

“So, what’s wrong with it? Well, there are lots of things wrong with it, and people have written lots of articles about various problems with the Gini coefficient. In this article, I will focus on one specific problem that I think is under-discussed about the Gini as a whole, but that has particular relevance to analyzing inequality in internet communities such as blockchains. The Gini coefficient combines together into a single inequality index two problems that actually look quite different: suffering due to lack of resources and concentration of power.”

His argument is that the apparent inequality in the Ethereum community is more an indicator of engagement than lived experience. Those who own the bulk of the value do so because they have dedicated the last 5 years of their lives to building it, whereas the majority of the “poor” are really just regular folk, living middle income lives, who have decided to dabble a $15 bet on ETH.

Another common critique of crypto is that it is used to fund illicit activities. Assumedly the bulk of this thinking came from Bitcoins use as the medium of exchange for dark web marketplace Silk Road. While statistically it is fairly easy to guesstimate the percentage of funds used like this, there are other rebuttals too. Some of these criminality arguments are less interested in hard crime, and more addressing the KYC/tax avoidance that Ethereum enables. The predominant rebuttal here is that technology is amoral. VPNs and Swiss banking can do much the same. These are ubiquitously seen as institutions that add net value to society, not lumped with their occasional deviant user. Besides, fiat onramps, the tying of IPs to addresses, and the publicity of blockchain all mean its anonymity is not absolute, and prosecution is entirely possible.

Source: Spencer Noon

One of the more economic critiques is that a deflationary supply discourages token use as folk would rather HODL than transact. Much of the dynamics of the Ethereum ecosystem have been covered throughout the essay, so this will be a slightly more theoretical take. The basis for this opinion is the economic understanding that HODL culture induces hoarding and cannot underpin generosity, proactive capital, or transactions.

This is a well covered debate that’s been present in economic literature from well before Bitcoin’s inception. Austrian economists (Rothbard, Mises, etc.) hold that investment (requiring a low public time preference) spurs economic growth more than consumption (as per the Keynesians). The middle line straddled by most economists is that governments should spur consumption at a population level and investment at a fiscal (if socialist) or institutional (if capitalist) level. Austrian theory holds the low time preference enabled by sound money forces investors to be shrewder with their capital allocation, prompting wiser investments and less consumption. The neoclassical response to this is the Ramsey–Cass–Koopmans model, which models growth over successive generations through a function of both K (capital) and C (consumption). It gets fairly sophisticated the more variables one accounts for, but the important thing is that a low discount rate (time preference) still makes future cash worth more, so yes – folk will invest more and consume less.

Whether this is a good thing is the point of debate between the Austrians and the rest of the economic faculties. Both sides present convincing arguments, and if this essay were able to sway you one way or the other, it’d simply be because you hadn’t heard enough from the other side. We’ve never actually lived in a world with an auto-adjusting net deflationary monetary supply. There’s also never been an asset that is concurrently cash, capital, and consumable. In a nutshell, nobody really knows for sure how it would look.

The final critique is far more philosophical: The belief that the world was constructed for or grew around centralisation, and that individual sovereignty is antisocial or immoral.

A sizable appeal for many of the crypto-phenomenon is its libertarian roots. It preaches autonomy, independence of state, and self-reliance. There is, in the technocratic buzz, undertones of the rugged individualism and dump-the-tea, built-on-the-backs-of-cowboys behavior. “We don’t trust, we verify”. “Bitcoin fixes this”. This is the newspeak of a self-centered movement. And I mean that with all respect.

Crypto, remote work, social media, home schooling, gun ownership, end of American hegemony, creator economy, shorter supply chains, nationalism, etc.

Sovereign individuals are sprouting around the globe.

— Naval (@naval) December 8, 2020

The idea of a “sovereign individual” stems from JD Davidson and Bill Rees-Mogg’s titular 1999 book. It was popularised by books like Ferriss’ 4-Hour Workweek, and Ammous’ The Bitcoin Standard, and is a genuinely enjoyable read.

Typically, critiques of the idea seem to come from a political, cultural, or religious belief in the appointment of government and centralized bodies as both better decision-makers and the top of a justly hierarchical system. Sometimes this is exactly where they come from (Romans 13:1-2). Other times, they come from the deeply religious belief that an individual is far better suited for community than they are for independence. A core of Christianity is that man cannot save himself. Reliance on God is one of the major Islamic virtues. Whether Taoist, or Western existentialist, Buddhist, or Hindu, selflessness and interdependence in community is a cornerstone of many people’s belief systems.

Before jumping in with why decentralisation is the solution or with yawps of “Bitcoin fixes this”, think about the zeitgeist this creates. Tech is culturally agnostic. It is true, decentralisation allows for centralisation around more localized nodes. A divisible sovereignty removes the “monopoly of power” from an individual entity. Crypto is a tool to enable the sliding scale between absolute centralisation and absolute decentralisation. Platforms like Ethereum or Bitcoin are ways of opening local communities up, not necessarily supercharging the sovereign individual.

Anyways, this is actually an investment thesis, so let’s jump back to the money.

Valuation

As mentioned at the start of the essay, current analyst price targets range from $5 700 to over $150 000. Following in the footsteps of Ryan and Vivek, I’ve roughly approximated a DCF-based valuation for Ethereum.

The “income statement” for Ethereum is laid out in brief below. Revenue grows through expanding Ethereum’s network effects into dApps and transactability, increasing transaction fees accrued. Expenses are currently ETH sold to recoup the high energy cost of mining. After the PoS merge, the network costs will be ~1% of sales, putting margins (FCF is earnings in this case) at 99%.

Source: James Wang

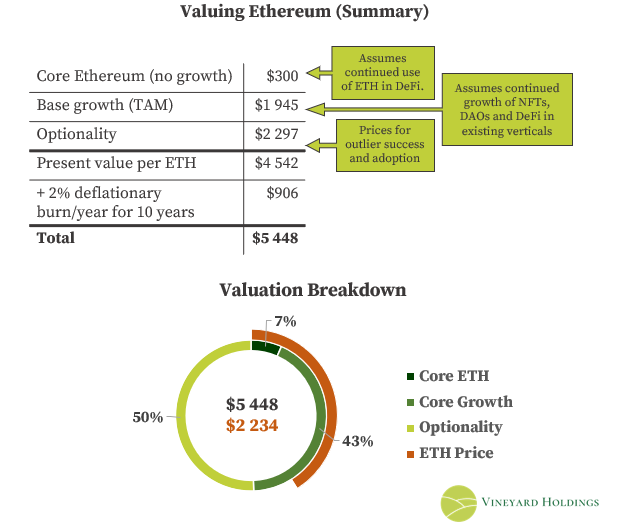

Rather than assume ETH will trade at the present sum of its DCF, this valuation attempts to split the approximate value of ETH into three elements: the “core business” with no growth, the expected value of conservative future growth, plus an approximate pricing of the “real world options” that Ethereum carries.

A word on the conservativism: this is a rough intrinsic valuation – I am neglecting flow-induced price-action here. I am also using a load of heuristics in the potential growth and optionality estimates. This is intended to be directionally correct and breakdown what I think currently is and is not priced in. The value of a model is getting to see the inputs.

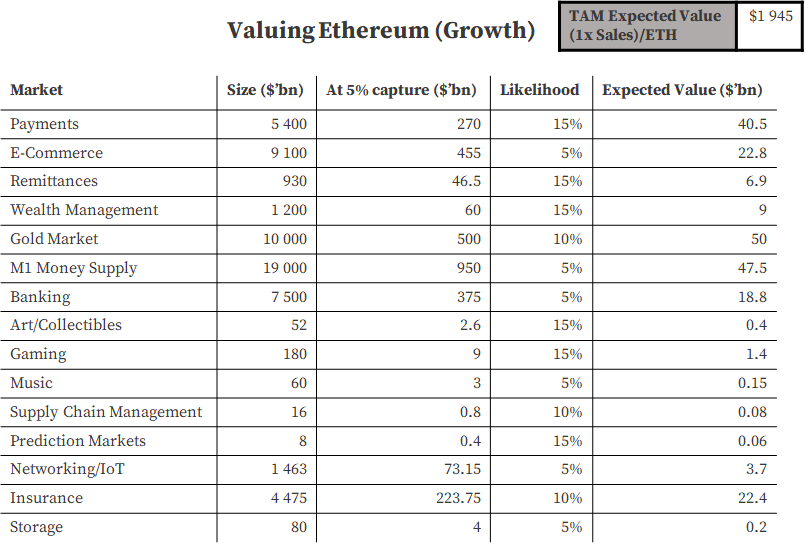

This is the “core business” at zero growth post FY21. A conservative discount rate of 15% is used in lieu of Ethereum’s perceived risk profile, high beta, and approximate WACC. The value of this core is $300/ETH, assuming 177M ETH in issue. It changes to $383 and $500 if we lower the discount rate to 10% and 5% respectively. It looks like the bulk of ETH’s valuation presently comes from expected growth.

When judging growth, breaking it down into industries Ethereum may disrupt, assuming it captures 5% of each of those markets, and assigning a probability to that possibility spits out an expected value of the future growth potential. This is not exact EV, not even close actually, but helps to contextualise the markets. There may be considerable overlap between industries, and the path dependency necessary in capturing even 5% here likely means the outcome is more binary than I’ve modelled below. If Ethereum cannot capture 5% of any of these it will likely fade to oblivion over the next decade. It will hit an absorbing barrier. Plus complex adaptivity means one sector adoption (payments) will strongly effect another (remittances). The flipside is that if it captures >5% in one of the big ones, it will likely capture far, far more than I’ve outlined below.

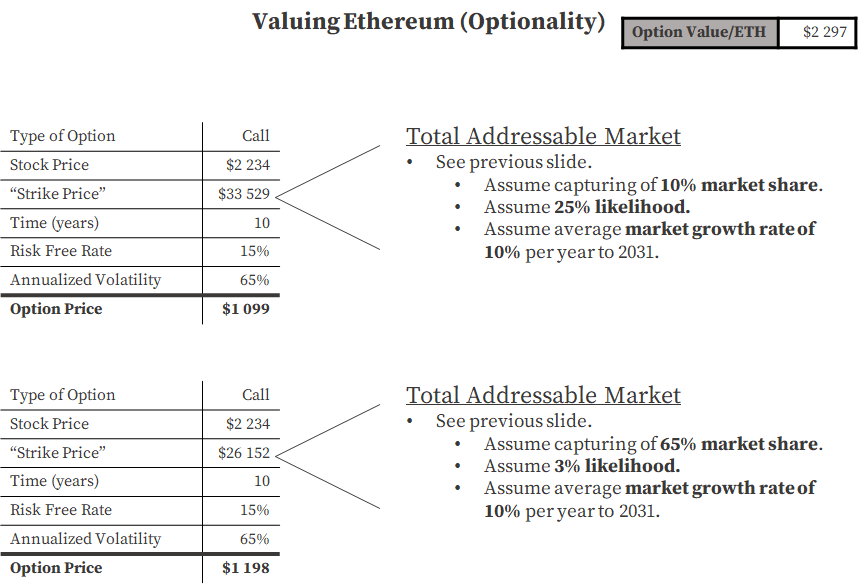

Conservatively assuming ETH trades a a 1x Sales multiple, that there is no overlap between industries (there obviously is), and that none of these industries have grown by the time of capture, you land at a value of $1 945/ETH. Our total is now $2 245/ETH. Roughly the price it trades at today. But what about the “right tail” outcomes – we haven’t really priced in much of the moonshot potential here. Well, we can use the abominable Black-Scholes model to approximate the price of a real world option, but we’ll have to butcher it with some assumptions.

Ideally, when applying this to real world options (which it wasn’t designed to do) you’d like to estimate the incremental capex cost of a project as the stock price, and the EV of the project as strike price. This is the idea from Mauboussin’s 1999 whitepaper. He has a nice formula, which I am trying to shove onto Ethereum (which it wasn’t designed to do).

Assuming some moonshot potential over the coming decade, with assumptions above, you arrive at a rough valuation for the optionality embedded in Ethereum at $2 297/ETH. This brings our total to $4 542/ETH. Adding in an expected 2% deflationary supply burn over the next decade, the intrinsic value of Ether currently arrives at around $5 448/ETH.

In theory, buying Ether at ~$2,234/ETH is buying the core business on the expectation that there is, at most, a 15% chance that it captures only 5% of all the markets it is busy disrupting. If you do that, you get the optionality for free.

Parting Thoughts

And so we arrive at the end of this essay. This has been a different piece to my usual writeups, I hope you have enjoyed it. If you opened the article and skipped to the conclusion hoping for a summary, I usually put them right in the beginning. In this article, the block on top is a 1-page thesis, but The Pitch is really where the meat is at.

I’ll leave you with a couple parting thoughts from some folk I admire.

“Kind of like a bet on a startup company management team, a bet on Ethereum is a bet that the developers will perform a massive transformation on the base layer and successfully maintain its dominant network effect against competitors.” – Lyn Alden (2021)

“You come to the realization that the blockchain is really a general mechanism for running programs, storing data, and verifiably carrying out transactions. It’s a superset of everything that exists in computing. We’ll eventually come to look at it as a computer that’s distributed and runs a billion times faster than the computer we have on our desktops, because it’s the combination of everyone’s computer.” – Tim Sweeney (2017)

“As great as open-source software development has been, far more people are willing to do far more things for money than for free, and suddenly all those things become possible and even easy to do. Again, it will take 30 years to work through the consequences of this, but I don’t think it’s crazy that this could be a civilizational shift in how people work and get paid.” – Marc Andreesen (2021)

Tyler Durden

Mon, 08/02/2021 – 06:30

via ZeroHedge News https://ift.tt/3jdqrRp Tyler Durden