As Sprott Goes “Hunt Brothers” On Uranium, A Copycat Joins The Squeeze To Force An Explosive Move Higher

Exactly two weeks ago, we laid out the investment thesis for what our friends at Adventures in Capitalism dubbed was a “bitcoin-like opportunity in Uranium.” In a nutshell, in mid-August, the Sprott Physical Uranium Trust, then roughly $300 million, announced that it would unleash an unprecedented buying spree in physical uranium, a relatively small market, in hopes of forcing a physical shortage and sending the price of urnium higher, leading to more buying of the Trust, more purchases of uranium, even higher prices and so on.

While some voiced concerns that this strategy was similar to what the Hunt Brothers tries to do with silver back in 1980, when the precious metal rose tenfold in months only to crush just as rapidly once the market became “uncornered” there are several distinct differences between what the Hunts and Sprott are doing (most notably the inability by producers to rapidly flood physical to meet demand, as well as the lack of a sizable paper market to short the move) so far – less than a month later – Sprott’s strategy has proven extremely successful, so much so that the Canadian asset manager upsized the size of its Trust from $300MM to $1.3BN… and just this morning got its first copycat, Uranium Royalty Corp (UROY) which this morning announced that it was taking a page out of the Sprott book and would expand its physical uranium holdings to 648,068 pounds.

Uranium Royalty Corp Expands Physical Uranium Holdings to 648,068 Pounds of U3O8 at a Weighted Average Cost of US$33.10 per pound U3O8. https://t.co/r3IYv9h8nT https://t.co/ybr2WV0uX0

— Uranium Royalty Corp (UROY: Nasdaq) (URC: TSX-V) (@UraniumRoyalty) September 15, 2021

But before we get there, a quick excerpt from a report this week by Bank of America which has broken down the Sprott strategy and discussed how it will impact the price of uranium going forward, and why it just hiked its price target for Cameco by 45% to $29/share

SPUT/Byron/Dresden add 4% to global demand, PO upped

Uranium (U3O8) purchased by the Sprott Physical Uranium Trust (SPUT) since launching an at-the-market (ATM) equity program on August 17th has added 3% to global demand. This is 52% annualized, or $4bn at flat prices. Prices have risen 42% to $43.75/lb. A supply response is likely but might take time and more SPUT buying is likely, we think. The Illinois House and Senate approved funding to keep the Byron & Dresden nuclear plants from closing. We add both back to our model, increasing annual U3O8 demand by 1.1%. We increase 2021E-2023E U3O8 prices by 18%, 41% and 18% to $36.30, $53.50 and $48.50/b. We raise our price objective (PO) for Cameco (CCO) by 45% to C$36.25/sh ($29/sh), CCO: Neutral as we think outlook is mostly reflected in the shares.

SPUT ATM funding increased to $1.3bn

SPUT has raised roughly $245mn of the $300mn maximum set-out under its ATM program. On Friday, SPUT obtained approval to increase the maximum to $1.3bn. The limiting factor on future SPUT capital raises is market demand for its units, which appears to us to be strong and correlated to SPUT’s ability to continue pushing up uranium prices. Given the relatively small size of the U3O8 spot market (~$2.7bn in 2020, unadjusted for churn), SPUT buying should push spot prices still higher, until supply responds or the price gets high enough to spook investor demand for SPUT units.

So the weakest link in the Sprott strategy is how quickly will incremental supply come on line. The good news for Sprott is that, at least according to BofA, it won’t be for some time.

A supply response is likely but not immediately

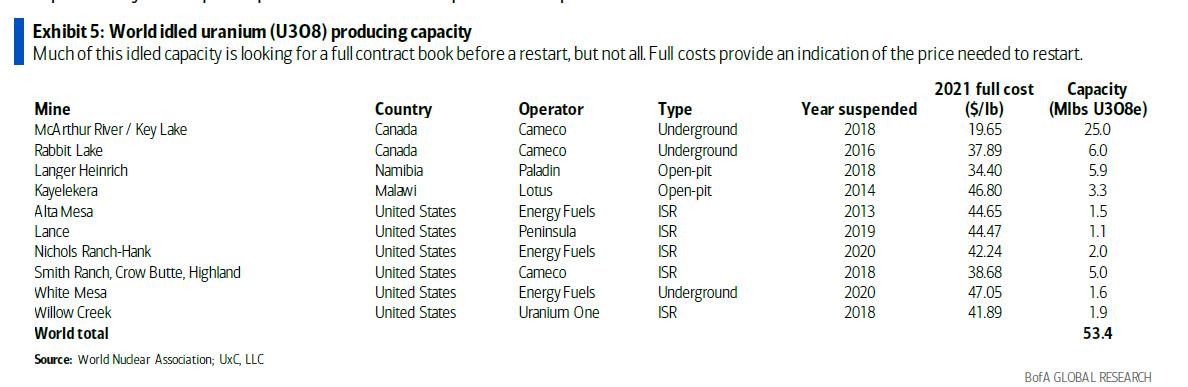

U3O8 held by junior miners and hedge funds, uncommitted supply from producers and a reversal of carry trades are among potential near-term sources of new market supply. Potentially larger sources are 58Mlbs of idled production capacity and 16.8Mlbs of unutilized capacity in Kazakhstan. However, a large majority of this is unlikely to respond without long-term contracts and would require six or more months to ramp-up.

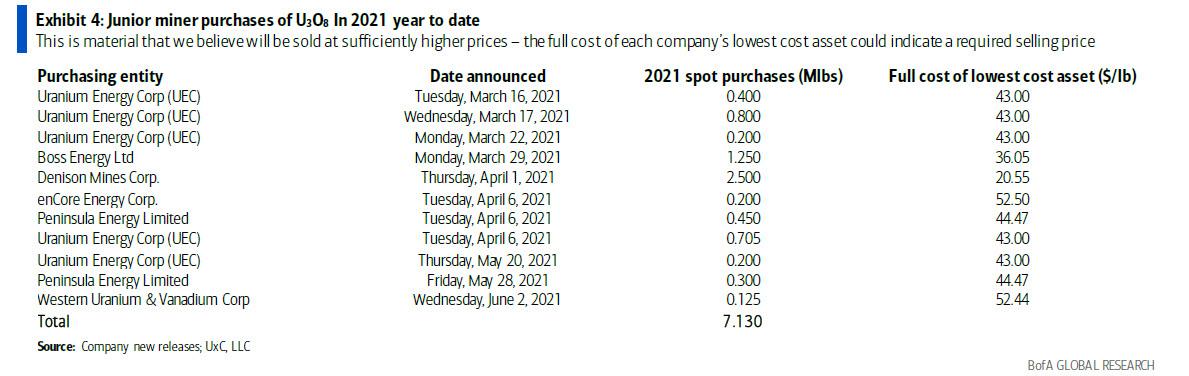

UxC estimates that hedge funds hold around 11Mlbs of U3O8 that was mostly purchased in 2018 and 2019 when prices averaged just $24.61/lb and $25.84/lb vs. the current spot price of $43.75/lb.

There can be many sources of uncommitted supply with BHP’s Olympic Dam (8-10Mlbs annually) and the Navoi mines in Uzbekistan (9Mlbs annually) the usual candidates. Other less obvious sources also exist. For example, we estimate that in H1’21, China imported nearly 21Mlbs of U3O8 which equates to approximately 82% of the country’s 2021E reactor requirements. In addition, Chinese utilities are estimated to hold as high as or more than 460Mlbs of U3O8 inventory, sufficient to cover expected requirements for the next 11 years. As prices rise we see the possibility for some of the U3O8 produced in Chinese owned mines outside of China to be sold into the spot market. We estimate that in H2’21, Chinese owned mines outside of China will produce roughly 8Mlbs of U3O8. We do not expect Chinese inventories to be sold, however. Those are considered strategic.

Kazakhstan under-utilizing capacity: In Kazakhstan, the world’s largest U3O8 producing nation, there are several uranium mines now producing below capacity. On a 100% basis, these mines have a capacity of around 75.4Mlbs but we forecast them producing 58.6Mlbs in 2021E, leaving 16.8Mlbs of additional production potential trough flexing up utilization. However, similar to Cameco, Kazatomprom has indicated it will not flex up its production until they are signing long-term contracts and the price is fair. The latter condition may now be realized, the former remains to be seen. We think KAP sees $40-$45/lb as fair pricing.

Idled capacity is substantial but a majority is disciplined: According to data compiled by the World Nuclear Association (WNA), there is 54.4Mlbs of idled capacity. Cameco, which controls 58% of this idled capacity, has indicated it must fill its contract book at attractive pricing before it will restart McArthur River and has indicated that very high prices would be necessary to restart Rabbit Lake. The price indicated by Cameco for a McArthur restart is $40/lb or greater. Paladin has suggested a similar approach with its Langer Heinrich mine which accounts for another 11% of this idled capacity. Of the remaining 31% of potentially undisciplined producers only 17% (8.9Mlbs) is profitable at the current spot price on a full cost basis. However, much of this potentially undisciplined production will soon be profitable as prices rise.

But while we wait for supply to rise, one thing is clear: producers – such as Cameco – will benefit when utilities re-enter the market, to wit:

The higher spot price means produced supply is more competitive vs. the carry trade, presenting an opportunity for longer-term contracting. When utilities re-enter the term market, existing producers should benefit. Will utilities enter the term market this week as they have historically? Likely, but volumes are uncertain and coverage is solid.

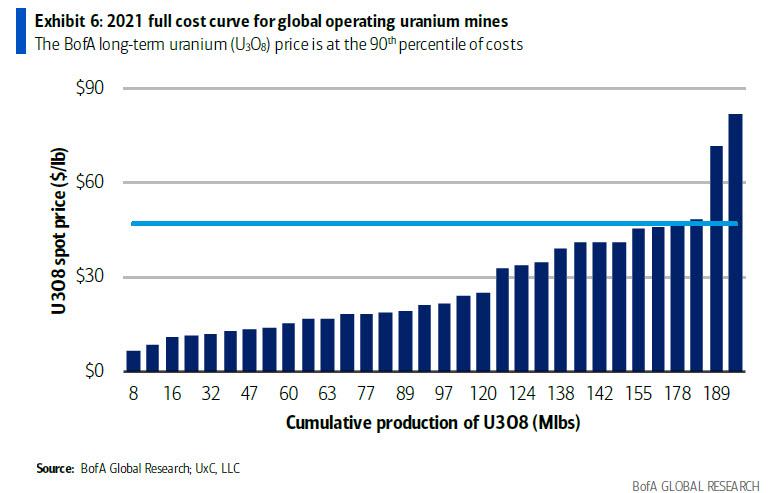

Of course, much of the production on the cost curve would require far higher prices to be profitable. The chart below shows the estimated 2021 global uranium industry cost curve. Full costs include all mining, processing and site G&A costs as well as sustaining capex. Sunk costs and a rates of return are excluded. The exhibit shows that our long-term U3O8 price forecast of $47/lb is in line with the 90th percentile on the cost curve.

In other words, there is some marginal supply available but the price of uranium will have to rise well above $60 for it to be accessible. Today uranium is trading around $46, up almost 50% since Sprott launched his buying vehicle.

And while utilities are currently well-covered, NPP life extension may change that substantially. As BofA notes, “US utilities have the best contract coverage in 30 years. In the EU coverage is even better. We think utilities thus have bargaining power even with much higher spot prices and see contract prices that are lower (closer to our $47/lb long-term price). Yet, potential nuclear plant life extensions like Byron and Dresden will mean less inventory and contract coverage. We lower our 2021E loss per share (LPS) to $0.45 from $0.22, raise 2022E EPS to $0.25 from $0.08 and raise 2023E EPS to $0.59 from $0.20. Using a net asset value approach, CCO shares imply a $50/lb U3O8 price.”

So what does all this mean for the industry? In a nutshell, sharply higher prices: here is BofA.

Given that we think there will be at the minimum a sustained bid in the spot market for U3O8 from SPUT combined with already tightening markets and the addition of Byron and Dresden to our demand forecast, we raise our 2021E to 2023E U3O8 price forecasts by 18%, 41% and 18% to $36.30, $53.50 and $48.50/b. Our long-term price is pushed to 2026E from 2025E and increased to $47/lb supported by an updated production cost curve. Our view is that prices will continue rising but peak in Q1’22 as plans for productive supply responses are revealed. We expect CCO to restart McArthur River in 2023E at a capacity utilization of around 30% and steadily ramp up from there.

A key driver of how fast uranium prices normalize will be the response time at the world’s largest miner, Cameco, which according to BofA is “the only large, liquid, US listed vehicle for exposure to uranium.” As BofA notes, “we are now assuming that CCO restarts it McArthur River mine, the largest uranium mine in the world at annual production of 25Mlbs, in 2023E. However, we see a very gradual restart with capacity utilization of just 30% in 2023E, 50% in 2024E to 2026E and then 100% from 2026E onward.“

To be sure, Cameco will be asking itself does it want to produce more and lower both the price of uranium and its stock, or take its time with ramping production. One look at the recent action of the OPEC+ cartel should give an indication as to what it may do.

In other words, we do not expect major downward pressure on either the price of uranium or CCJ for the foreseeable future, something which even retail investors have now grasped making CCJ the most actively discussed name on the WallStreetBets forum a few days ago.

CCJ it is pic.twitter.com/UTwIbjhdF6

— zerohedge (@zerohedge) September 13, 2021

So with all that in mind, we look at what appears to be the first Sprott copycat to emerge in the past month, namely Uranium Royalty, which has surged as much as 18% after announcing that it’s entered into contracts for three additional spot purchases totaling 300,000 pounds of uranium, noting that the average cost of the purchases is $38.17 per pound, a number which is already a substantial discount to today’s price.

Following completion of the deliveries, URC CN will hold a physical inventory of 648,068 pounds of uranium at a weighted average cost of $33.10 per pound. More from the press release:

It is within URC’s mandate to make periodic purchases of physical uranium to provide attractive commodity price exposure to shareholders, especially in these early stages of a bull market in uranium. The global mega-trend towards de-carbonization is providing a major catalyst for carbon-free, safe, and reliable nuclear energy. The supply and demand fundamentals for uranium continue to improve, with demand for uranium now exceeding pre-Fukushima levels and global mine production (128 million pounds) expected to lag global consumption (191 million pounds) by 63 million pounds in 2021 (UxC data – Q3 2021 report).

This is the 5th year of the production/consumption gap which has had a positive impact on drawing down excess market inventories. The purchasing activities of producers and financial entities, like the Sprott Physical Uranium Trust have accelerated this rebalancing as of late, resulting in a 49% rise in the spot price in the past five weeks.

As Sprott continues to upsize its physical uranium fund to meet growing demand, and as the price of both uranium and producers continues to rise, expect many more tactical and strategic buyers of uranium to emerge as suddenly Uranium is the new silver and everyone is hoping to be the new Hunt Brothers.

Tyler Durden

Wed, 09/15/2021 – 11:44

via ZeroHedge News https://ift.tt/2YUDEIl Tyler Durden