Nomura: Clients Are Desperate For A Dip To Buy

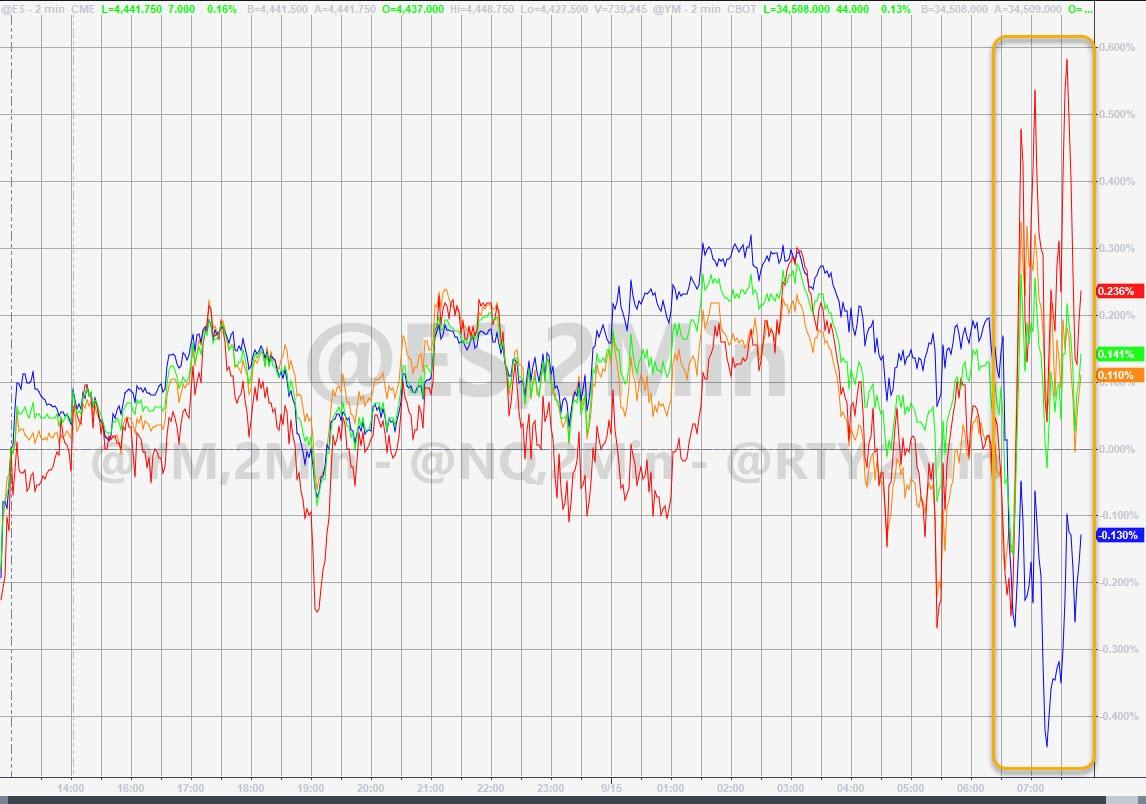

This morning’s chaotic trading in stocks could be indicative of the pull and push that Nomura’s Charlie McElligott sees playing out over the next week or so.

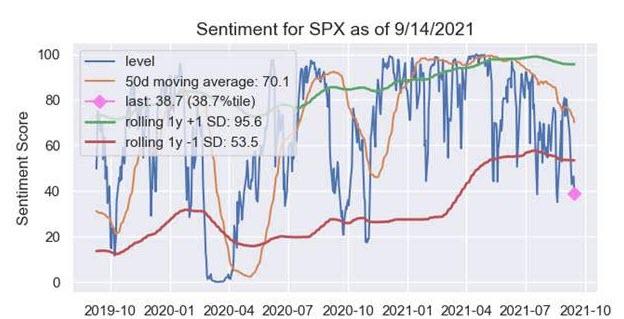

Specifically, Nomura’s SPX sentiment index is cratering and at 38.7%ile, back near lows of the year.

Forward returns backtest to show sideways for the next 1m with negative excess return.

But it is the ultra-short-term which is most interesting…

The bearish story in Equities continues to be based around taking down exposure ahead of Op-Ex cycle “vol expansion” and in front of pending EPS season + FOMC meeting event risks, with a lot of net long positioning from discretionary and historically extreme exposures from target risk types that could still turn slippery as we lose vanna, charm and gamma supports / stabilizers when stuff rolls-off from these expirations, particularly as so much of this sits in front-month (i.e. +80% of SPX delta in front-month)

Overall, we see 32% of SPX / SPY Gamma and over 50% of QQQ / IWM Gamma coming off—“free like a bird”

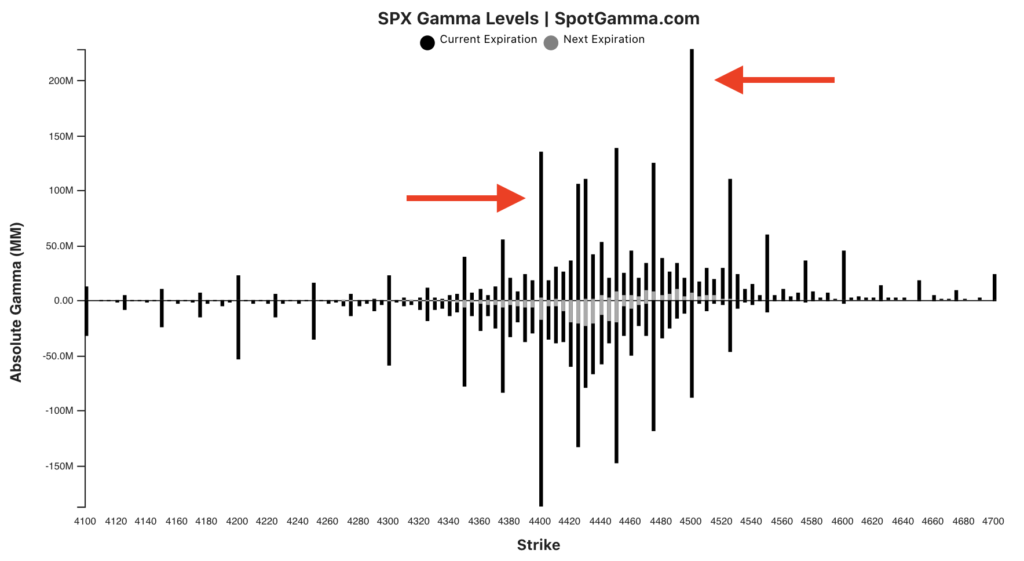

Options positioning has clearly turned, with SPX, QQQ and IWM all in ‘negative gamma vs spot’ territory as of today—although $3.3B of $Gamma at the obscure 4430 strike matters (45k OI in that line, from the big Collar which trades in the market that the entire universe knows about), which is helping us hold (worth noting $4.3B down at 4400, $3.2B up at 4450)

Delta still net long / positive for SPX as a potential source of de-risking flow (66%ile at $205B, flips negative Delta below 4388), neutral QQQ here (ref 375), negative for IWM

But, in the short-term, McElligott notes share-buybackers and vol-control algos are looking for dips to buy…

Vol Control still set to load up thurs and Friday approx $15 to $20B depending on daily changes btwn zero and 50bps…

however next week and beyond is the de-allocation risk, enormous notional supply potential in -1.5% or greater daily change environment.

The trick here, warns the Nomura strategist, is the magnitude of a potential selloff between now and The Fed, because the normally reflexive vol selling into these Op-Ex “gamma unclench / vol expansion” windows experienced YTD could be held-off into the likely upside risks in the Fed “dots” update / release.

* * *

So, to sum it all up simply: the question is, can buybacks (before blackout windows) and vol-control flows (realized to implied vol spread still extreme) in the next few days ahead of the big options expiration be enough to outweigh any Fed event risk anxiety and de-grossing ahead of next week?

Specifically, SpotGamma notes that it appears that positions are filling in around this 4450 area, with 4400SPX/440SPY and 4500SPX/450SPY showing as large “bookends”.

While little of this position expires today in SPX, roughly 20% of SPY gamma expires at the close, which should add to volatility into Friday.

SpotGamma thinks one of these ends is tagged into 9/17 OPEX, and that could determine how we open next week.

Tyler Durden

Wed, 09/15/2021 – 12:25

via ZeroHedge News https://ift.tt/3nEV2eu Tyler Durden