How Can Houses Be Unaffordable And Booming?

Authored by John Rubino via DollarCollapse.com,

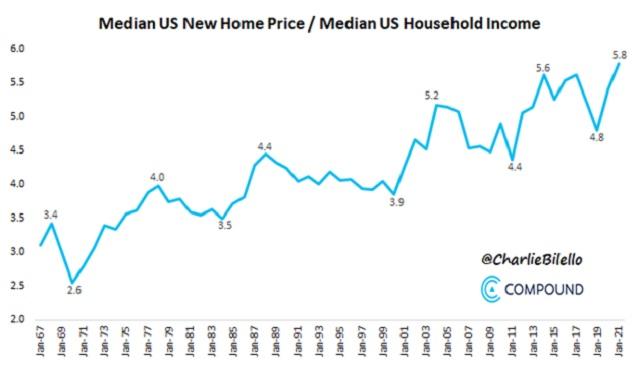

Home prices have never been higher when compared to the average family’s income.

This kind of imbalance is normally a sign of an impending crash in home sales, followed by a drop in prices. But that’s not happening.

Some recent headlines:

How is it that homes are both unaffordable and soaring in price?

As with so many other things that shouldn’t be, the answer can be found at the intersection of Wall Street and easy money.

During the previous decade’s Great Recession, hedge funds and private equity firms figured out that they could borrow for next-to-nothing and buy up the houses that banks were repossessing, then rent those houses back to millions of newly homeless Americans for good returns. Combine these positive cash flows with massive recent price appreciation, and those foreclosed houses turned out to be phenomenal investments.

Now Wall Street is doubling down, using hundreds of billions of essentially free money to outbid individual buyers for whatever houses are still available. In some cases investment giants like Blackrock buy up entire neighborhoods at big premiums to the asking price, pushing everyone else out of the market. Hence the disconnect between home prices and family incomes.

But wait, there’s more. Now the securitization machine has discovered houses.

Zillow’s Home-Flipping Bonds Draw Wall Street Deeper Into Housing

(Bloomberg Businessweek) — Zillow Group Inc. is best known for the addictive real estate listings that keep people browsing the internet all night, has dived into the house-flipping business, offering to quickly take properties off sellers’ hands. And in the process it’s helping pull Wall Street even deeper into the $2 trillion U.S. housing market.

In August, Zillow raised $450 million from a bond backed by homes it’s bought but not yet sold. The offering, led by Credit Suisse Group AG, was modeled on the loan facilities that car dealerships use to finance floor models. The novelty of using that structure for houses didn’t scare off investors hungry for a new way to bet on the hottest housing market on record. The offering was over subscribed and Zillow, which declined to comment on its bond market activities, is now in the process of selling another $700 million in bonds.

Now those volumes are set to explode. Zillow expects to acquire homes at a pace of 5,000 a month by 2024. Another competitor, Offerpad Solutions Inc. could eventually buy 70,000 homes a year, based on its view of the future opportunity. Opendoor, still the largest iBuyer, has said its playbook calls for the company to capture 4% of all home sales in 100 markets. Together the three companies could soon be buying close to $100 billion worth of homes a year, requiring more than $20 billion in revolving credit facilities.

Looks like housing is yet another example of how easy money perverts formerly free markets. Where family income used to dictate (and limit) home prices, now the driver is the yield on corporate and asset-backed bonds. The lower those rates go, the higher home prices climb. If individual buyers are priced out, well, they can just rent from Wall Street, on whatever terms our new landlords think is fair.

Tyler Durden

Sat, 10/02/2021 – 13:30

via ZeroHedge News https://ift.tt/39Wd2ZU Tyler Durden