Bulls Regain Control Of The Market As Fed Taper Looms

Authored by Lance Roberts via RealInvestmentAdvice.com,

Market Rallies As Earnings Season Kicks Off

Two weeks ago, we laid out the case for why we started increasing our equity exposure in portfolios.

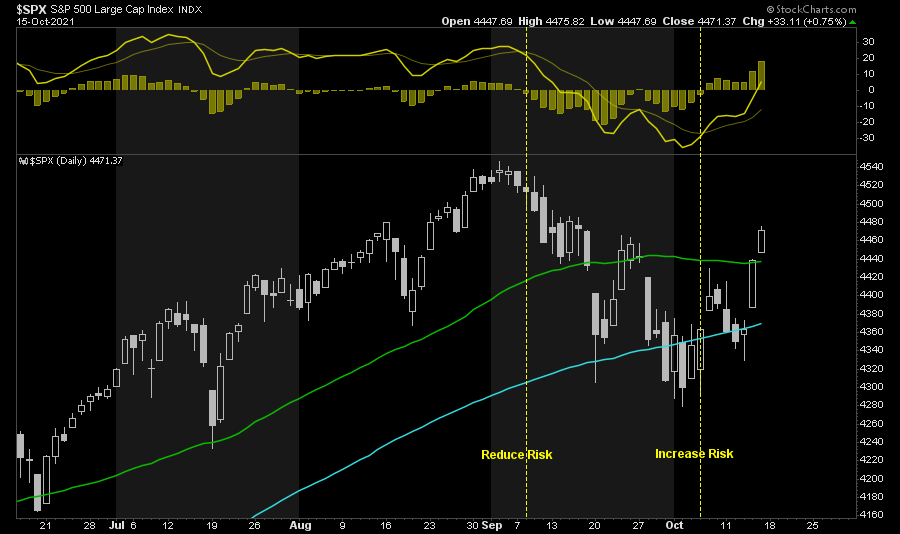

“It is worth noting there are two primary support levels for the S&P. The previous July lows (red dashed line) and the 200-dma. Any meaningful decline occurring in October will most likely be an excellent buying opportunity particularly when the MACD buy signal gets triggered.

The rally back above the 100-dma on Friday was strong and sets up a retest of the 50-dma. If the market can cross that barrier we will trigger the seasonal MACD buy signal suggesting the bull market remains intact for now.“

Chart updated through Friday.

While the market started the week a bit sloppily, the bulls charged back on Thursday as earnings season officially got underway. With the market crossing above significant resistance at the 50-dma and turning both seasonal “buy signals” confirmed, it appears a push for previous highs is possible.

Correction Is Over For Now

After nearly a month of selling pressure, the rally over the last couple of days came on cue and supported our recommendation to increase exposure to equities. As noted by Barron’s:

“Market sentiment is getting more buoyant. Thursday, the S&P 500 saw its largest gain since March 5, according to Instinet. The percent of stocks on the index that rose, 95%, was the highest since June 21. Friday, about 90% of components were positive. Instinet sees a high likelihood that the index will reach 4.570 fairly soon, for a more than 2% gain.”

Two factors are driving the rebound. Earnings, so far, are coming in above estimates. Such isn’t surprising as analysts suppressed estimates going into reporting season. Secondly, bond yields declined.

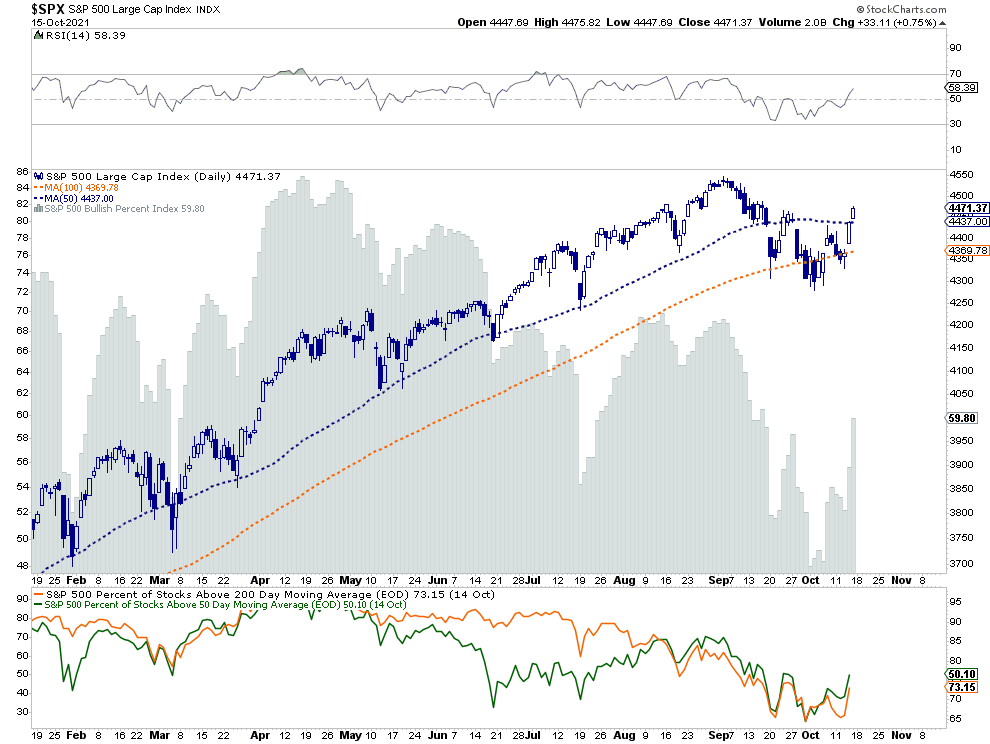

However, there are still reasons to remain cautious near term. As shown below, the internals of the market, while improved slightly, remain negatively diverged. The number of stocks above respective 50- and 200-dma remains low, the bullish percent index remains weak, and relative strength declines.

Furthermore, most companies haven’t reported earnings yet, and macroeconomic challenges still exist. So far, large banks beat estimates on reduced loan loss reserves, but they don’t deal with supply-chain limitations. We are about to see earnings from companies directly impacted by, and don’t benefit from, higher inflation, labor costs, and supply line disruptions.

Technically, If the current rally is going to push back to all-time highs, the market’s underlying strength must begin to improve markedly over the next couple of weeks. If not, the current rally will likely fail sooner than later. Furthermore, the odds of a correction increase as the Fed begins to reduce monetary accommodation.

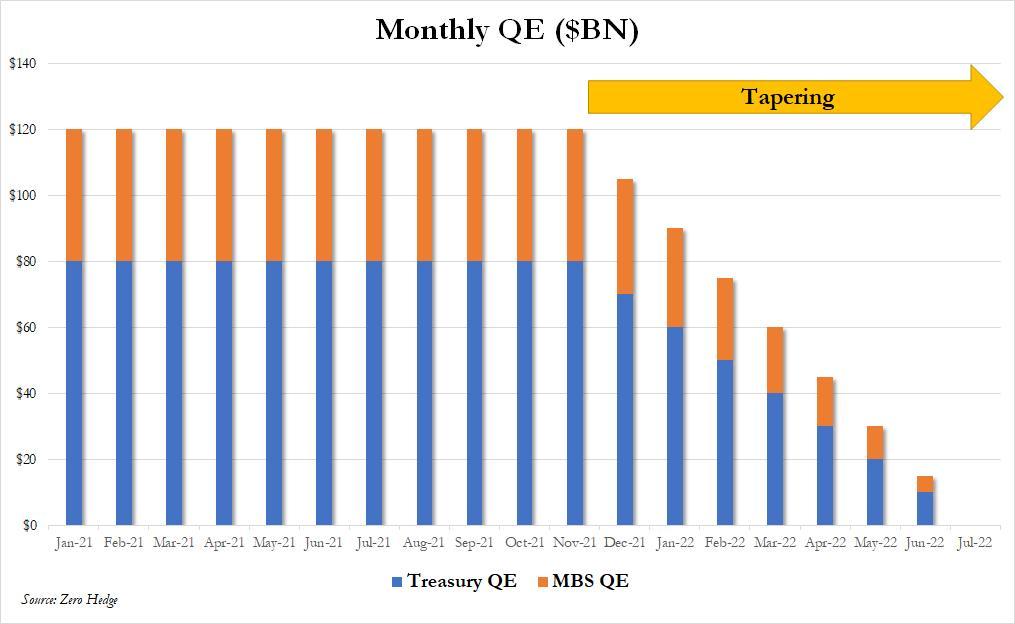

FOMC Minutes Confirms Taper Is Coming

In the most recent release of the Federal Reserve’s FOMC minutes, the much anticipated “taper” of bond-buying programs got confirmed. To wit:

“The illustrative tapering path was designed to be simple to communicate and entailed a gradual reduction in the pace of net asset purchases that, if begun later this year, would lead the Federal Reserve to end purchases around the middle of next year.

The path featured monthly reductions in the pace of asset purchases, by $10 billion in the case of Treasury securities and $5 billion in the case of agency mortgage-backed securities (MBS). Participants generally commented that the illustrative path provided a straightforward and appropriate template that policymakers might follow, and a couple of participants observed that giving advance notice to the general public of a plan along these lines may reduce the risk of an adverse market reaction to a moderation in asset purchases.“

While the Fed did not explicitly discuss rate hikes, as noted in our Daily Commentary, the futures market has already priced in two rate hikes next year.

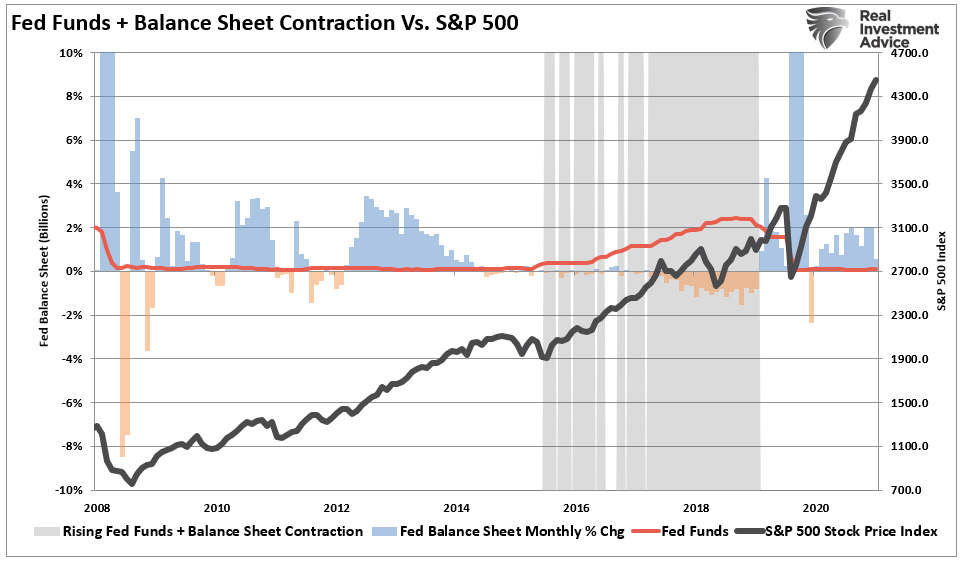

Between reducing bond purchases and lifting overnight rates, the risk to investors is more than evident. As we noted in “3-Things That Will Trigger The Next Bear Market:”

“The risk of a market correction rises further when the Fed is both tapering its balance sheet and increasing the overnight lending rate.

What we now know, after more than a decade of experience, is that when the Fed starts to slow or drain its monetary liquidity, the clock starts ticking to the next corrective cycle.”

The problem for the Fed is that while they suggest they will “adjust” based on incoming data, they may well get trapped between surging inflation and a recessionary economy.

Inflation: Transient Or Persistant

As noted, the risk to the Fed is getting trapped by inflation. The hope has been that current inflationary pressures from the economic shutdown would be “temporary” or “transient” and resolved as the economy reopened. However, nearly 18-months later, with the economy booming, employment running hot, and more job openings than unemployed persons, the disruptions remain. Notably, prices are surging, particularly in the areas that affect households the most.

If inflation is running ‘hot” and employment is full, the Fed should remove monetary accommodation and hike interest rates. However, with economic growth weak, financial stability dependent on monetary interventions, and record numbers of near-bankrupt companies dependent on low-interest-rate debt, a reversal of accommodation could be disastrous.

The hope was inflation would be transient and monetary accommodations could continue unfettered. Now, as noted by St. Louis President James Bullard, this year’s surge in inflation may well persist amid a strong U.S. economy and tight labor market.

“While I do think there is some probability that this will naturally dissipate over the next six months, I wouldn’t say that’s such a strong case that we can count on it,” Bullard said Thursday during a virtual discussion hosted by the Euro 50 Group.

“I would put 50% probability on the dissipation story and 50% probability on the persistent story.”

As Michael Lebowitz noted this week:

“If demand stays high, and supply lines and production remain fractured, inflation will continue to run hot. If such occurs, CEOs may decide not to invest in new production facilities where ‘persistent’ inflation becomes more likely.

Primarily, ‘persistent’ is not ‘transitory.’ Nor is persistent in the Fed’s forecast. Persistent inflation requires the Fed to take detrimental actions to investors.

Given the oddities of the current environment, and our fiscal leaders’ carelessness, it is something we must consider.”

Both Bulls And Bears Have Valid Views

Given the potential for a “policy mistake” and our cautionary views, the following email question currently sums up many investors’ views.

“I really am not sure what to do. Should I raise more cash and be defensive with inflationary pressures rising, and the Fed set to taper. Or, should I just stay invested given the market seems to be doing okay?”

For investors, they have gotten caught between logical views.

From the bullish perspective:

-

The market just completed a much-needed 5% correction.

-

Short-term conditions are oversold.

-

Bullish sentiment is largely negative.

-

Earnings season should be supportive.

-

Stock buybacks are running at a record pace.

-

The seasonally strong period of the year tends to be positive for stocks.

However, those views get countered by the bearish perspective discussed last week.

-

Valuations remain elevated.

-

Inflation is proving to be sticker than expected.

-

The Fed confirmed they will likely move forward with “tapering” their balance sheet purchases in November.

-

Economic growth continues to wane.

-

Technical underpinnings remain weak.

-

Corporate profit margins will shrink due to inflationary pressures.

-

Earnings estimates will get downwardly revised keeping valuations elevated.

-

Liquidity continues to contract on a global scale

-

Consumer confidence continues to slide.

Given this backdrop, it is understandable why investors are finding reasons “not” to invest. However, as stated previously, avoiding crashes and downturns can be as costly to investment outcomes as the downturn itself.

Navigating Uncertainty In Your Portfolio

As noted above, the market has not done anything technically wrong. Longer-term, the bullish trend remains intact, the recent correction worked off much of the overbought condition, and investor sentiment is negative enough to support a short-term rally.

However, while we think a rally is likely near-term, there is considerable risk to the market as we head into 2022. Such is why we stated last week:

“If you didn’t like the recent decline, you have too much risk in your portfolio. We suggest using any rally to the 50-dma next week to reduce risk and rebalance your portfolio accordingly.“

So here are some guidelines to follow.

-

Move slowly. There is no rush in making dramatic changes.

-

If you are over-weight equities, DO NOT try and fully adjust your portfolio to your target allocation in one move. Think logically above where you want to be and use the rally to adjust to that level.

-

Begin by selling laggards and losers.

-

Add to sectors, or positions, that are performing with, or outperforming the broader market.

-

Move “stop-loss” levels up to recent lows for each position. Managing a portfolio without “stop-loss” levels is foolish.

-

Be prepared to sell into the rally and reduce overall portfolio risk. Not every trade will always be a winner. But keeping a loser will make you a loser of both capital and opportunity.

-

If none of this makes any sense to you – please consider hiring someone to manage your portfolio for you. It will be worth the additional expense over the long term.

While we remain optimistic about the markets, we are also taking precautionary steps to tighten up stops, add non-correlated assets, raise some cash, and hedge risk opportunistically on any rally.

…as Seth Klarman from Baupost Capital once stated:

“Can we say when it will end? No. Can we say that it will end? Yes. And when it ends and the trend reverses, here is what we can say for sure. Few will be ready. Few will be prepared.”

We are not in the “prediction business.”

We are in the “risk management business.”

Tyler Durden

Sun, 10/17/2021 – 10:30

via ZeroHedge News https://ift.tt/3aIBRc4 Tyler Durden