For Robinhood, Firing Vlad Tenev Is The First Step To Redemption

Submitted by QTR’s Fringe Finance

Robinhood (HOOD) – a name that I have been buying since about 40% ago, as detailed here, and am continuing to buy (baghold) this afternoon – posted an ugly-looking quarter after hours today, as I actually somewhat expected again from the struggling brokerage.

Before diving into the details of the report, there’s one thing I think HOOD shareholders should unify around: Vlad Tenev needs to go. I mean, look at this photo and tell me the market doesn’t think this is the Martin Shkreli of the financial world:

I think this company would re-rate about 50% higher overnight if they brought in a seasoned industry veteran with decades of experience.

For example, don’t you think Robinhood would do better with someone at the helm like well known European banking executive Christian Herzog, who has extensive experience at Deutsche Bank and Barclays and was most recently head of retail trading for years at Bank of Montreal?

Of course you do. And I know you do because you’re impressed by that photo and its literally just a piece of clip art I found when I searched for “investment banker” and “Christian Herzog” is a name I made up out of nowhere.

But I get the feeling that even if they rolled in the clip art guy to the CEO suite at Robinhood looking like this, the stock would re-rate higher. Robinhood shareholders at least deserve someone who looks like they have their shit together while they torpedo the company. With Vlad at the helm, people take one look at the GameStop clusterfuck and a photo of him and say: “Yeah, what did you expect?”

Forget about the new products Robinhood is aspiring to launch (I think they are all good ideas, for the most part), but the company needs an immediate shift in optics even before its shift in financials. And the day Vlad’s frat party ends is the day confidence is restored in Robinhood as a serious player in the financial world.

Now, onto the not-quite-as-ugly-as-it-sounded-but-still-dogshit quarter.

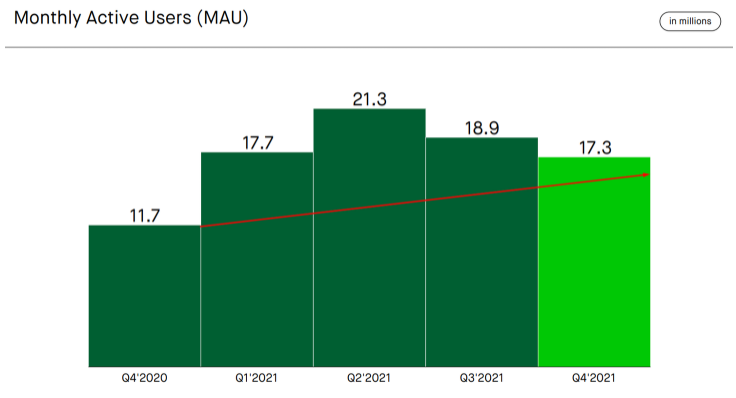

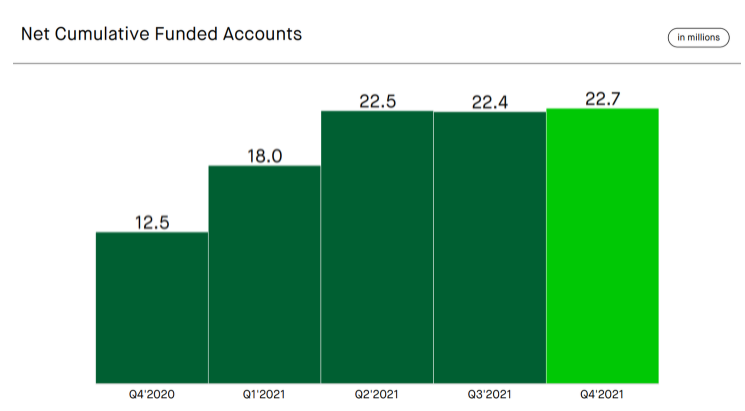

The company saw its monthly active users fall to 17.3 million from 18.9 million in Q3, but its net cumulative funded accounts came in at 22.7 million, which was about in-line with estimates, according to CNBC.

The financials weren’t anything to write home about, either. The company posted a $423 million net loss, missing expectations of a $0.45/share net loss, but slightly beat on revenue, posting $363 million versus estimates of $362.1 million.

Bears will say the numbers are atrocious and you have regression when it comes to MAUs and real concern about the company’s losses. Bulls will say that the company’s MAU number represents leveling off after the meme stock madness and a reversion to the mean that the company was always going to have to face.

Bulls hope that MAUs will level off and steady after a burst of users joined in Q1 2021 due to “meme madness”. They will note that 17.3 million MAUs, despite being a drop, is still an incremental incline and positive trend from Q4 2020:

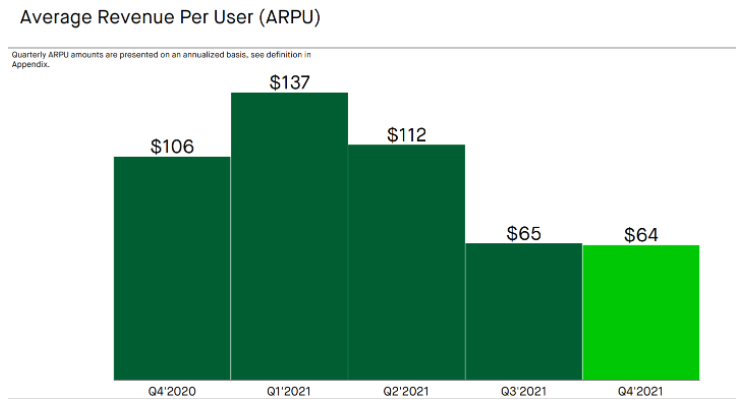

Sequentially, ARPU appears to have steadied:

Net cumulative funded accounts (essentially new accounts, minus accounts that have gone to a $0 balance, plus accounts that have risen back from a $0 balance over a period of time – full definition on slide 29 here), despite the churn from meme stock madness, have remained steady:

Robinhood faces some of its toughest comps for these metrics heading into Q1 2022, which is one year after the infamous GameStop short squeeze and the ensuing months of “meme stock” madness.

Bears are in control after hours, with the stock even dipping under $10 for moment and, no matter how you spin it, shares have been porked since the company’s IPO:

The financials are of some concern to me, though I am willing to give the company a couple more quarters before I start to get nervous about financing. More than the financials, I am keeping a close eye on sentiment, which could really cause an outflow of customer accounts from the name and put the business under pressure, run-on-the-bank style. We’re not there yet – and Robinhood needs to get moving on several things immediately to prevent it:

-

I am encouraged that they are rolling out crypto wallets. They will be able to rip big margins on crypto like Coinbase does and they will become a destination for sending and receiving crypto, as opposed to just buying and selling it. This will increase their user footprint, assuming they get their roll out done in Q1, as expected (or at least before Coinbase moves into equities)

-

I like the idea of expanding into tax advantaged and retirement accounts. I think that names like Fidelity, et. al who may already be potential acquirers for Robinhood will take note that the mobile app one dedicated only to quick daytrading could

-

Before doing any of these things or moving into 2022, Robinhood’s Board of Directors must get Vlad Tenev out of the CEO seat and replace him with a seasoned executive (a former from literally any major investment bank would do immense things for sentiment and market perception of the company)

I nibbled more Robinhood today after hours and will continue to do so into the next quarter, despite the fact that I will be watching sentiment very closely. I am aware that this is an extremely risky bet at this stage in the game, and I have allocated an amount to this investment that I am comfortable with losing 100% of. I am also hedged with puts as a small percentage of my overall position.

But why exactly do I continue to bet on with Robinhood shares?

-

For now, I am betting that competition in the brokerage industry and a red-hot M&A climate amongst brokerages will have numerous suitors looking at Robinhood at this price

-

I am betting that none of the potential suitors are going to want to wait for Robinhood’s equity to become an equity stub or to re-rate much lower before taking the company out of its misery in what will probably be the ugliest take-under of any recent IPO

-

I am betting that a potential acquirer is going to see the company’s 20+ million accounts and $80 billion AUM as more of an asset than the company’s cash burning liability

On a final note, just a reminder that this is not financial advice and that people much smarter than me, two of whom I just read opinions from, stand at stark odds with my investment thesis on this name and believe HOOD is moving much lower. I am only writing about my own thoughts and ideas, presenting what I do with my own portfolio, and am never suggesting anyone do the same – even moreso in inordinately risky special situations like this.

—

If you don’t already subscribe to Fringe Finance and would like access, I’d be happy to offer you 20% off. This coupon expires in 48 hours: Get 20% off forever

Now read:

-

Inflation Is The Kryptonite That Will End Our Decades-Long Monetary Policy Ponzi Scheme

-

When The Global Monetary Reset Happens, Don’t You Dare Forget Why

-

The Fed Is Fucked And So Are The Lobotomized “Genius” Fund Managers It Has Created

-

For Robinhood, Firing Vlad Tenev Is The First Step To Redemption

Disclaimer: I own HOOD and am eating large quantities of shit on my position, but am adding. I own a nominal amount of puts as a hedge. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. I may hedge in any way. None of this is a solicitation to buy or sell securities. Please do not attempt these trades at home. These positions can change immediately as soon as I publish this, with or without notice. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I get shit wrong a lot.

Tyler Durden

Fri, 01/28/2022 – 08:21

via ZeroHedge News https://ift.tt/35lV1VE Tyler Durden