Revisiting The Anatomy Of A Bubble

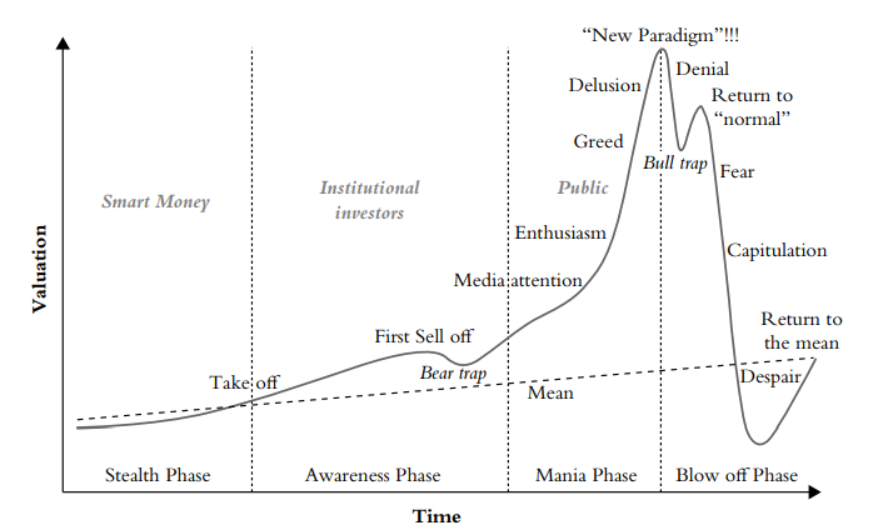

Jeremy Grantham’s recent piece, Let the wild rumpus begin, argued that the US is in its 4th “superbubble” of the last 100 years and is in its final stages. This inspired us to refresh our bubble framework (below, taken from our 2017 blog post). Many valuation measures of the US equity market are near historic highs and with the Fed about to tighten monetary policy, investors should naturally be skeptical of US equity allocations.

We are heavily influenced by the work of Charles Kindleberger and Hymen Minsky at Variant Perception, and we’ve dedicated much of our work to understanding how boom and bust cycles progress.

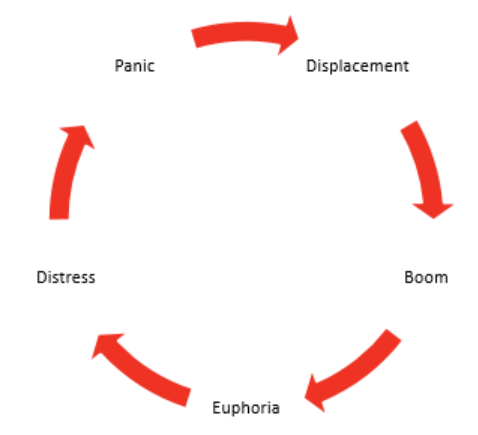

In Kindleberger’s classic, Panics, Manias and Crashes, he expands on earlier work by Minsky in Stabilizing an Unstable Economy. They found that no two bubbles are alike, but they all share a common structure. Below we’ve summarized the five key stages of market bubbles that allow you to identify them as they happen.

-

Displacement:

Bubbles start with a displacement, some sort of a shock to the system. A displacement could be war (usually the end of war), a major political change, deregulation, a technological innovation, a financial innovation or a shift in monetary policy. The displacement creates a new opportunity in at least one sector of the economy. One example is the widespread adoption of computers, the internet and email in the US in the 1990s, which set the stage for the dot-com bubble.

-

Boom:

A boom begins, especially in the favored sector, as optimism grows. There is a positive feedback loop as the price of stocks, one or more commodities, and/or real estate increase, which then leads to greater consumption and investment, which leads to greater economic growth. Credit fuels the boom. Borrowers become more willing to take on debt and lenders are increasingly willing to make riskier loans as economic prospects improve.

This expansion of credit isn’t necessarily provided by banks. The Tulip Mania in 1636 in Holland, for example, was fueled by vendor-financing from bulb sellers. However, banks have been the predominant source of credit since the 19th century. Banks can expand credit further and more rapidly than vendors could. To make matters worse, new banks are often formed in the expanding economy. This causes banks to further loosen their credit standards to avoid losing market share.

-

Euphoria:

A boom transforms into euphoria as “rational exuberance morphs into irrational exuberance.” There are hundreds of books documenting the endless possibilities of the economy (e.g. Japan as Number One and The East Asian Miracle in Japan in the 1980s, and Dow 40,000 in 1999). Participants extrapolate recent price increases into the future, expecting prices to continue to increase at unsustainable rates. Some, especially industry insiders, realize that there is a bubble, but many continue to participate in the market, believing they can sell to “the greater fool” before the implosion.

However, more and more euphoric outsiders begin to enter the market as media attention grows and individuals see others getting rich. As Kindleberger quoted in Manias, Panics and Crashes, “there is nothing as disturbing to one’s well-being and judgment as to see a friend get rich.” The rush of capital causes a further increase in prices, and sound investment shifts to wild speculation. Individuals invest with the hope of short-term capital gains, and debt compounds as people borrow or trade on margin to further speculate. Money seems free. Fraud is also common at this stage, although it typically is not exposed until later.

-

Distress:

At some point, an event hits that causes a decline in confidence and a pause in the explosive price increase. The event could be a bankruptcy, a change in government policy, a piece of news (real or rumored), or a flow of funds from the country. The response to these events differs in bubbles because of the debt build-up. People who financed their purchases with borrowed money become distressed sellers as the income on their assets drops below their interest payments. Kindleberger noted, “The economic situation in a country after several years of bubble-like behavior resembles that of a young person on a bicycle; the rider needs to maintain forward momentum or the bike becomes unstable.”

A slowing bike is actually a better metaphor than a bubble. Sometimes panic sets in immediately, but in other cases it can take up to several years for the crisis to fully develop. In the dot-com crisis, panic happened almost immediately, while it took a few months for panic to set in during the Great Financial Crisis.

-

Panic:

Not everyone realizes that a crisis is unfolding at the same time. Insiders and institutional investors usually sell first. Once other market participants realize the gravity of the situation (perhaps after another major event), run-of-the-mill selling turns into outright panic as everyone tries to get out at the same time. Prices plummet and levered companies increasingly go bankrupt as they can’t meet their interest payments. The sell-off typically spreads to other sectors and other countries. As bankruptcies mount, banks can begin to fail, further drying up credit when it’s needed the most. The panic continues until a lender of last resort convinces investors that cash will be made available to meet demand, or prices fall so low that value investors start to buy back in.

* * *

Get the full picture at variantperception.com.

Tyler Durden

Sat, 01/29/2022 – 11:30

via ZeroHedge News https://bit.ly/3Hee4PW Tyler Durden