Traders Brace For Chaotic FX Market Open As Ruble Set To Collapse

A great deal has changed for Russia (and Ukraine) since the close on Friday and traders are bracing for chaotic movers in bond and FX markets.

Amid ATMs drying up, Central and Commercial bank sanctions (as well as personal sanctions), and talk of SWIFT-constraints; combined with significant credit ratings downgrades, capital flow from Russian assets could accelerate fast as we suspect most traders will live by the ‘Margin Call’ maxim of “be first, be smarter, or cheat” and sell-first before asking questions (despite some potential silver lining from talk of Ukraine being willing to talk).

As Bloomberg reports, sanctioning Russia’s central bank is likely to have a dramatic effect on the country’s economy and its banking system, Elina Ribakova, deputy chief economist for the Institute of International Finance, said before the latest round of penalties was announced.

“This would likely lead to massive bank runs and dollarization, with a sharp sell-off, drain on reserves — and, possibly, a full-on collapse of Russia’s financial system.”

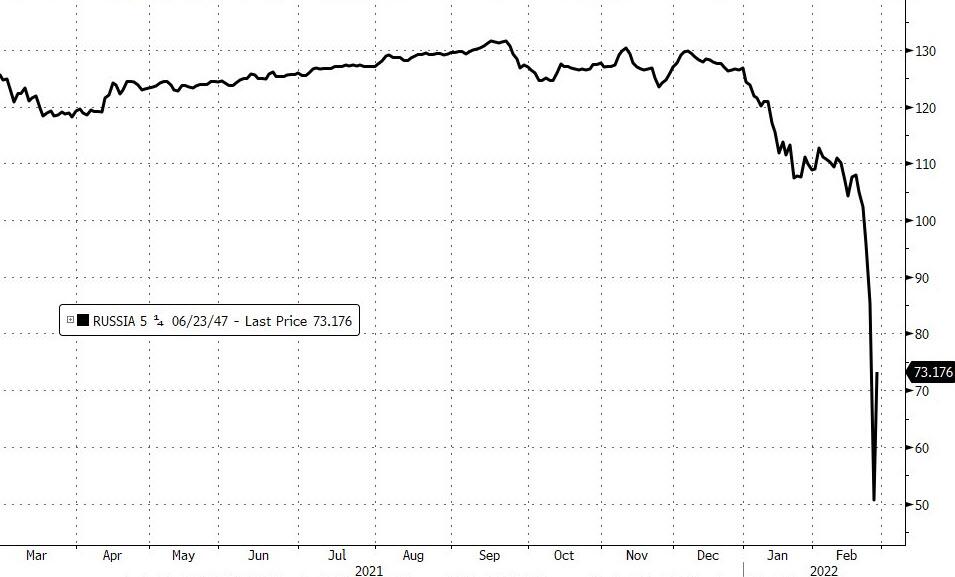

S&P Global cut Russia’s credit rating one notch to BB+ (and Moody’s said it was reviewing for a potential downgrade, which could take Russian debt into junk). Additionally Ukraine was also downgraded to CCC from B.

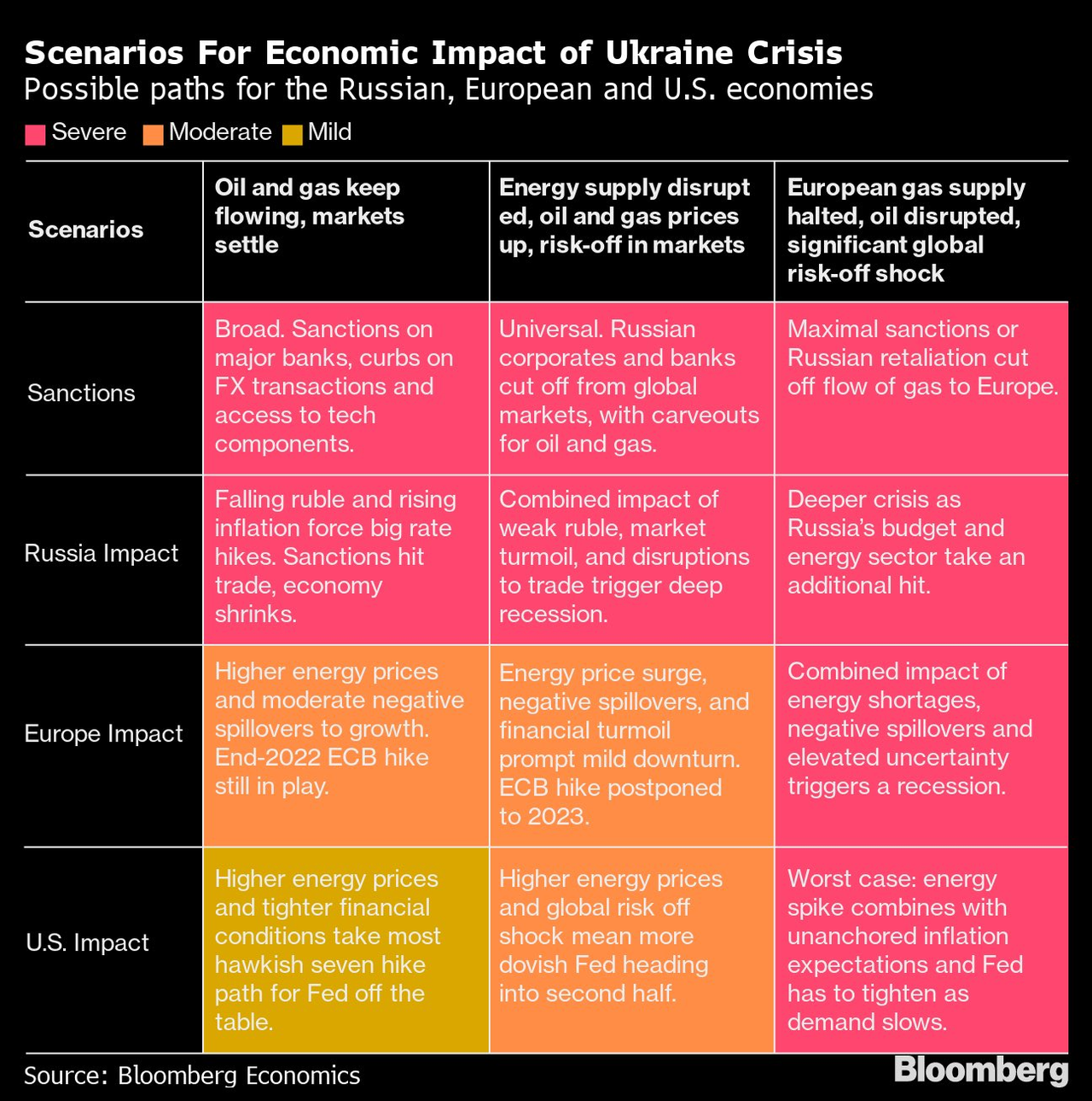

The economic impact of the various sanctions are significant…

There may be less turbulence there since bond prices in both nations have already utterly collapsed…

As we noted earlier, there are indications that the ruble could fall sharply when trading opens.

Exchange rates being offered by lenders (retail) are already varying widely on Sunday, from 98.08 rubles per dollar at Alfa Bank to 99.49 at Sberbank PJSC, 105 at VTB Group and 115 at Otkritie Bank in Moscow.

Russian bank Tinkoff now offering to exchange rubles for dollars at a rate of 171 rubles per dollar. It was 83 before the European/US announcement about targeting the Russian central bank. Currency market formally opens tomorrow. This is brutal. pic.twitter.com/NsTBI4tvTZ

— Paul Sonne (@PaulSonne) February 27, 2022

Those are all dramatically worse than the 83/USD close on Friday…

“Safe havens will likely remain bid in the current environment,” Geoffrey Yu, senior strategist for EMEA Markets at BNY Mellon.

“In currencies, we note that last week the yen and Swiss franc did not materially outperform, so we would just focus on dollar demand for the time being.”

Finally, before US futures open, traders should consider if the ‘relief rally’ – driven by hedge unwinds on the basis that Biden didn’t pull the SWIFT trigger – may be moot since Europe seems hell-bent on some form of SWIFT-restriction for Russia, and the knock-on effects of that liquidity-suck are hard to fathom.

Tyler Durden

Sun, 02/27/2022 – 12:55

via ZeroHedge News https://ift.tt/lq6i24O Tyler Durden