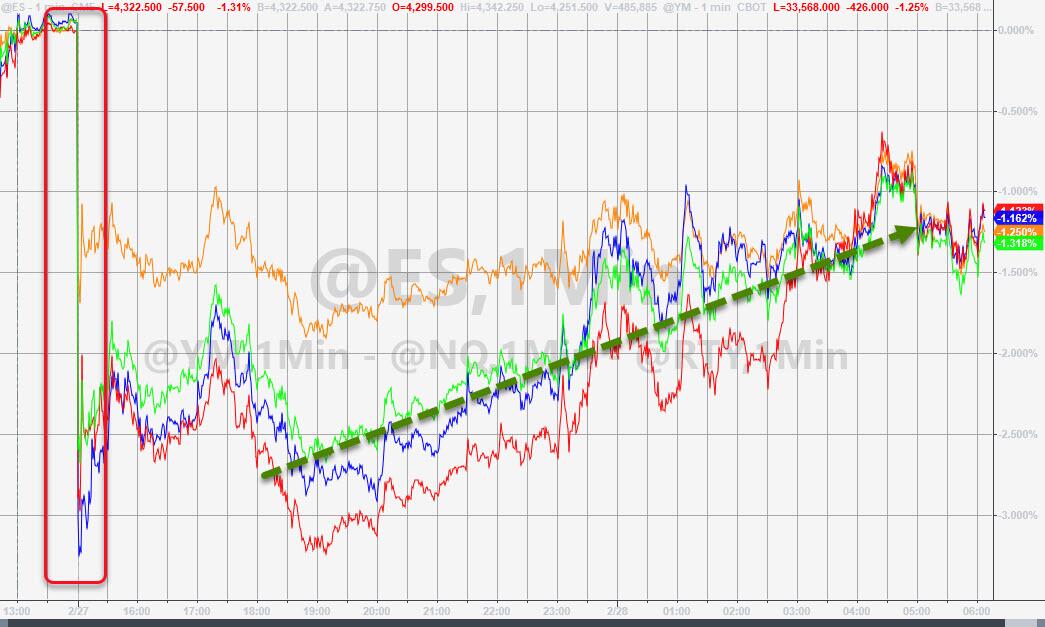

Stocks Bounce On “End Of US Exceptionalism” Trade Unwinds, ‘Short Gamma’ & ‘Plumbing’ Fears Remain Serious Threats

After crashing at the Sunday night open – erasing all of Friday’s melt-up – US equity futures have staged their ubiquitous rebound (though still remain notably lower). Through SpotGamma’s options lens, the market has just simply reverted back to equilibrium after a strong short cover rally.

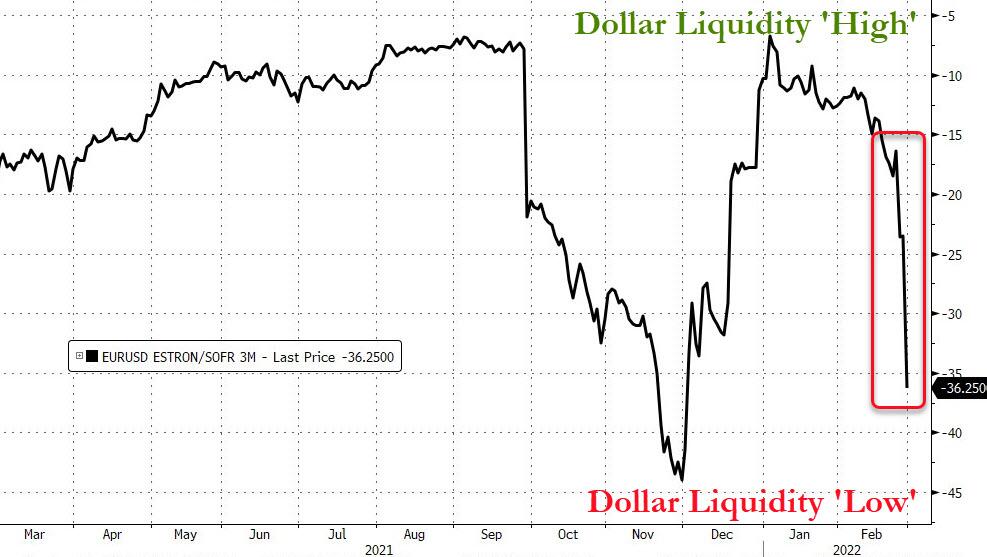

Crucially however, Nomura’s Charlie McElligott warns that the focus in coming-days will likely be in the financial system “plumbing,” where we are seeing expected signs of risk-off – but certainly no current “stress” – in USD funding space, as markets wait for the first fallouts of the Russian liquidity lockout:

Front-end FRA-OIS gapped meaningfully (USFOSC1 +8bps initial), x-currency basis swaps widened (EUBSC -20, EUXOQQC -20, JYBSC -14 – more negative means “more expensive” to borrow Dollars through FX swaps than domestically)…

…and front Mar / Apr ED$ contracts underperformed the rest of the curve contracts (EDH2EDM2 -10 initial), as these markets are beginning to reflect increased demand for- / cost of- Dollar funding…

…but I’d say more anticipatory than anything else at this juncture (so far this morning, no abnormal flows in US bills or repo as of yet)

But for now, the Nomura cross-asset strategist is “watching and waiting”?

Because something, somewhere within the global banking ecosystem will most likely inevitably “break” off the back of the Russian SWIFT exclusion and frozen Bank of Russia assets—potentially in the form of transactions related to the sprawling Russian commodities trade, perhaps with a European subsidiary of a Russian bank being unable to pay liabilities as these “knock-on” throughout the system

To this point on funding stress and who is housing the risk (and as opposed to the pairing of losses in US Eq Index futures), SX7E (EU Banks) has not really bounced at all overnight and remain parked near lows, -6.0%ish with a number of large entities down double-digits on the session (and SX7E -20% in 3 weeks).

Perhaps this is why US Equities are now bouncing off earlier lows this morning… as that “end of US exceptionalism” trade that saw folks unwinding into Europe and R.O.W. DM just a few weeks ago – including EU Banks – now reverses again, and money flows back into US assets.

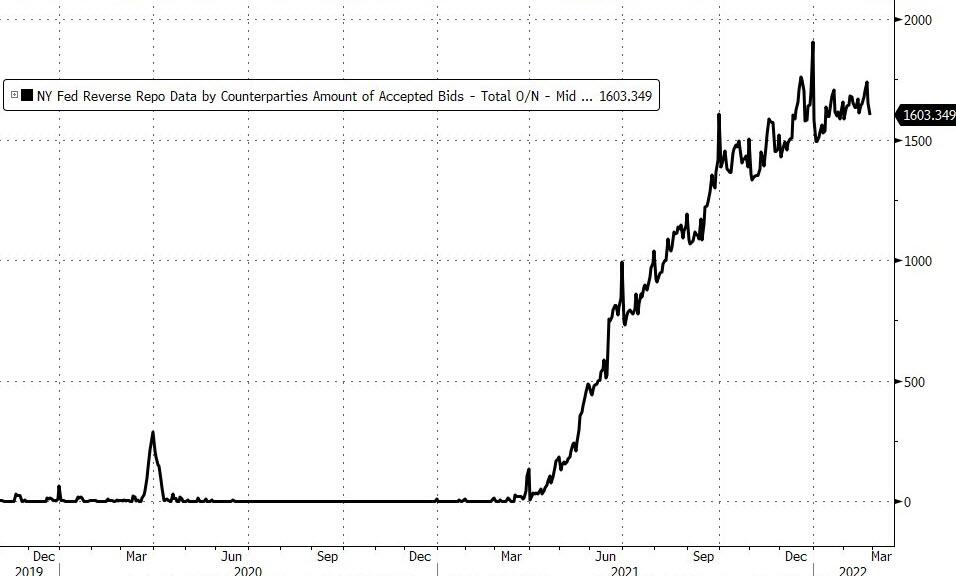

The big “what if?” observation from CS Zoltan’s provocative Sunday piece that has folks talking was the POSSIBILITY we could see headlines soon on Fed daily swap-line activation – hence a key dynamic to watch for in coming-days would be any large decrease in usage of the Fed’s o/n RRP facility, as a sign that the Street is tapping the $1.6T in reserves, in the case that, say, a correspondent were to mush repo markets with collateral (even before QT were to begin).

And I think this stasis around waiting for potential core “plumbing” issues which could see this “geopolitical matter turn systemic” (as well as any new military and / or negotiation updates out of Ukraine) is why Markets and Vol are kinda in no-man’s land overnight (who trades the Sunday reopening, anyhow?!).

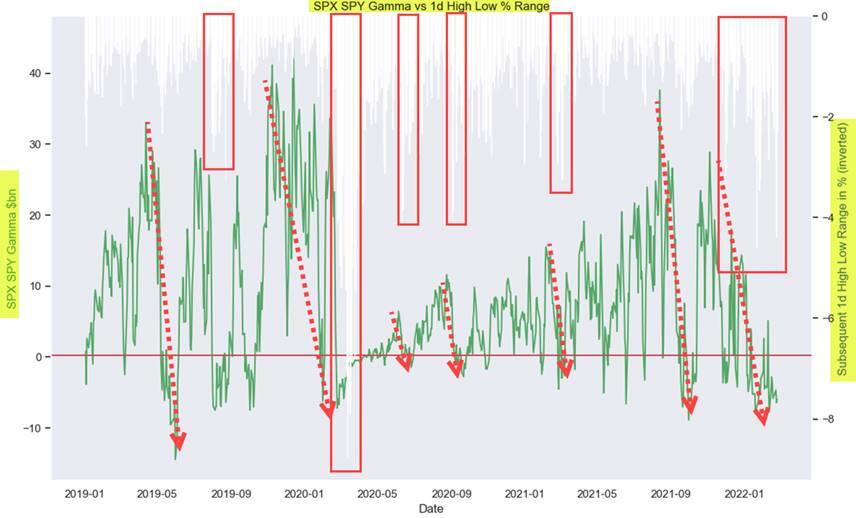

The doiminating theme in equity vol-land remains demand for super short-dated (0-5 DTE) Puts.

McElligott says this will continue to remain a driver of persistent “Short Gamma” trading dynamics which we struggle under, as it siphons from supporting market depth in futures / ETFs / singles, because Dealers turn from (Long Gamma) “liquidity makers” into (Short Gamma) “liquidity takers”.

The ongoing Equities index option Dealer “Short Gamma” environment most obviously created these now daily “overshoots” in both directions, via accelerant hedging flows which “presses” into moves both higher and lower with persistent and larger 1d high-low ranges…instead of the halcyon days of the prior legacy “Long Gamma” regime, where Dealer flows would stabilize markets through liquidity injection, “insulating” or “buffering” large sell-offs with bids, or impulse rallies with offers.

However, as SpotGamma notes, Friday’s expiration did serve to reduce the total amount of negative gamma across the S&P/QQQ.

Therefore, while markets should remain volatile, they should have less movement compared to the extreme moves of last week.

McElligott believes it continues to feel like bounces in US Equities for the foreseeable future likely remain viewed as “rentals” from tactical traders playing short-term positioning and flows (“bear market rallies” on mechnical hedge flows and covering / short-squeezes) and not-yet that “buyable dip,” until we begin clearing the initial Fed liftoff and learn more about plans for the balance-sheet – both of which will act to shrink the distribution of future outcomes and help to suppress volatility thereafter (on top of the backtest of prior “impulse tightening” cycles from the Fed–4 hikes or more first 12m of a liftoff cycle–where on the median, we stabilize nicely in risk t+6m and then broadly rally out +12m).

In the meantime however, ongoing risk of “upside volatility” from US inflation data in the midst of this current “peak” territory – and still “too easy” FCI (Real Yields collapsing deeply more negative in recent days, while Credit Spreads relatively underwhelming from a long-term widening perspective) – remain huge headwinds for the FOMC, who are confronted by consumers at home facing down real price duress and politicians who are focused on this as “the” stress point into US midterm elections later this year.

Hence that idea that the Fed is “selling Calls” in Equity overhead strikes anytime in the next few months if we were to reapproach prior Equities highs – as that would perversely imply an “easing” in FCI which would be counterproduct to said Fed efforts to rein-in inflation from the demand side – hence clients remain comfortable “selling the rips” for these next 2-3 months, until we can then clear the inflation peak and reprice hawkish Fed “behind the curve” left-tails which ultimately sees us move to the “post-tightening” regime and actually look towards a more market-friendly “Goldilocks” economic backdrop, as Fed “easing” then becomes the “next trade”.

Tyler Durden

Mon, 02/28/2022 – 10:12

via ZeroHedge News https://ift.tt/j0eyXux Tyler Durden