“Suffocating” Impact From Higher Rates Will Force The Fed To Ease Much Sooner Than Expected

Back in December, when we first showed that the market had begun pricing in rate cuts as the forward OIS curve inverted, many laughed: after all, such a dire (for the Fed) outcome – one which suggested that the Fed’s tightening would lead to a hard landing, was seen as anathema by the majority who believed (erroneously) that the Fed would keep hiking and hiking and hiking… and the US economy would just somehow take it without imploding.

Well, fast forward to today when nobody is laughing any more.

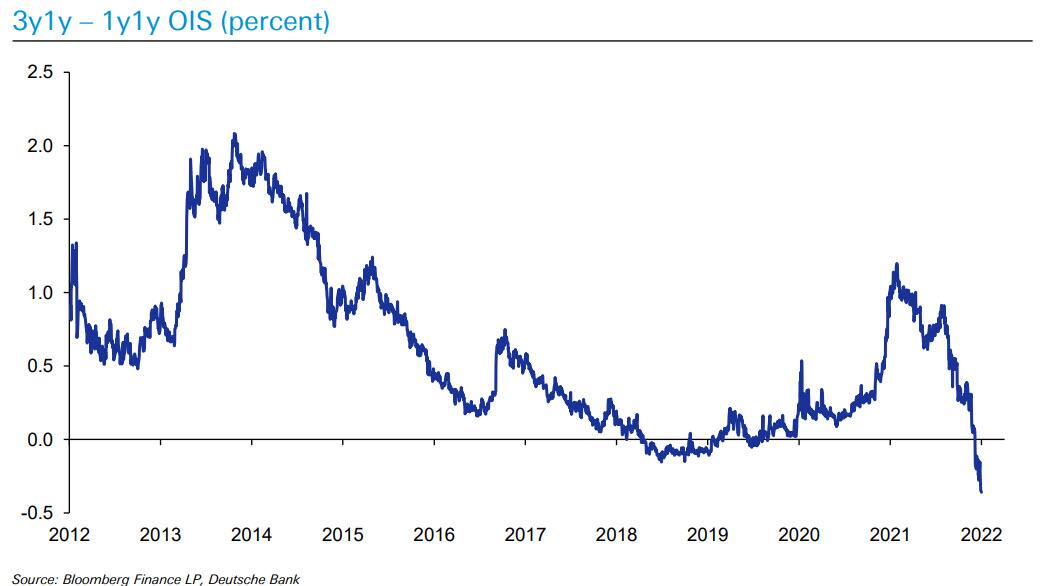

First, as we noted on Sunday, in one of his multiple “market dislocation” charts, DB’s Jim Reid showed a chart of of two-year forward OIS rates (the same chart we pointed to back in December) which are now at their lowest in a decade. As Reid explained, “markets are now pricing the Fed funds rate to be 36bps higher from 2023-2024 than 2025- 2026. Markets are expecting the Fed to have to quickly cut rates shortly after the hiking cycle begins, which looks like a hard landing.“

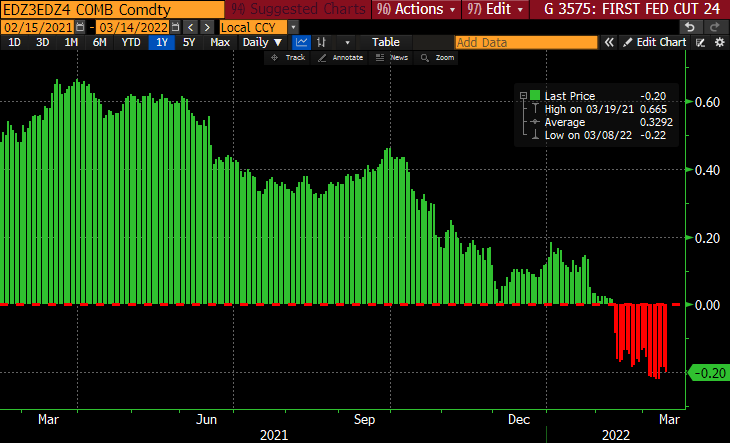

Second, as Nomura’s Charie McElligott writes in his daily note as he previews what the Fed will do on Wednesday, as Powell scrambles to contain runaway inflation (UBS’ economist Paul Donovan said this morning that “there is little a central bank can do about commodity prices—Fed Chair Powell can hardly dig an oil well in the middle of Washington D.C“) “the market expects the hiking cycle to be completed by early / mid ’23 (with the July ’23 – Dec ’23 spread @ -2bps), while a full-blown inversion in EDZ3-Z4 (Dec ’23 – Dec ’24) shows that the Fed’s guidance will turn outright dovish towards easing in ’24 (-20bps priced…i.e. 80% odds of a Fed CUT in that window).” Spoiler alert: the easing will begin in 2023, if not late 2022, but we’ll cross that bridge (soon enough).

Some more details from the CME note:

- I continue to believe that with March done-and-dusted at 25bps, May is absolutely a very high probability of a 50bps move for the Fed, which would then comfortably get us to 5 hikes by end Summer and 7 hikes through the Dec meeting (where market-implieds are already moving / leading the Fed to)

- A front-loaded FOMC hiking cycle would ultimately be the right outcome for the Economy, as it “rips off the bandaid” and gets us to “Neutral” policy rate fast—critically, giving the Fed future optionality across two opposing scenarios moving-forward:

- The first scenario would be to “buy time,” in order to see if inflation “relief” organically appears in 2H22 (i.e. supply chain issues easing in-time, or “demand destruction” from higher prices), which would allow the Fed to accordingly slow tightening efforts and avoid “overtightening policy error” by going fast then pausing, theoretically improving the odds that the economy could be managed back into a goldilocks “soft landing”

- The second scenario would be “if you’re gonna break it, break it fast” move in the case that there is no pull-back in inflation, as the latest Commodities disruption catalysts (Russia sanctions effectively removing their supply from a western world that is “short” them, along with Ukraine infrastructure destruction; new wave of COVID in China seeing lockdowns which further disrupt global shipping / supply chain) only extend the inflation shocks—which perversely then requires global Central Banks to actually seek to “hike us into a recession” so that a growth crash works to destroy demand and regain control over inflation

- And despite these seemingly polar opposite scenarios listed above, the market has already made up its mind as to what it means: EDM3-Z3 shows us that the market expects the hiking cycle to be completed by early / mid ’23 (with the July ’23 – Dec ’23 spread @ -2bps), while a full-blown inversion in EDZ3-Z4 (Dec ’23 – Dec ’24) shows that the Fed’s guidance will turn outright DOVISH towards EASING in ’24 (-20bps priced…i.e. 80% odds of a Fed CUT in that window)

Finally, we go to Bloomberg’s Simon White who today published the most scathing assessment of just how cornered Powell finds himself, and how brief the upcoming rate hike cycle will be, and how the economy is already suffocating from higher rates… even though the Fed hasn’t even hiked once yet, and only concluded QE last week:

Suffocating Impact From Higher Rates to Cause Early Fed Pullback

The Fed is almost certain to hike rates this week for the first time since 2018. Focus will be on how hawkish or dovish the move is. Regardless, higher rates are already having a throttling effect across the U.S. economy, and growth in the U.S. is set to slow sharply this year. Fed hike expectations continue to look too ambitious.

The move in longer-term yields has thus far been relatively contained given the degree of Fed tightening priced in. But the flatness in the yield curve is incommensurate with the degree of uncertainty captured by the rapid rise in inflation and inflation volatility.

GDP is a lagging indicator, and we are already beginning to see the lagged effect from higher rates have a pervasive impact across the U.S. economy. With U.S. 10y rates touching 2.10% and making a 30-month high, that effect will only intensify in the coming months.

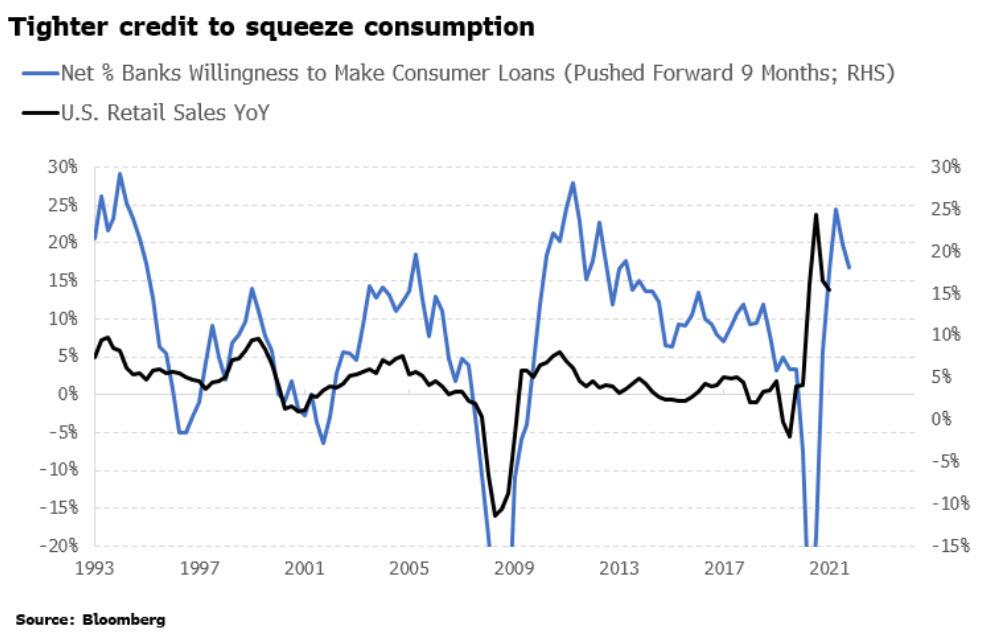

Consumption remains the biggest component of GDP, accounting for about 67% of annual output. Normally, growth in consumption is driven by credit, but stimulus checks and other fiscal transfers drove personal incomes significantly higher during the pandemic, fueling a mini-boom in consumption.

Now that disposable-income growth is beginning to fade, an extension of credit will be necessary to maintain the prevailing rate of consumption. However, rising rates are causing lending standards to tighten and banks are becoming less willing to extend consumer loans. Consumption will face growing headwinds as credit is squeezed.

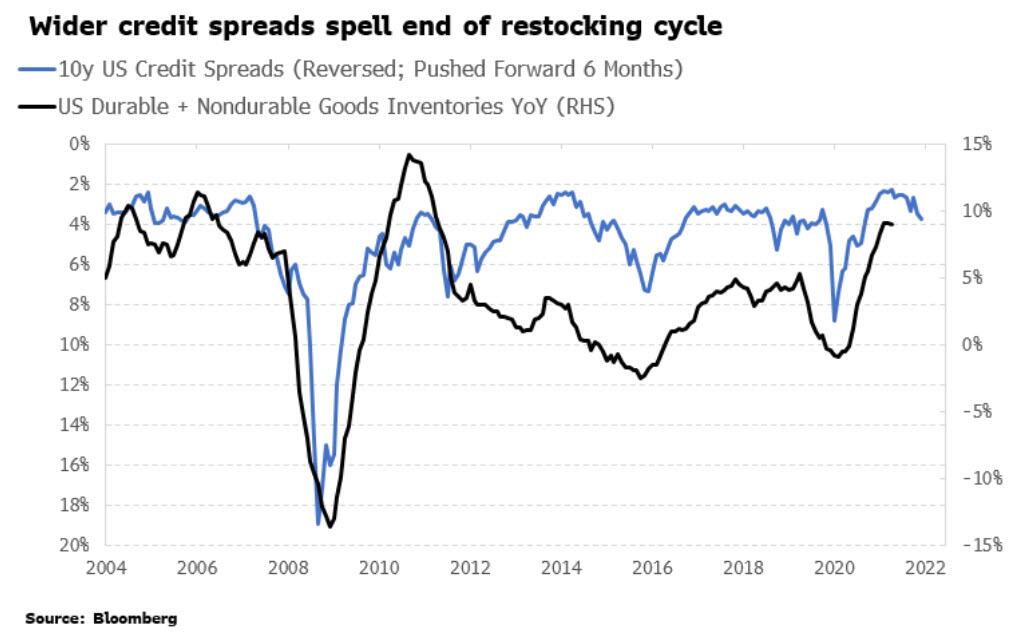

Along with consumption, inventories have been the other main driver of GDP growth in recent quarters. Lockdowns caused widespread factory shutdowns, while demand for goods remained undiminished. Inventories were quickly depleted. As lockdowns eased, firms embarked on an inventory boom. This was seen around the world, with global inventory-to-sales ratios reaching 20-year highs. Now that the demand/supply imbalance is less extreme, the impulse from restocking is set to fade.

At the same time, tighter credit conditions will further hamper the growth contribution from restocking as inventories become more costly to finance. Widening credit spreads point to the end of the current restocking cycle, and GDP losing a significant support.

Housing, too, is facing mounting headwinds from higher rates. The housing market in the US is beginning to look as overvalued as it was in 2005, prior to the housing crisis. The dynamics are different this time — this is a supply-led rise in prices rather than a credit-driven demand one — but once again rising rates are having a deadening impact.

The 30-year mortgage rate has risen over 100bps over the last year, taking the rate to 4.33%. Rises in mortgage rates typically precede falls in building permits, an excellent leading indicator for the housing market overall. Annual growth in building permits has already collapsed from 35% a year ago to only 3% at the end of last year. The malaise in residential fixed investment is soon set to drag non-residential investment lower too. Both sectors together account for almost 20% of GDP.

GDP should continue to slow this year as the impact of higher yields filters through the economy, bringing into question whether Fed rate hike and balance-sheet contraction expectations will be met.

Of course, this is all according to plan: as we said more than a month ago in another view that roundly mocked at the time and has now become consensus, the Fed is now desperate to start a “soft” recession (in order to create the demand destruction needed to send commodity prices lower) but without also crashing the market.

Fed desperate to figure out how to start a soft recession without also crashing the market

— zerohedge (@zerohedge) February 10, 2022

Alas, as recent events in the stock market have demonstrated vividly, the Fed is finding it impossible to have a “gentle” recession, one which does not crash stocks as well. The question is what the Fed will do then.

Tyler Durden

Mon, 03/14/2022 – 14:53

via ZeroHedge News https://ift.tt/WZP15bT Tyler Durden