McElligott: Game On

From Nomura’s Charlie McElligott

Game One

SUMMARY: I go over the latest risk macro catalyst datapoints overnight from China (wow!) and Russia / Ukraine “compromise” progress, particularly as that further interacts with the mechanical factors behind my anticipated rally scenario into / around Op-Ex that were on full-display yesterday; from here, a very hawkish Fed caps medium-term upside, as the Fed has to remain heavy-handed on FCI tightening into the upcoming 2-3 months of “peak” upside inflation surprise risk—which also just-so-happens to align with our prior backtest of “front-loaded” Fed hiking cycles, as the 2 months post liftoff typically sees the peak of the Equities drawdown

First thing’s first, the Nomura Econ Team’s expectations for a very hawkish FOMC meeting at 2pm today (our hike projections see us getting to a terminal rate of 2.875% in 2024 vs FOMC’s long-run projection of 2.5%–i.e. “mildly restrictive”):

We believe the March FOMC meeting will continue the Fed’s hawkish pivot towards combating elevated inflation, with a focus on getting to a neutral policy setting quickly. Along with a 25bp rate hike, the first since the pandemic, we expect the updated dot plot to show 11 cumulative 25bp hikes forecast by end-2024, including six in 2022. The Committee has rapidly coalesced around getting rates to a more neutral setting soon, including front-loaded rate hikes. The updated dot plot will likely also show rates going into mildly restrictive territory, adding fuel to what will be an important debate in coming months. The post-meeting statement is unlikely to provide any concrete guidance on the pace of post-liftoff rate hikes beyond acknowledging that additional hikes are likely, with the size and pace being data-dependent. The FOMC will likely release an addendum to its balance sheet normalization principles, outlining the maximum monthly runoff caps and how quickly those caps will be reached. During the press conference, we expect Chair Powell to lean into the notion that the Fed is prepared to do “whatever it takes” to ensure high inflation does not become entrenched. We continue to expect seven 25bp rate hikes in 2022, plus an additional two hikes in 2023, with a growing risk of a 50bp hike later this year, potentially as early as May. A May balance sheet runoff announcement is likely, effective June.

Last week’s acceleration of the global risk-market hemmoraging is now seeing a sharp and swift reversal over the past 24 hrs and into today’s long-awaited FOMC policy “liftoff’ main-event—as yesterday’s prolific US Equities mechanical “positioning” –squeeze rally (profound covering in short books and dynamic hedges, alongside substantial options Dealer “short Delta” unwinds—more below) is further goosed overnight (Broken-market chronicles: Spooz at highs +4.4% off yday’s lows, with euros DAX +6.0% & Estoxx +6.3% LOL) with a profound verbal intervention from Chinese authorities in equities- and property- markets, on top of still-further “constructive language” on Ukraine / Russian compromise–*KREMLIN: NEUTRAL UKRAINE W/ OWN ARMY POSSIBLE COMPROMISE OPTION

It looks like we just saw China’s own “whatever it takes” stock- and real estate- market moment overnight too: In one fell swoop, China’s State Council pledged stock market stability, support overseas listings, stated that the dialogue with US regarding ADRs is “good,” promised to handle risks for property developers and clarified that regulation of Big Tech will end “as soon as possible” per a report by “official” Xinhua news, citing a meeting chaired by Vice Premier Liu He

(Government Departments should) “…actively introduce policies that benefit markets” according to the meeting of China’s top financial policy committee led by Vice Premier He

And later there was even more centrally planned pile-on, with PBoC head Yi holding a meeting on the aforementioned State Council’s vow of market support, saying that the central bank too will “ensure” a stable stock market with other agencies, while the CBIRC then too pledged supporting property project M&A, voiced a vow of support for direct financing and stating that they will release policies which can benefit the market

With that, a historic boom in their Equities—Chinas’s Shanghai Comp closed +3.5% and CSI 300 +4.3% (largest 1d return since Jul ’20 for both), while incredibly in HK, the Hang Seng closed +9.0%, HS China Enterprises Index +13.0% for its largest move since the 2008 crisis, and HSTECH an astounding +22.2% at the highs in its largest 1d move ever

Will this stick? Difficult to say, especially after prior assurances of market support from securities regulators in July ’21 and September ’21 clearly did not stop the bleeding; but after authorities allowed the market freefall in silence over the past few months which saw investors liquidate their positions, today the State Council now told those same people that it’s time to get long again

What will be “more than critical” moving-forward in order to sustain the bullishness will be the follow-through, as Ting Lu expects the PBoC to take actions to bolster credit growth and do some policy easing imminently / in coming-weeks

This Chinese bounce should also be of significant relief to many US Tech investors who’ve been turned to dust after finding themselves stuck in a number of these Chinese ADRs, and with this “good news” coming fresh off the heels of what already was a substantial relief rally yesterday in US

So on that note, and regarding yesterday’s US Equities behavior—there is no doubt the rally was a whopper—but was it actually “constructive” and indicative of some sentiment turn?

My short answer is “ehhh, not really,” as it mirrored what I have already been anticipating, which was a rally that was largely a function of mechanical flows and hedging dynamics which left us open to a violent move higher this week—particularly around Op-Ex:

The previously laid-out dynamics and thought-process were as follows:

- Chronic underpositioning / netted-down funds and with shorts dialed-UP, which were then going to be particularly susceptible to a squeeze, particularly in futures shorts which they’ve been dynamically-hedging with (preferred now by many clients, as options have remained so expensive)—which is a source of implicit “Short Gamma” in the market, as they have to buy into rallies (or sell into weakness)

- And all that well publicized client loading into downside / Put options too would be set to “bleed” in the face of a rollover in implied Vol (UX1 -4.5 vols from the past week’s highs) with this “Vanna” impact providing broad market support alongside natural “Charm” (Put decay) as we approach Friday’s mammoth serial Op-Ex, due to the virtuous feedback loop of those large and now deeply OTM Put strikes rallied away from, as Dealers buy-back their futures shorts

- So with shorts forcibly covered, this would contribute to an extension of the ongoing “gross-down” optics (recent losers HIGHER, recent leaders LOWER), which is somewhat reasonable into today’s event-risk, where the Fed will commence the new policy tightening cycle

And that looks like much of what we experienced yesterday…

To the first point above, our futures imbalance monitor showed RAGE buying of NQ futures all day as offers were aggressively lifted in a forced covering manner, with the single-biggest “buy pressure” day for large lots size seen in Nasdaq futures over the past month, with the third-largest day for medium lots of the past month, and making the aggregate buy impulse in Nasdaq minis the fourth-largest over the past month across all lot sizes

To the second point on the likelihood of options Dealer covering of “short hedges” due to changes in greeks into Op-Ex, the day-over-day $Delta changes picked-up massive positive Delta adjustments:

- SPX / SPY Net $Delta went from -$592.1B to -$536.5B, a +$55.6B DoD change

- QQQ Net $Delta went from -$43.0B to -$33.5B, a +$9.5 DoD change

- IWM Net $Delta went from -$15.5BB to -$12.8B, a +$2.7B DoD change

- HYG Net $Delta went from -$19.8B to -$15.1B, a +$4.7B DoD change

Desk flow –wise, the “positive Delta” did see some macro product “offense” being played (FXI buyer 7.5k May 33 and 34 Calls, XLF buyer 14k Mar 37.50 Calls)…but by-and-large, it was about downside being taken-off / closed (LOTS of selling downside in Singles, along with FEZ massive Put Spread sellers in mkt, HYG seller 50k Mar 77 / May 75 PS, XLE seller 10k Mar 72 / 69 PS)

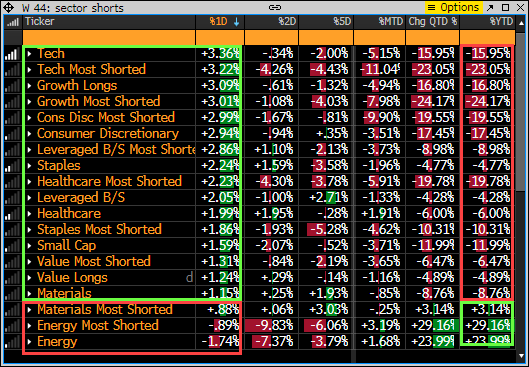

So then accordingly, the entire trade yesterday looked like a “gross-down,” as almost every single performance theme year-to-date was REVERSED IN SIZE yesterday across US Equities sectors, themes and factor risk-premia—as “losers were loved” while “leaders turned laggards” (shorts covered, longs sold)

So yes, mechanical catalysts are there and remain loaded for more supportive flow into Op-Ex—particularly as so much of the anticipated Gamma “unclench” is predominately downside Puts being set to expire

The Vanna tailwind and declining iVol will also matter here, bc an extension of “lower iVol” will help reduce the already now less extreme Dealer “Short Gamma vs Spot” position, pushing us ever-closer to the “Zero Gamma” levels across key index / ETF, and even potentially into that market stabilizing / vol compressing “Long / Positive Gamma” location

SPX / SPY still “Short Gamma vs Spot,” approx -$5B per 1% move, Gamma flips positive at 4389, 39% Gamma drops-off Friday

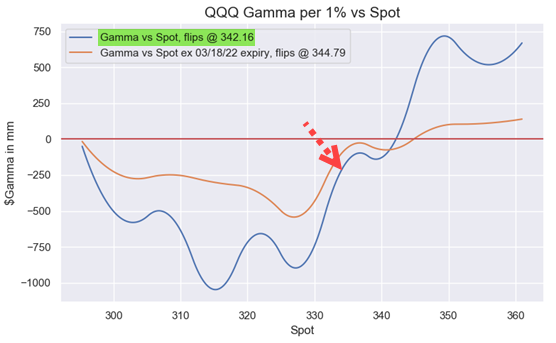

QQQ still “Short Gamma vs Spot,” approx -$225mm per 1% move, Gamma flips positive at $342.16, 50% Gamma drops-off Friday

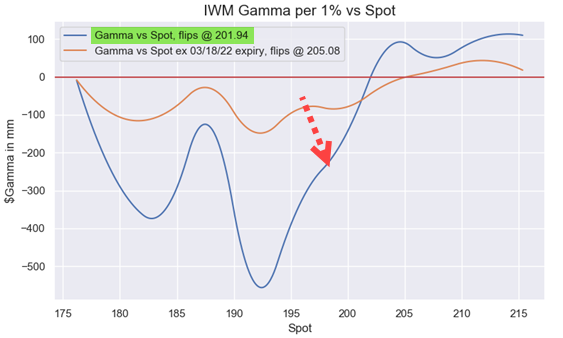

IWM still “Short Gamma vs Spot,” approx -$225mm per 1% move, Gamma flips positive at $201.94, 65% Gamma drops-off Friday

Nevertheless, and in-line with status quote messaging, we will continue range-trading in Equities on account of what I believe to be high liklihood that the Fed simply has to “take what the market is giving them” with still easy FCI meaning they must hawkishly hike until inflation abates, either from demand destruction…or preferably to them, through “natural causes” as supply kinks are worked-out (ehhh…not being helped by recent Chinese resumption of lockdowns and Russia / Ukraine Commodities shock—for which there is no “off-ramp” to Russian sanctions)

Market odds are currently in-favor of the prior scenario, where they hike until the economy forcibly slows…and in a particularly front-loaded fashion, as inflation is their overriding mandate now, and is nearing “left tail” status, with the next 2-3 months as “peak” of inflation upside surprise risk

This 2-3 month “inflation upside risk” window will keep the Fed totally focused on tighter FCI, and that should see upside capped in Equities, because rallies will have to be “leaned into” with increasingly hawkish rhetoric in order to prevent counter-productive EASING in FCI that would work against their efforts to crimp from the demand-side

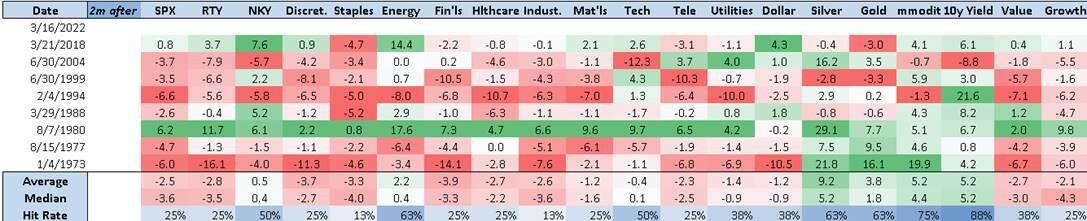

And this view then fits / aligns with our separate backtest of prior Fed “front-loaded” hiking cycles (defined as “4 hikes in the first 12m of the cycle”), where the peak of the Equities drawdown is seen around the “2 months in” (post initial hike) window

Tyler Durden

Wed, 03/16/2022 – 10:22

via ZeroHedge News https://ift.tt/vKhFrsI Tyler Durden