The Fed’s Feckless Inflation Fight

Authored by Michael Maharrey via SchiffGold.com,

The Fed is supposedly about to step into the ring to fight inflation. But all indications are it’s going to be a feckless fight.

Gold flirted with an all-time record high last week driven in part by safe-haven demand due to the geopolitical uncertainty caused by Russia’s invasion of Ukraine. But as the war drags on and the panic subsides, that safe-haven bid seems to be unwinding.

Now investors have turned their attention back to the Fed. When the war broke out, people thought it could slow the central bank’s monetary tightening plans. But with a 7.9% CPI print for February, the mainstream is back on the tightening bandwagon. They’re betting the central bank is going to tighten fast and hard, and they’re selling gold on the expectation of higher interest rates.

But even if the Fed does what the market is betting it will do, it’s not going to put a dent in inflation, and interest rates will not rise high enough to undermine gold.

According to a Reuters article:

A key money market indicator is now pricing US interest rates peaking at a higher level than previously forecast, as traders bet that the Federal Reserve will prioritize stamping out inflation over fretting about risks to economic growth.”

And just how high are they betting interest rates will rise?

2.5%

That’s it.

They think the Fed will push interest rates to 2.5% by mid-2023.

Goldman Sachs economist Sven Jari Stehn is betting on the high side. He thinks the so-called “terminal rate” will come in between 2.75 and 3%.

This is supposed to “stamp out” 7.9% inflation. (Which is really 15-plus percent inflation is measured honestly.)

Paul Volker went to war against inflation in the early 80s. He pushed interest rates to 20%. He had to in order to get ahead of the inflation curve.

In other words, if we accept the government’s 7.9% CPI, the Fed would have to push interest rates to at least 9% to get above the inflation rate in order to “go to war” with inflation.

And they’re talking about 2.5% as if it were some kind of nuclear bomb.

The thinking here is muddled and silly.

Nevertheless, any rate hike is seen as a negative for gold. Whenever interest rates tick up slightly, the mainstream is quick to inform us that “rising interest rates increase the opportunity cost of holding gold.” This is why we’re seeing another selloff in gold as everybody gears up for the March FOMC meeting.

So, what exactly is the mainstream thinking here?

Holding gold does not generate interest income like a bond or a bank account. If interest rates rise and you’re holding gold, you’re forgoing the interest income you could earn if you instead owned a bond or put dollars in a money market account. That’s why rising interest rates tend to create headwinds for gold. And it’s why we saw gold sell off on every bit of high inflation news last year. The markets expect the Fed to fight inflation with rate hikes, thus raising the opportunity cost of holding gold.

This makes sense on the surface, but there is a problem with this mainstream analysis. They are not thinking in terms of real interest rates.

Consider the 10-year Treasury. Currently, the yield is around 2.1%. With a 7.9% inflation rate, the real interest rate on the 10-year is -5.8%.

To state the obvious, there is no “opportunity cost” in holding gold when real rates are deeply negative. You are losing real money holding bonds that aren’t yielding enough interest income to keep up with inflation.

At some point, the markets will figure this out.

It’s also highly unlikely that the Fed will ever get to 2.5%. As you’ll recall, when the Fed started tightening in earnest after the 2008 meltdown, it barely got above 2% before the economy went wobbly. The stock market tanked in the fall of 2018 and the central bank went right back to rate cuts and QE.

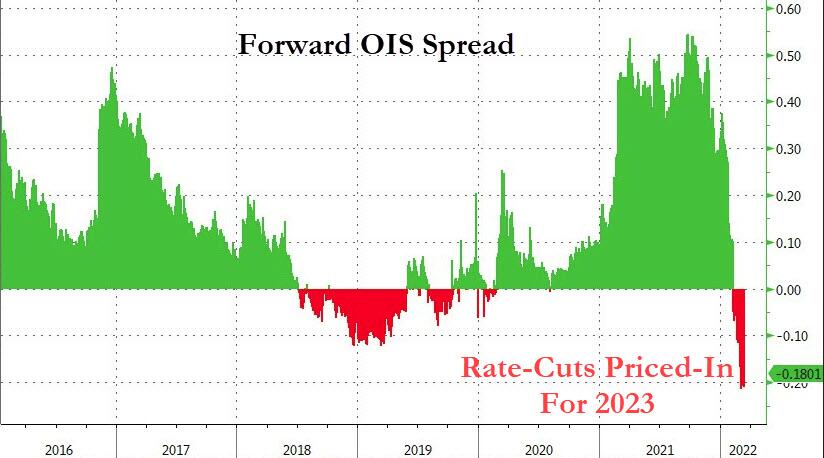

[ZH: On a side note, the market is pricing in 1 hike today, a 60% chance of a 50bps hike in May, and 7 rate-hikes in 2022…

[ZH: But, it is also pricing in rate-cuts next year and more in 2024…

Today, the bubbles are even bigger. The levels of debt are even higher. How will the Fed raise rates substantially in this environment? I think they’ll be doing good to even get to 1%.

Here’s a question to ask yourself: do you think the Fed will keep hiking rates if the markets tank and the economy slides toward recession?

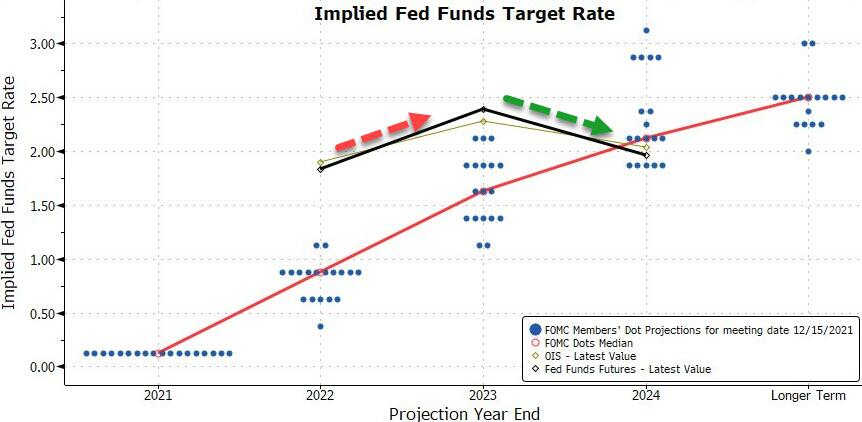

[ZH: The market really does not believe The Fed will keep hiking…

Most people aren’t paying any attention to real interest rates — at least not yet. Right now, they’re distracted by negligible nominal interest rate hikes in the Fed’s feckless “war” on inflation. But this will almost certainly change soon.

The markets can remain delusional for a long time. But they can’t remain delusional forever.

Tyler Durden

Wed, 03/16/2022 – 08:10

via ZeroHedge News https://ift.tt/byJShRg Tyler Durden