Volatile Commodities Force Investors To Sell

By Tatiana Darie, Bloomberg Markets Live commentator and analyst

Nickel’s blowout and oil’s roller-coaster this year show commodities have become more volatile across the asset class. That’s a problem because volatility begets volatility as investors are forced to rein in exposure or pay higher hedging costs.

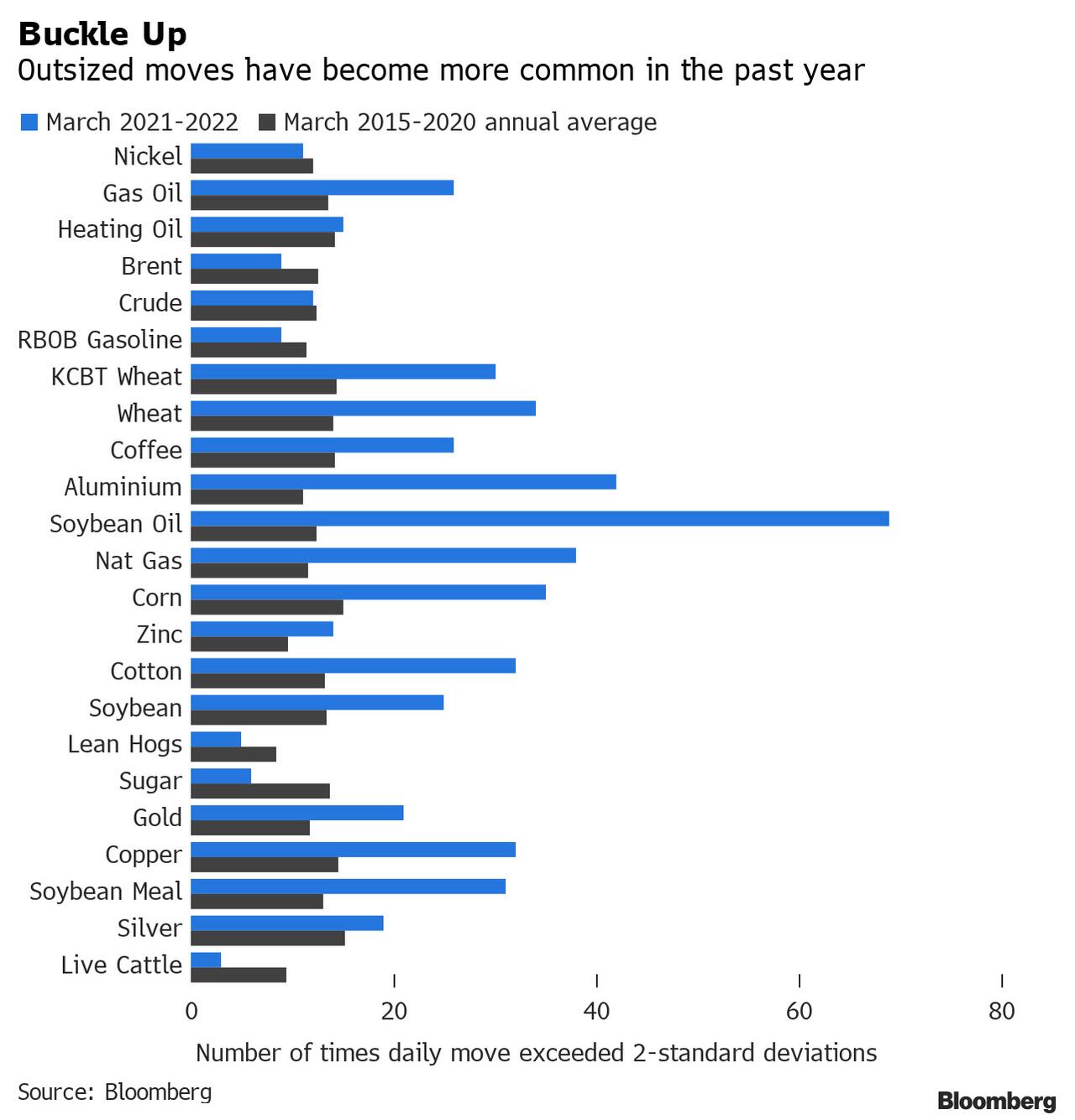

In the five years before Covid-19 struck markets, the Bloomberg Commodity Index saw daily moves larger than two-standard deviations on average about 14 times per year. Then, in the past year, we suddenly had 33.

The index’s absolute daily average move has increased by 38% over the past year. Its standard deviation rose to 1.2% from 0.8% during March 2015-2020.

Looking under the hood also reveals that 16 out of 23 components in the index had a similar dynamic: they’ve moved above or below two-standard deviations more often in the past year than pre-pandemic. Also, 17 out of 23 commodities have seen their absolute average daily move increase since 2021 versus the prior period.

Big swings make it harder to trade and also make hedging more expensive. It forces money managers targeting a certain level of volatility across portfolios to cut exposure. Greater volatility also creates higher hedging costs via options pricing.

That’s part of the reason why hedge funds have been selling in recent weeks, taking some steam out of the sector’s rally, according to Saxo Bank’s head of commodity strategy Ole Hansen. And that’s also why oil slumped last week.

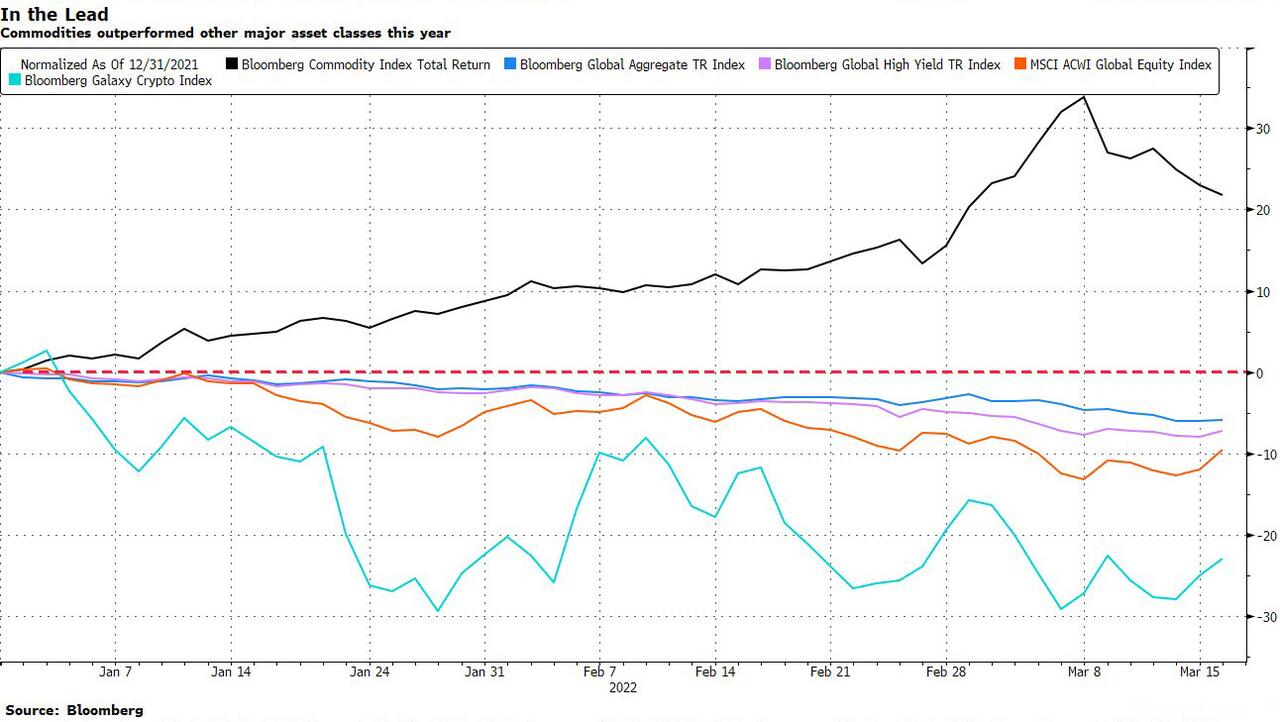

That, coupled with the fact that a quick jump in prices tends to hurt demand, could spell risks for the best performing major asset class this year and the most crowded long trade, per Bank of America’s latest global fund survey for the week ending March 10.

A breakdown of the most volatile commodities shows natural gas, aluminum and soybean oil at the top, seeing nearly three, four and six times more two-sigma events over the past year versus the average of the pre-pandemic period. What used to be a two-standard deviation move for soybean oil, one of the most used in cooking, has become the norm, being exceeded in almost every fourth session since March 2021.

Surprisingly, nickel, Brent and crude oil have been among the more stable commodities, seeing fewer outsized moves. Brent has actually seen its average absolute daily move slip to 1.58% over the past year from 1.60% seen pre-pandemic. At 1.71%, WTI’s is largely unchanged.

Other resources that have seen large moves less frequently than in the past include: gasoline, lean hogs, sugar and live cattle.

The study analyzed futures daily price movements to look at how many times a given commodity moved outside of its pre-pandemic two-standard deviation derived from March 9, 2015 to March 9, 2020. It then applied it to the past year starting March 9, 2021.

As market observers like to say, commodities are their own worst enemies when they jump in price as quickly as they did in March. They’ve proved to be a great bet for investors this year so far, but only for those who’re able to handle the stomach-churning gyrations.

Tyler Durden

Mon, 03/21/2022 – 21:00

via ZeroHedge News https://ift.tt/4fw7gdE Tyler Durden