“Hard Landing Virtually Inevitable” – Countdown To Recession Begins As 2s10s Curve Inverts

While several asset-gatherers and commission-rakers will try to gaslight investors into monitoring the steepening in the 3M2Y spread – “see no recession to fear there”; for anyone who has actually lived through a Fed hiking cycle, or has read any market history, the 2s10s curve is the most-monitored, the most-studied, and the most accurate predictor of recession the market has to offer.

And today, after a long wait…

waiting for the 2s10s to invert pic.twitter.com/58y3sPTb7X

— Newsquawk (@Newsquawk) March 29, 2022

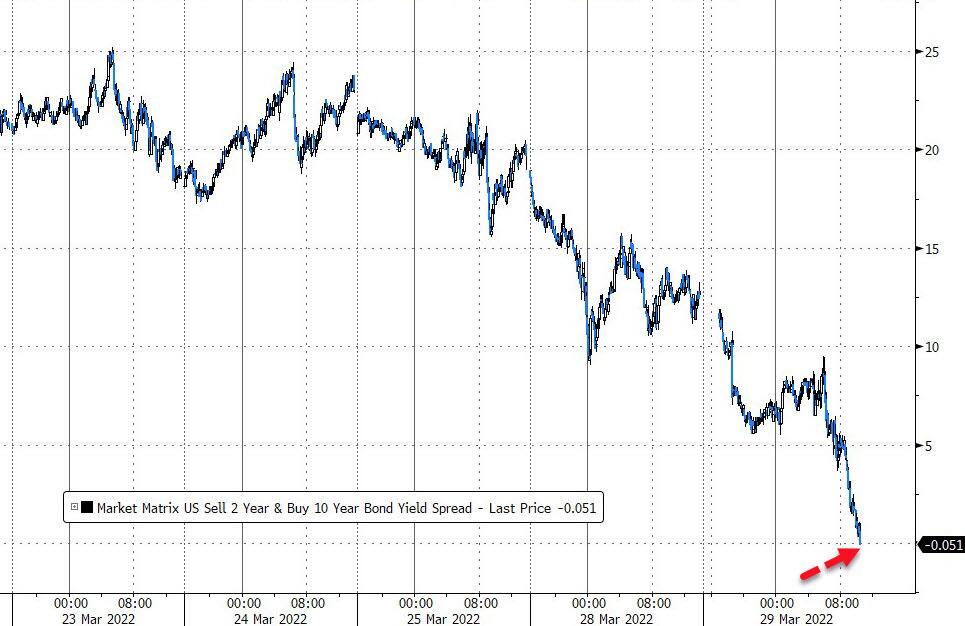

…2s10s has finally inverted…(according to Bloomberg data 2s10s spread was -0.23bps)

…chasing the rest of the curve (3s10s, 5s10s, 5s30s, 20s30s) all into inversion…

As Deutsche Bank’s Jim Reid notes this morning, there has never been such a directional divergence possibly because the Fed have never been as behind the curve as they are today.

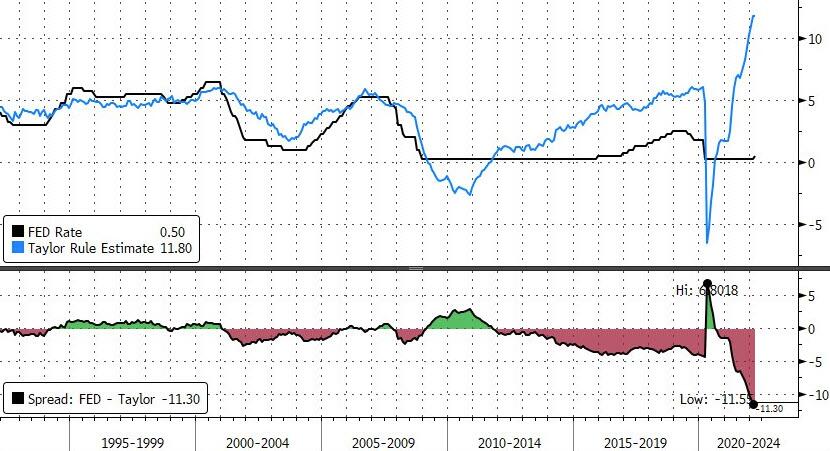

For a sense of just how far behind, The Taylor Rule suggests given the current inflation rate and unemployment rate, The Fed needs to hike by an absurd-sounding 1155bps to get back to ‘normal’…

But back to the divergences in the curve, Reid notes that the remarkable thing is that the two have always gone hand in hand directionally until around December 2021 when 3m10s started to steepen as 2s10s collapsed.

If market pricing is correct, they will rapidly catch up over the next year so it’s possible that in 12 months’ time this measure will be flat.

As a reminder, every hiking cycle that has inverted the curve has led to a recession within 1-3 years.

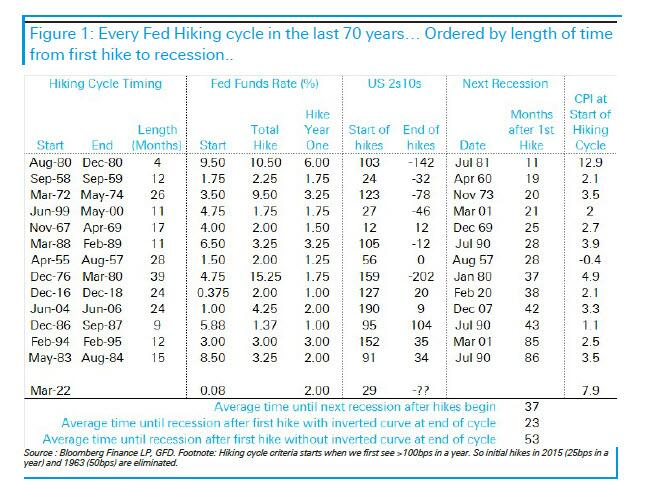

The table from DB below shows the details of every Fed hiking cycle over the last 70 years alongside the time to recession, yield curve shape, and inflation at the first hike. DB has ordered this by length of time from first hike to recession to demonstrate that the quickest recessions following hikes were associated with an inverted curve by the time the Fed stopped hiking.

On average it takes around three years from the first Fed hike to recession. However all but one of the recessions inside 37 months (essentially three years) occurred when the 2s10s curve inverted before the hiking cycle ended. With all the recessions that started later than that, none of them had an inverted curve when the hiking cycle ended. In fact, hiking cycles that ended with the curve in positive territory saw the next recession hit 53 months on average after the first rate hike, whereas the next recession for hiking cycles that ended with an inverted curve started on average in 23 months, just under two years. All these cycles eventually saw an inverted curve but this happened after the Fed stopped hiking. As a reminder, none of the US recessions in the last 70 years have occurred until the 2s10s has inverted. On average it takes 12-18 months from inversion to recession. Then again, the Fed has never before started a rate hiking cycle when inflation was already 7.9%.

Many would prefer to ignore this indicator, or make general excuses for why it’s different this time “because of QE”, “because of COVID”, “because of Putin”, but as Jim Reid explains so eloquently:

…for me I think about it very differently. I don’t care why the curve inverts as I think the transmission mechanism is through animal spirits. When a curve is steep it should encourage entrepreneurial behaviour as borrowing costs at the front end are low relative to potential returns. In an inverted curve environment, the rational investor/entrepreneur/business should be more risk averse and either place more money in safe assets at the front end or do less animal spirits enhancing longer-term investments/economic activity.

As Reid notes, this all operates with a lag but if I exaggerate to illustrate, if 2yr yields are 5% and 10yr yields are 1% then rational economic agents will be highly likely to park money at the front end and wait for better opportunities irrespective of how negative the term premium is.

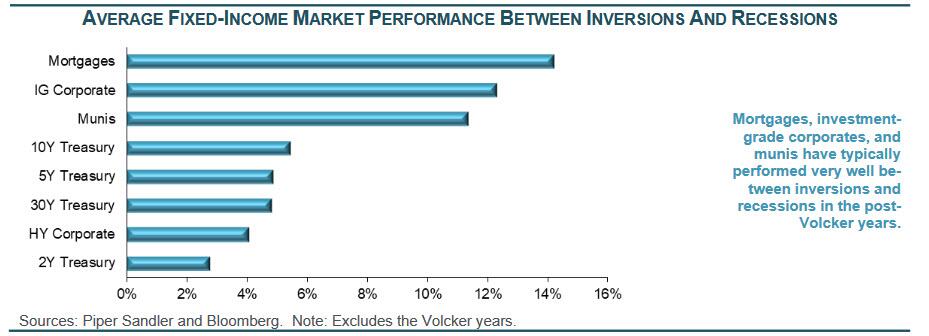

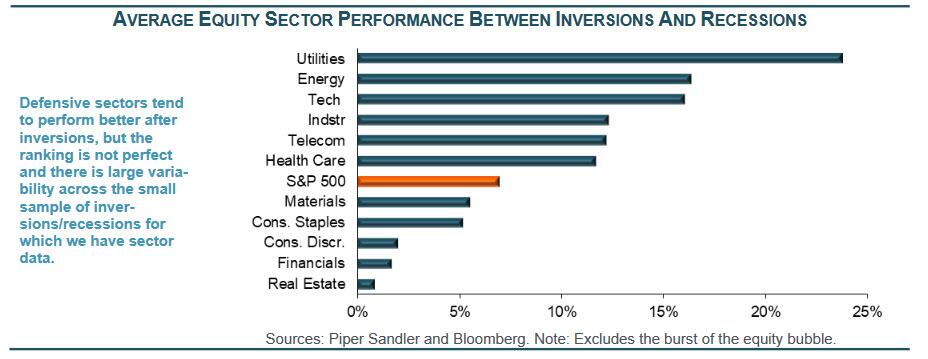

But, as a new Piper Sandler study finds, stocks and bonds tend to do quite well in the window between yield-curves inverting and the onset of the actual recessions.

“The broad stock-market appreciates between inversions and the onset of the subsequent recession,” Roberto Perli, the head of global policy at Piper Sandler, wrote in a note with his colleagues Tuesday.

“With the exception of the Volcker years, fixed-income assets always appreciated, with mortgages, investment-grade corporates, and munis as top performers.”

“Overall, the message seems clear for equity and fixed-income investors alike: Don’t get too gloomy as soon as the yield curve (or a portion of it) inverts — doing so is very likely to leave performance on the table,” Perli wrote.

We do note that this study ‘excludes the Volcker years’ and the ‘burst of the equity bubble’ – consider that before piling in.

However, bear in mind that this could well be what The Fed wants – politics and plunge protectors aside – as the only solution to soaring inflation…

Fed wants recession. It will get it in a few months.

— zerohedge (@zerohedge) March 16, 2022

In fact, for those who still believe ‘the consumer is strong’ and ‘just look at the stock market’, we suggest just look at sentiment surveys – all crashing to multi-decade lows as inflation expectations hit multi-decade highs.

As none other than the former head of the Hew York Fed, Bill Dudley, wrote this morning, The Fed’s application of its framework has left it behind the curve in controlling inflation. This, in turn, has made a hard landing virtually inevitable.

Tyler Durden

Tue, 03/29/2022 – 13:34

via ZeroHedge News https://ift.tt/BaxOZ8R Tyler Durden