Trouble Ahead: Fed Policy On A Preset Course to Fail

By Joe Carson, former chief economist at Alliance Bernstein

Policymakers are trying to achieve a benign economic outcome, a soft landing similar to 1995. But unfortunately, history shows that soft landings are rare. Since 1960, there have been three soft landings but nine recessions. Soft landings happen when the Fed acts early and often, and recessions occur when the Fed acts late. Unfortunately, the Fed is late, very late today.

One of the biggest challenges for the Federal Reserve is that it confronts the most significant inflation cycle in decades without any trusted policy gauges. Decades ago, policymakers abandoned the monetary targets, arguing that they no longer provided a consistent and reliable nominal spending and inflation signal. And a few years ago, Fed Chair Powell “retired” the Phillips Curve from a policy gauge, arguing that there was no consistent pattern between labor market slack and up and down movements in inflation for the past two decades.

The Fed’s playbook from the 1994 episode should have helped, but policymakers did not follow it. The 1994 transcripts of the Federal Open Market Committee (FOMC) meetings reveal that Fed Chair Alan Greenspan argued, “we are facing a test over whether inflation is a Phillips Curve phenomenon or a monetary phenomenon.” He said if it’s a Phillips Curve phenomenon, we are on the edge of significant inflation as there was no slack in the industrial markets. However, if inflation is a monetary phenomenon, then the inflation pressures should be a “blip” as “subnormal growth in money and credit” has to mean something.

Even though Greenspan debated with his colleagues, he concluded that “we have to presume the pressures are there.” As a result, he felt that the FOMC needed to take more preemptive actions of raising official rates since it was too risky to be wrong. Whether by design or luck, the economy achieved a soft-landing in 1995, and the much-dreaded consumer inflation cycle never took off.

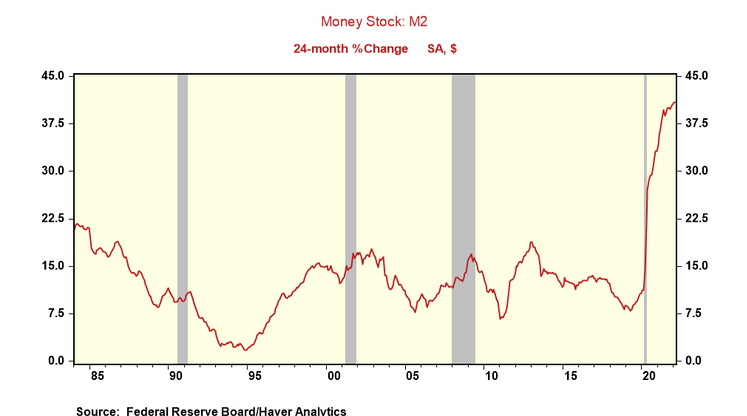

Policymakers need not have the same debate nowadays as Phillips Curve, and monetary inflation features are present. To be sure, broad money growth has topped 40% in the past two years, the fastest ever. And, wage increases have become significant and persistent (average wages up 6.7% in the past year). And wage pressure will continue to be an issue with a relatively low jobless rate of 3.8%.

The inflation cycle of today is also more advanced, markedly different in scale and scope compared with 1994. For example, in 1994, producer prices for crude goods, excluding food and energy, rose 15%, but in 2021, the same prices rose 29%. Greenspan’s primary concern in 1994 was the spike in crude prices would work its way up to the pipeline, lifting prices everywhere and in everything. In 1994, that didn’t happen. But in 2022, it has.

Producer prices for intermediate materials, excluding food and energy, rose 23% last year. That was nearly 5X times the increase of 1994. Consumer prices have increased 7.9% in the past year, and the peak is not yet. Yet, in 1994, consumer prices showed no acceleration, ending the year at 2.7%, the same rate at the outset.

Policymakers’ 2022 playbook is a “wing and prayer” strategy, hoping for a good outcome but unwilling to apply sufficient monetary restraint to get a good result. Current projections show a peak fed funds rate of 2.8% at the end of 2023, or less than half today’s inflation rate. Soft landings of 1994 and 1984 came about with policy rates 300 to 600 basis points above inflation.

If lifting nominal interest rates well above inflation helped engineer a soft landing in the past, what are the odds of achieving a soft landing by doing the opposite? Close to zero, in my view. Also, policymakers expect the jobless rate to be even lower at the end of 2023 (3.5%) than today. So how does the Fed expect to break the wage-price cycle (Phillips Curve) without creating slack in the labor markets?

Fed Chair Jerome Powell has often said monetary policy is not on a preset course. Yet, it’s on a preset path to fail this time as long as it let’s inflation linger and keeps policy rates too low. Investors forewarned.

Tyler Durden

Tue, 03/29/2022 – 15:39

via ZeroHedge News https://ift.tt/bzY1vwd Tyler Durden