It’s Official: Deutsche Is The First Bank To Forecast A US Recession In Late 2023

Up until now, with the exception of various bearish splinter voices within Wall Street banks – such as those of Michael Hartnett or Albert Edwards who pitched recessionary scenarios explicitly different from the banks’ bullish “base cases”, not one bank dared to make the coming recession its official prediction narrative. That changed this morning when Deutsche Bank’s chief economists and heads of research, David Folkerts-Landau and Peter Hooper, became the first to make a recession in the US and a growth recession in the euro area within the next two years, their official forecast.

The only valid independent measure of impending recession is the Fed denying it https://t.co/ukHazUSrtW

— zerohedge (@zerohedge) March 28, 2022

The “shocks” behind DB’s dramatic reassessment – the same ones we have been pounding the table on for the past 2 months: the war in Ukraine and the build-up of momentum in elevated US and European inflation. Some more details from the DB duo:

- The war, which has transitioned into a stalemate that is unlikely to be resolved any time soon, has disrupted activity on a number of fronts. These include upheavals in markets for energy, food grains, and key materials, that have in turn further disrupted global supply chains. That said, the economists assume that the critical flow of gas from Russia to Europe will not be cut off, keeping the crisis from substantially deepening costs to the European and global economies, but that remains a downside risk.

- Inflation in the US and Europe is now pushing 8%, well in excess of what was expected as recently as December. More troubling, especially in the US, are signs that the underlying drivers of inflation have broadened, emanating from very tight labor market conditions and spreading from goods to services. Inflation psychology has shifted significantly, and while longer-term inflation expectations have not yet become unanchored, they are increasingly at risk of doing so.

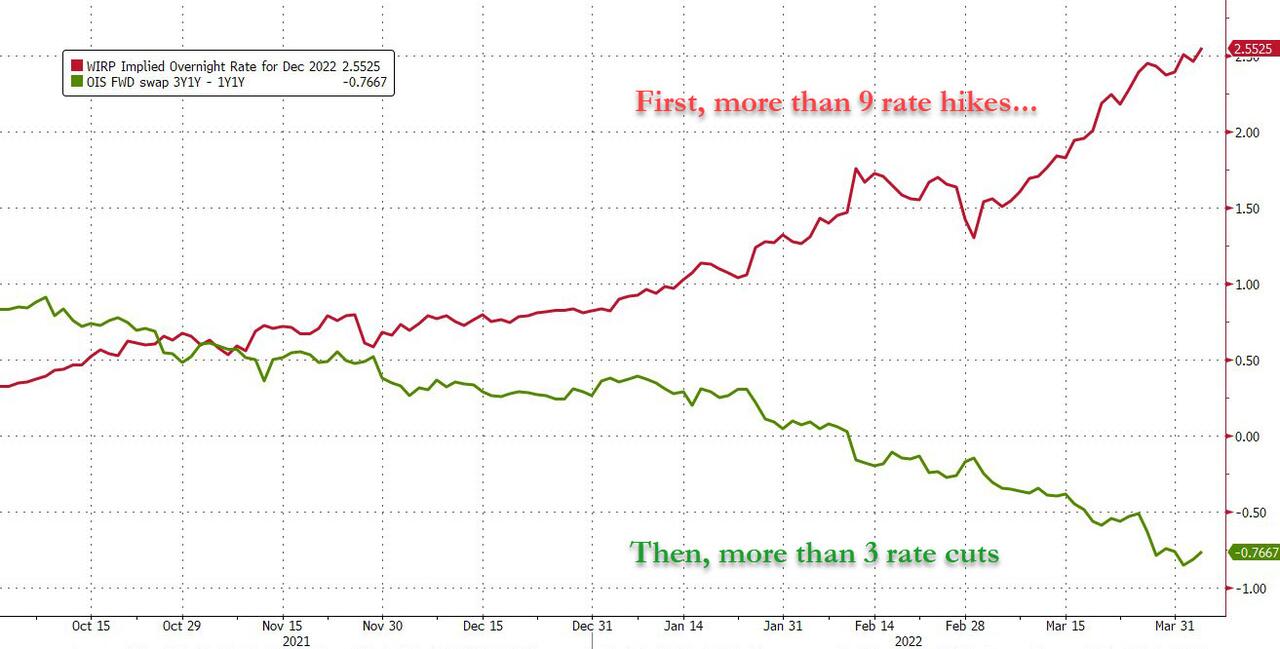

Meanwhile, as confirmed by today’s uberhawkish comments from Lael Brainard, the Fed has found itself greatly behind the curve, and has given clear signals that it is shifting to a more aggressive tightening mode, so DB now expects the Fed funds rate to peak above 3-1/2% next summer, with balance sheet rundown adding at least another 75bp-equivalent in rate hikes. With EA inflation likely to be sustained at 2% or more, the German bank also sees the ECB raising rates 250 bps between this September and next December.

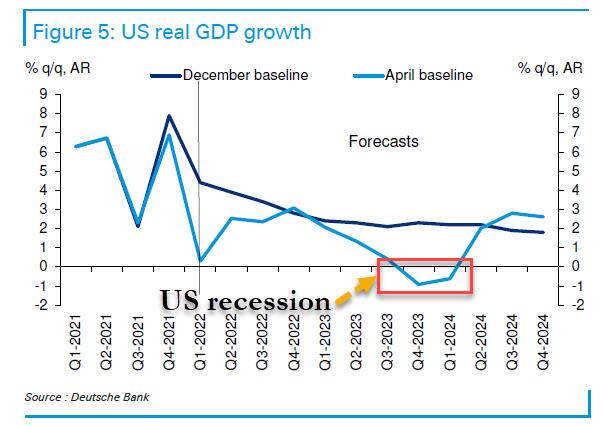

Here, DB echoes what we have repeatedly said in the past 6 months, and warns that the Fed’s tightening is expected to yield negative growth in the US for two quarters during the fall-winter of 2023-24 and to reduce EA growth to modestly above zero that winter. In other words, the Fed hopes to start a “soft landing” recession…

Fed wants recession. It will get it in a few months.

— zerohedge (@zerohedge) March 16, 2022

… but since it will fail miserably, all it is doing is bringing forward the next massive monetary stimulus (read QE and ETF purchases).

What Brainard said: the Fed will accelerate the onset of the next recession so its can accelerate the ETF-buying QE that follows

— zerohedge (@zerohedge) April 5, 2022

And sure enough, DB agrees with that too, with the bank writing that “growth is seen recovering thereafter as inflation recedes and the Fed reverses some of its rate hikes”, translation rate cuts begin as soon as 2023.

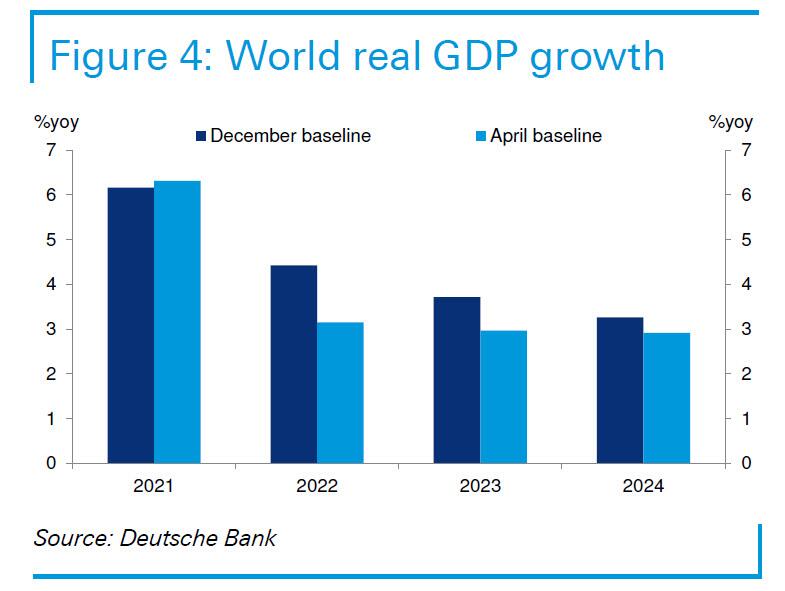

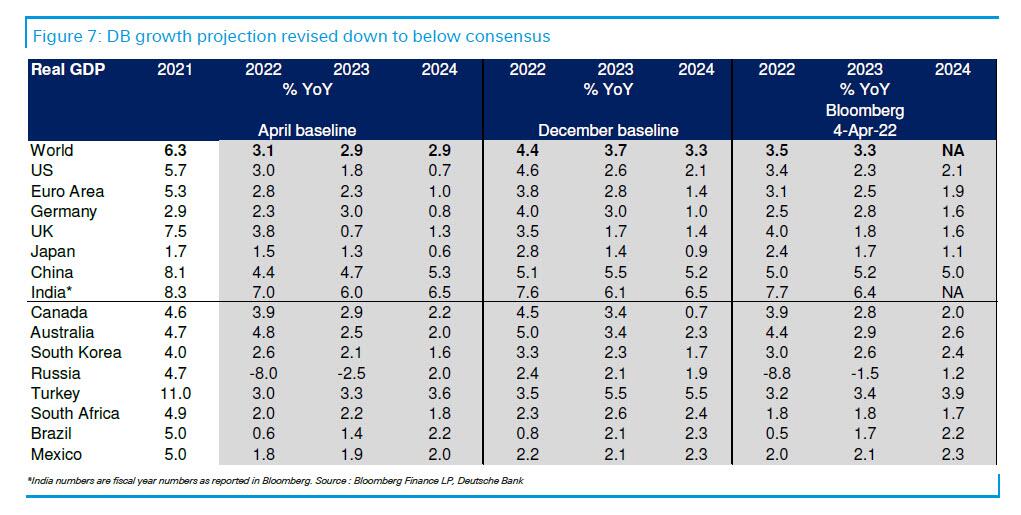

In more specific terms, DB writes that the war in Ukraine and the more aggressive monetary policy tightening “have caused us to mark down our forecast for global growth—by more than 1pp this year and 3/4pp next year”…

… With the EA and especially Germany hit hardest this year by the war and surges in energy and other prices that have depressed household and corporate real incomes. China’s growth has been marked down significantly as well, this year and next, primarily because of the disruptive effects of official measures including lockdowns to deal with the spread of the highly infectious Omicron BA.2 variant of Covid-19.

The US economy is expected to take an especially hard hit from the extra Fed tightening by late next year and early 2024, and as a result Deutsche sees two negative quarters of growth and a more than 1.5% pt rise in the US unemployment rate, developments that clearly qualify as a recession.

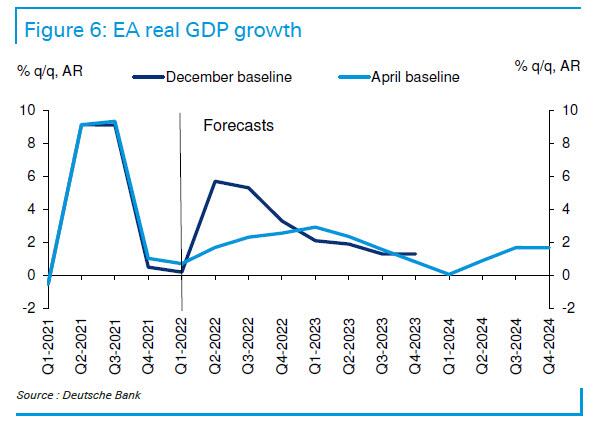

This US slowdown – and recession – spills over to some extent to much of the rest of the world, with EA growth dipping briefly to about zero in early 2024, a number which will only be pulled lower in coming weeks as the European recession gets “worse”.

The good news is that by late 2024, US growth picks up after the Fed eases rates and/or resumes QE.

There is more in the full 62-page report available to pro subs in the usual place.

Tyler Durden

Tue, 04/05/2022 – 12:16

via ZeroHedge News https://ift.tt/7AHuzPa Tyler Durden