Markets Puke After Nomura Warns Of Multiple 75bps Rate-Hikes This Year

“Hard landing” risks are on the rise and equity markets are starting to catch down to the reality of outlier Fed tightening that is priced into short-term interest-rates (STIRs).

Nomura’s North America Economics team raised a red flag for that tightening as they warn that Fedspeak this week is clearly laying the groundwork for 75bp hikes after the May FOMC meeting (note the blackout period starts 23 April)

We expect the first 75bp rate hikes since 1994 at the June and July meetings following a 50bp rate hike in May

We believe momentum for a 75bp rate hike at some point later this year has increased; we now expect a 75bp hike at both the June and July FOMC meetings, following a widely expected 50bp hike in the May meeting.

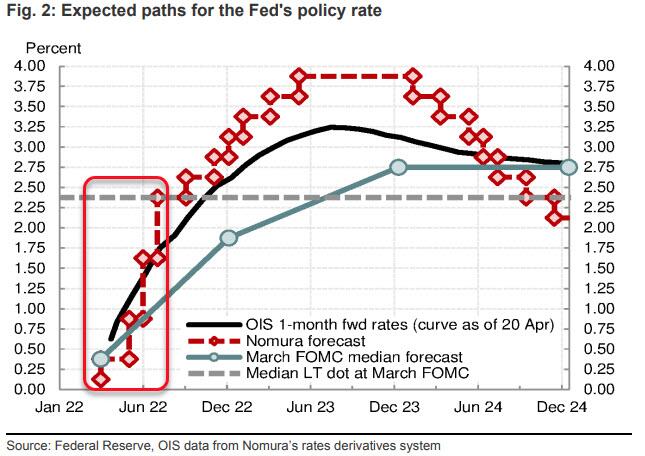

FOMC participants appeared to open the door to such action this week. Over the near term, the Fed remains squarely focused on bringing rates to a neutral setting. Even dovish participants like Evans and Daly have recently suggested support for bringing rates to around 2.25-2.50%, which they consider to be neutral.

Hikes of 50bp in May and 75bp in both June and July would bring rates to the FOMC’s perceived neutral setting very quickly (2.25-2.50%). Note the median long-term dot is currently 2.375%, with one participant at 2.00%, six at 2.25%, one at 2.375%, five at 2.50% and two at 3.00%. We believe most participants at the 2.25% level would be comfortable with 2.25-2.50% as neutral.

For some time, our view has been that if the Fed could hike 200bp at one meeting without significantly affecting market functioning, they would. So far, markets have been reluctant to price 75bp hikes, but stronger pricing for such a move would likely ease the path for the FOMC and participants could likely forge a consensus on such action quickly.

We believe comments from FOMC participants this week were an intentional effort to “trial balloon” a 75bp hike and then closely monitor the market’s response.

Moreover, Chair Powell acknowledged today he supports frontloading rate hikes. Markets have responded, but not in a way the Fed would consider “disorderly.” From the Fed’s perspective, hiking multiple times by 75bp would bring them to neutral more quickly

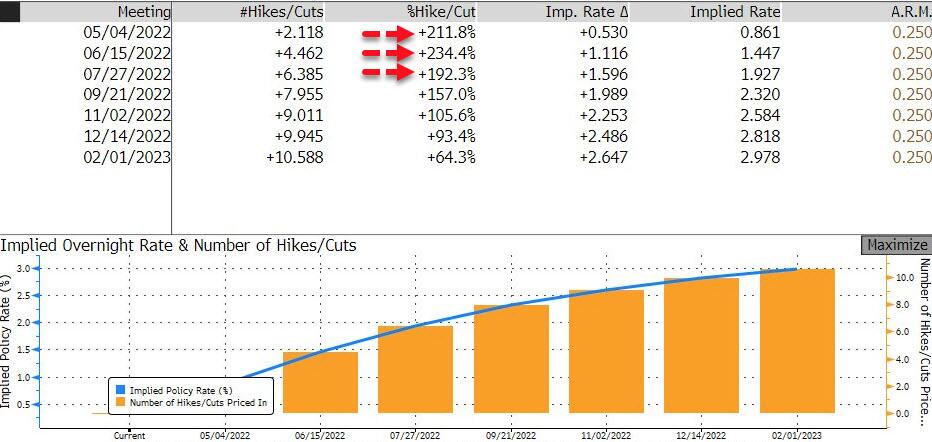

In fact, STIRs have quickly started to price that in with a 35% chance of a 75bps hike now in June (with 50bps more than fully priced for May)…

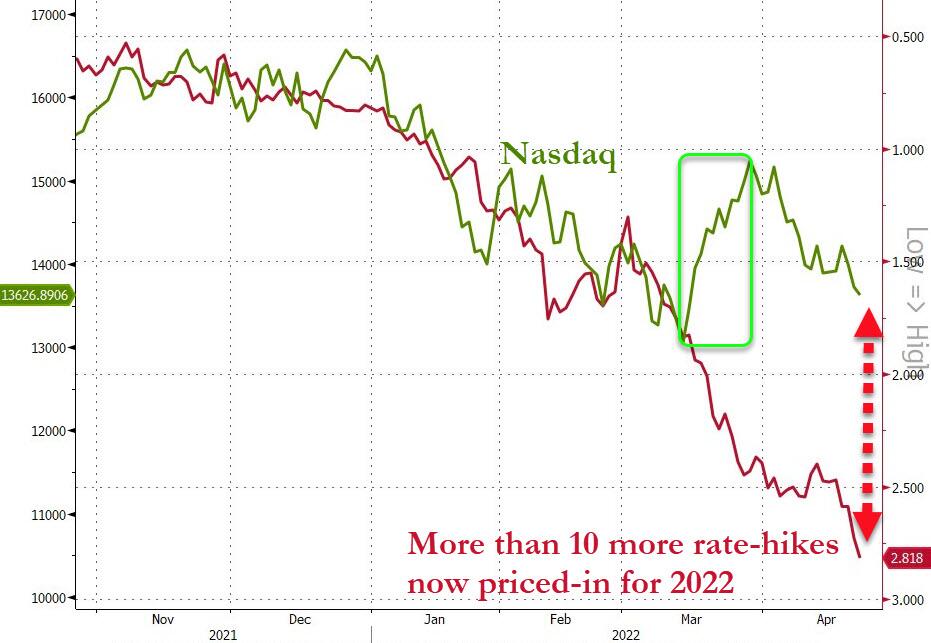

And as Nomura’s Charlie McElligott notes, the Equities-set has learned in painful fashion over the past six months that shock Rates re-pricings off the back of “hawkish escalation” are a gut-punch to markets and sentiment (as they risk “hard landing” into an economic cycle-turn), especially the “lazy long Duration” crowd which means up so much legacy positioning and general index-weighting…but yesterday, even seeing the recent “cyclical” leaders get hit too into enhanced “contraction / recession” de-risking.

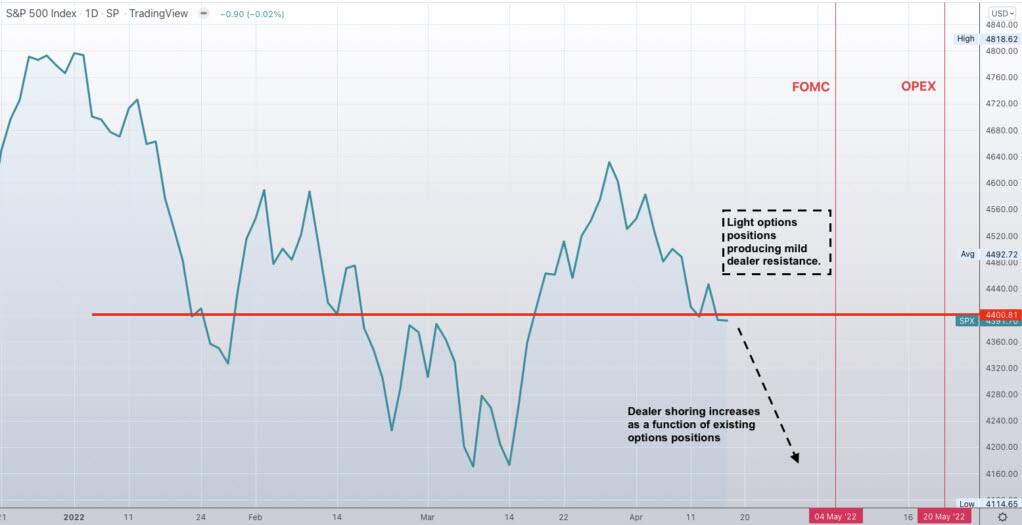

The map ahead continues to look like this

As SpotGamma explains, 4400SPX is the last “neutral” strike on the board, meaning it is the last strike with material call gamma. Below 4400 its primarily put gamma, which leaves the market exposed to dealer short-hedging.

Tyler Durden

Fri, 04/22/2022 – 11:23

via ZeroHedge News https://ift.tt/kQsum75 Tyler Durden