Oil Markets Could Face A Doomsday Scenario This Week

Authored by Cyril Widdershoven via Oilprice.com,

-

Expect lots of oil price volatility in the coming months as markets finally discover just how much spare capacity OPEC members really have.

-

Oil production outages in Libya and the continued impact of Russia’s invasion of Ukraine are going to push oil prices higher if new supply isn’t found.

-

While some analysts are predicting oil demand destruction in the near future, there is little evidence to back up those claims.

Global oil markets are going to be very volatile in the coming months if news emerging from OPEC’s main producers about production capacity constraints turns out to be true.

OPEC will be meeting again in the coming days to discuss its export agreements, while today the oil group is presenting its Annual Statistical Bulletin (ASB) 2022. While the media is likely to be focused on rumors in the next 24 hours of a possible change in the export strategy of OPEC+, the real focus should be on whether or not the oil cartel is even capable of substantially increasing its production.

For years, OPEC producers have been the main swing producers in oil markets. With a presumed spare capacity of more than 3-4 million bpd, Saudi Arabia and the UAE have always been seen as a point of last resort in case of a major crisis in oil and gas markets. During the former global oil glut, it seemed nothing could threaten the oil market, even when major conflicts emerged in Libya, Iraq, or elsewhere. The re-opening of the global economy after COVID-19, however, has brought fear back into the market that leading oil producers, including the USA and Russia, are unable to supply adequate volumes to the market. OPEC kingpins Saudi Arabia and the UAE are now being looked upon to increase production to historically high levels and bring oil prices down. Russia’s war against Ukraine, removing a possible 4.4 million bpd of crude and products in the coming months, has thrown this spare capacity problem into sharp relief.

This week, a possible doomsday scenario could emerge in oil markets, based not only on OPEC+ export strategies but also due to increased internal turmoil in Libya, Iraq, and Ecuador. Possible other political and economic turmoil is also brewing in other producers, while US shale is still not showing any signs of a substantial production increase in the coming months.

Global oil markets have long believed that OPEC has enough spare production capacity to stabilize markets, with Saudi Arabia and the UAE just needing to open their taps. There is ,however, no real evidence to suggest that OPEC has increased production capacity in place in the short term. A research note by Commonwealth Bank commodities analyst Tobin Gorey already noted that OPEC’s two leaders are producing at near-term capacity limits. At the same time, UAE Minister of Energy Suhail Al Mazrouei put even more pressure on oil prices as he stated that the UAE is producing near-maximum capacity based on its quota of 3.168 million barrels per day (bpd) under the agreement with OPEC and its allies. That comment could still indicate that there is some spare capacity left in Abu Dhabi, but the remarks were made after French President Emmanuel Macron had stated to US president Biden during the G7 meeting that not only is the UAE producing at maximum production capacity, but also that Saudi Arabia only has another 150,000 bpd of spare capacity available.

Macron stated that UAE’s president Mohammed bin Zayed (MBZ) told him that the UAE is at maximum production capacity while claiming that Saudi Arabia can increase production by another 150,000 bpd. Macron also claimed that Saudi Arabia won’t have a huge additional capacity within the coming six months. The official figures for both OPEC producers counter this narrative, however. Saudi Arabia is producing at 10.5 million bpd, with official capacity between 12-12.5 million bpd. The UAE is producing around 3 million bpd, claiming to have a capacity of 3.4 million bpd. The two countries’ spare production is still officially slated to be around 3.9 million bpd combined. Most analysts, however, have been questioning these figures for years.

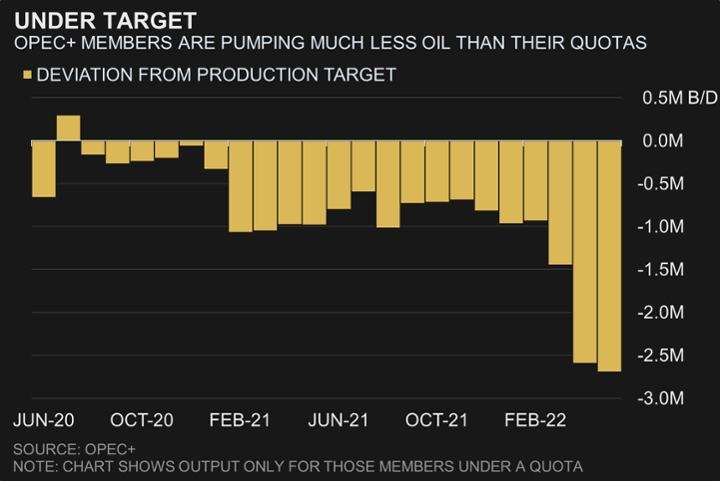

Looking at OPEC+’s own production targets, the group has not been producing at agreed levels for months. At the Middle East and North Africa-Europe Future Energy Dialogue in Jordan, UAE’s Al Mazrouei said that OPEC+ was running 2.6 million barrels a day short of its production target. That means a potential shortage in the market, which could increase even further if internal turmoil causes further production decreases. For July-August, OPEC+ agreed to increase output by another 648,000 bpd, which would mean that the total output cut during COVID-19 pandemic of 5.8 million bpd has been restored. Whether or not OPEC+ is able to reach that level in the coming weeks remains very uncertain.

Pressure will build in the coming days, as Al Mazrouei’s remarks seem to rebuke claims of a spare capacity shortage, but as always “where there is smoke, there is a fire”. A possible spare production capacity shortage, or non-availability at all, combined with an expected force majeure of Libya’s NOC in the Gulf of Sirte, and a suspension of Ecuador’s oil output (520,000 bpd) in the coming days due to anti-government protests, are likely to lead to an oil price spike.

There is still some optimism in markets about a real demand-supply crunch, as high inflation levels and a possible global economic slowdown could lead to lower demand. Until now, however, that optimism has not materialized at all, demand is still increasing, even though gasoline and diesel prices are breaking historical price levels. The re-opening of the Chinese economy, a natural gas shortage globally, and higher temperatures in the coming weeks, combined with the normal peak in demand due to the US and EU driving season, all look set to push oil prices higher.

OPEC’s future is at stake if spare production capacity really has run out. For years, analysts (including myself) have been warning about a lack of investment in upstream worldwide. That has already led to lower production capacity of independent oil companies, such as most IOCs, and for national oil companies, the situation appears to be similar. Even though Saudi Aramco, ADNOC, and some others, have been keeping their upstream (and downstream) investments level during the last decade (even during COVID), other main OPEC producers have seen dwindling investment budgets or even full-scale crises. Most OPEC producers could increase their overall production still, but only for a limited period of time. Where most spare production capacity is short-term based, partly to avoid damaging reserves in the long run, the current oil crisis is a much more prolonged long-term issue. Western sanctions on Russia, combined with existing sanctions on Venezuela and Iran, will hurt markets for years to come.

There is no quick-fix solution to the current oil market crisis, even the lifting of sanctions on Venezuela or Iran will not result in substantial volume increases. At the same time, increased Western political interference in the already struggling market will hit volumes too. The growing call in the USA, UK, and EU, to put a windfall tax on oil and gas companies will not only constrain further investments in upstream but will also lead to higher prices at the pump. Consumers are not going to feel any positive price effects and can expect steadily increasing energy bills in the coming months.

No statements made by OPEC in the coming two days are going to be able to remove the worries in the market. OPEC’s future depends fully on its power to stabilize markets. At present, there appear to be no options available to the cartel. Without new oil production hitting markets soon, OPEC leaders MBZ and Crown Prince Mohammed bin Salman need to try to maintain the illusion of spare capacity. If spare production capacity is revealed to be under 1.5-2 million bpd, the future of both OPEC and oil markets would be bleak.

Tyler Durden

Wed, 06/29/2022 – 14:05

via ZeroHedge News https://ift.tt/xMl4j1H Tyler Durden