The Squeeze Is Over: Goldman Prime Sees A Flood Of New Hedge Fund Shorts

The bear market rally from the mid-June lows was triggered by three key drivers: gradual bullish reversal by the systematic crowd, accelerating buybacks, and a sudden retail frenzy back into the market. But the real catalyst for the meltup was the “apocalyptic” bearish positioning by institutional and hedge fund investors, who were forced to FOMO chase the “most hated rally” higher, accelerating the meltup as they did. This unprecedented bearish bias prompted none other than Michael Hartnett to correctly turn bullish in mid-July citing “Record Pessimism”, “Full Investor Capitulation.”

But far more remarkable was Hartnett’s bearish reversal earlier this week, when the BofA chief investment officer correctly timed the spoos peak to within half a tick, urging clients (and ZH readers) to short at 4,328 (which was also the 200DMA). This is what happened then.

Well, there’s a reason why we call Hartnett (unlike so many of his broken record competitors) Wall Steet’s most accurate analyst. But while we hope that readers saved some cash (or made a profit) by timing the bear-market top (for now), it appears that another batch of investors also decided to start shorting… again.

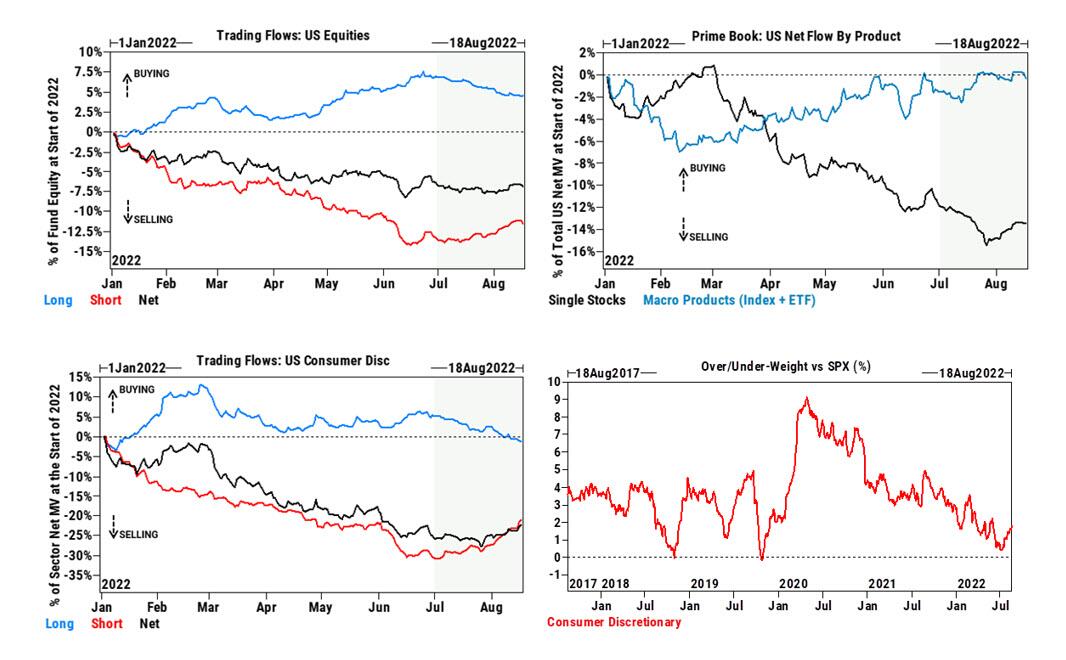

According to Goldman Prime, after 4 weeks of relentless short covering unwinds, hedge funds are starting to play more bearish offense, layering new shorts as the GS prime book saw the largest notional net selling in three weeks (1-Year Z score -0.7), driven by short sales outpacing long buys 3 to 1.

Here are some more details from the note available to pro subscribers:

- Overall gross trading activity saw the largest 1-day increase since 6/16 (when SPX fell to YTD lows). While one day does not make a trend, yesterday’s activity suggests hedge funds could be starting to play a bit more offense following four straight weeks of risk unwinds.

- Macro Products (Index and ETF combined) saw the largest notional net selling since mid-July driven entirely by short sales. US-listed ETF shorts rose +2.0%, the largest 1-day increase in more than two months: Large Cap Equity, Technology, and Small Cap Equity ETFs were among the most shorted.

- Single Stocks saw little net activity overall, but flows were risk-on with long buys offset by roughly the same notional amount of short sales. Consumer Discretionary (short covers), Financials (long buys), and Health Care (long buys) were the most notionally net bought sectors; Comm Svcs (long sales), Info Tech (short sales), and Industrials (short sales) were the most notionally net sold.

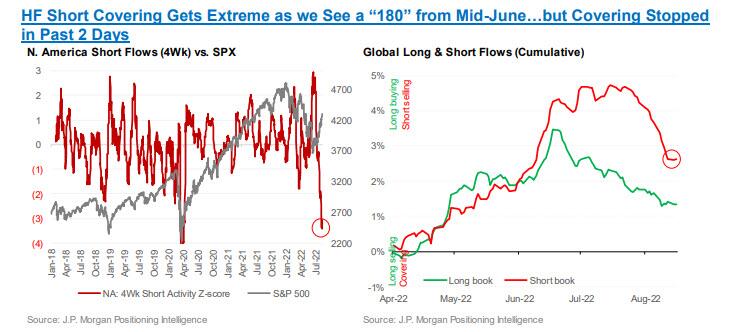

JPMorgan agree, and in a note from the bank’s prime brokerage, writes that following a massive burst of short covering from mid-June, it has suddenly stopped in the past 2 days… oddly around the time Hartnett said to resume shorting.

And now that a bunch of potentially bearish events are on deck, we expect the shorting to only accelerate over the next two weeks, at least until through the Jackson Hole symposium next weekend, and the next batch of data on CPI and employment in early September.

“Hedge funds may view the June-to-August rally as too far, too fast, and now are licking their chops for another round of downside,” said Mike Bailey, director of research at wealth management firm FBB Capital Partners. “Tactically, markets look a bit feeble at the moment, as investors price in good inflation and Fed news.”

Ironically, so hated was this bear market rally, that the new round of shorting takes place even as the previous bearish bets have not been fully unwound, and according to Morgan Stanley there are still a lot of bearish positions outstanding: the bank’s data show that in the cash market, while $50 billion has been covered since June, the net amount of added shorts remains elevated, sitting at $165 billion this year. Short interest among single stocks stands in the 84th percentile of a one-year range.

“The short base in US equities is still not cleaned up though,” Morgan Stanley wrote in a note. “With short leverage still high, there is more potential for hedge fund short covering.”

“Nobody trusts the rally,” said Benjamin Dunn, president of Alpha Theory Advisors. “We could be in for a period of weakness, but by the same token, a lot of people who want to sell have already sold,” he added. “That’s been the problem the last several months in this market. It’s nothing but positioning, almost nothing fundamental.”

Still, as Bloomberg notes, shorts unwinding amplified the market upside during the summer lull, but all the caution suggests that the downside risk is likely limited, and as we noted last night…

And they’re back: “HFs pressing shorts again… US equities saw the largest 1-day increase in gross trading flow since 6/16 driven by short sales” – GS

here we go again

— zerohedge (@zerohedge) August 19, 2022

… it sets the stage for the next short covering squeeze the moment the market views Powell’s next comments as “pivotish.”

Tyler Durden

Fri, 08/19/2022 – 14:19

via ZeroHedge News https://ift.tt/Dlnir1Q Tyler Durden