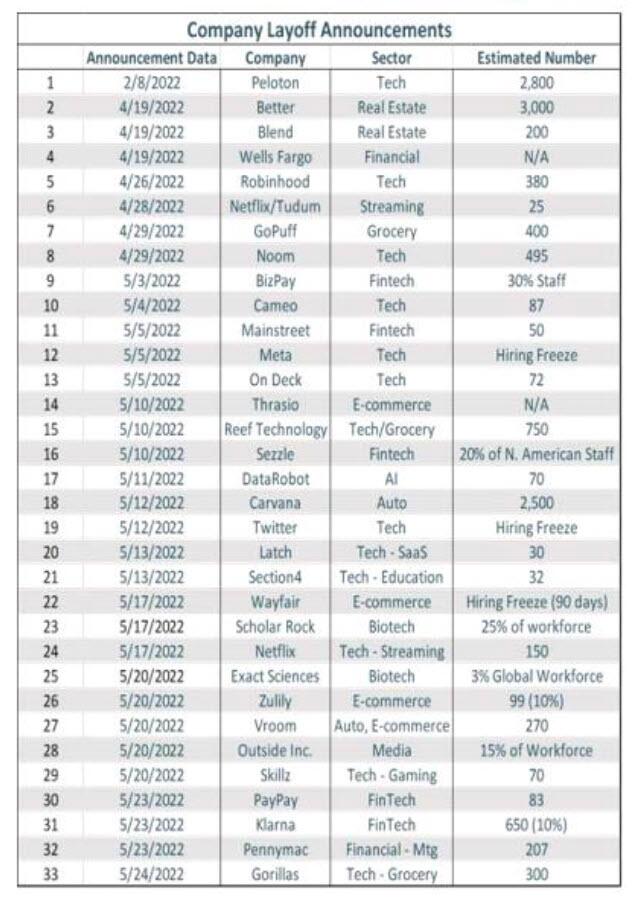

Just How Cooked Is The Official Jobs Data: PwC Finds More Than Half Of US Companies Are Laying Off Workers

Nearly three months ago, when tabulating real-time mass layoffs data…

… Piper Sandler chief economist Nancy Lazar concluded that “post-covid rightsizing means that lots more layoffs are coming” and added that “many companies overhired and overpaid during the Covid crisis.”

Since then, it’s only gotten worse for those who track corporate layoff announcements, such as the following:

- #1 Ultratec Inc. says that it will be laying off more than 600 workers.

- #2 Electric truck maker Rivian will be laying off approximately 840 workers.

- #3 7-Eleven has announced that it will be eliminating 880 corporate jobs.

- #4 Shopify is laying off about 1,000 people.

- #5 Vimeo says that it will be eliminating 6 percent of its current workforce.

- #6 Redfin will be reducing the size of its workforce by 8 percent.

- #7 Compass will be reducing the size of its workforce by 10 percent.

- #8 RE/MAX will be reducing the size of its workforce by 17 percent.

- #9 Robinhood will be reducing the size of its workforce by 23 percent.

- #10 It is being reported that Ford “is preparing to cut as many as 8,000 jobs in the coming weeks”.

- #11 Geico has closed every single one of their offices in the state of California, and that will result in vast numbers of workers losing their jobs.

- #12 Walmart is eliminating about 200 corporate jobs as it contends with rising costs, bloated inventories and weakening demand for general merchandise.

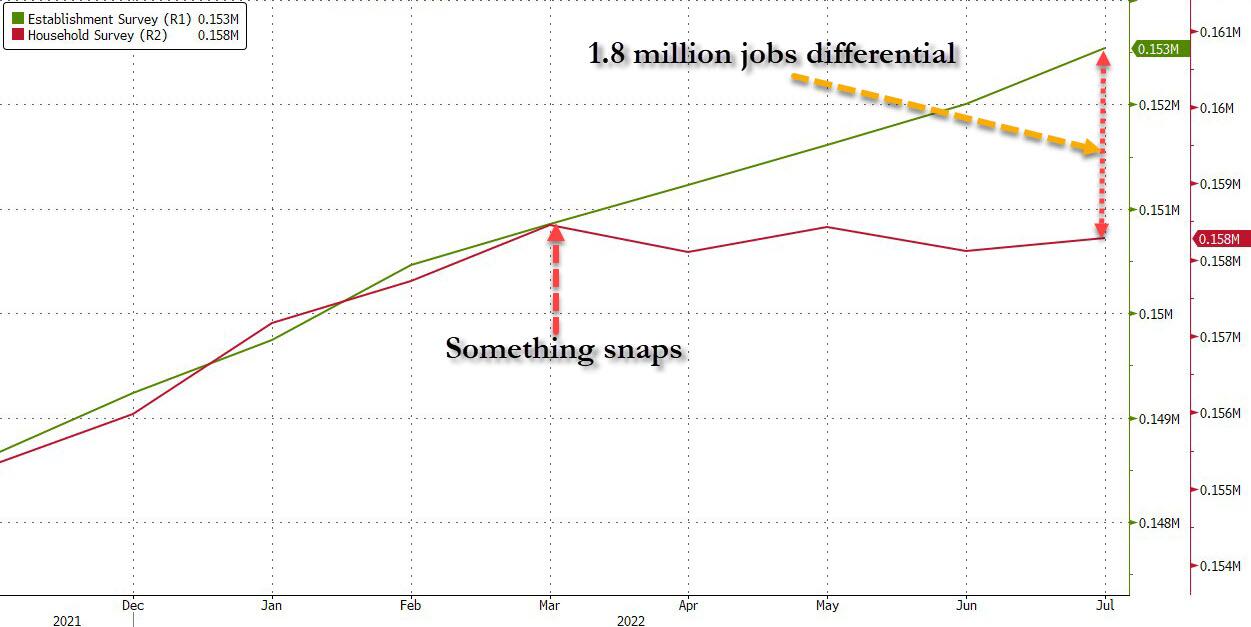

… and yet while initial jobless claims have indeed moved notably higher in recent months, the Bureau of Labor Statistics stubbornly refuses to report the true state of the US labor market, where despite continued softness in the Household Survey where no new jobs have been added since March, the far more politicized Establishment survey – which, after all, is what the Biden administration points toward as the only silver cloud in an otherwise recessionary and hyperinflating economy – has continued to show remarkable resilience and growth in recent months. So much so, that the differential between the Household and Establishment surveys has grown to a record 1.8 million jobs since March.

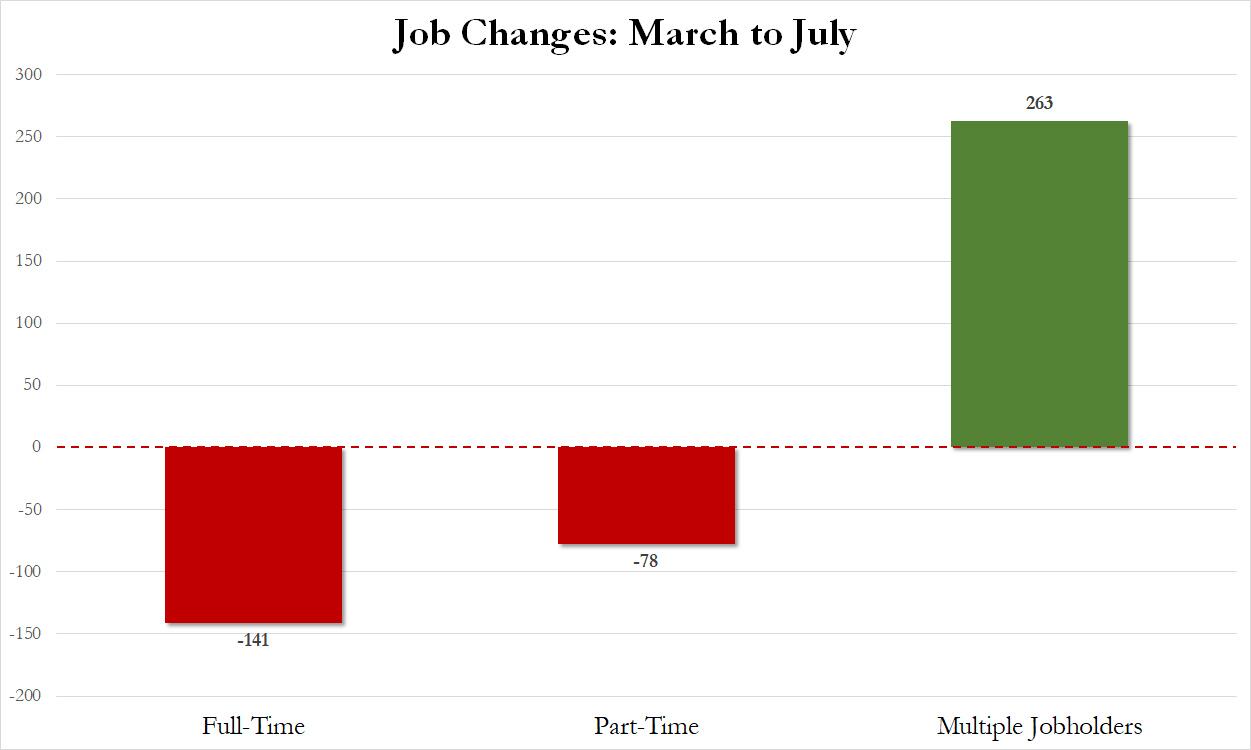

And while one possible explanation for this bizarre divergence is the record surge in multiple jobholders who now hold both a primary and secondary full-time job…

… even as full and part-time job gains have slumped…

… the truth is that there is no comprehensive explanation for the variation in data. Which, needless to say, is problematic because the “solid” jobs market is one of the very few things that is preventing the Fed from substantially easing back on its hawkish policies (now that peak inflation has clearly been reached… if only for the time being), and the Fed’s sharply higher rates are already wreaking havoc on the housing market not to mention various stock sectors that have also gotten walloped.

But what if the BLS data is not merely “off” due to benign factors such as “residual seasonality” or a post-covid hangover? What if it is intentionally manipulated to make Biden’s economy appear stronger than it is for midterm election purposes even if it means distortions across the entire market?

We bring up all these rhetorical questions because a new survey released by consultancy PwC confirms our previous observations about rampant mass layoffs in the US labor market, and suggests that the true state of the job market is far, far uglier than the alleged 528K job gain reported by the BLS in July would suggest.

In the PwC survey released last Thursday, which last month polled more than 700 US executives and board members across a range of industries, half of respondents said they’re reducing headcount or plan to, and 52% have implemented hiring freezes. At the same time, more than four in ten are rescinding job offers, and a similar amount are reducing or eliminating the sign-on bonuses that had become common to attract talent in a tight job market.

At the same time, though, about two-thirds of firms are boosting pay – for those who keep their jobs – or expanding “mental-health benefits”, because we now live in a liberal dystopia where a growing number of workers are batshit insane.

The findings, as even Bloomberg concludes, illustrate the contradictory nature of today’s labor market, where skilled workers can still largely name their terms amid talent shortages (in high demand sectors like line cooks and bartenders), even as companies look to let people go elsewhere, particularly in hard-hit industries like technology and real estate.

“Firms are playing offense and defense with their talent strategies,” said Bhushan Sethi, joint global leader of PwC’s people and organization practice, noting that employers have to weigh reputational damage and employee morale when planning layoffs. “People have long memories, and social media plays a much bigger role now.”

Of course, reputational damage won’t matter if a company is facing bankruptcy damage by having far too many workers and not enough cash flow.

One big reason for the ongoing crunch in the job market is the treatment of “work from home” – having become a staple during the Scamdemic courtesy of overpaid charlatans such as Anthony Fauci, corporations are increasingly seeking a return to the “old normal” which however is proving to be quite a challenge. As a result, the PwC survey found “contradictions” in companies’ approaches to remote work. While 70% of those surveyed said they’re expanding permanent remote-work options for roles that allow it, 61% said they’re requiring employees to be in the office or job site more often.

To be sure, some organizations could be doing both of those things at once: Roles that don’t require much in-person collaboration could go remote for good, while other staffers could be required to get back to their desks a few times a week. September is shaping up to be a line in the sand for many companies’ return-to-office plans, even though previous so-called RTO deadlines came and went.

One thing is certain: the coming labor shock will have dire and wide-raning consequences on the broader office market: with fewer employees in offices, organizations don’t need as many far-flung locations. As such, more than one in five respondents told PwC that they plan to decrease their investment in real estate, making it the most common area of cutbacks, and yes, fewer employees.

As for the divergence between the rosy official government labor “data” and the dire jobs picture painted by mass-terminating corporations on the ground, we are confident that the delta between the two data sets will promptly and magically resolve itself… right after the midterm elections.

Tyler Durden

Mon, 08/22/2022 – 22:40

via ZeroHedge News https://ift.tt/RpCA3Pi Tyler Durden