“Forced Selling Of Everything” – UK Pension Funds Are Still Liquidating Assets, Seeking Bailouts

UK pension funds are/have been servicing ever increasing margin calls driven by the extreme moves in real and nominal rates.

As BondVigilantes.com notes, they are on a hunt for liquidity (cash) to service these calls at the same time the liquidity (bid offer spread) of asset markets is extremely fragile. A sub layer to this dynamic is that pension funds are also a significant provider of gilts to the repo market (which they repo out to fund levered investments) and where we are now seeing some strain as these gilts are either withdrawn from repo programmes (to sell, as of yesterday to the BOE) or repo’d out to raise cash to fund said margin calls.

The timing could not be worse with quarter end looming, increasing demand for bank balance sheet from non-bank market participants and an ever increasing war chest of cash from the liquidity ‘Haves’ chasing collateral.

While The Bank of England stepped in to buy gilts on Wednesday, stabilising the market, The Financial Times reports that the pension funds are continuing to sell assets to meet cash calls.

“There’s a lot of pain out there, a lot of forced selling,” said Ariel Bezalel, fund manager at Jupiter.

“People who are getting margin called are having to sell what they can rather than what they would like to.”

He said the BoE’s intervention had helped to bring down yields in longer-dated bonds but other assets remained “under pressure” because pension schemes were “having to liquidate paper”. He added:

“We’re seeing really quality investment grade paper coming up for grabs…names like Heathrow, John Lewis, Gatwick, BT – solid fundamentals – to raise cash.”

Simeon Willis, partner at XPS Pensions Group, said:

“Pension schemes are selling equities and corporate bonds and using those assets to top up their hedges.”

“There could be many hundreds of schemes that have had their hedges reduced or removed. This means their funding positions are now much more vulnerable than they were a week ago.”

To fund the collateral calls, some pension schemes have resorted to asking employers backing their plans for cash. Outsourcing group Serco provided £60mn after a request from pension trustees, according to a person familiar with the matter, a highly unusual move for a well-funded corporate scheme. Sky News first reported the move.

While some schemes continue to rush to raise cash to fund their derivatives positions, others have had the positions terminated by LDI managers, including BlackRock, leaving them exposed to further moves in rates and inflation.

Related to this liquidation, more behind-the scenes details of this week’s chaos in the UK are being exposed with The FT reporting that none other virtue-signaler-extraordinaire BlackRock basically ‘blackmailed’ the UK government into intervention as UK pension funds faced crises.

BlackRock, which sits between the pension schemes and banks on derivatives trades designed to hedge against adverse movement in interest rates and inflation, told its clients that it would no longer demand additional collateral but would instead liquidate holdings to meet margin calls that were soaring due to the extreme volatility in UK asset prices.

In a memo sent on Wednesday morning, BlackRock told clients using its liability-driven investing strategies that it would freeze “funds more at risk of assets being exhausted” and move the assets to cash.

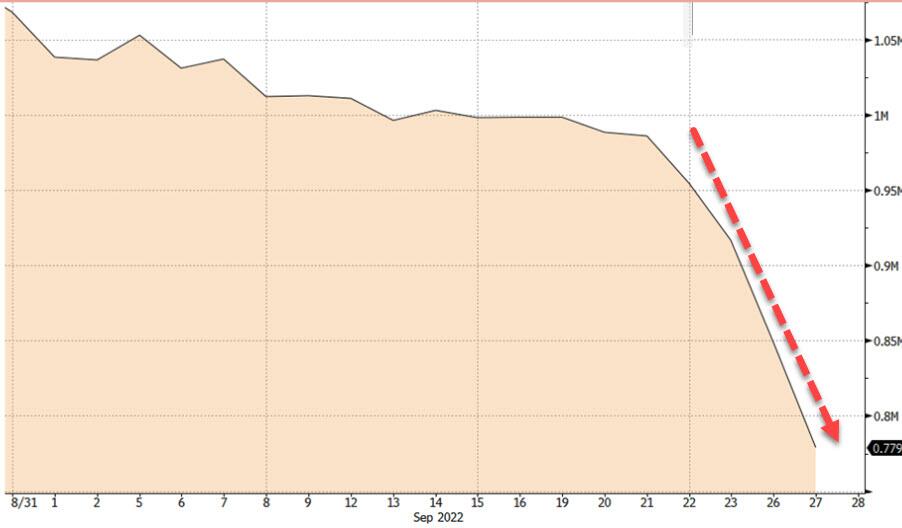

The graph below shows the overall market value of available gilt collateral has fallen sharply over recent days…

BlackRock is “not proceeding with any further recapitalization events until further notice”, said the email to LDI clients, which was seen by the Financial Times and was sent at about 11am, before the Bank of England announced its emergency intervention to stabilise the gilt market.

David Fogarty, a professional trustee with Dalriada, a trustee firm, said:

“If you run out of collateral they were saying, ‘we will close the position’, without going back to ask for more money from the fund. It is protecting their positions against contagion but it is not protecting their pension funds.”

This liquidation would have caused even further vicious spiral plunges in gilt prices and, just as JPMorgan did in 2019 with The Fed and ‘Not QE’ to bailout the repo market, BlackRock exercised its ‘TBTF Put’ and forced The Bank of England’s hand to re-liquify the long-end of the gilts market.

In summary, as BondVigilantes.com notes, there are very clear collateral strains for some sterling market participants and demarcation of the liquidity ‘Have and Have Nots’. The urgent question (with an unclear answer at the moment in my view) is whether this could spill over into a broader liquidity breakdown as the various actors seek to right-size or further shore up their defensive cash stocks during these unprecedented markets. One thing that goes without saying is that cash really is king at the moment.

Tyler Durden

Fri, 09/30/2022 – 12:20

via ZeroHedge News https://ift.tt/fXnVlyE Tyler Durden