Deflation Will Become The Problem When “Something Breaks”

Authored by Lance Roberts via RealInvestmentAdvice.com,

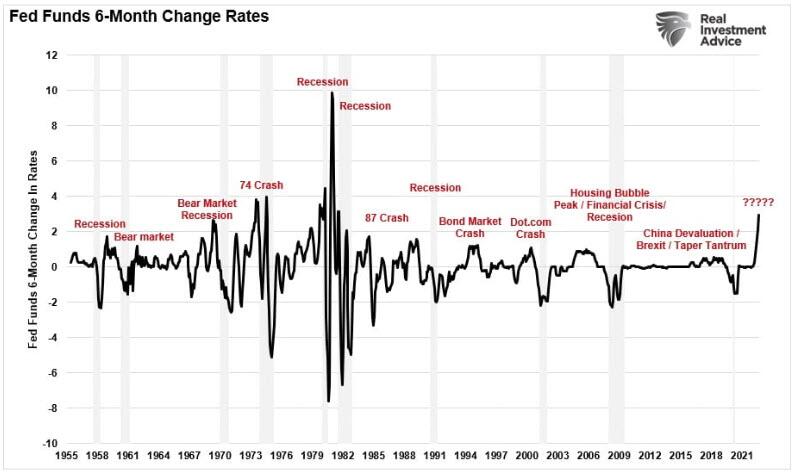

While the Fed continues to hike rates to combat high inflation levels aggressively, history shows that deflation will become a more significant threat when something “breaks” in the financial or credit markets.

As I discussed in a recent MarketWatch article:

“Stable markets can become unstable rapidly when something breaks due to rising rates or volatility. The Bank of England (BOE) is a current example of what happens when things go awry. The BOE on Wednesday was forced to start buying bonds to solve a potential crisis with U.K. pension funds. The pension funds receive margin when yields fall and post additional collateral when yields rise.

As they have recently, the pension funds are hit with margin calls, which have the potential to cause market instability. Due to leverage built up through the financial system, market instability can spread like a virus through global markets. That’s what happened in 2008 with the Lehman crisis.”

In the U.S., given the sheer magnitude of leverage throughout the financial system, we are likely well on the cusp of an even bigger “break” as Fed officials double down on the need to aggressively raise rates to fight what appears to be falling inflation regardless of the systemic consequences.

Those systemic consequences of the Fed tightening monetary policy have repeatedly occurred throughout history. The Latin American Crisis resulted from rising rates impacting dollar-denominated debt. That crisis could have rendered many U.S. banks insolvent. Rising rates triggered the 1987 Market Crash as “portfolio insurance” failed. Following that was a series of adverse events from the 1994 bond market crash, the Mexican peso crisis, Orange Country bankruptcy, Asian Contagion, Russian debt default, Long-Term Capital Management, the Dot.com crash, and the Financial Crisis.

While “high inflation rates” are certainly problematic for the economy, as it creates demand destruction, the more considerable risk remains “financial instability,” which is “deflationary.” As we will discuss, deflation remains a more significant threat for the Fed as it coincides with wealth destruction, further undermining consumer confidence.

Inflation Is Unsustainable

Inflationary pressures can be a “good thing” when they correspond with strong economic growth and productivity. However, when price inflation rises faster than wages and increases debt servicing costs on heavily levered households, the resulting liquidity contraction triggers economic recessions.

Such was a point made by Michael Wilson of Morgan Stanley, stating:

“In our view, such tightness is unsustainable because it will lead to intolerable economic and financial stress.”

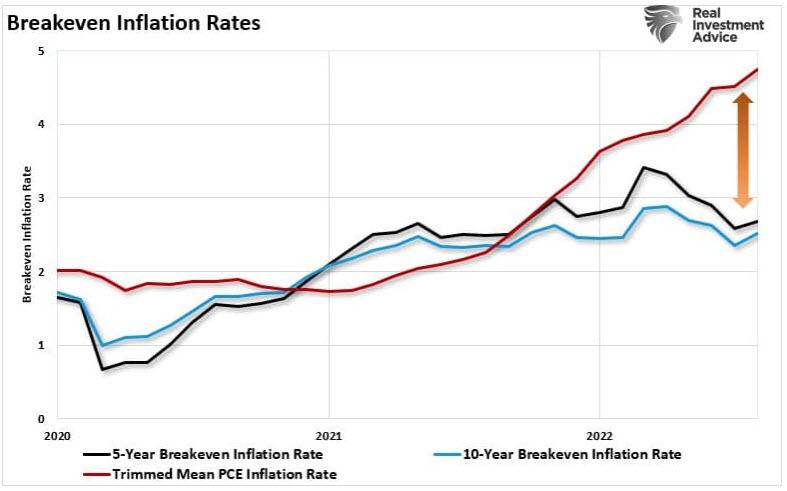

The chart below shows the three major components that comprise inflation:

-

Commodity prices that reflect real economic activity,

-

Wages that allow for increases in spending and support for higher prices; and,

-

The Velocity Of Money shows the demand for money through the economic system.

When we combine these three components into a composite inflation index, we can see that high inflation rates precede recessions and deflationary periods.

There is an inherent problem with the chart above. The inflationary spike was not a function of organic economic activity but rather artificial capital injections into a supply-stricken economy. The surge in demand against limited supply created a surge in prices along with commodities. However, organic economic demand remained weak as the monetary base failed to gain traction.

While many today compare the economic environment to the 1970’s inflationary spike, the impact of demographics and debt are vastly different. As discussed in “Sugar Rush,” as the liquidity injections dissipate, the deflationary pressures are again reasserting themselves.

The problem for the Fed is additional rate hikes will exacerbate the disinflationary processes already at work in the economy. As such, when the eventual recession occurs, demand destruction will likely be more significant than anticipated. A brief review of previous inflationary periods suggests such will be the case.

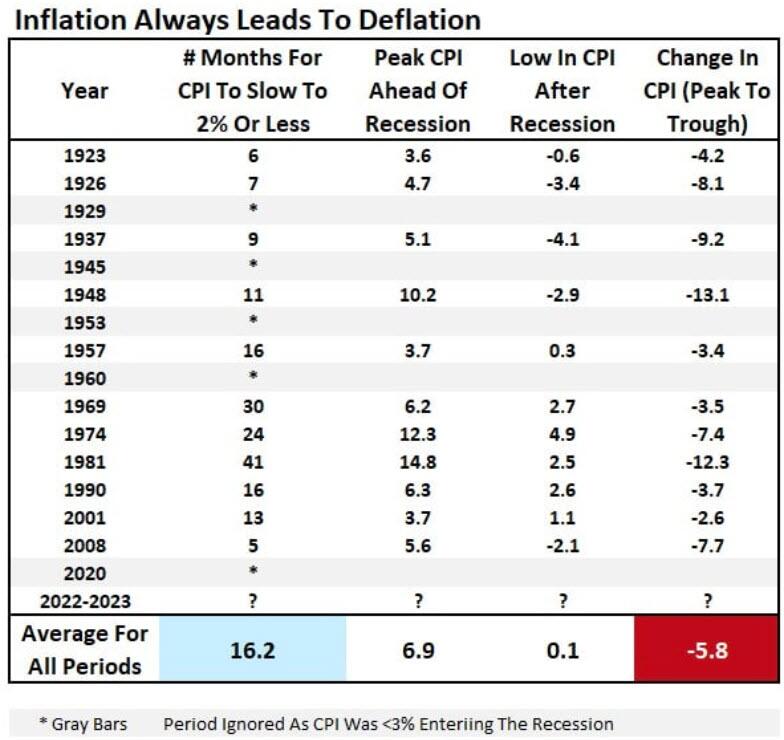

A Brief History Of Deflation From Inflation

While many believe periods of high inflation are “persistent,” history doesn’t support such claims. As Alfonso Peccatiello recently pointed out, high inflation periods reverted to low levels over 16 months.

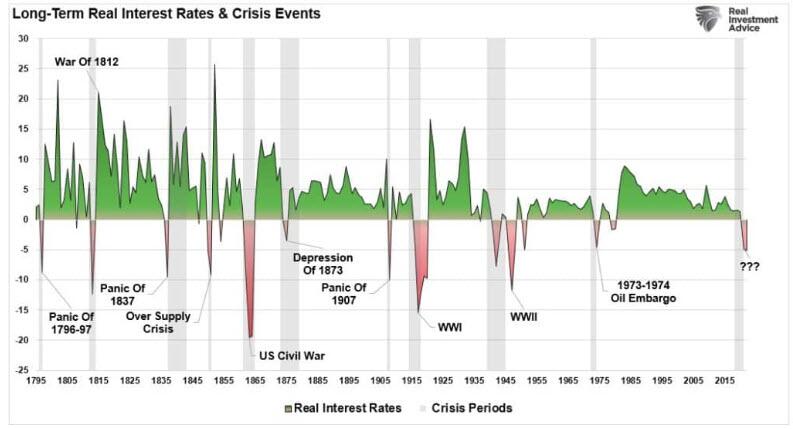

Such is because high inflationary periods also correspond with higher interest rates. In highly indebted economies, as in the U.S. today, such creates faster demand destruction as prices and debt servicing costs rise, thereby consuming more of available disposable income. The chart below shows “real interest rates,” which include inflation, going back to 1795.

Not surprisingly, each period of high inflation is followed by very low or negative inflationary (deflation) periods.

As noted initially, surging interest rates impact market functions, leading to financial instability.

“Thin U.S. Treasury liquidity and limited demand may make the U.S. market vulnerable to a market functioning breakdown, similar to U.K.” – Mark Cabana, BofA

As the Fed continues to hike rates to fight an inflationary “boogeyman,” the more considerable threat remains deflation from an economic or credit crisis caused by overtightening monetary policy.

History is clear that the Fed’s current actions are once again behind the curve. While the Fed wants to slow the economy, not have it come crashing down, the real risk is “something breaks.”

Each rate hike puts the Fed closer to the unwanted “event horizon.” When the lag effect of monetary policy collides with accelerating economic weakness, the Fed’s inflationary problem will transform into a destructive deflationary recession.

Tyler Durden

Fri, 10/14/2022 – 12:40

via ZeroHedge News https://ift.tt/ZfN3gVP Tyler Durden