ISM Manufacturing Tumbles To Post-COVID Lows, Employment Slumps

US ‘hard’ macro data has continued to surprise to the upside in the last month (despite ‘soft’ regional Fed survey data fading), and consensus expected both ISM and PMI Manufacturing surveys for March to show another month of contraction.

-

S&P Global US Manufacturing PMI Final March 49.2, down from flash print at 49.3, but up from the 47.3 in Feb – that is the 5th straight month of contraction (sub-50)

-

ISM Manufacturing March dropped to 46.3, from 47.7, and below 47.5 expectations – that is the 5th straight monthly contraction to the lowest since May 2020

Source: Bloomberg

Twelve industries reported contraction in March, led by furniture, nonmetallic mineral products and textiles. Six sectors expanded.

“New order rates remain sluggish as panelists become more concerned about when manufacturing growth will resume,” Timothy Fiore, chair of ISM’s Manufacturing Business Survey Committee, said in a statement.

“Price instability remains, but future demand is uncertain as companies continue to work down overdue deliveries and backlogs.”

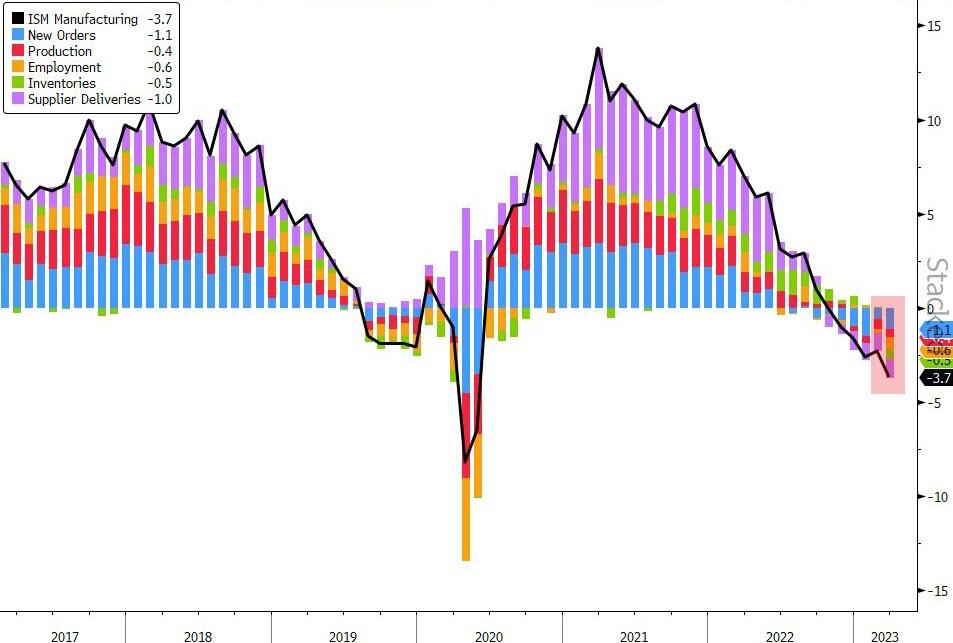

Under the hood, ISM is ugly with all the factors weighing negatively on the headline for the second month in a row…

Source: Bloomberg

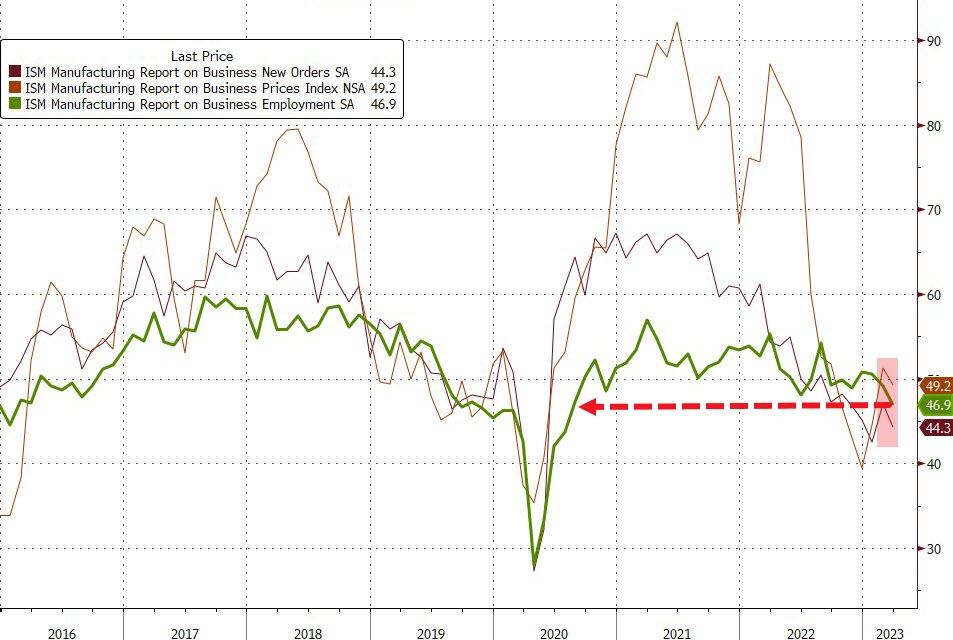

ISM employment weakest since July 2020…

Source: Bloomberg

New Orders/Inventories has stopped improving as the signal remains deeply in recession-signaling territory…

Source: Bloomberg

Siân Jones, Senior Economist at S&P Global Market Intelligence, said:

“The US manufacturing sector continued to signal concerning trends during March. Although output rose for the first time since last October, growth was fractional, and largely supported by ramping up production following an unprecedented reduction in supply chain pressures. “

“The timely delivery of inputs allowed firms to work through backlogs, but sparse demand amid pressure on customer spending due to higher interest rates and inflation spoke to challenges ahead for goods producers if there is little change in domestic and international client appetite. “

“Weak demand for inputs resulted in some relief for manufacturers as input cost inflation slowed again. A paucity of new orders sparked efforts to entice customers, however, as selling price inflation eased notably to the weakest since October 2020. Nonetheless, inflationary concerns weighed on business confidence once again amid pressure on margins.

“Encouragingly, firms were able to expand factory workforce capacity again, albeit at only a marginal pace, as skilled candidates for long-held vacancies were found.”

Finally, here’s how S&P Global describes the way forward:

Goods producers remained strongly upbeat in their outlook for output over the coming year in March. Hopes of greater client demand drove optimism. Confidence slipped to the lowest level in three months amid inflation concerns, however.

Confused?

Tyler Durden

Mon, 04/03/2023 – 10:05

via ZeroHedge News https://ift.tt/vFLpDrY Tyler Durden