Yuan Tumbles To 2023 Low After Chinese Exports Collapse Amid Speculation Unrigged Numbers Are Much Worse

It’s been a while since the market considered the possibility of a yuan devaluation: after the latest Chinese trade data it’s time to start seriously thinking about it once again.

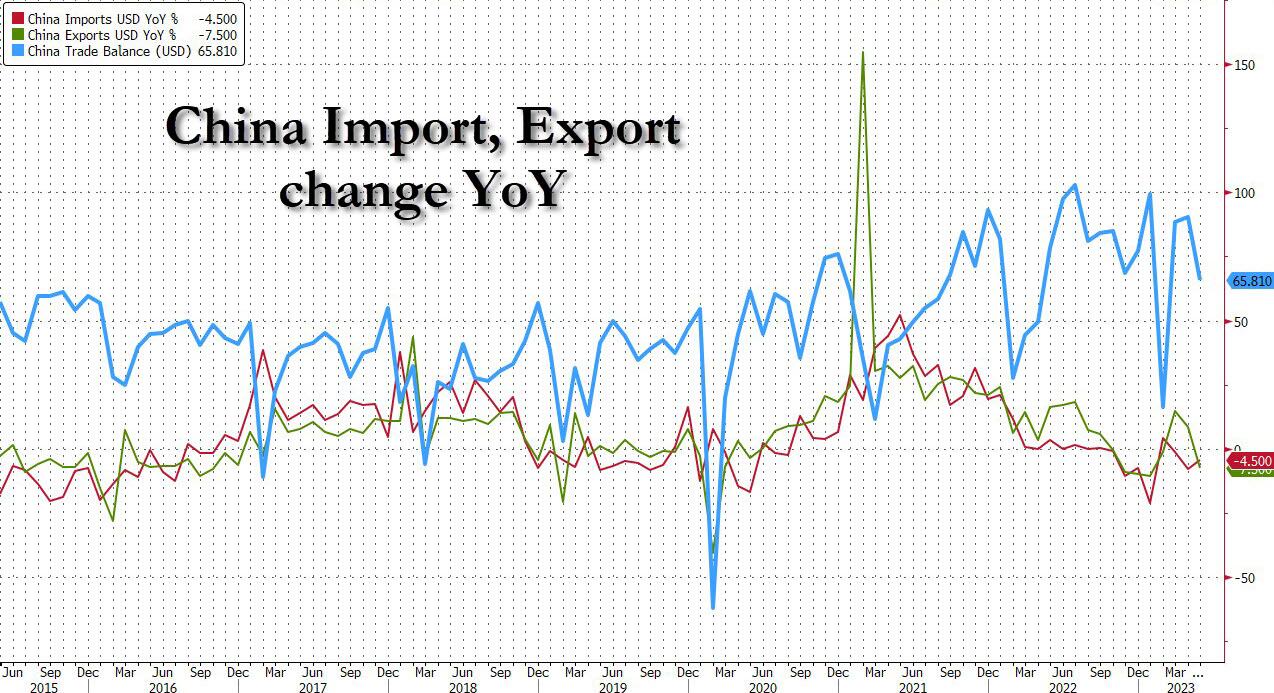

Overnight, China reported May trade data which revealed that exports again slowed sharply and missed market expectations, while imports also contracted but modestly beat expectations:

- *CHINA MAY EXPORTS -7.5% Y/Y IN DOLLAR TERMS; EST. -1.8%

- *CHINA MAY IMPORTS -4.5% Y/Y IN DOLLAR TERMS; EST. -8.0%

Although it was partly due to base effects, the underlying momentum has clearly slowed after a resilient 1Q. As SocGen notes, the disappointing export data helps explain the weakness in the manufacturing sector as the latest PMI data showed.

And despite the French bank’s call for near-term growth resilience in DMs, exports remain a key headwind to China’s manufacturing sector. More importantly, the data clearly reinforces expectation for more easing from the PBoC.

Some more details:

- May exports slowed sharply from +8.5% in April to -7.5% in USD terms, partly due to base effects as exports recovered in May 2022 after the Shanghai lockdown. The weakness was broad-based. By product, machinery and electrical equipment (MEE) products plunged from +10.4% to -2.1%. Within that, electronic products remained in deep contraction in yoy terms: mobile phones deteriorated again from -13% to -25%; IC plunged by 26% after a 7% decline; but the slowdown in PC and parts seems to have stabilized. Autos also slowed from +83% to +55% but remained strong.

- Outside MEEs, there was an even more pronounced deceleration in traditional consumer goods, such as apparel, footwear and furniture, reflecting normalising consumer demand in DMs. By destination, the slowdown was mainly driven by exports to ASEAN economies, which slowed from +5% to -16%. Exports to the US and the EU also moderated, from -7% to -18% and from 4% to -7%, respectively.

- Meanwhile, after the disappointment in April, imports improved slightly from -7.9% to -4.5% but remained at a weak pace, reflecting sluggish domestic demand. Among commodities, there was a notable rebound in oil (from -1% to +12%, in volume terms) and copper (from -13% to -5%), while iron ore eased slightly from +5% to +4%, as high-frequency data show that construction activities remained soft in May. The contraction in MEE imports eased somewhat from -16% to -14%, led by ICs, but remained weak due to stagnant export demand for electronics

While China’s economy has had a dreadful post-covid “recovery”, at least trade was solid. Well, not anymore, which is why we asked yesterday if yuan devaluation was coming (China suddenly needs a far weaker yuan to boost its exports, which account for roughly 40% of China’s GDP).

*CHINA MAY EXPORTS -7.5% Y/Y IN DOLLAR TERMS; EST. -1.8%

*CHINA MAY IMPORTS -4.5% Y/Y IN DOLLAR TERMS; EST. -8.0%a little yuan devaluation on deck to spice things up

— zerohedge (@zerohedge) June 7, 2023

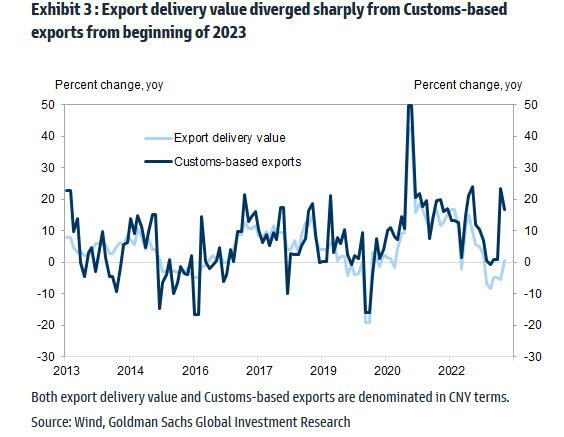

But wait, there’s more, because while China’s exports are clearly slowing, the real picture could be far worse. Why? Because as everyone has known for years, China has been rigging its trade data to make its economy appears stronger than it is, similar to what the Biden admin is doing with labor data.

In a recent piece from Goldman “Analyzing recent puzzles on China trade data” (available to pro subs in the usual place), the bank wrote in late May that despite weakening external demand, “China’s exports have beaten consensus expectations for four consecutive months now” (but not five months as the latest trade data showed).

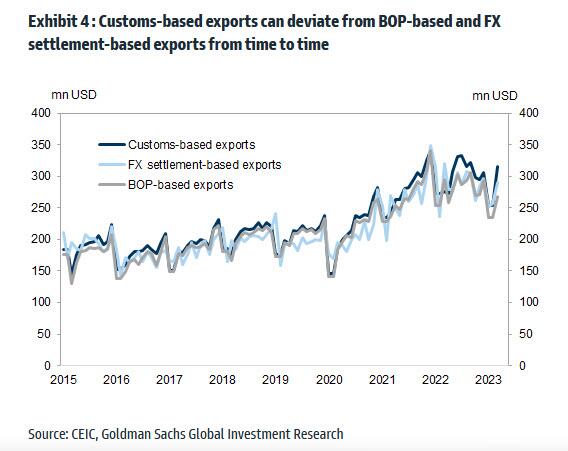

But, as we have observed frequently in the past, Goldman cautions that different trade-related data seem to send conflicting signals and some trading partners’ reported imports from China appear inconsistent with China’s exports to these countries. This has prompted “many client questions on the reliability of Chinese trade data” according to the bank’s strategists. Here is Goldman’s punchline:

Our “outside-in” measure does not show systematic divergences between China’s import data and trading partners’ exports to China in Q1. However, trading partners’ data released so far suggest significantly lower year-over-year growth than China’s export data in March.

A chart showing just how glaring the trade discrepancy has become:

Nowhere is the trade discrepancy more obvious than in bilateral “trade” with Singapore: here, the gap between China-reported exports to Singapore and Singapore-reported imports from China has become laughable.

Goldman then writes that “some of the discrepancies may be related to re-exports and transshipment, but disguised capital outflows are also a potential explanation.”

But whatever the reason for the staggering divergence between China’s export data and everyone else’s, the conclusion is that China’s true exports are far, far weaker than the officially reported. And while China’s fake export “data” was stronger than expected for 4 months in a row, now that even Goldman pointed out just how fake the Chinese data is, reality may be coming home to roost. Which is also why the market is now starting to frontrun what comes next: a powerful impulse to weaken the currency, because while Beijing may not feel the heat to stimulate as long as (fake) exports are growing and are coming stronger than expected, once China’s mercantilist engine begins to sputter, even Xi has to pay attention. And sure enough:

- *OFFSHORE YUAN WEAKENS TO 7.1479 PER DOLLAR TO FRESH 2023 LOW

And one China aggressively pursues quasi (or full) devaluation, the race to the currency bottom will restart with a vengeance.

Tyler Durden

Wed, 06/07/2023 – 13:40

via ZeroHedge News https://ift.tt/Dx9rtEp Tyler Durden