Coders, Learn To Build

Back in late January, when prevailing consensus was that the Fed’s aggressive rate hikes would crush US residential housing, we showed readers a little known market indicator which signaled that the housing market was in far better shape than conventional wisdom suggested, and asked whether the housing market has bottomed.

Has The Housing Market Bottomed? The Surprising Result From A Little-Known Market Indicator https://t.co/0Om3HalcSI

— zerohedge (@zerohedge) January 30, 2023

Since then, despite mortgage rates rising to 7%, back to the highest level of the 21st century, housing stocks have continued to push higher, and the homebuilder ETF (XTB) is up 20%, and just shy of its all time high. In other words, at least as far as the market is concerned, the answer whether housing has bottomed has been a resounding yes.

{kind=link}

But how is that possible? Isn’t the US consumer crushed? Aren’t credit standards so tight that virtually nobody can get a mortgage? Haven’t 7% mortgages made housing the most unaffordable in history?

While the answer to all those questions is a resounding yes, there is something else that matters much more, and is a far bigger driver of housing supply/demand equilibrium levels, i.e., prices.

We are talking, of course, about housing inventory… or the lack thereof.

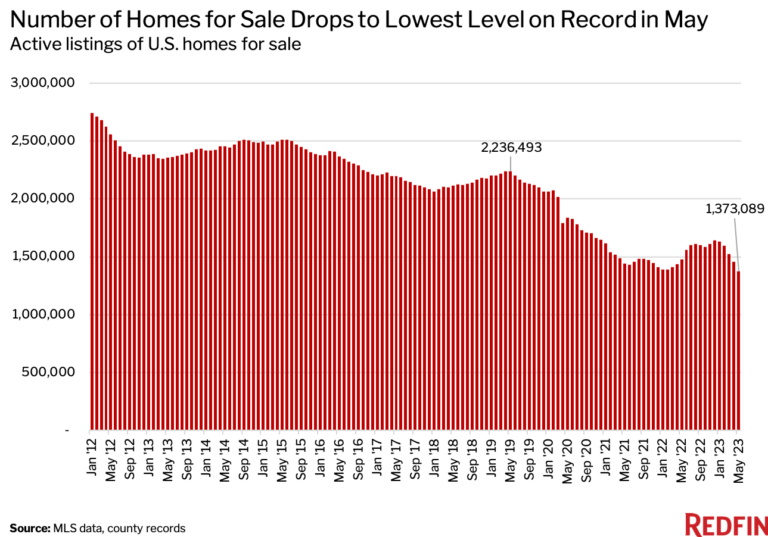

Consider: according to the latest report RedFin, in May there were fewer homes for sale than any other month on record! Specifically, the number of homes for sale in the U.S. fell 7.1% year over year to 1.4 million on a seasonally adjusted basis in May. That’s the lowest level in Redfin’s records, which date back to 2012, and the first annual decline since April 2022.

{kind=link}

By comparison, there were 2.2 million homes for sale in May 2019, before the pandemic rocked the U.S. housing market, meaning housing supply was 38.6% below pre-pandemic levels this May.

America’s housing stock is dwindling because there are very few people selling homes. A key reason cited for the lack of supply is that nobody who has a mortgage in the 3-4% ballpark, wants to cash out and take out a new mortgage that is up to 4% higher, wiping out any capital gains from the sale transaction. Some more math:

Nearly every homeowner with a mortgage has an interest rate below 6%, meaning many are opting to stay put because selling and buying a new home would mean taking on a higher monthly mortgage payment. The average 30-year-fixed mortgage rate in May was 6.43%, up from 5.23% a year earlier and a record low of 2.65% in 2021.

Whatever the reason for the lack of sales, new listings of homes for sale declined 25.2% year over year in May to the third lowest level on record on a seasonally adjusted basis, as homeowners were handcuffed by high mortgage rates.

As the pool of homes for sale shrinks, homebuyers in many markets are grappling with competition, which is preventing home prices from plunging despite a freeze in buyer demand brought on by elevated mortgage rates. Effectively, there is a standoff where sellers don’t fell compelled to sell, and buyers can’t afford to pay prices demanded by sellers, which has resulted in a deep freeze of the housing market where bids and asks for the same house are sometimes hundreds of thousands of dollars apart.

Meanwhile, the median U.S. home sale price was $419,103 in May. That’s down just 3.1% from a year earlier, when prices hit a record high of $432,311. While home prices fell in May, they posted a smaller decline than they did in April, when prices dropped 4.2% from a year earlier—the largest decrease on record with the exception of January 2012.

{kind=link}

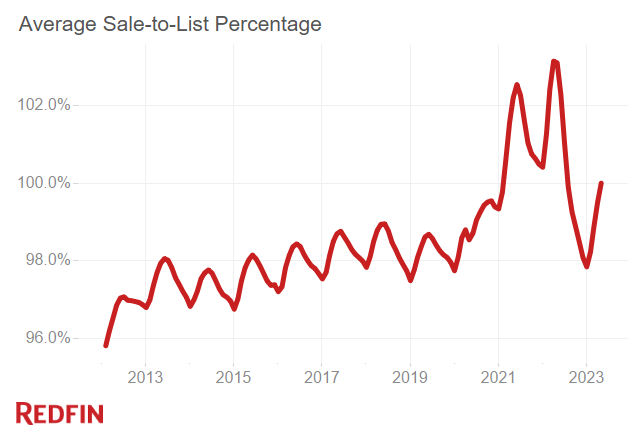

Another remarkable consequence of the plunge in inventory is that the typical home that sells is no longer selling at a discount. According to RedFin, the average sale-to-list-price ratio, which measures how close homes are selling to their final asking prices, was 100% in May, meaning the typical home that sold was purchased at its list price. That’s down from 103.1% a year earlier, but is the highest level of any May on record prior to the pandemic and follows nine straight months of sub-100% sale-to-list-price ratio

{kind=link}

Still, as Redfin Chief Economist Daryl Fairweather says, “it’s too early to say that price declines have bottomed out. Prices may have room to fall because mortgage rates could still rise. The Federal Reserve just signaled that it is likely to continue raising interest rates this year. That could further hamper homebuyer demand and cause home prices to fall in the near term, though the drops would be minimal. We’re unlikely to see double-digit price declines like we did during the 2008 housing crisis.”

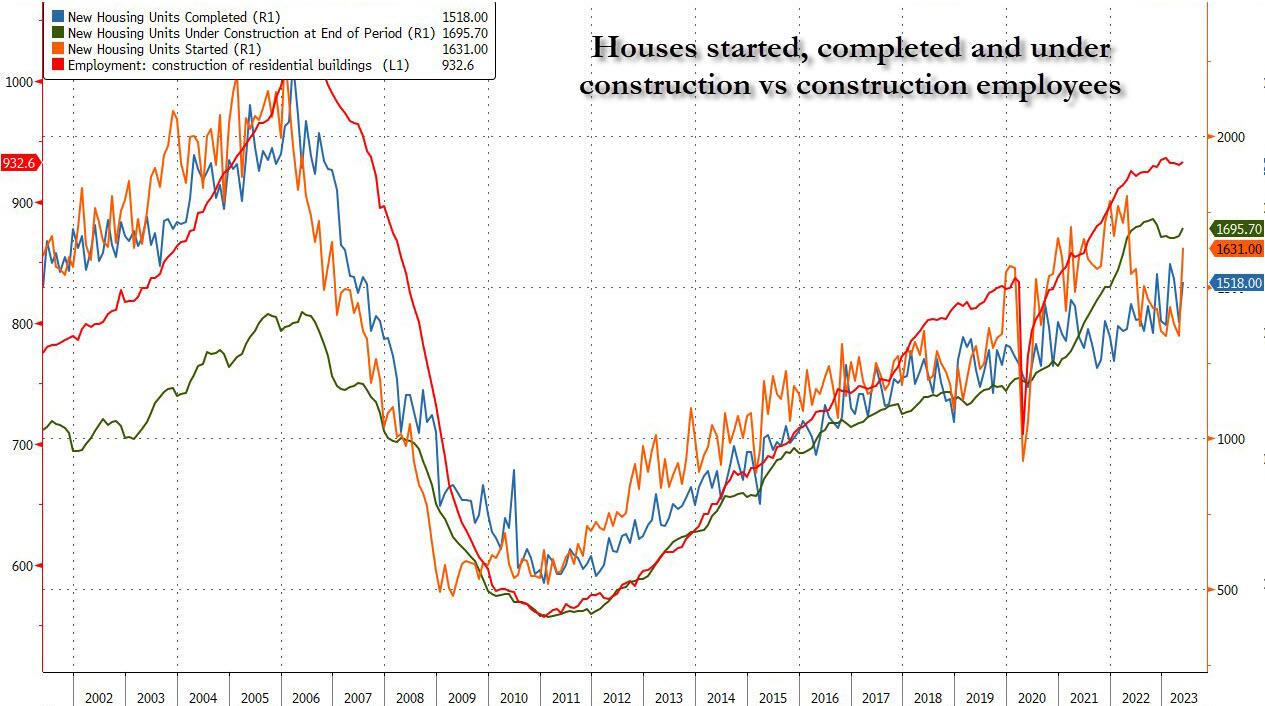

There is another reason why prices may drop: there has been a flood of new home construction. As the next chart shows, the number of houses under construction at this moment are just shy of their all time high, and well above both starts and completions.

{kind=link}

Which has a profound consequences for the US labor market: thanks to the frenzied in process construction of single family houses, employment in the construction sector is effectively the highest it has been since 2007, and rapidly approaching an all time high.

Which brings us to the punchline.

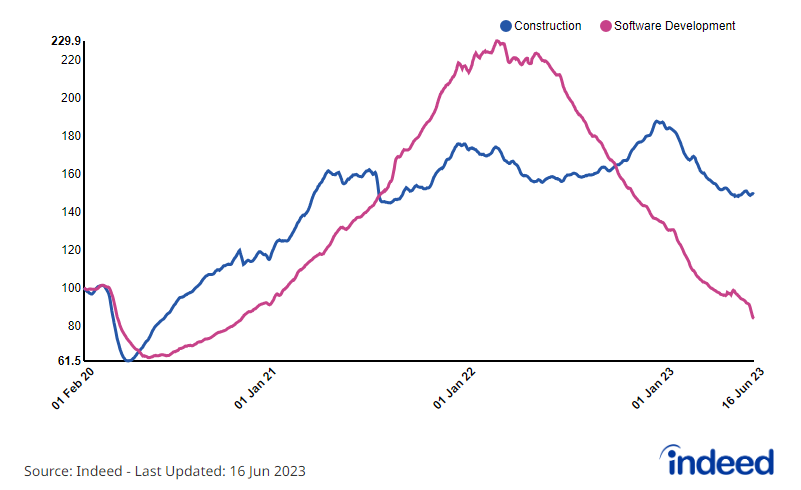

Remember when a few years ago the derogatory punchline lobbed at all those (reporters) who had been recently let go was to “learn to code.” Fast forward a few years, and coder jobs have gone stone colder as a result of not only the surge in rates which has forced tech companies to become profitable (which most of them can’t so they have had to lay off hundreds of thousands of highly paid workers), but the coming AI/ChatGPT shock which will lead to even more layoffs. In any case, as the following chart from the Indeed hiring platform (which tracks job openings much more accurately than the politically-mandated mess that is JOLTs) shows, hiring for softwarre development jobs has plunged and is now near the March 2020 trough even as hiring of construction workers fires on all cylinders. Some more details:

Indeed hiring tabs open jobs by US sector relative to pre-covid Feb 2020 baseline: purple is Software Development (-16.1% from pre-pandemic) and blue is Construction (+49.2% from pre-pandemic). As Goldman notes, this is “clearly a reflection of the continued shortage of blue collar labor while the job cuts in big tech have had an impact on software employment.”

{kind=link}

The bank concludes that this is “a good reminder that this labor market can not be painted with a broad brush while the secular forces of demographics, immigration and the wake of covid has left lasting labor shortages in pockets of the economy.”

Which is true. What is also true, is that the worker class that until not too long ago was certain it was immune from the vagaries of the economic cycle, and acted accordingly refusing to show up to the office and instead of actually working, spent the day at home in various yoga positions or drinking some supposedly healthy green crap while getting their 10th covid booster shot, the “coders” are suddenly in zero demand, while the “hot” job sector is now construction. To all those programmers, who are about to get steamrolled by the double whammy of being made obsolete by a chatGPT algos, we have three words of advice: “learn to build.”

Tyler Durden

Tue, 06/27/2023 – 19:05

via ZeroHedge News https://ift.tt/V26uw5s Tyler Durden