China To Bail Out 1 Trillion Yuan In “Hidden” LGFV Debt By Shifting It To Provinces

It was just on Monday when we reported that China was facing a new debt crisis as a record number of local government financing vehicles (or LGFVs also considered the currently most aggressive form of Chinese shadow banks), had missed commercial paper debt payments:

A total of 48 LGFVs were overdue on commercial paper, which typically carries a maturity of less than a year, up from 29 in June, according to a Huaan Securities report citing data from the Shanghai Commercial Paper Exchange. Their missed payments amounted to 1.86 billion yuan ($259 million), more than double the 780 million yuan in June.

And with Beijing suddenly finding itself on the defensive everywhere, amid collapsing exports, CPI deflation, record youth unemployment and lack of credit growth, overnight China’s leadership decided to finally take some proactive steps instead of just endlessly talking, and as Bloomberg reported, China will allow provincial-level governments to raise about 1 trillion yuan ($139 billion) via bond sales to repay the debt of local-government financing vehicles and other off-balance sheet issuers, a small step toward addressing what it called “one of the biggest threats to the nation’s economy and financial stability.”

The Ministry of Finance has informed relevant authorities about the “refinancing bonds” program, people with knowledge of the matter said, asking not to be identified as they aren’t authorized to discuss the program. The quota has been set for each region, one of the people said, without providing further details on sizing.

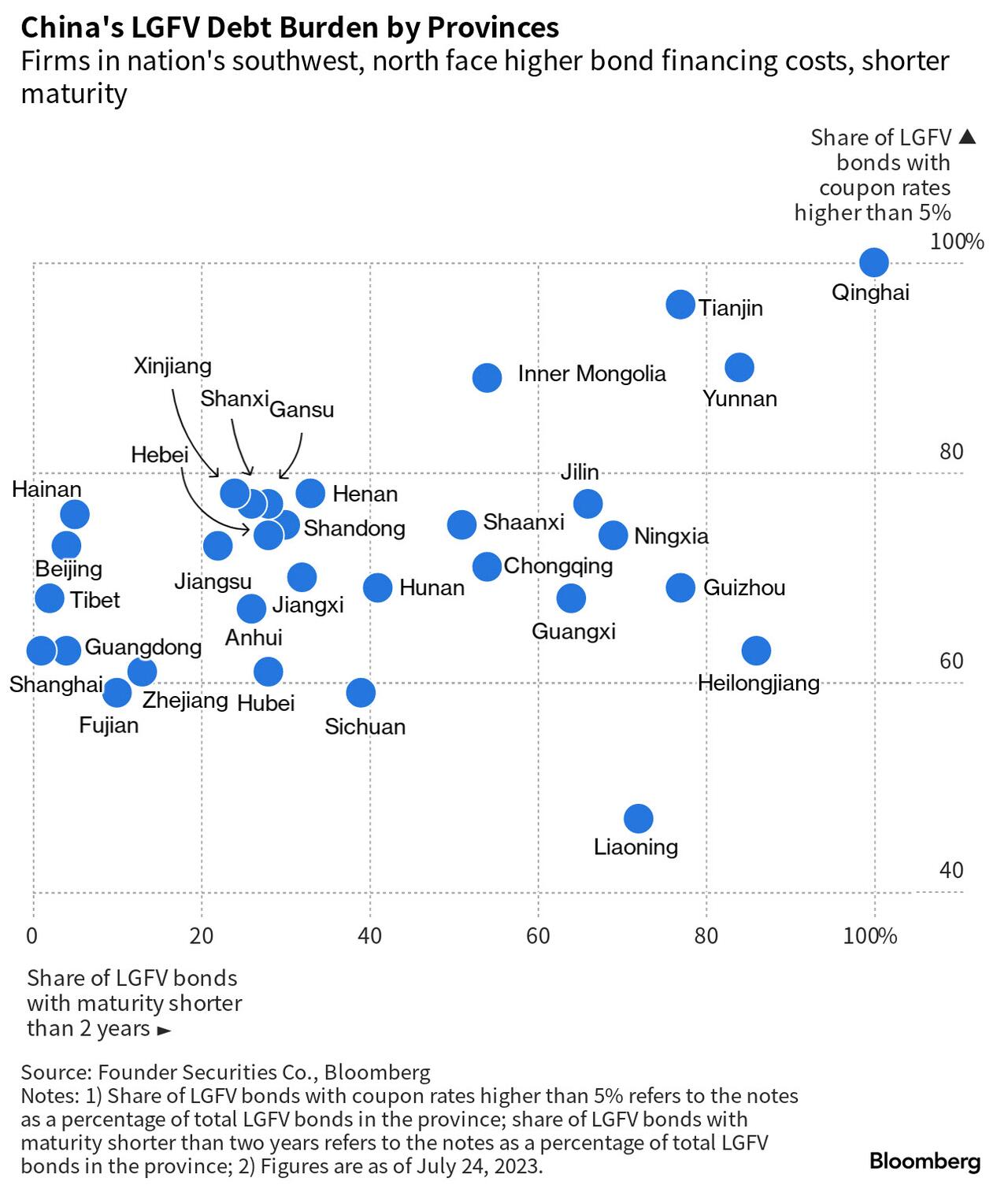

The report notes that all provincial-level governments but Beijing, Shanghai, Guangdong and Tibet will be able to use the bonds to repay off-balance sheet liabilities, known as “hidden” debt in China, as it is kept off the balance sheets of local authorities, yet is widely considered in financial markets to carry an implicit government guarantee of repayment. Authorities also identified 12 provinces and cities as “high-risk” areas where more support will be provided, including the provinces of Guizhou, Hunan, Jilin and Anhui, as well as Tianjin city. A Bloomberg source familiar with the latest plan didn’t explain why Beijing, Shanghai, Guangdong and Tibet had been excluded from the new debt swap program, those four places either have no “hidden” debt or have very little.

Effectively what China is doing is bailing out weaker issuers including LGFVs, and shifting the debt burden to provincial governments instead.

The debt raised is kept off the balance sheets of local authorities, yet is widely considered in financial markets to carry an implicit government guarantee of repayment.

The problem however, as Goldman notes this morning, is that it’s small in the context of the issue:

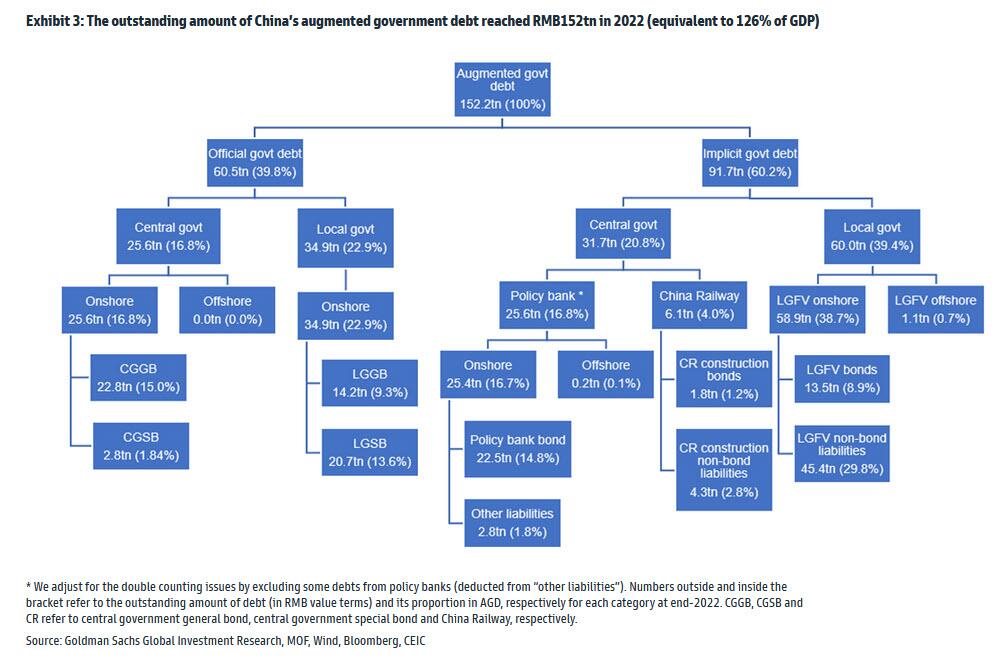

“The amount covered under the debt swap program, though, is a drop in the bucket compared to the 66 trillion yuan the International Monetary Fund estimates local government financing vehicles will hold by the end of this year. It’s also far smaller in size than a similar initiative launched by the government in 2015.”

Back then, China deployed a massive debt-swap arrangement worth 12.2 trillion yuan for a few years in a bid to lower the amount of off-balance sheet debt carried by local governments. Now widely referred to as “hidden” debt, the term refers to funds raised by government-related entities — such as LGFVs — which borrow from banks and bond markets to finance infrastructure spending and other public projects.

President Xi Jinping had previously described the issue of hidden debt as one of the “major economic and financial risks” facing China. The government began a round of nationwide inspections to work out how much money local governments’ owe, another sign of how authorities were working to tackle financial risks, Bloomberg News reported in June.

The program suggests that “China is reducing the debt load on local government financing platforms to boost their capacity to serve as a channel for future stimulus,” rather than stimulus in the second half of the year, said Duncan Wrigley, chief China economist at Pantheon Macroeconomics Ltd.

He added that the “main buyers” of refinancing bonds are likely to be domestic banks and asset managers, such as wealth management funds, insurers and pension funds.

The modest size of the bailout is just one problem; the other one is that it doesn’t really do anything besides shift debt around: indeed, as Bloomberg notes, China’s 2015 program didn’t do much to actually solve the debt issue. Meanwhile, the costs of servicing debt have risen in recent years, creating a drag on Chinese fiscal spending. At the same time, many local governments have seen their income drop due to a two-year property market slump and two years of pandemic relief spending. That’s raised the risk that LGFVs will default on their debt, which could destabilize China’s financial system.

Even so, the swap program this time around – which is just another can-kicking exercise – may help defuse the risks of default faced in the regions where it’s implemented. It can also bring down the financing costs on the hidden debts, give local governments more time to repay, and improve funding conditions in those places. One person said the issuance will be planned in batches.

Unlike a write-off, however, the debt will still have to be serviced — squeezing the room already debt-laden local governments have to sell more bonds to fund infrastructure investment and spur economic growth.

Beijing has tried a few other ways to resolve debt woes in recent years. In 2019, some counties in less-developed regions were picked by the government to replace their hidden debt with bonds in a trial program to improve their financing ability.

In late 2020, special local bonds for refinancing purposes were introduced — first as a way for weak regions to reduce their off-balance sheet liabilities, and then as a strategy for rich places including Beijing, Shanghai and Guangdong in southern China to clear hidden debt. Guangdong in 2021 became the first to claim it had successfully eliminated such debt.

Unfortunately for China, there is just no magic wand it can wave and watch its record debt disappear. Meanwhile, no matter how it classifies it, reshuffles it or spreads it around…

… the total will just keep rising, giving Beijing only one option: to kick the can it will have to shift more of it to the buyer of last resort, the PBOC, something the “developed” world discovered in 2008.

Tyler Durden

Fri, 08/11/2023 – 07:46

via ZeroHedge News https://ift.tt/2wr3buX Tyler Durden