Key Events This Week: Retail Sales And FOMC Minutes

With the mid-summer sun rising, things turn much quieter across markets although there are still enough events to keep traders on their toes and within Wifi coverage at their favorite vacation spot. As DB’s Peter Sidorov writes, in terms of events this week, we will get several soundbites on the strength of the US economic cycle, especially on the consumer front, with retail sales (Tuesday) industrial production (Wednesday) and a number of key retailers reporting results. In addition, the Fed will release the minutes of the July FOMC meeting (Wednesday).

In Europe, the key data will be in the UK, with the July labour market (Tuesday), inflation (Wednesday) and retail sales (Friday). It will also be a busy week in Asia with the July activity data and the 1-year MLF rate decision in China (Tuesday) and with preliminary Q2 GDP (Tuesday) and national CPI (Friday) in Japan.

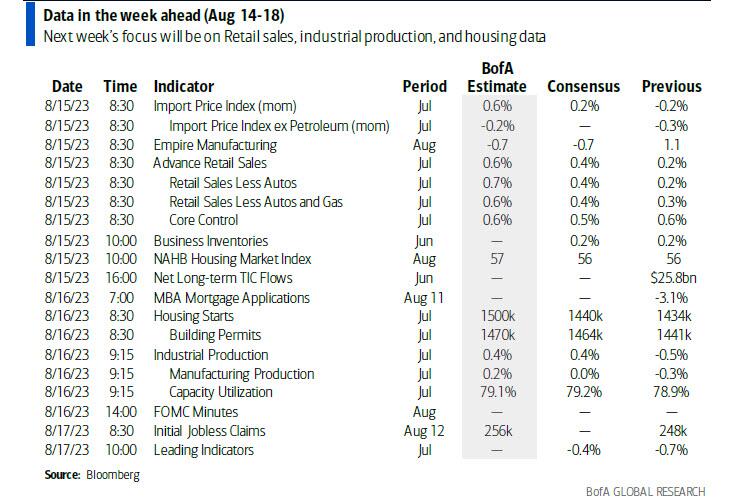

In more detail, DB economists expect monthly retail sales to rise +0.3% in July (vs +0.4% consensus and +0.2% prev.) with a slightly slower rise in retail control (+0.2% vs +0.5% consensus). We will also get July industrial production (est. +0.3%), housing starts, the NAHB housing market survey and business surveys from the New York and Philly Feds. The health of the consumer will be crucial to whether the US can avoid a recession. US households will face more headwinds in H2 – slowing employment growth, pass through of policy tightening as well as the resumption of student loan repayments and deferred taxes coming due – though these are more likely to become visible in the autumn. As a reminder, our US economists continue to see a baseline of a mild recession from late 2023, but consumer resilience has made it a closer call.

Consumer activity will also be in focus at the tail end of the earnings season with reports this week from Home Depot (Tuesday), Target (Wednesday) and Walmart (Thursday). Other notable corporate earnings include Cisco and Applied Materials in the US and Tencent and JD.com in China.

From a central bank perspective, the minutes of the July FOMC meeting will give hints about the Fed’s reaction function ahead of the September meeting, where the Fed is expected to keep rates on hold. With the data-dependent tone from Fed speakers, any discussion on the expected path of inflation will be particularly interesting.

Over in Europe, the UK inflation print for July will be the highlight. A strong downside surprise last month drove the second strongest daily rally in 2yr gilts (-18bp) since March. DB’s UK economist Sanjay Raja sees headline inflation at 6.8% in line with consensus, with core at 6.9% (consensus 6.8%). This would mark the lowest headline inflation since February 2022, but still the highest among the G7.

In Asia, China will dominate the headlines on Tuesday with the July activity data including retail sales and industrial production (we also get the 1yr MLF rate fixing the same day). After weaker trade and bank credit numbers last week, investors will watch for further evidence on the trajectory of China’s economy. The same day we will get the Q2 GDP print in Japan (DBe: +0.9% qoq vs +0.7% qoq consensus). Meanwhile, Japan’s CPI print on Thursday is expected to show CPI ex fresh food and energy moving back to its May peak (+4.3% DBe and consensus vs +4.2% prev.).

Courtesy of DB, here is a day-by-day calendar of global events

Monday August 14

- Data: Germany July wholesale price index

Tuesday August 15

- Data: US August Empire manufacturing index, NAHB housing market index, July retail sales, import and export price index, June total net TIC flows, business inventories, China July retail sales, industrial production, property investment, UK June average weekly earnings, unemployment rate, July jobless claims change, Japan Q2 GDP, June capacity utilization, Germany and the Eurozone August ZEW survey, Canada July CPI, existing home sales, June manufacturing sales

- Central banks: China 1-year MLF rate, Fed’s Kashkari speaks

- Earnings: Home Depot, Agilent Technologies, Cava

Wednesday August 16

- Data: US August New York Fed services business activity, July industrial production, housing starts, capacity utilization, building permits, China July new home prices, UK July CPI, PPI, RPI, June house price index, Italy June general government debt, Eurozone June industrial production, Canada July housing starts

- Central banks: Fed FOMC meeting minutes

- Earnings: Tencent, Cisco, JD.com, Target, Wolfspeed

Thursday August 17

- Data: US August Philadelphia Fed business outlook, July leading index, initial jobless claims, Japan July trade balance, June Tertiary industry index, core machine orders, Eurozone June trade balance, Canada June international securities transactions

- Earnings: Walmart, Applied Materials, SQM, Lenovo, Bilibili, Farfetch

Friday August 18

- Data: UK August GfK consumer confidence, July retail sales, Japan July national CPI, Eurozone June construction output, Canada July raw materials and industrial product price index

- Earnings: Deere, Palo Alto Networks, Estee Lauder, XPeng

* * *

Finally, turning to just the US, Goldman writes that the key economic data releases this week are the retail sales report on Tuesday and the Philadelphia Fed manufacturing index on Thursday. The minutes from the July FOMC meeting will be released on Wednesday, and Minneapolis Fed President Kashkari has a speaking engagement on Tuesday.

Monday, August 14

- There are no major economic data releases scheduled.

Tuesday, August 15

- 08:30 AM Empire state manufacturing survey, August (consensus -0.4, last 1.1)

- 08:30 AM Import price index, July (consensus +0.2%, last -0.2%); Export price index, July (consensus +0.2, last -0.9%)

- 08:30 AM Retail sales, July (GS +0.7%, consensus +0.4%, last +0.2%); Retail sales ex-auto, July (GS +0.7%, consensus +0.4%, last +0.2%); Retail sales ex-auto & gas, July (GS +0.7%, consensus +0.4%, last +0.3%); Core retail sales, July (GS +0.7%, consensus +0.5%, last +0.6%): We estimate core retail sales rose 0.7% in July (ex-autos, gasoline, and building materials; mom sa). Our forecast reflects a boost in the nonstore category from record sales on Amazon Prime Day, as well as solid high-frequency consumer spending data in the brick-and-mortar segment. We also estimate a 0.7% rise in headline retail sales.

- 10:00 AM Business inventories, June (consensus +0.2%, last +0.2%)

- 10:00 AM NAHB housing market index, August (consensus 56, last 56)

- 11:00 AM Minneapolis Fed President Neel Kashkari (FOMC voter) speaks: Federal Reserve Bank of Minneapolis President Neel Kashkari will participate in a moderated conversation followed by audience Q&A for APi’s annual global controllers conference. Livestream of the event will be available. On July 12, Kashkari said “one way supervisors could ensure banks are prepared is to run new high-inflation stress tests to identify at-risk banks and size individual capital shortfalls.”

Wednesday, August 16

- 08:30 AM Housing starts, July (GS -1.5%, consensus +0.9%, last -8.0%); Building permits, July (consensus +2.0%, last -3.7%)

- 09:15 AM Industrial production, July (GS +0.3%, consensus +0.3%, last -0.5%); Manufacturing production, July (GS +0.1%, consensus flat, last -0.3%); Capacity utilization, July (GS 79.0%, consensus 79.1%, last 78.9%): We estimate industrial production increased 0.3%, as strong electric utilities and auto production outweigh weak mining production. We estimate capacity utilization edged up to 79.0%.

- 02:00 PM FOMC meeting minutes, July 25-26 meeting: The FOMC raised the target range for the federal funds rate by 25bp at its July meeting, but declined to provide any clear signal about its intentions for the September meeting. Chair Powell said during his post-meeting press conference that the FOMC has not made a decision to hike every other meeting and will instead proceed meeting by meeting.

Thursday, August 17

- 08:30 AM Philadelphia Fed manufacturing index, August (GS -9.0, consensus -10.5, last -13.5): We estimate that the Philadelphia Fed manufacturing index picked up to -9 in August, reflecting the bottoming in East Asian industrial activity and the sequential improvement in US freight metrics.

- 08:30 AM Initial jobless claims, week ended August 12 (GS 240k, consensus 239k, last 248k): Continuing jobless claims, week ended August 5 (consensus 1,700k, last 1,684k)

Friday, August 18

- There are no major economic data releases scheduled.

Source: DB, Goldman, BofA

Tyler Durden

Mon, 08/14/2023 – 09:45

via ZeroHedge News https://ift.tt/ubJv4l9 Tyler Durden