Regulators Hope You Don’t Notice The Massive Hidden Losses In The Banking System

Subitted by Paul Kupiec, Senior Fellow, American Enterprise Institute

The Secretary of the Treasury and the Financial Stability Oversight Council would like you to believe that climate-change and unregulated non-bank financial institutions are the biggest threats to financial stability. If financial regulators were actually safeguarding the integrity of banks and financial markets, they would recognize, and do something about, the largest immediate threat to financial stability: the nearly $1.3 trillion of unrealized interest rate related losses in the regulated banking system. This is the real systemic risk today.

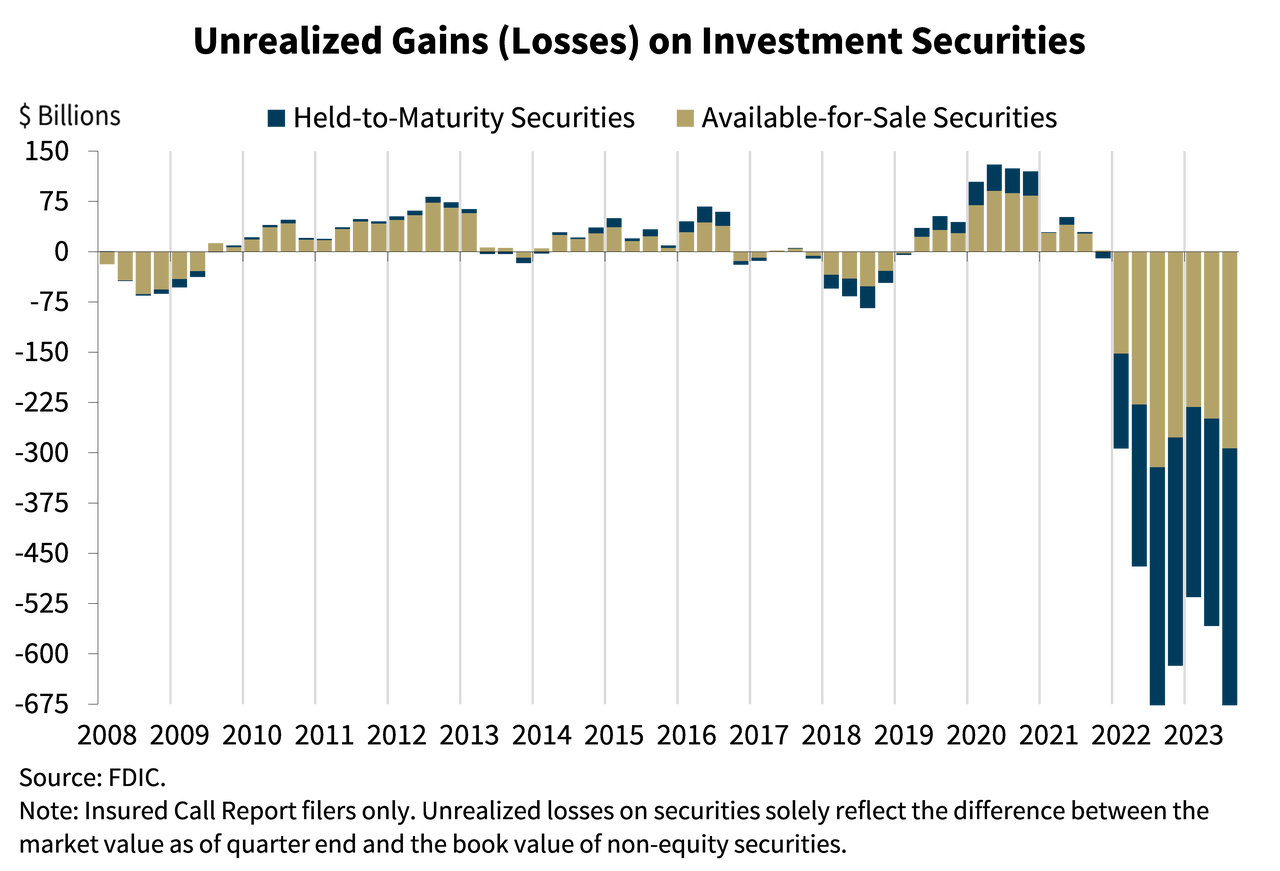

The $1.3 trillion is my estimate of the banking system’s total unrealized interest rate related losses as of June 30, 2023. Using bank regulatory data, I estimate that the banking system has total unrealized losses of about $548 billion on bank-owned securities and about $726 billion in interest rate driven losses on bank loan and lease portfolios.

These losses are important because they are not recognized in the value of banks’ reported regulatory capital. Regulatory capital is the buffer that is supposed to keep banks from failing and imposing losses on the FDIC insurance fund. Banks’ need sufficient capital to keep their incentives properly aligned. When banks have little capital their shareholders keep gains generated by their risky investments but off load losses to the FDIC when their risky investments sour.

If unrealized interest rate losses were realized, they would consume more than half of the banking system’s $2.3 trillion in total equity capital. And the loss absorbing capacity of the system’s equity is already reduced by the almost $800 billion in intangible assets and goodwill counted as bank equity. These assets historically have had little loss absorbing capacity when a bank fails. Taking these factors into account, the banking system is not nearly as well capitalized as our regulatory leaders claim.

Coincidently, the banking systems’ unrealized interest rate driven losses are roughly equal to the $1.3 trillion unrealized mark-to-market interest rate losses on the securities owned by the Federal Reserve.1 Given the Fed’s own reported unrealized interest rate losses, we can be sure that the Fed and other FSOC banking regulators are well aware that the banking system has a similar problem.

How did this happen? Between the Fed and Congress, COVID19 stimulus injected trillions of dollars of new deposits into the banking system. Between 2019/Q4 and 2022/Q1, total banking system deposits grew by more than 37 percent. Banks had to put these deposits to work earning enough interest to cover deposit insurance premiums, examination and other regulatory costs, service depositor accounts, and earn a return on shareholders’ investment. Under the Fed’s COVID-era zero interest rate policy, banks were unable to cover costs if deposits were invested in in short-term Treasury securities and deposits at the Federal Reserve.

To earn a positive margin, banks invested deposits in longer-term securities and loans with low or no credit risk and favorable regulatory capital treatment. The yields on these investments, while low by historical standards, paid an interest rate premium over short-term instruments by virtue of their longer maturities.

The strategy of investing demandable deposits in long-maturity fixed rate instruments with low regulatory capital requirements was profitable as long as inflation remained low and deposit interest rates were close to zero. The onset of unexpected inflation eventually forced the Fed to change monetary policy. The Fed increased short-term interest rates and started draining bank deposits from the system causing interest rates at all maturities to increase, raising banks’ cost of retaining deposits, and creating market value losses on bank’s long-maturity fixed-rate investments.

For accounting statement and regulatory capital purposes, banks value their loans, leases and held-to-maturity securities at historical cost. The largest banks have to include market value losses on their securities designated “available for sale” when calculating their regulatory capital, but most smaller banks are allowed to ignore these losses. As a consequence, banks’ regulatory capital ratios claim that bank asset values are approximately $1.3 trillion larger than the current market value these assets would command if they were sold or pledged as collateral.

Regulators measure banks’ capital adequacy using several different ratios that involve some measure of bank regulatory capital divided by some measure of bank assets. I focus on bank regulatory Tier 1 leverage ratios, the ratio of bank total Tier 1 regulatory capital to a bank’s average quarterly assets. All banks are required to report this measure but nearly 1700 smaller banks do not report any of the risk-weighted capital ratios reported by larger banks.

As of June 30, 2023, only 8 banks had a regulatory Tier 1 leverage ratio below the 6 percent threshold that regulators use to designate a bank as “well capitalized”. No bank has a ratio below the 4 percent threshold that designates an “undercapitalized” institution. By this regulatory measure, the banking system appears to be well-capitalized, but this regulatory ratio ignores the actual market value of bank assets.

Adjusting bank Tier 1 regulatory capital ratios by the unrealized mark-to-market losses on bank securities reported by banks, and by a reasonable (likely low) estimate of the mark-value losses banks have suffered on their loan and lease portfolios, gives a radically different picture of the banking system’s capital adequacy. Out of the 4697 insured depository institutions, 2372 have market-value adjusted Tier 1 leverage ratios smaller than the 4 percent “undercapitalized” threshold requiring regulators to take “prompt corrective action”. This number includes 1790 banks with ratios below the 3 percent “significantly undercapitalized” threshold. Undercapitalized banks hold more than 54 percent of the total assets in the banking system including more than 46 percent held in significantly undercapitalized institutions.

The Treasury Secretary and FSOC members are well aware of the danger posed by unrealized interest rate related losses in the banking system, but you would not know it from their public statements. Regulators should be using prompt corrective action powers to restrict under-capitalized banks from paying dividends and require them to raise new capital. Instead they have allowed banks to pay out almost $96 billion in dividends in the first half of 2023 and focused their regulatory efforts on imposing new complex capital regulations for the largest banks that would not address this real systemic problem.

Federal bank regulators are hoping that if they ignore this problem, you will too, and the problem will go away when the inflation genie is back in the bottle and interest rates decline. But this may not happen soon. Core inflation is still running at nearly twice the Fed’s target rate, unemployment is low, economic growth remains stronger than many anticipated, and Congress remains on a massive deficit spending spree. Hoping for a speedy return to a near zero environment before there a run of costly bank failures is not a sound regulatory strategy.

[1] www.federalreserve.gov/aboutthefed/files/quarterly-report-20231117.pdf Table 3.

Tyler Durden

Mon, 12/04/2023 – 15:00

via ZeroHedge News https://ift.tt/WnDg9V2 Tyler Durden