China’s Debt Binge Spurs Moody’s To Downgrade Credit Outlook

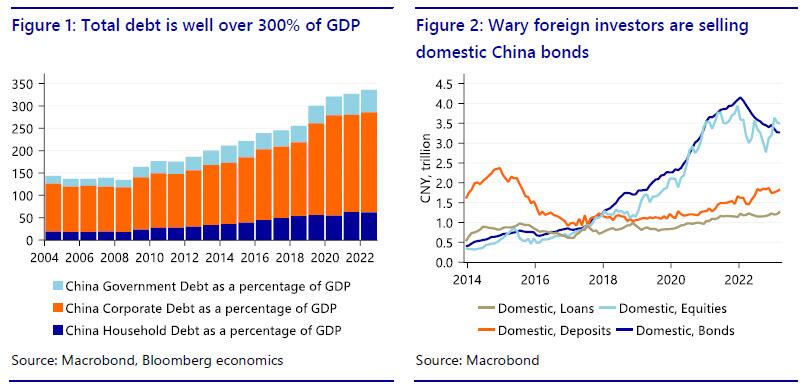

A protracted downturn in China’s real estate sector as well as a broader economic deceleration, but most of all downside risks from China’s record debt load which is now well over 300% of GDP…

… has led Moody’s Investors Service to downgrade China’s sovereign credit rating outlook from stable to negative.

While the revision does not signify Moody’s will imminently downgrade China’s credit rating, it does increase the odds if persistently lower growth and troubles in the property sector do not diminish.

As the FT reports, the rating agency – which one month ago also lowered its US credit rating to negative – was concerned that government and state firms would provide fresh financial support to weak regions in the country, “posing broad downside risks to China’s fiscal, economic and institutional strength.” And they will, because they have no other choice, and the alternative is economic collapse and social upheaval.

The deteriorating outlook comes as the latest housing data in the world’s second-largest economy shows no end in sight for the property crisis amid worsening home sales. We noted last month that home prices plunged the most in eight years.

Accelerating turmoil in the property market is further evidence that fiscal and housing stimulus to reboot the economy has failed so far, and perhaps a depression is unavoidable.

Another concern is that local government debt has surged due to plummeting land sale revenues from the property downturn and pandemic lockdowns. This raises fears of a broader financial crisis. Additionally, there are mounting worries in China’s $3 trillion “shadow banking” sector, primarily because of bad property investments.

For the broader economy, Moody’s forecasts GDP growth around 4% in 2024 and 2025 – nearly halved from 2019 levels.

Moody’s also maintained an A1 rating on China’s sovereign bonds:

“The affirmation of the A1 rating reflects China’s financial and institutional resources to manage the transition in an orderly fashion.

“Its economy’s vast size and robust, albeit slowing, potential growth rate, support its high shock-absorption capacity.”

China’s Finance Ministry, predictably, called Moody’s decision “disappointing”:

“China’s economy is shifting to high-quality development, new drivers of China’s economic growth are taking effect, and China has the ability to continue to deepen reforms and respond to risks and challenges,” adding that Moody’s concerns about the country’s growth and fiscal profile are “unnecessary.”

Simon Harvey, head of FX analysis at Monex Europe, responded to the decision and warned it’s tough to turn constructive on Chinese assets and the yuan.

“It was notable that the decline in USD/CNY towards the end of November didn’t necessarily coincide with an improvement in China’s macro outlook, without which we think it is difficult to turn constructive on Chinese assets and the yuan,” Harvey said.

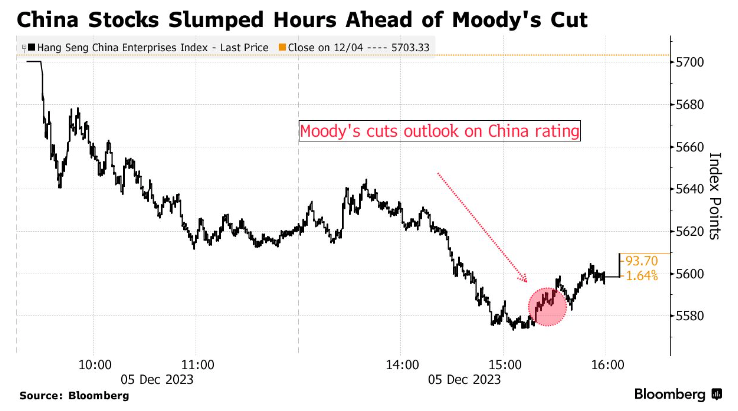

As a result, the yuan extended losses on Tuesday. China equity indexes, including the CSI 300 Index and Hong Kong’s Hang Seng, fell 1.90% and 1.91%, respectively.

Bloomberg indicated that details of Moody’s decision were leaked prior to the official announcement, with speculations suggesting a possible leak as early as last Friday.

Last week, the OECD warned that “structural stresses” in China contributed to downside risk to global growth.

This comes less than a month after Moody’s cut its outlook on US credit ratings to negative from stable, citing downside risks to the world’s largest economy’s fiscal strength.

Tyler Durden

Tue, 12/05/2023 – 07:43

via ZeroHedge News https://ift.tt/gn4eyB6 Tyler Durden