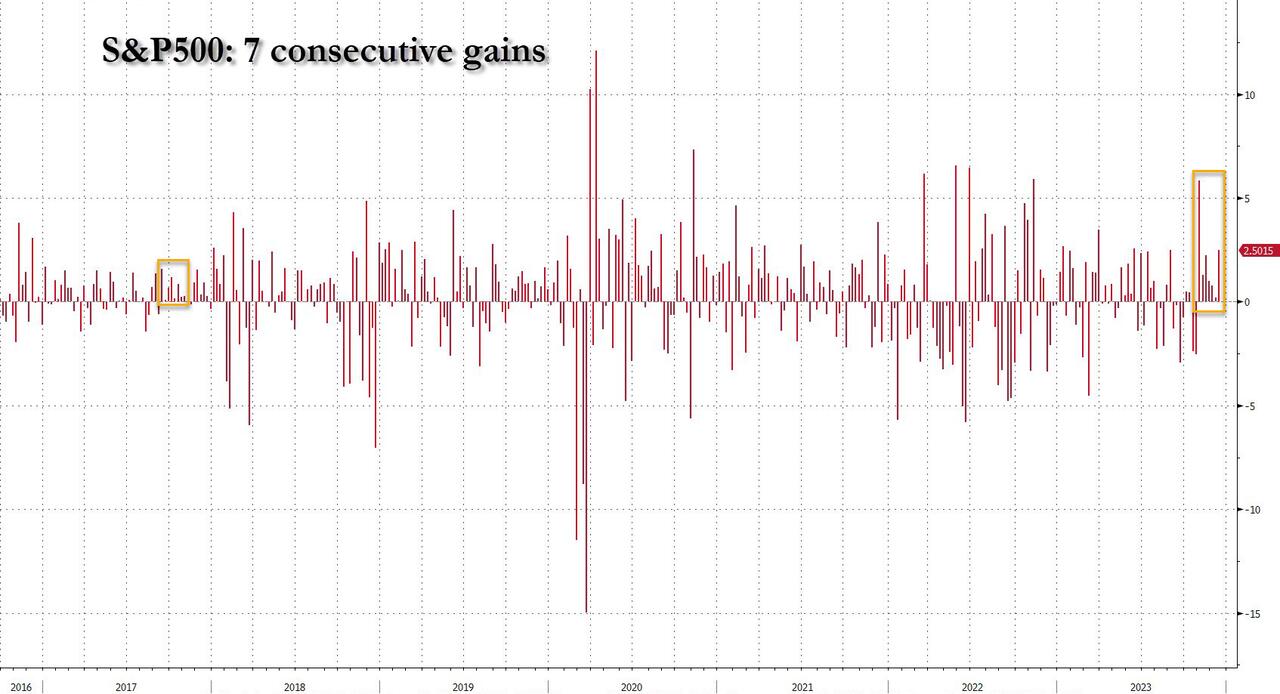

S&P Poised For 7th Weekly Gain As Futures Gain Ahead Of $4.9 Trillion Quad-Witching

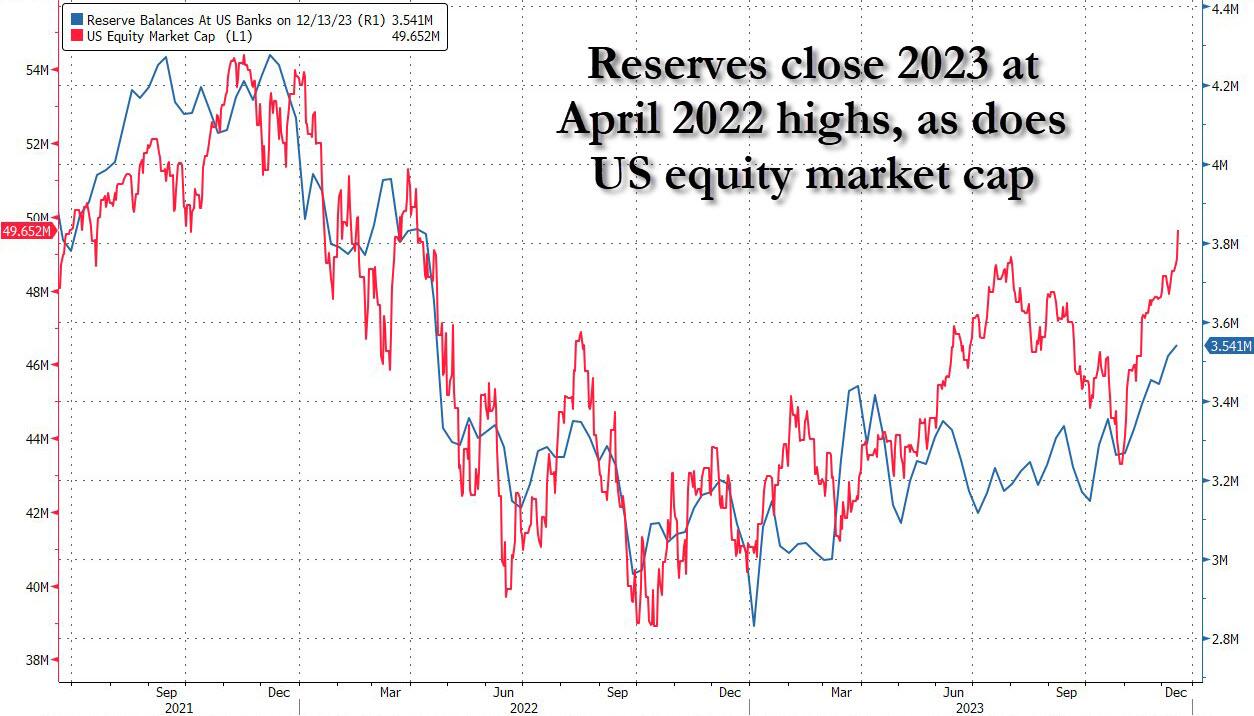

2023 is almost in the history books (the last two weeks of December are usually a volumeless, skeleton crew formality), and the S&P is set to close out the year just shy of all time highs hit in January 2022, largely thanks to the dovish Fed pivot this week and to a relentless buildup (well ahead of said pivot) in Fed reserves which are also closing out the year at 2023 highs…

… and are set for 7 consecutive gains in a row, the longest such stretch since 2017.

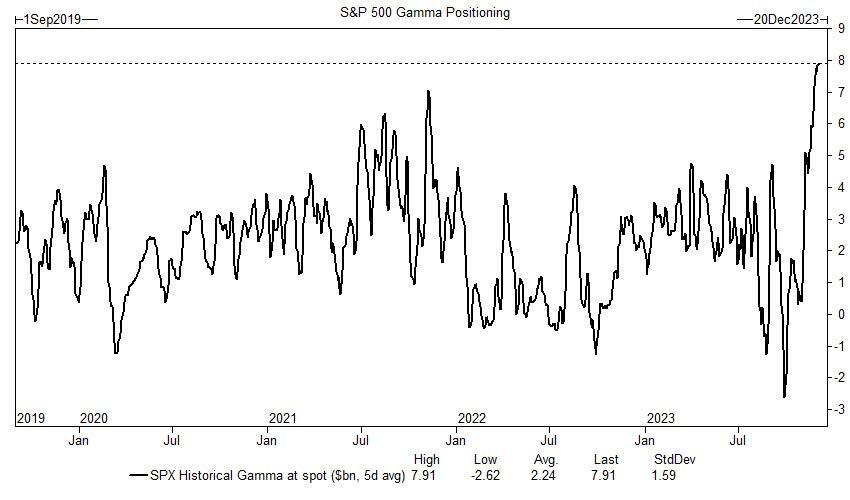

S&P futures are up 0.2% as of 7:50am, although today’s smooth meltup sailing is anything but assured as today we see a record $4.9 trillion option expiration quad witching…

… one which will promptly cancel out the record $8 billion in dealer gamma, which has served as rock-solid gamma gravity over the past two weeks, resulting in a potential spike in volatility.

Treasuries were steady after the yield on the 10-year benchmark broke below 4% for the first time since August. The dollar traded in tight range against Group-of-10 peers. In company news, Citigroup is shutting down its municipal business, meaning most of the relevant sales, trading and banking staffers will be leaving in the coming months. Today’s key macro events include industrial production and capacity utilisation for November, along with the Empire State manufacturing survey for December and the latest TIC data release.

In premarket trading, Intel rose 2.3%, looking set to extend recent gains, after the world’s biggest maker of PC processors unveiled new chips for personal computers and data centers as it seeks to break into the lucrative AI hardware space. Here are some other notable movers:

- Costco gains 2.8% after reporting earnings per share for the first quarter that beat the average analyst estimate.

- First Solar rises 2.7%, Enphase gains 3.1% and Sunrun is up by 3.6% after Jefferies initiates a slew of US solar stocks as the broker starts to see tailwinds and a turnaround in performance for the sector.

- Independence Realty Trust falls 2.2% and Camden Property Trust is lower by 0.8% following downgrades from BMO. Analysts cited concerns over new supply in many of the apartment REITs’ markets.

- Rocket Lab USA shares rise as much as 15% after the SpaceX rival blasted off for space for the first time since its September failure.

The Fed ignited a speculative frenzy this week when it affirmed speculation it’s ready to declare victory on inflation and shift to rate cuts without a significant cost to the economy. US equity funds clocked a ninth week of inflows, taking in $25.9 billion, the longest streak since Dec. 2021, according to BofA’s Michael Hartnett.

“The pivot is pretty distinct and the Fed is now talking about rate cuts,” Wei Li, global chief investment strategist at BlackRock, said in an interview with Bloomberg TV. “We’re now keen to really think about the selective opportunities that we can take advantage of, as we think about the year that is going to be characterized by rate cuts.”

A note of caution from Europe’s central bankers that they’re not ready to follow the Fed’s policy pivot damped some of the excitement. European Central Bank Governing Council member Madis Muller said Friday that markets are getting ahead of themselves in betting that the ECB will start cutting interest rates in the first half of next year. Yesterday ECB President Christine Lagarde said the bank had not discussed rate cuts at all.

“The contrast between the resilient US economy adopting a dovish stance and faltering European economies holding on to a hawkish position gives the impression that something is amiss,” Ipek Ozkardeskaya, a senior analyst at Swissquote, wrote in a note to clients.

European stocks are on course to log a fifth consecutive week of gains, boosted by expectations of looser monetary policy in 2024 despite that – unlike the Fed – ECB policymakers yesterday pushed back further on dovish expectations, urging patience and data-dependence before any rate reductions emerge. The Stoxx 600 rises 0.5% to its highest since January 2022, led higher by mining and auto shares. Here are some of Europe’s biggest movers today:

- Trainline shares rise as much as 22% to hit a one-year high following the UK government’s decision to abandon plans to create a rival rail ticketing platform. Barclays upgraded the stock.

- STMicroelectronics shares gain as much as 2.6% in Paris to the highest since August as Citi names the chipmaker as a top pick in Europe’s tech hardware sector.

- H&M shares gain as much as 1.4%, in line with the wider Stockholm stock market, after the Swedish fast-fashion retailer reported 4Q sales figures that analysts say were in line with expectations.

- Inchcape rises as much as 2.7% to a two-month high after BNP Paribas Exane said the automotive stock’s valuation does not reflect its growth potential.

- Atos shares gain as much as 20% after Le Figaro reports Airbus is in advanced talks to buy the French IT services firm’s big data and cybersecurity (BDS) activities.

- Sectra shares jump as much as 17%, the most since Sept. 2021, after the Swedish medical imaging and cybersecurity firm reported an increase in 2Q net sales and operating profit.

- Symrise shares fall as much as 10% after the company posted a profit warning due to inventory writedowns and FX impacts.

- Santander Bank Polska leads a retreat in Polish lenders after the country’s financial regulator published dividend rules for 2024 limiting the maximum payout to 75% of profits.

- Campari shares fall as much as 5.9% after the Italian drinks maker agreed to pay at least $1.2 billion for Courvoisier Cognac, a brand that Jefferies described as “dusty and unloved.”

Earlier in the session, Asian stocks gained, led by advances in Hong Kong after China’s central bank stepped up support for the economy by adding $112 billion of cash into the financial system. The MSCI Asia Pacific Index rose as much as 1.1% to the highest level since early August, with Tencent, Alibaba and BHP among the biggest boosts. Benchmarks in Hong Kong climbed more than 3% after the People’s Bank of China offered a record amount of cash via its medium-term lending facility. Mainland equities also gained. In a further positive, authorities late Thursday relaxed homebuying curbs in Beijing and Shanghai. A batch of data released Friday showed China’s economic recovery remains patchy, putting more pressure on the government to roll out supportive policies to fuel growth.

- Hang Seng and Shanghai Comp were varied with notable outperformance in the Hong Kong benchmark amid tech strength although the mainland lagged after mixed Chinese data in which Industrial Production topped estimates but Retail Sales disappointed despite showing double-digit percentage growth, while House Prices continued to decline and attention was also on the PBoC which maintained its 1-year MLF rate at 2.50% but delivered a record net injection through the facility.

- Japan’s Nikkei 225 was lifted at the open and briefly returned to above the 33,000 level amid the global risk-on mood.

- Australia’s ASX 200 was led higher by the commodity-related sectors after gains in oil and metal prices which helped the index shrug off the latest flash PMIs from Australia which slightly improved but remained in contractionary territory.

- Key stock gauges in India rise, on pace for their record closing highs, driven by a rally in the country’s information technology stocks. The S&P BSE SENSEX Index rose 1.4% to 71,490.13 as of 3:15 p.m. Mumbai time, while the NSE Nifty 50 Index advanced 1.3% to 21,467.80 A gauge of technology stocks on the BSE gains as much as 4.2%, taking its two-day gains to 7.6%

In FX, the euro underperforms, falling 0.3% versus the greenback. The pound rises 0.2% after UK companies reported their strongest growth in six months. Emerging-market currencies and stocks rose on Friday as investors’ appetite for riskier assets soared after the Federal Reserve sent dovish signals this week. The South African rand led gains among its peers as it advanced as much as 1.2% against the dollar to trade at the strongest since August. The Hungarian forint dropped most in emerging markets after the country blocked the European Union’s planned financial aid package for Ukraine.

In rates, treasuries are mixed with front-end and belly holding small gains after plying narrow ranges during Asia session and European morning. Long-end lags, steepening 5s30s spread by ~2bp. Treasury 10-year yields around 3.915%, ~1bp richer on the day, trailing bunds in the sector by ~6bp following European PMIs. Gilts also outperform Treasuries despite stronger-than-forecast UK services PMI. Bunds jumped after euro area PMI data missed estimates, raising the risk that the region may experience a recession in the second half. German 10-year yields fall 9bp to 2.03%. US session includes manufacturing data and comments by Fed’s Williams at 8:30am New York time.

In commodities, oil was set to post its first weekly gain in almost two months as the Fed’s latest stance triggered a bullish pulse across markets. WTI rose 0.5% to trade near $72. Spot gold also rose, adding 0.3%

Looking to the day ahead now, and data releases include the global flash PMIs for December, and in the US there’s industrial production and capacity utilisation for November, along with the Empire State manufacturing survey for December and the latest TIC data release. Central bank speakers include the ECB’s Holzmann, Centeno, Vasle, Kazimir, Muller, Scicluna, Simkus and Vujcic, along with BoE Deputy Governor Ramsden and Bank of Canada Governor Macklem.

Market Snapshot

- S&P 500 futures up 0.3% to 4,734.00

- MXAP up 1.0% to 165.58

- MXAPJ up 1.2% to 515.85

- Nikkei up 0.9% to 32,970.55

- Topix up 0.5% to 2,332.28

- Hang Seng Index up 2.4% to 16,792.19

- Shanghai Composite down 0.6% to 2,942.56

- Sensex up 1.2% to 71,347.18

- Australia S&P/ASX 200 up 0.9% to 7,442.69

- Kospi up 0.8% to 2,563.56

- STOXX Europe 600 up 0.3% to 478.09

- German 10Y yield little changed at 2.06%

- Euro down 0.3% to $1.0960

- Brent Futures up 0.4% to $76.88/bbl

- Gold spot up 0.3% to $2,041.46

- U.S. Dollar Index up 0.13% to 102.09

Top Overnight News

- China’s economic data was mixed for Nov, with strong industrial production (+6.6% vs. the Street +5.7% and up from +4.6% in Oct) but relatively soft retail sales (+10.1% vs. the Street +12.5% and up from +7.6% in Oct). BBG

- China will target a 2024 fiscal deficit of 3%, lower than the 3.8% objective for this year, although additional fiscal support could come from off-budget debt. RTRS

- China ramps liquidity via the MLF (the net injection was CNY800B, “the biggest monthly increase on record”) but keeps rates unchanged at 2.5%. RTRS

- The EU has failed to agree a critical €50bn financial aid package to Ukraine after Hungary’s Prime Minister Viktor Orbán vetoed the proposal, throwing into doubt Europe’s ongoing support to Kyiv. FT

- The euro-area dipped deeper into contraction, with Germany and France hit particularly hard. Private-sector activity unexpectedly worsened this month, PMIs show, raising the risk of a recession. ECB speakers echoed Christine Lagarde’s pushback on rate cuts, with Francois Villeroy saying the bank will be patient. BBG

- The EU is set to extend its truce with the US over steel tariffs imposed by Donald Trump until after presidential elections next year. FT

- Fed QT is feeding angst in overnight funding markets over whether officials are misjudging how far it can shrink its balance sheet without causing dislocations. The Fed said it will slow or halt reductions to make sure reserves remain “ample,” but markets participants said it’s unclear what that level is. BBG

- Jan Marsalek, the jet-setting former COO of now-defunct Wirecard, enabled Moscow to fund covert operations around the world, officials say; ‘whiff of Silicon Valley’. WSJ

- Blackstone and CPPIB won a $1.2 billion stake in a portfolio of commercial-property loans from the failed Signature Bank. BBG

- Trading in call options surged to an all-time high during the Fed-fueled stock rally Thursday. Around 43 million calls changed hands, Cboe Global Markets data showed. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly higher after the positive handover from Wall St where sentiment remained underpinned amid encouraging data and as yields continued to decline following the recent dovish Fed pivot, while the region also digested mixed Chinese activity data. ASX 200 was led higher by the commodity-related sectors after gains in oil and metal prices which helped the index shrug off the latest flash PMIs from Australia which slightly improved but remained in contractionary territory. Nikkei 225 was lifted at the open and briefly returned to above the 33,000 level amid the global risk-on mood. Hang Seng and Shanghai Comp were varied with notable outperformance in the Hong Kong benchmark amid tech strength although the mainland lagged after mixed Chinese data in which Industrial Production topped estimates but Retail Sales disappointed despite showing double-digit percentage growth, while House Prices continued to decline and attention was also on the PBoC which maintained its 1-year MLF rate at 2.50% but delivered a record net injection through the facility.

Top Asian News

- PBoC conducted CNY 1.45tln in 1-year MLF lending with the rate kept unchanged at 2.50% for a net injection of CNY 800bln.

- China stats bureau spokesperson said China’s economy recovers as macro policy effects kick in but added that domestic demand is still not sufficient and the economic recovery needs further consolidation. Furthermore, the spokesperson said China is to increase the intensity of macro policies and full-year development targets are expected to be achieved, while short-term adjustments in the property sector are said to be conducive for the stable and sound development of the sector in the long run.

- China is likely to set the 2024 GDP growth target at around 5% and is to target a budget deficit of 3% of GDP in 2024 vs. a revised ratio of 3.8% for 2023, while it may issue off-budget special bonds if the economy requires extra fiscal support, according to Reuters sources.

- China’s MOFCOM said it determined that restrictive trade measures taken by Taiwan against it constitute trade barriers and stated that Taiwan’s restrictive trade measures have caused negative impacts on relevant mainland industries and enterprises. Taiwan’s government later stated they can talk anytime if China is sincere and that issues can be dealt with under WTO mechanisms as both are WTO members, while Taiwan’s government also said China’s trade barrier probe does not accord with the facts and called on China to stop politicking.

- Nio (NIO/ 9866 HK) President says tariffs from EU probe into subsidies for China-made EVs would affect sales forecasts and investments

European equities, Eurostoxx50 (+0.3%), are building on yesterday’s gains; though the FTSE 100 (-0.1%) marginally lags weighed on by losses in heavyweight AstraZeneca (-1.9%) European sectors have a strong positive bias; Automobiles & Parts and Basic Resources are the clear outperformers, with the former seemingly benefitting from broad-based gains within the sector, alongside strength in Renault on a buyback update; Chemicals underperform, hampered by Symrise (-9.2%). US equity futures are entirely in the green, having traded mixed in yesterday’s session; the RTY (+0.9%) continues to outperform.

Top European News

- ECB’s Muller says it is still a little early to celebrate victory over inflation; still a little bit to go to reach 2% inflation, and its still too early to talk about near-term rate cuts, according to Bloomberg. Adds, markets are a bit optimistic if they see cuts in H1.

- ECB’s Holzmann says there was no discussion on rate cuts at yesterday’s meeting; Majority said there are risks to the upside on inflation; Majority are focus on core inflation; When questioned on whether the ECB is at terminal, the chance has increased but there is a remaining chance that they haven’t.

- ECB’s Villeroy says they want to express a message of confidence and patience at the December meeting. Change to the inflation outlook was the important signal; Will bring inflation back to target by 2025; Policy transmission is slightly faster than initially expected; Next policy move should be a lowering of rates “unless surprises”

- ECB’s Vasle says the current policy rate is to help return inflation to 2%

- UBS now expects ECB to deliver its first rate cut in April (prev. June)

- EU is to extend the trade truce with the US until after the presidential election, according to FT.

- Bundesbank Forecasts: HICP: 2023 6.1%; 2024 2.7%; 2025 2.5%; 2026 2.2%; GDP: 2023 -0.1%; 2024 0.4%; 2025 1.2%; 2026 1.3%

- CBRT Survey (Dec): Repo Rate seen at 36.65% (prev. survey 37.01%), USD/TRY seen at 29.6229 (prev. 29.9961), 12-month CPI seen at 41.23% (prev. 43.94%). End-2023 CPI seen at 65.39% (prev. 67.23%). End-2023 GDP growth seen at 4.2% (prev. 4.1%).

FX

- The Dollar is firmer intraday as a function of the softer EUR post-PMIs, whilst the index attempts to trim the hefty post-Fed losses after the ECB and BoE struck a less dovish tone than their US peer.

- Antipodeans are bid intraday largely a factor of commodities gains after a higher-than-expected Chinese Industrial Output metric.

- EUR on a softer footing amid dismal Flash PMI data whereby France and Germany fell deeper into contraction territory, though labour unit cost pressures remain a concern.

- PBoC set USD/CNY mid-point at 7.0957 vs exp. 7.1132 (prev. 7.1090).

Fixed Income

- USTs are a touch firmer on the session having moved in tandem with the EGB reaction and only paring slightly from their 112.22 peak on the Gilt move, which itself is 6 ticks shy of the contract best.

- EGBs are bid across the board with initial contained performance giving way to an approach of the contract high after the morning’s Flash PMI data for December.

- Gilts were initially bolstered by the EZ figures, but then trimmed on the regions own strong PMI data with Services continuing to prop up the economy and crucially with wage pressures still evident.

Commodities

- WTI Jan and Brent (+0.7%) Feb futures hold a modest positive bias, in line with the broader risk tone, with prices also underpinned by firmer Chinese Industrial Output overnight.

- Metals trade on a firmer footing, with spot gold holding a mild positive bias keeping its sight on the USD 2,050/oz level to the upside; Base metal futures are firmer across the board after the Chinese Industrial Output data topped forecasts and reignited demand optimism for the sector.

- Commerzbank says OPEC+ production cuts are likely to keep the oil market in balance at the start of next year despite weaker demand; For WTI, expects price of USD 75/bbl at the end of the first quarter; USD 85/bbl in H2’24

- Commerzbank sees a further price increase to USD 2150/oz for Gold in H2’24; Silver price increase to USD 30/oz by end 2024; Sees further significant upside for Copper and price recovery to USD 9200/t over the course of the year; Sees aluminium around USD 2,800/t next year.

- Qatar reportedly sells February-loading cargoes at discounts and lowest levels in years, according to Reuters sources.

Geopolitics

- Israel reportedly told Washington intensive raids and the large-scale ground operation will be completed within two or three weeks, according to Al Jazeera via social media platform X.

- Yemen’s Houthis said it carried out an operation against a Maersk cargo ship on its way to Israel and that it targeted the ship with a drone after the ship’s crew refused to respond to calls from Yemeni naval forces. Furthermore, US Central Command said a ballistic missile was fired from the Houthi-controlled area of Yemen towards the international shipping lane north of Bab-El-Mandeb Strait on Thursday but there were no injuries or damage from the ballistic missile attack.

- US President Biden’s administration sent messages to the Houthi rebels in Yemen via several channels recently warning them to stop their attacks on ships in the Red Sea and against Israel, according to Axios.

- US President Biden and Turkish President Erdogan discussed the importance of strengthening the NATO alliance including the importance of welcoming Sweden as an ally. Biden expressed support for recent constructive steps in the relationship between Turkey and Greece, while they discussed efforts to increase humanitarian assistance to Gaza and protect civilians and the need for a political horizon for Palestinians, according to the White House.

- EU agreed to open accession talks with Ukraine, while it was separately reported that Hungary’s PM Orban said Ukraine’s membership in the EU is a bad decision and that talks continue on the modification of the budget.

- Hungary held up the deal on EUR 50bln of financing for Ukraine and EU leaders postponed the discussion to January. Furthermore, Dutch PM Rutte said he is fairly confident the EU can reach a breakthrough early next year on Ukraine financing and the EU budget revision, according to Reuters.

- Japan is to ban imports of Russian diamonds for non-industrial use and will impose new sanctions on Russia-related groups and individuals, according to the Foreign Ministry.

- Guyana and Venezuela agreed to continue dialogue on pending matters related to the territorial dispute and to avoid conflict escalation, while the sides agreed to meet again in Brazil to continue dialogue over border issues, according to St Vincent’s PM.

- UKMTO has received reports of an incident in the vicinity of Hodeideah, Yemen

- US Officials say there is an almost complete halt in ship access to Israel’s Eilat port, via AJA Breaking citing Axios

US Event Calendar

- 08:30: Dec. Empire Manufacturing, est. 2.1, prior 9.1

- 09:15: Nov. Industrial Production MoM, est. 0.3%, prior -0.6%

- Nov. Manufacturing (SIC) Production, est. 0.5%, prior -0.7%

- Nov. Capacity Utilization, est. 79.1%, prior 78.9%

- 09:45: Dec. S&P Global US Services PMI, est. 50.7, prior 50.8

- 09:45: Dec. S&P Global US Manufacturing PM, est. 49.5, prior 49.4

- 16:00: Oct. Total Net TIC Flows, prior -$67.4b

DB’s Jim Reid concludes the overnight wrap

This is my last EMR of 2023. Many thanks for reading and interacting this year and happy holidays to you and your family if you’re celebrating. Henry will be carrying on the EMR for most of next week so it’s only good bye from me. We have a 14 hour car journey today to the Alps and I still can’t hear due to the ear infection in both ears so it’s not going to be one packed with enlightening conversation. At this rate I’ll be put in the rear with poor Bronte. As it’s my last of the year I’ll add my favourite TV series of 2023 at the end. Regular readers know that I try to carve out 45-60 minutes every night when I’m home to watch TV with my wife. The last week has been with subtitles due to the above. By the way I’ve seen two of the worst films I’ve ever seen relative to the hype this year. Namely “Everything everywhere all at once” and “Barbie”. Perhaps the second one wasn’t aimed at me.

Everything everywhere all at once was a good description of the last 24 hours as there were several stories operating in parallel when it came to markets, albeit slightly less confusing in nature than those in that film. On one level it was more of the same from recent weeks, with the massive rally continuing and the 10yr Treasury yield closing (3.92%) beneath 4% for the first time since July. Indeed, we’ve seen one of the sharpest 2-day declines in real yields since the height of the Covid pandemic (-42.9bps for the 5yr). Moreover, the S&P 500 (+0.26%) closed less than 2% from its all-time high last year, with the small cap Russell 2000 (+3.52% and +2.72% over 2-days) moving into bull market territory, having now risen by +22.2% from its low on October 27.

So there was undoubtedly a lot of good news. But after the wave of euphoria following the Fed meeting, neither the ECB nor the BoE offered the same dovishness with their own decisions, which led markets to row back a bit on the chances of aggressive rate cuts next year. Then we had another batch of decent US data, which led to further questions about how soon the Fed would be able to cut rates. So even though expectations are still far more dovish than before the Fed’s decision, yesterday saw a mild pushback, albeit nothing that was able to break the astonishing market rally we’ve seen into year-end.

Starting from the top, the day began with the dovish narrative in the ascendancy, with European bonds seeing a massive rally at the open as they caught up with the Fed’s decision the previous day. And then in the morning, the Swiss National Bank kept rates on hold and dropped the wording in their statement about possible future hikes. But then we heard from the Bank of England, who struck a much less dovish tone in their own statement. Specifically, they held rates at 5.25%, and three of the nine members on the committee were still in favour of another 25bp hike. The statement also said that monetary policy would “need to be sufficiently restrictive for sufficiently long”, so there wasn’t an equivalent nod to rate cuts like we had from the Fed. Governor Bailey himself pushed back on market expectations, saying that “we are more cautious because we need to see those more persistent elements of inflation, which we see in things like services prices, turn in the right direction quite decisively .”

Shortly afterwards, the ECB then announced their own decision, where they kept rates on hold as widely expected. But as with the BoE, they didn’t echo the more dovish stance from the Fed, and President Lagarde said that “we should absolutely not lower our guard” and that “we did not discuss rate cuts at all”. Alongside that, the ECB also announced that they would reduce the PEPP portfolio by €7.5bn per month on average over H2 2024, and discontinue reinvestments under PEPP by year-end 2024 .

Nevertheless, the ECB did acknowledge the better inflation picture, dropping the wording from previous statements that inflation was set “to stay too high for too long”. Their latest forecasts also expect weaker inflation, with headline inflation now seen falling to 2.7% in 2024 (vs. 3.2% in September ). Looking further out, they even saw inflation falling below target to 1.9% in 2026, but core inflation was still seen at 2.1% then. But even with the downgrades, our European economists see the updated inflation forecasts as too high, with a meaningful downgrade likely by the March meeting. They see the hawkish tilt of yesterday’s meeting as reducing the risk of the ECB cutting as soon as March, but retain their view of rate cuts starting in April with 150bp of cuts by the end of next year. See their reaction note here.

Despite the more hawkish tones from the ECB, sovereign bond yields still fell in Europe yesterday, as the impact of the Fed’s dovishness at the open outweighed Lagarde’s remarks. For instance, yields on 10yr bunds (-6.4bps) initially fell as low as 2.02% intraday, before recovering to end the session at 2.11%. That was echoed elsewhere, with yields on 10yr OATs (-7.0bps) and gilts (-4.6bps) both closing at their lowest in months. The largest yield decline came for BTPs (-13.9bps), as the delayed and gradual reduction in PEPP reinvestments was favourable for sovereign spreads. The Fed’s impact was evident across other asset classes too, as the STOXX 600 (+0.87%) closed at a 22-month high, and the iTraxx Crossover (-24.4bps) saw its biggest daily move tighter since March .

Whilst central banks helped to push back on the European yield moves, the rally in US Treasuries showed little sign of stopping yesterday. Indeed, the 10yr Treasury yield was down a further -9.5bps to 3.92%, though they did rise slightly during the latter half of the US session, having traded as low as 3.88% near the European close, and this morning they’re up another +2.2bps to 3.94%. The 10yr real yield saw an even larger decline of -13.9bps, which builds on the move after the Fed meeting, and brings the 2-day decline to -34.4bps in the 10yr real yield. So this is a substantial easing in financial conditions, and US HY spreads (-29bps) are also at their tightest since April 2022, whilst Bloomberg’s index of US financial conditions is now at its most accommodative this morning since the Fed began hiking rates in early 2022 .

That optimism carried over into other risk assets, with the S&P 500 (+0.26%) posting a 6th consecutive advance, which left the index at a fresh all-time high in total return terms. It also means the index is still on track for a 7th consecutive weekly advance, which would be the first time that’s happened since 2017. Small-cap stocks led the gains, with the Russell 2000 advancing +2.72%, following on from its +3.52% gain the previous day. So maybe some rebalancing going in the small caps’ favour after the FOMC. Tech stocks posted ‘only’ a slight increase (NASDAQ +0.19%), while banks were an outperformer within the S&P 500, up +4.15%.

The risk-on mood was also positive for commodities, with the Bloomberg commodity index (+2.27%) posting its strongest daily gain in over a year, whilst oil prices (Brent +3.16% to $76.61/bbl) are now on course to avoid an 8th consecutive weekly decline .

Whilst that was happening, we had another round of positive data on the surface from the US. For instance, retail sales surprised on the upside in November, with the headline number up +0.3% (vs. -0.1% expected). However downward revisions meant that retail control (which feeds into GDP) netted out in line with expectations. Back to the positives, weekly initial jobless claims fell back to 202k over the week ending December 9 (vs. 220k expected). Next stop will be the December flash PMIs today from the US and Europe, which are one of the last major pieces of data before Christmas. Overnight the initial releases have shown signs of improvement from November, with Japan’s composite PMI back into expansionary territory at 50.4, whilst Australia’s composite PMI picked up to 47.4, from 46.2 last month.

Equity markets in Asia have continued the positive momentum overnight, as the PBoC offered commercial lenders a net 800bn yuan of 1yr loans. However, the data from China has been a bit more mixed, with industrial production up +6.6% year-on-year in November (vs. +5.7% expected), whilst retail sales were beneath consensus at +10.1% year-on-year (vs. +12.5% expected). Against that background, the H ang Seng (+2.18%) is leading gains in the region, with the Nikkei (+0.76%) and the KOSPI (+0.70%) also posting a strong advance. However, the CSI 300 (-0.15%) and the Shanghai Composite (-0.39%) have both lost ground. Looking forward, US equity futures are pointing to modest gains, with those on the S&P 500 (+0.06%) and the NASDAQ 100 (+0.09%) both advancing.

To the day ahead now, and data releases include the global flash PMIs for December, and in the US there’s industrial production and capacity utilisation for November, along with the Empire State manufacturing survey for December. Central bank speakers include the ECB’s Holzmann, Centeno, Vasle, Kazimir, Muller, Scicluna, Simkus and Vujcic, along with BoE Deputy Governor Ramsden and Bank of Canada Governor Macklem.

Tyler Durden

Fri, 12/15/2023 – 08:19

via ZeroHedge News https://ift.tt/uV8xmBp Tyler Durden