Preview Of The Fed’s “Pivot” Minutes: How Much Pushback?

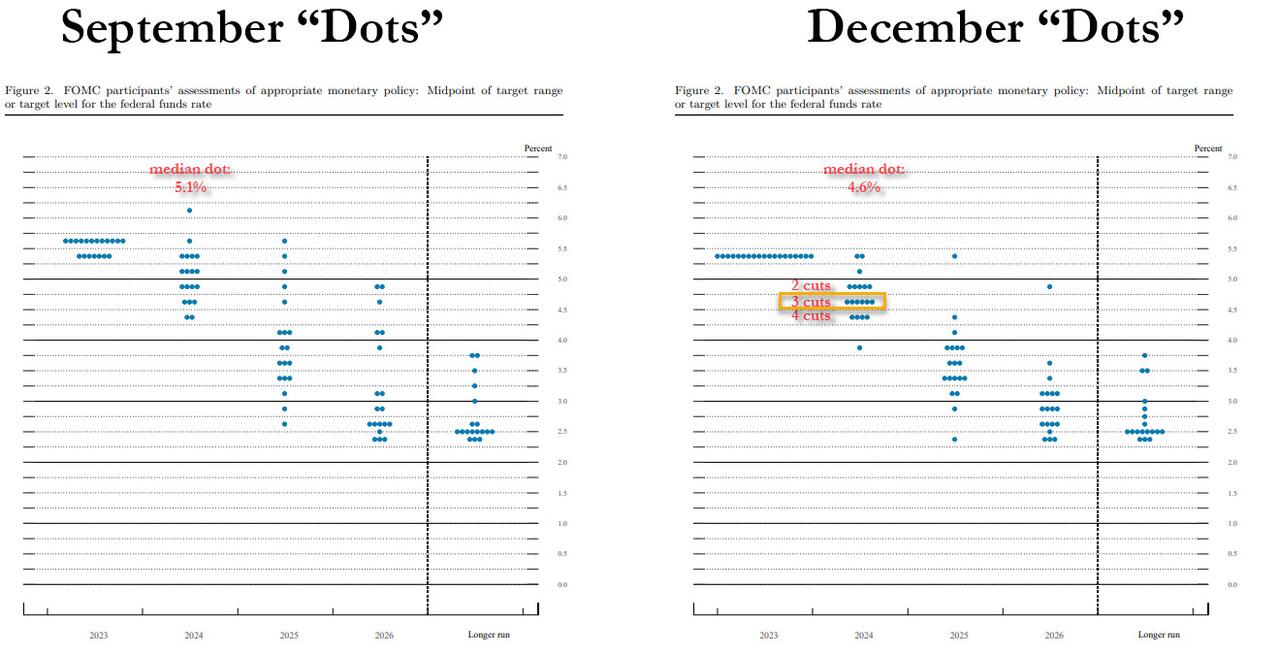

Today’s minutes from the Fed’s memorable December “Dovish Pivot” FOMC will be eyed to view the Fed’s true appetite on rate cuts in 2024 after the 2024 dot plot in the SEP implied three rate cuts from current levels throughout the year.

And, as Newsquawk writes in its Fed Minutes preview, Powell and Waller have sounded somewhat dovish, which has seen money markets price in 150bp of cuts throughout the year, more than the 75bp of cuts implied by the Fed’s median SEP.

Below we excerpt the highlights from the report:

-

Fed speakers have attempted to dial back these expectations since the latest Fed meeting, with Williams and Mester both noting the focus is still on determining whether policy is in the right place.

-

Although the median dot looks for the target level for the FFR at 4.6% by the end of 2024 (currently 5.4%), the range of the dot plots was wide with eight participants pencilling a rate above 4.6% and five penciling a rate beneath that level.

As a result, the minutes will be viewed by the market to gather more information on the FOMC’s thinking, but it is worth noting the minutes will only incorporate the information up to the latest meeting, therefore any development since the December 13th meeting, i.e. even more dovish market pricing, cooler than expected November PCE, cooler than expected Final Q3 GDP and the attempted pushback on market pricing from the FOMC, will not be incorporated.

Fed December Statement & SEP: The Fed left rates unchanged at 5.25-5.5%, made dovish tweaks to its statement, whilst indicating a greater fall than many had expected to its Fed rate projections. The 2024 median rate dot was lowered to 4.6% from the prior 5.1%, beneath the analyst consensus 4.9%, indicating three cuts from current levels in 2024 – the uncertainty remains high, however, with eight out of 19 officials forecasting rates above the median and five beneath it with a forecast range of 3.9–5.4%. The 2025 median Dot was dropped to 3.6% from 3.9%, whilst the 2026 and long run dots were left unchanged at 2.9% and 2.5%, respectively, bucking some expectations for an upward drift in the longer run (‘neutral’) estimate. The lower rate projections were reflective of faster progress than previously anticipated for inflation, with the Core PCE projections falling to 3.2% from 3.7% for 2023, to 2.4% from 2.6% in 2024, and to 2.2% from 2.3% for 2025. The unemployment rate forecasts were unchanged through 2025 (4.1% in both 2024 and 2025), while the 2024 GDP forecast nudged lower to 1.4% from 1.5% in 2024. The statement saw its tightening guidance softened, “In determining the extent of ANY [new word] additional policy firming that may be appropriate…”, whilst it also maintained its language added in November describing financial and credit conditions as tighter, despite some expectations that it would be removed after a rally in USTs and stocks since then. It noted growth had slowed from the strong pace in Q3 (prev. expanded at a strong pace in Q3), while it also added that inflation has eased over the past year, but maintained language it remains elevated.

Fed Speak: Powell’s Press Conference and Q&A were notably dovish, noting policymakers think they have done enough on rates and it is not likely the Fed will hike further.

-

When asked, Powell said the topic of rate cuts are starting to come into view and they are now a topic of discussion with the FOMC, adding there was a general expectation that rate cuts would be a topic of conversation going forward.

-

Powell acknowledged they had seen real progress on core inflation, whilst saying they had made reasonable progress in non-housing services inflation, he also acknowledged the rise in real rates as inflation declines, stating the Fed is very conscious of real rates and is a part of how it thinks about things.

-

Waller had also noted before the December meeting that there are good economic arguments that if inflation was to continue falling for several more months, then the Fed could lower the policy rate.

However, with the markets now pricing 150bp of cuts throughout 2024, much more aggressive than what the Fed SEP’s imply, Fed speakers since the December blackout period have been notably more hawkish, in what seems to be an attempt to dial back market pricing after a dovish Powell, cool PCE and cool GDP report.

-

Williams said that the Fed is not really talking about rate cuts right now and that the question is have they got monetary policy to sufficiently restrictive levels and the Fed will be thinking about this for some time.

-

Bostic said rate cuts are not an imminent thing, but he has instructed staff to begin developing possible principles and thresholds to guide the rate cut process.

-

Mester said that markets are “a little bit ahead” of the Fed on rate cuts, while she also echoed Williams in saying that the next phase is not when to reduce rates, it is about how long policy should remain restrictive.

-

Goolsbee also acknowledged that the market has gotten ahead of itself, but if inflation keeps coming down, the Fed can consider how restrictive it is.

-

Harker said the Fed will not cut rates right away, the job on controlling inflation is not done but things are looking better for the inflation outlook.

Tyler Durden

Wed, 01/03/2024 – 12:45

via ZeroHedge News https://ift.tt/yEGhxJm Tyler Durden