Futures Slide As Earnings Season Begins, Oil Surges After US Strikes Houthi Rebels In Yemen

US equity futures are muted on the last day of the week, as investors mull the impact of inflation’s rebound on the outlook for monetary easing and waited for earnings from some of the world’s biggest banks. At 6:54am, S&P 500 futures are down -0.5%, dragged lower by poor earnings reported by BofA with JPM fallilng in sympathy, while Nasdaq 100 futures fell 0.6%. 10Y Yields rose to 3.99% and was set to rise above 4.00% after sliding yesterday for reasons still unknown. The dollar reversed earlier losses and was last trading near session highs.

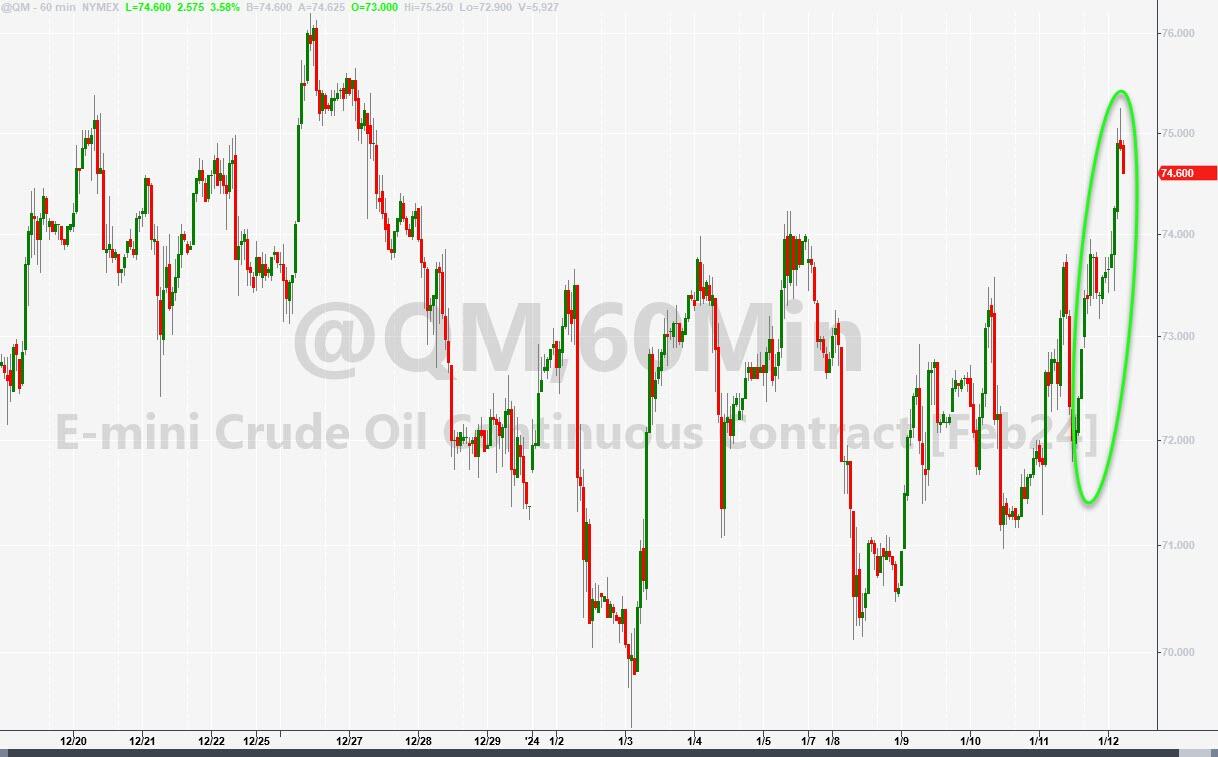

Brent futures jumped as the US and UK retaliated against Houthi rebels in Yemen for attacks on ships in the Red Sea. The allies launched more more than 60 airstrikes on Houthi targets in Yemen early Friday. In response, Houthis vowed more ship attacks, potentially engulfing the region into a larger conflict. The threat of a wider war in the Mideast and new hotspots of political turmoil in Ecuador and Poland are complicating an otherwise bullish outlook for markets in 2024.

In premarket trading, Tesla fell in premarket on disruption at its German factory due to the Red Sea unrest and price cuts in China. Cryptocurrency stocks extend declines after the first US exchange-traded funds for Bitcoin went live on Thursday, with $4.6 billion worth of shares exchanged in the first day of trading. Bakkt -2%, Bitdeer Technologies -3.8%, Cipher Mining -5.1%, Cleanspark -2.3%, Coinbase -1.9%, Marathon Digital -2.1%, Riot Platforms -2.4%, Terawulf -3.1%. Here are some other notable premarket movers:

-

International Flavors & Fragrances (IFF US) shares rise 2% after it was raised to buy from hold at Jefferies, which says that the new CEO change “finally” positions IFF for several years of “sustainable structural improvement.”

-

Twilio shares gain 2.4% after it was raised to overweight from neutral by Piper Sandler with the analyst saying that the spending environment will rebound in 2024.

Expectations that officials are done hiking and will ease policy in 2024 — even if that happens a little later than markets are pricing — remain in place after faster-than-expected US inflation data on Thursday. The European Central Bank President Christine Lagarde said once the bank’s 2% inflation goal comes into view she’s “very confident, then rates will start to decline.”

“The downside reaction to the hot CPI figure was a lot more benign than it likely would have been if we had seen a cool number – a very telling sign of positioning and the sheer amount of cash sloshing around in the system and waiting to be put to work,” FAB Global Markets economists including Simon Ballard wrote in a note.

Earnings season gets underway on Friday, with some of the biggest US banks including JPMorgan Chase, Bank of America, Citigroup and Wells Fargo & Co. set to report fourth-quarter results.

European stocks are also on the front foot with the Stoxx 600 rising 0.9% buoyed by energy companies TotalEnergies SE and Shell Plc, and set to notch a small weekly gain. Here are the biggest movers on Friday:

-

Airbus rises as much as 2.4% to hit a new record high after the airplane manufacturer sold a record number of planes in 2023 and surpassed its annual delivery target.

-

Bureau Veritas shares rise as much as 4.3%, the most since October 2022, after Morgan Stanley upgraded its rating to overweight and named the company its new sector top pick.

-

Arkema rises as much as 2% after Morgan Stanley resumed coverage at equal-weight.

-

Vistry Group rises as much as 3.3% after the UK housebuilder said annual adjusted pretax profit in 2023 will be ahead of expectations and broadly flat from the year before.

-

AMS-Osram rises as much as 5.6% after Bernstein raises its rating on the chipmaker to outperform.

-

Wood Group rises as much as 3.7% after the engineering services company revealed trading in 2023 has been in-line with expectations and will lead to increases in annual Ebitda.

-

J.Martins drops as much as 7.1% as 4Q sales raised analysts concerns about like-for-like deceleration in Poland, its main market.

-

Grifols extends weekly declines and is 36% down since the publication on Tuesday of a short-seller report, the worst weekly drop on record for the Spanish blood plasma company.

-

Burberry dropped as much as 15% in huge volumes to their lowest levels since 2020 as the UK luxury group unexpectedly lowered its profit forecast after weak sales in December.

-

Suedzucker fall as much as 6.6% to the lowest intraday in over a year, as Barclays says peak sugar profitability is likely over and Warburg downgrades the stock to sell.

-

Lanxess falls as much as 2.6% after Morgan Stanley cut the stock to underweight from equal-weight.

-

Ceres falls as much as 7.1% after RBC cut the recommendation on the energy generator and distributor to underperform, citing delays hitting cash reserves and stalling sector momentum.

Earlier in the session, Asian stocks rose, on track for a weekly gain, as a rally in Japan extended and investors took hotter-than-expected US inflation data in stride. The MSCI Asia Pacific Index climbed as much as 0.6%, with Infosys and Fast Retailing among the biggest boosts after results reports. Data showing accelerated growth in US headline prices was seen having limited impact on Federal Reserve policy.

-

Benchmarks in Japan continued their ascent to fresh three-decade highs, while stocks in India also gained.

-

China and Hong Kong gauges were little changed after data showing the world’s second-largest economy continues to struggle with deflation, as consumer prices dropped for a third-straight month.

-

Key stock gauges in India closed at new record highs, outperforming most Asian peers, driven by a sharp rally in technology companies. The S&P BSE Sensex rose 1.2% to 72,568.45 in Mumbai, while the NSE Nifty 50 Index advanced 1.1% to 21,894.55. The MSCI Asia Pacific India was up 0.5% for the day.

In rates, bunds and gilts rise with German and UK 10-year yields both falling 6bps. US 10-year yields rise 1bps to 3.97%.

In FX, the Bloomberg Dollar Spot Index is little changed. The Norwegian krone is the best performer among the G-10 currencies, rising 0.4% versus the greenback. The pound falls 0.1% despite data showing UK GDP rose slightly more than expected in November. Crude-price gains filtered through to commodity-linked currencies including the Canadian dollar and Norwegian krone.

In commodities, oil prices jump after the US and UK launched more than 60 airstrikes on Houthi targets in Yemen, in a bid to stop the Iran-backed group’s shipping attacks in the Red Sea. Brent climbs 3.4% to hit $80 while WTI tops $74 a barrel. Spot gold rises 0.6%.

Bitcoin, -0.5%, takes a breather and holds just shy of USD 46k, while Ethereum, +0.5%, continues to build on the prior day’s advances as attention shifts now to the upcoming Ether ETF.

Looking to the day ahead now, and data releases include US PPI for December, along with UK GDP for November. From central banks, we’ll hear from the ECB’s Lane and the Fed’s Kashkari. Finally, there are several earnings releases today, including JPMorgan Chase, Citigroup, Bank of America and BlackRock.

Market Snapshot

-

S&P 500 futures little changed at 4,818.25

-

STOXX Europe 600 up 0.9% to 477.17

-

MXAP up 0.6% to 167.50

-

MXAPJ up 0.2% to 512.25

-

Nikkei up 1.5% to 35,577.11

-

Topix up 0.5% to 2,494.23

-

Hang Seng Index down 0.4% to 16,244.58

-

Shanghai Composite down 0.2% to 2,881.98

-

Sensex up 1.2% to 72,607.15

-

Australia S&P/ASX 200 down 0.1% to 7,498.28

-

Kospi down 0.6% to 2,525.05

-

German 10Y yield little changed at 2.19%

-

Euro little changed at $1.0967

-

Brent Futures up 2.4% to $79.25/bbl

-

Brent Futures up 2.4% to $79.25/bbl

-

Gold spot up 0.5% to $2,039.48

-

U.S. Dollar Index little changed at 102.31

Top Overnight News

-

China CPI -0.3% (vs. the Street -0.4% and a tiny improvement from -0.5% in Nov) while exports rose 2.3% (vs. the Street +1.5% and an uptick from +0.5% in Nov) and imports inched up 0.2% (vs. the Street -0.5%), although the PPI is still deeply in deflationary territory (down 2.7% vs. the Street -2.6%). BBG

-

China’s M2 money supply growth came in at +9.7% in Dec, down from +10% in Nov and below the Street’s +10.1% forecast. New CNY loans and aggregate financing in Dec came in light too at CNY1.17T (vs. the Street CNY1.35T) and CNY1.94T (vs. the Street CNY2.16T), respectively. BBG

-

Tesla cut the price of both its locally made models in China, potentially setting the stage for further discounting by rivals. Shares fell premarket. Citi analysts slashed their price target for BYD on expectations that sales and profit margins will come under pressure. BBG

-

The US and UK launched joint airstrikes against Houthi targets in Yemen after a spate of attacks on merchant vessels in the Red Sea. President Biden left the door open to more and the Houthis vowed to continue their attacks. Brent jumped to $80, the highest in two weeks, and WTI surpassed $75. BBG

-

The Panama Canal drought conditions have led shipping giant Maersk to inform clients this week that vessels with freight from Oceania (Australia and New Zealand) will no longer traverse the canal because of the ongoing low water levels. Maersk will be servicing the client’s containers by using a “land bridge.” CNBC

-

TSLA will suspend most production at its plant in Germany from 1/29 to 2/11 due to Red Sea-related component shipment disruptions. RTRS

-

BAC -3% in the pre: miss on weaker revenues – FICC modestly weaker and consensus likely not including the $1.6b of BSBY cessation impact. Roughly inline NII while NIM was weaker 1.97% vs cons 2.04% and deposit costs grew to 1.82% in the qtr. Core expenses at the ~$15.6b they guided to. Net reserve releases in the print while NCOs went up on card. Capital declined to 11.8% from 11.9%. TBV grew to $24.46 or implying stock trading at 1.35x of TBV. We think most important driver of the stock today will be the ’24 NII guide which we are likely to get on the call. GS GBM

-

BlackRock agreed to buy private-equity firm Global Infrastructure Partners for $12.5 billion in cash and stock, its largest acquisition in 15 years. WSJ

-

UNH -4% on very light volume in the pre-mkt after a pretty significant MLR miss (1.13% above expectations). Q4 revenue and EPS both modestly above estimates. Conference call at 8:45 ET. Will be back with more details. Q4 MLR 85% vs 83.87%. Q4 EPS $6.16 vs $5.97 est. Q4 revenue $94.43B vs $92.11B. Managed Care will be under pressure today as a result. GS GBM

-

BOJ officials are likely to discuss cutting their forecasts for economic growth and a gauge of inflation that includes energy when they gather to set policy later this month, even as their overall assessment of price trends remains intact, according to people familiar with the matter. The officials will probably mull a downward revision to the outlook for consumer prices excluding fresh food to around 2.5% from 2.8% for the fiscal year starting in April due to a drop in oil prices, the people said. For the following fiscal year, they continue to expect the gauge to be a tad lower than the bank’s 2% target. BBG

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed with the major indices mostly rangebound alongside geopolitical concerns after the US and UK conducted joint strikes on Houthi targets, while participants also digested Chinese inflation and trade data. ASX 200 was subdued as strength in commodity-related sectors was offset by weakness in defensives. Nikkei 225 continued to rally and is up over 6% this week with gains helped by strong earnings from top-weighted Fast Retailing. Hang Seng and Shanghai Comp struggled for direction despite the latest Chinese trade data which either improved or topped forecasts although 2023 USD-denominated exports contracted for the first time since 2016, while the Chinese inflation figures were mixed but ultimately deflationary on a Y/Y basis. US equity futures (ES -0.2%) were contained after whipsawing post-CPI, while participants also await big bank earnings. European equity futures are indicative of a higher open with Euro Stoxx 50 future +0.7% after the cash market closed lower by 0.6% yesterday.

Top Asian News

-

China’s Customs said China’s 2023 exports and imports of goods are better than expected but noted complexity and uncertainty of the external environment are expected to rise in 2024, while it added more efforts are needed to improve China’s trade stabilisation in 2024.

-

Chinese Foreign Minister Wang Yi held a call with his Canadian counterpart and said the current difficult situation in China-Canada relations is not what China wants to see but added that China is open to contacts and dialogue with Canada. Wang noted the fundamental reason why relations have fallen to a low point in recent years is that there has been a serious deviation in Canada’s perception of China and he hopes the Canadian side will interpret China’s domestic and foreign policies objectively, rationally and correctly.

-

Japanese government is reportedly mulling issuing a deficit-covering bond worth JPY 500bln as a source of funding to double budget reserves to JPY 1tln for FY24 for earthquake relief, according to Reuters citing TV Tokyo.

-

BoJ policymakers see the economy making progress towards meeting the threshold for ending negative rates, though they are divided on how long they should wait, according to Reuters sources and recent BoJ minutes.

-

European Commission investigators are to visit Chinese EV names within China in the coming weeks, via Reuters citing sources; as part of a subsidies probe, could result in tariffs. BYD (1211 HK), Geely (0175 HK), SAIC (600104 CH).

European equities, Stoxx600 +0.8%, are firmer across the board, having started the session in the green and continue to build on strength throughout the session. European sectors have largely been dictated by geopolitics and the Burberry update; Industrials leads after the US and UK conducted a joint strike against Houthi targets. Luxury hampered by Burberry cutting guidance. Burberry (BRBY LN) -9.3% now expect FY results to be below the prior guidance. “The slowdown in luxury demand is having an impact on current trading”. Reminder; Richemont reports next Thursday. US equity futures are mixed with the NQ (-0.2%) incrementally lagging, paring back some of the mild outperformance seen yesterday; focus broadly on upcoming earnings metrics.

Top European News

- Goldman Sachs cuts the UK’s 2024 GDP growth forecast to 0.5% (prev. 0.6%)

FX

-

DXY is marginally firmer though within contained parameters of 102.17-40. USD in consolidation mode as CPI failed to have a lasting impact, PPI next.

-

EUR is steady vs. the USD with EUR/USD failing to breach 1.10 after printing a high of 1.0999 yesterday; a deluge of option expiries will be in focus 1.0920-25 (1.2BLN), 1.0940-50 (1.5BLN), 1.0975-80 (1.3BLN),1.0990-1.1000 (2.1BLN),1.1050-55 (2BLN).

-

JPY is lingering around the 145 mark as it looks for some respite from yesterday’s USD/JPY rally which took the pair to 146.41. JPY relatively unreactive to BoJ sources in which it sees the economy making progress towards criteria for ending negative rates.

-

Antipodeans are benefitting from the favourable risk environment. AUD/USD back on a 0.67 handle but chart formation still one of consolidation.

-

PBoC set USD/CNY mid-point at 7.1050 vs exp. 7.1592 (prev. 7.1087).

-

Peru Central Bank cut its reference rate by 25bps to 6.50%, as expected, while it stated the rate cut does not necessarily imply a cycle of successive reductions to the interest rate and that annual inflation is expected to reach the target range in the next months.

Fixed Income

-

USTs around unchanged in a narrow nine tick range ahead of PPI and Fed’s Kashkari (2026 Voter), though in the meantime US focus will likely be on the commencement of bank earnings; benchmarks dipped slightly following BoJ sources.

-

Bunds are bid despite more contained UST action, fleeting pressure around a JGB auction and a lessening of the magnitude of China’s deflation. Likely deriving support from the escalation in geopolitical tensions overnight between UK/US & Houthis.

-

Gilts were unreactive to November GDP and largely trading in tandem with core EGB peers. Inched above Thursday’s peak to a current 100.60 best, but nine ticks shy of the WTD best.

Commodities

-

Crude is markedly firmer as geopolitical risk premium continues to be woven in after yesterday’s events near the Strait of Hormuz, with reports overnight that the US and UK conducted a joint airstrike against Houthi rebel targets; Brent around USD 80.10/bbl, at session highs.

-

Precious metals post mild gains whilst the Dollar remains rangebound amid heightened geopolitical tensions in the Middle East; Base metals are mostly firmer with participants citing expectations of a rate cut in China to support the economy.

Geopolitics

-

US and UK conducted a joint strike against Houthi targets in Yemen which targeted Houthi radar, air defence sites, weapon storages and launch sites. US and allies released a joint statement that Yemen strikes were intended to disrupt and degrade the capabilities the Houthis use to threaten global trade, while their aim remains to de-escalate tensions and restore stability in the Red Sea but will not hesitate to defend lives and protect the free flow of commerce in one of the world’s most critical waterways in the face of continued threats.

-

US President Biden said US military forces together with the UK and with support from Australia, Bahrain, Canada and the Netherlands successfully conducted strikes against targets in Yemen used by Houthi rebels and the strikes were a direct response to Houthi attacks against international maritime vessels in the Red Sea, while he added that they will not hesitate to direct further measures.

-

US senior official said Houthi actions present a threat to the US and the entire world, while the official added there is no intent to escalate the situation after strikes on Houthi targets and that US and British forces in the Red Sea remain well prepared to defend themselves following the Yemen strikes. Furthermore, they believe Iran has been involved in every phase of Houthi attacks and that they hold Iran responsible for the role it has played in attacks against US forces.

-

Yemen’s Houthis spokesman said there is no justification for the US-UK attack on Yemen and the targeting of ships heading towards Israel will continue. It was also separately reported that Iran strongly condemned the US-UK attack against Houthis and said it is a violation of Yemen’s sovereignty and territorial integrity.

-

Russian letter to Security Council members considers the use of force in Yemen a violation of the UN Charter, while Russia requested a UN Security Council meeting regarding the US-UK strikes on Yemen.

-

Saudi Arabia said it so closely monitoring with great concern the air strikes on Yemen and it emphasises the importance of maintaining the security and stability of the Red Sea, while it called for restraint and avoiding escalation in light of the events taking place in the region.

-

US military said Iranian-backed Houthis fired an anti-ship ballistic missile into international shipping lanes in the Gulf of Aden on Thursday but there were no injuries or damage reported from the attack.

-

Houthis says “All US-British interests have become legitimate targets in response to aggression”, according to Sky News Arabia

-

US Secretary of State Blinken said the State Department is imposing sanctions on three Russian entities and one individual involved in the transfer and testing of North Korea’s ballistic missiles for Russia’s use against Ukraine.

-

China’s Military says they will always maintain the highest level of vigilance and “smash” any form of “Taiwan independence” separatist plot, according to the Chinese Defence Ministry

US Event Calendar

-

08:30: Dec. PPI Final Demand MoM, est. 0.1%, prior 0%

-

08:30: Dec. PPI Final Demand YoY, est. 1.3%, prior 0.9%

-

08:30: Dec. PPI Ex Food and Energy YoY, est. 2.0%, prior 2.0%

-

08:30: Dec. PPI Ex Food and Energy MoM, est. 0.2%, prior 0%

Central Bank Speakers

-

10:00: Fed’s Kashkari Speaks at Regional Economic Conditions Conference

DB’s Jim Reid concludes the overnight wrap

Geopolitical risks are in focus again for markets, as overnight the US and the UK carried out air strikes against the Houthi rebels in Yemen, which follows the Houthi attacks on commercial shipping in the Red Sea. In a statement from US President Biden, he said that he would “not hesitate to direct further measures to protect our people and the free flow of international commerce as necessary.” In response, oil prices have risen further overnight, with Brent Crude up +2.05% this morning to $79.00/bbl, which follows on from its +0.79% increase yesterday.

Clearly, the focus will now be on whether this might lead to any escalation in the Middle East, but for now the impact on asset prices more broadly has proven contained, and futures on the S&P 500 are only down -0.14% this morning. Nevertheless, several shipping stocks have advanced in Asia, and even before the strikes overnight, we’d already seen a significant rise in freight costs as a result of the attacks in the Red Sea. This was something we discussed in our CoTD yesterday (link here), since freight costs had already doubled from their levels in November, so this is an important story for global inflation more broadly.

Before the overnight news, yesterday had brought some interesting price action in markets after the latest US CPI print. On the one hand, the print delivered an upside surprise, which added to fears that getting inflation back to target will be bumpier than many hoped. But even as inflation breakevens moved higher, suggesting that investors are conscious of this risk, real yields fell back and we saw futures price in a growing chance that the Fed are set to cut rates as soon as March. Indeed, the probability of a cut by the March meeting is now up to 73% this morning, up from around 70% just before the CPI print. And the moves came despite comments from Cleveland Fed President Mester that March was “probably too early” for a rate cut. So this is going to set up an important few weeks when it comes to upcoming data releases, as the divergence between market pricing and commentary from Fed officials is raising questions as to whether markets are once again too confident about a dovish pivot from the Fed, which is a pattern we’ve seen multiple times over the last couple of years.

In terms of the details of that inflation print, monthly headline CPI was a tenth stronger than expected at +0.3%, which in turn pushed the year-on-year number up to +3.4%. Meanwhile for core CPI, it also came at +0.3% for the month, which was in line with expectations, but meant the year-on-year number only slowed by a tenth to +3.9% (vs. +3.8% expected). So the progress on disinflation is proving slower than hoped, and that’s also evident by just focusing on the last 6 months of data. For instance, on a 6-month annualised basis, core CPI was up from +2.9% to +3.2%, and headline CPI was up from +3.1% to +3.3%.

All that said, one of the factors pushing up inflation was shelter, which was running at +0.46% in December. But shelter takes up a much larger weight in the CPI index than it does in the PCE index, with the latter being the inflation measure that the Fed officially targets. We won’t get the PCE number for another couple of weeks, but in November it was already running at 2.6% year-on-year, half a point below the CPI print at 3.1%. With shelter inflation still running at elevated levels, it’s plausible that you could end up with a larger wedge between the two, with the PCE indicators looking better on a relative basis, which would offer the Fed greater justification to cut rates. As part of that, it’ll be worth looking out for today’s PPI reading, as some of the measures there will provide an indication about some of the larger components for core PCE, like healthcare and portfolio management.

Even with the upside surprise on the CPI, investors grew in confidence that the Fed are likely to cut rates soon, and yesterday saw the likelihood of a cut by March rise to 78% by the close (from 68% the day before). Similarly, the amount of cuts priced in by the December meeting actually went up by +14.0bps to 155bps, so that’s still a reasonably rapid pace of cuts for the year as a whole, and one that tends to be more consistent with what happens in a recession rather than continued growth. Indeed, we pointed out in Tuesday’s chart of the day (link here) that there’s historically been a high hurdle to cutting that much without a recession. The shift in pricing occurred despite Cleveland Fed President Mester saying that “I think March is probably too early in my estimate for a rate decline because I think we need to see some more evidence”. Later on though, others left the decision more open, with Richmond Fed President Barkin saying that he didn’t wish to “prejudge” a decision about March, whilst Chicago Fed President Goolsbee said that “I don’t like tying our hands”.

With investors still expecting near-term rate cuts, Treasuries rallied across the curve on the day, despite selling off initially after the CPI print. The 2yr yield fell -11.3bps on the day to 4.25%, having traded as high as 4.39% post-CPI. That was driven by lower real yields, however, as the 2yr inflation breakeven was actually up +2.7bps on the day to 2.15%, suggesting that the CPI print did have some impact on market expectations of inflation. Otherwise, the 10yr yield fell -6.2bps to 3.97%, with the 10yr inflation breakeven (+1.8bps) up to 2.24%. Over in Europe, yields on 10yr bunds (-0.8bps), OATs (-1.2bps) and BTPs (-3.8bps) all ended the day lower as well.

By contrast to the increased pricing of cuts in the US, the likelihood of March rate cut by the ECB inched down from 37% to 34% yesterday. This came amid comments from Croatia’s Vujcic, one of the more hawkish ECB voices, who said that he definitely wanted to see Q1 wage developments before considering rate cuts (which would effectively rule out a cut in March) and suggested that the market was optimistic on the timing of the first cut. In the evening, we heard from ECB President Lagarde who said that she “cannot give you a date” for rate cuts, adding that if data confirm the path of inflation back towards 2%, “then rates will start to decline as so as we have this certainty”.

Turning to equities, the US CPI report saw futures give up their initial gains, but there was a strong recovery over the US session, which meant the S&P 500 came back from an intraday low of -0.92%, to only close down -0.07%. That also leaves the index less than half a percent beneath its all-time closing high from January 2022. Small-cap stocks continued to struggle and the Russell 2000 (-0.75%) lost further ground. Meanwhile in Europe, where markets closed before the recovery later in the US session, the STOXX 600 (-0.77%) lost ground for a third consecutive day for the first time since October, which also left the index at its lowest in nearly a month.

Other data yesterday painted a resilient picture of the US economy, with the weekly initial jobless claims down to 202k (vs. 210k expected) over the week ending January 6. That’s their lowest level since October, and it also leaves the 4-week moving average at its lowest since October as well. Alongside that, the continuing claims for the week ending December 30 fell to 1.834m (vs. 1.87m expected), marking their lowest since October too.

Overnight in Asia, we’ve seen a mixed performance for equity markets, which comes as China’s consumer prices remained in deflationary territory. The latest CPI print showed prices fell by -0.3% year-on-year (vs. -0.4% expected), while the PPI reading came in at -2.7% (vs. -2.6% expected). Otherwise, equity markets have been mixed in Asia overnight, with the Hang Seng (-0.03%), the CSI 30 (-0.04%) and the Shanghai Comp (+0.09%) all broadly flat, whereas the Nikkei (+1.39%) is on track for its highest closing level since 1990. By contrast, the KOSPI is currently down -0.84% this morning, leaving it down -5.14% so far on a YTD basis.

To the day ahead now, and data releases include US PPI for December, along with UK GDP for November. From central banks, we’ll hear from the ECB’s Lane and the Fed’s Kashkari. Finally, there are several earnings releases today, including JPMorgan Chase, Citigroup, Bank of America and BlackRock.

Tyler Durden

Fri, 01/12/2024 – 07:20

via ZeroHedge News https://ift.tt/SQ8POzq Tyler Durden