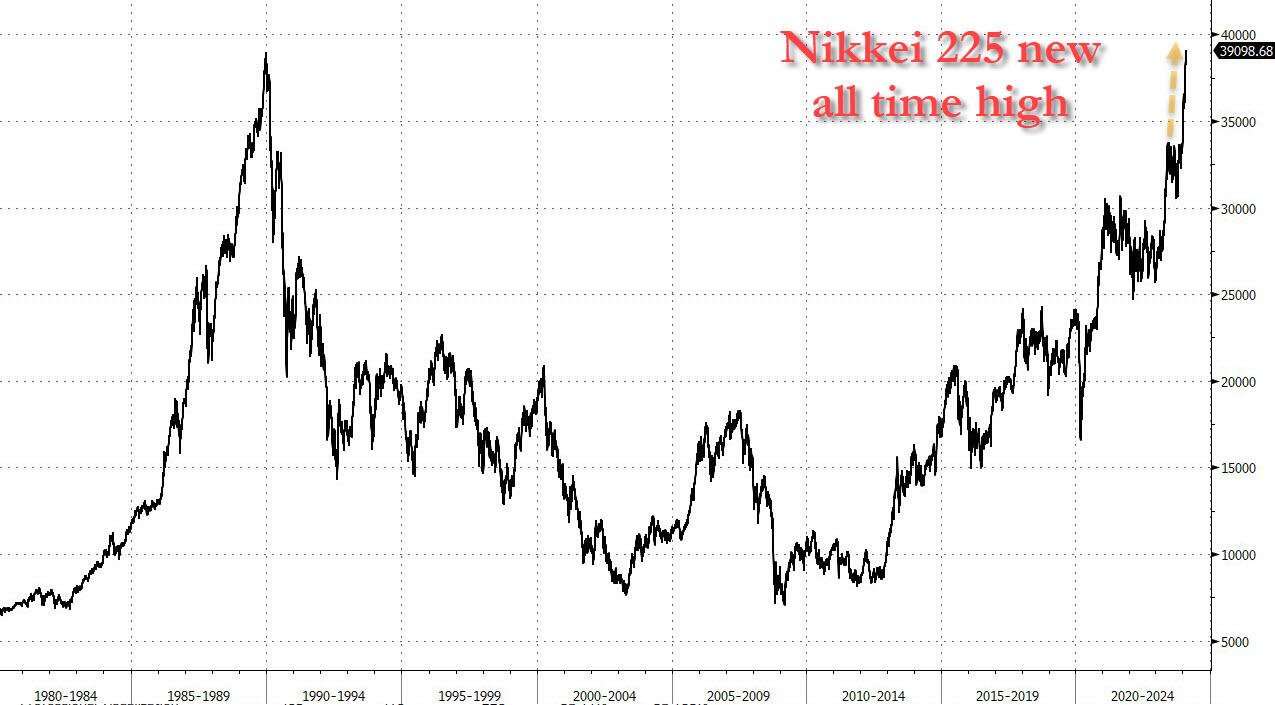

AIphoria: Nvidia Blowout Sends US Futures Soaring, Pushes Japan And Europe To New Record Highs

US equity futures blasted higher, and were set to push US the S&P500 to a new all time high when markets open for trading, matching record highs hit earlier in the session for both Japanese stocks…

… and European bourses…

… boosted by blowout earnings by Nvidia which surged in early trading after delivering another eye-popping sales forecast – it really was the $2BN delta between NVDA’s $24BN revenue forecast for the current quarter and the $21.9BN consensus estimate – that added fresh momentum to a stock rally that already made it the world’s most valuable chipmaker and fanned gains in tech stocks – and really all stocks – around the world. As of 7:40am S&P futures were higher by 1.3% on the day with Nasdaq futures outperforming and higher by 2.1% following Nvidia earnings which sent the stock up as much as 15%; in Europe, the Stoxx 600 hit a new all time high, rising 0.8% with Japan’s Nikkei also surpassing its December 1989 record high, and closing above 39K for the first time ever. Meanwhile, even as tech rocketed higher, yields continued their ascent, and the 10Y yield rose to a new 2024 high, while the dollar dipped and oil swung from gains to losses in a narrow range. Today’s calendar sees jobless claims (8:30am), February S&P US PMI’s (9:45am) and January existing home sales (10am) as well as several Fed speakers.

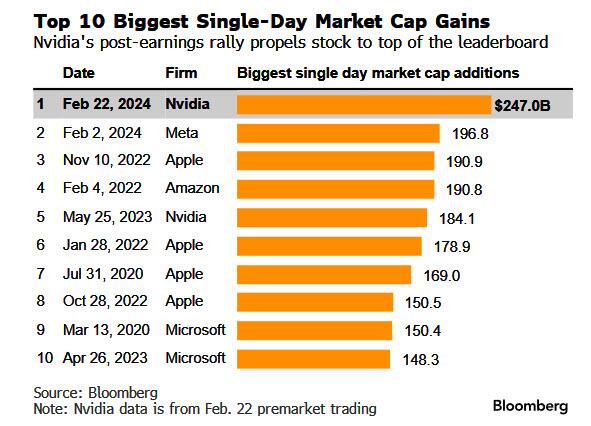

Naturally, all eyes are on Nvidia this morning which soared as much as 15% in pre-market trading after results showed demand continues to be strong for artificial intelligence computing hardware enabling extremely racist chatbots such as Google’s Gemini. The company, which will once again surpass Amazon and Alphabet in market value, has been the biggest driver of US stock market gains this year and has gained over $250BN premarket. And here is a stunning fact: the $250BN in market cap NVDA is set to gain today eclipses the previous record, that of Meta, which soared by $197BN just three weeks ago.

Nivida’s gain dragged other chipmakers higher in premarket trading, with Advanced Micro Devices Inc. climbing 6%, Applied Materials Inc. rising 4% and Intel Corp. up more than 2%. Here are some other notable premarket movers:

- B. Riley surged 35% after the embattled bank said internal review confirms that the company and its executives, including Bryant Riley, had no involvement with, or knowledge of, any of the alleged misconduct concerning Prophecy

- Carnival gains 5% as rival Royal Caribbean lifted its annual guidance. Royal Caribbean (RCL) +5%

- DigitalOcean jumps 9% after the provider of platform tools for start-ups posted 4Q revenue that beat estimates.

- DoorDash rises 4% as Morgan Stanley raises its rating, predicting robust growth.

- Enerplus ADRs gain 9% after Chord agreed to buy the Canadian oil and gas company for $3.7 billion in stock and cash.

- Etsy falls 9% after the e-commerce company’s outlook pointed to a slow start to the fiscal year, prompting Jefferies to cut its earnings estimate.

- Indivior ADRs jump 16% after the drugmaker reported upbeat results for the fourth quarter.

- Lucid Group sinks 8% after the electric vehicles maker forecast production for 2024 of about 9,000 vehicles, which analysts described as disappointing.

- Moderna Inc. gains 3% after the company reported fourth-quarter revenue that beat analysts’ expectations by gaining Covid vaccine market share on its rival, Pfizer Inc.

- Nvidia surges 13% after delivering another eye-popping sales forecast.

- Remitly soars 24% after the money transfer firm provided a year revenue forecast that topped estimates and a strong 4Q sales beat.

- Rivian falls 16% after the electric vehicle maker provided a disappointing forecast for 2024 production.

- Vertiv gains 5% with analysts noting strong order numbers for the data center equipment company.

Yet despite lots of activity elsewhere, this morning is all about AI (which apparently is raginly anti-white racist, forcing Google’s Bard or whatever it is called now, to pull all of its image generation altogether). The global market for generative AI may reach $1.3 trillion in 2032, according to estimates from Bloomberg Intelligence analyst Mandeep Singh. Explosive growth in the sector should boost hardware, software and internet companies again this year, he wrote in a recent report.

“As goes Nvidia, so goes the market,” said Kim Forrest, chief investment officer of Bokeh Capital Partners LLC. “It does confirm the narrative that AI is going to continue to be strong for the foreseeable future. This narrative supported the markets last year, why wouldn’t it do the same this year?”

The latest numbers mean Wall Street estimates for Nvidia are set to be revised higher, which will likely bring down the valuation once again if the share price doesn’t keep pace. While some investors have been concerned about a possible bubble forming around AI-related stocks, others noted that Nvidia is still less expensive than peers. The stock traded at about 30 times forward earnings as of Wednesday’s close, compared with AMD at 43 times. The shares are also cheaper than those of Amazon.com Inc. and Microsoft Corp., while the Nasdaq 100 Index trades at a 25 times multiple.

The hype around Nvidia’s earnings overshadowed a hawkish tone to the minutes of the Federal Reserve’s last policy meeting, where most officials expressed concern about the risk of cutting interest rates too soon. Fed Governor Lisa Cook and Minneapolis Fed President Neel Kashkari are set to speak today, providing investors with more food for thought along with jobs and home-sales data.

European stocks also benefited from the AIphoria, with the Stoxx 600 rising to a record high after Japan’s Nikkei 225 did the same earlier on Thursday. European semiconductor stocks rallied after Nvidia delivered another eye-popping sales forecast, as demand for chips to power AI algorithms shows no signs of letting up. Among European chip equipment makers, ASML rose as much as +5.1%. Here are some other notable premarket movers:

- Mercedes shares rise as much as 5.4% as the German carmaker’s gloomy earnings forecast was offset by its plan for an accelerated $3.2 billion buyback.

- Rolls-Royce gains as much as 9.4% after the UK aircraft engine maker reported strong earnings and guidance confirming its turnaround story, according to analysts at Jefferies.

- Marlowe shares jump as much as 39%, extending yesterday gains, after agreeing to sell some Governance, Risk & Compliance software and services assets to Inflexion Private Equity for an enterprise value of £430 million.

- Axa shares gain as much as 4% after its FY underlying profit beat the average analyst estimate, while the French insurer also vowed to return about €6 billion ($6.5 billion) of last year’s earnings to investors under a new payout policy.

- Indivior shares jump as much as 22% after the drugmaker reported upbeat results for the fourth quarter and provided outlook that was above consensus expectations at the mid-point.

- Delivery Hero shares fall as much as 10% on Thursday after the food delivery firm said negotiations to sell the Foodpanda business in some Southeast Asia markets have failed.

- Nestle shares drop as much as 5.3% after the food manufacturer posted “lackluster” full-year results amid significant currency headwinds, according to Vontobel. Morgan Stanley expects a downward revision to consensus EPS figures.

- ISS drops as much as 11% in Copenhagen as the cleaning and support services firm’s free cash flow guidance disappoints analysts. Stock is worst performer on Stoxx Europe 600 on Thursday.

- Hargreaves Lansdown shares slide as much as 8.9% after the wealth manager reported what analysts described as mixed first-half results.

Earlier in the session, Asian stocks gained as Nvidia’s better-than-expected revenue forecast sparked a rally in tech shares, helping Japan’s Nikkei 225 hit a new record. The MSCI Asia Pacific Index gained as much as 0.7% to its highest level since April 2022, with Toyota among the biggest boosts along with Nvidia suppliers TSMC and SK Hynix. Japan’s blue chip index surpassed its 1989 all-time high.

- Hang Seng and Shanghai Comp. were both firmer albeit with price action in Hong Kong choppy amid US-China chip-related frictions, while the mainland remained afloat after the latest stability efforts by China.

- Nikkei 225 outperformed amid tech strength and eventually printed fresh intraday record highs above 39,000.

- ASX 200 lagged as participants continued to digest an influx of earnings and after Australia’s Flash Manufacturing PMI returned to contraction territory.

- KOSPI was marginally higher after the BoK kept rates unchanged and signalled an unlikelihood of a cut soon.

- Indian stocks overcame a sell off in the preceding session to post their biggest single-day surge in three weeks with the biggest boost from automakers and software exporters. The S&P BSE Sensex Index rose 0.7% to 73,158.24 in Mumbai, the most since Jan. 31. The NSE Nifty 50 Index advanced by a similar measure to a new all-time high.

In FX, the risk-on mood has weighed on the greenback, with the Bloomberg Dollar Spot Index down 0.3% after edging lower in the last three days and looking at its first weekly fall of 2024. Minutes of the Fed’s Jan. 30-31 meeting flagged that policymakers were more concerned about the risks of moving too soon to cut interest rates than waiting too long; a view presaged by Fed Governor Michelle Bowman who said that the time for a rate cut was “Certainly not now.” A slip in the dollar is “probably a reflection of overall bullish sentiment, which has been given a boost after Nvidia,” said Kyle Rodda, a senior analyst at Capital.com. “Don’t overlook the China narrative, either. We’ve seen antipodeans a bit firmer over the last few days and I think stronger Chinese markets are having an impact at the margins”

In rates, treasury yields hit session highs with the long-end outperforming, flattening 2s10s and 5s30s spreads through Wednesday session lows. The 10Y yield traded at 4.33%, as treasury yields were richer by up to 3bps across long-end of the curve with front-end slightly cheaper on the day. Spreads including 2s10s, 5s30s are flatter by 2bp and 1.5bp, following similar bull flattening move seen across German curve. Core European rates are choppy following a round of services and manufacturing PMI’s data, while risk sentiment continues to be boosted by Nvidia surging in premarket trading after delivering stellar earnings after Wednesday’s close. US session focus includes jobless claims and PMI data, along with a busy Fed speaker slate. The dollar issuance slate is busy and includes BNG Bank 3Y; Cisco headlined a four-deal $19.4b slate for Wednesday, pushing weekly volume through $33b with more jumbo acquisition financing expected in the coming days. We algo get a $9b 30-year TIPS auction is scheduled for 1pm.

In commodities, oil prices advance, with WTI rising 0.5% to trade near $78.30. Spot gold adds 0.2%.

Bitcoin sits just shy of USD 52k, whilst Ethereum (+2.2%) edges higher and back towards USD 3k.

On today’s calendar, we get the January Chicago Fed national activity index, jobless claims (8:30am), February S&P US PMI’s (9:45am) and January existing home sales (10am). Federal Reserve members scheduled to speak include Jefferson (10am), Harker (3:15pm), Cook, Kashkari (5pm) and Waller (7:35pm)

Market Snapshot

- S&P 500 futures up 1.3% to 5,058.50

- STOXX Europe 600 up 0.6% to 493.87

- MXAP up 1.1% to 173.05

- MXAPJ up 1.0% to 528.53

- Nikkei up 2.2% to 39,098.68

- Topix up 1.3% to 2,660.71

- Hang Seng Index up 1.5% to 16,742.95

- Shanghai Composite up 1.3% to 2,988.36

- Sensex up 0.7% to 73,115.45

- Australia S&P/ASX 200 little changed at 7,611.20

- Kospi up 0.4% to 2,664.27

- German 10Y yield little changed at 2.46%

- Euro up 0.3% to $1.0850

- Brent Futures up 0.3% to $83.31/bbl

- Brent Futures up 0.3% to $83.31/bbl

- Gold spot up 0.1% to $2,028.84

- U.S. Dollar Index down 0.30% to 103.70

Top Overnight News

- As the annual meeting of China’s parliament approaches next month, its leaders are facing the greatest pressure in almost a decade to take bold policy decisions that safeguard the economy’s long-term growth potential. The start of the year saw Chinese stocks tumbling to five-year lows on growth concerns and deflation deepening to levels unseen since the global financial crisis, prompting comparisons with the 2015 turmoil that forced policymakers into action. RTRS

- South Korea’s central bank on Thursday joined its peers in the U.S. and Australia in seeking to hose down investors’ aggressive rate cut expectations after keeping interest rates at a 15-year high. “Most board members still see it as premature to discuss any interest rate cuts as inflation is above our target level and we need to check its slowdown path,” governor Rhee Chang-yong said in a news conference in Seoul. The Bank of Korea (BOK) kept interest rates steady at 3.50%, as expected by all 38 analysts polled by Reuters. RTRS

- The BOJ will pull the plug on its eight-year negative interest rate policy in April, according to more than 80% of economists polled by Reuters, marking a long-awaited major shift from a global outlier central bank. Nearly the same proportion of economists, 76%, also expect the BOJ to scrap yield curve control at that meeting, with almost all saying ultra-loose monetary conditions will end then, just months before many major central banks are expected to start cutting rates. RTRS

- European flash PMIs for Feb are mixed, with manufacturing dipping to 46.1 (down from 46.6 in Jan) while services climbed to 50 (up from 48.4 in Jan) and inflation pressures built (“overall rates of input cost inflation and selling price inflation accelerated in February to their highest since last May”). RTRS

- Benny Gantz, a member of Israel’s war cabinet, said that “preliminary signs” of progress have emerged on a deal to pause fighting in Gaza in exchange for the release of Israeli hostages. Without offering specifics, Mr. Gantz said there has been momentum on a new draft of the deal that indicates a “possibility to advance.” NYT

- US crude inventories surged by 7.2 million barrels last week, API data is said to show. That would take total holdings to the highest since November if confirmed by the EIA. Distillate supply fell, while gasoline stockpiles edged higher. BBG

- Ukraine has the right to strike “Russian military targets outside Ukraine” in line with international law, Nato Secretary-General Jens Stoltenberg has said, while acknowledging that Kyiv’s western suppliers of weapons have divergent stances on the issue. FT

- WMT has eased the delivery requirements for its suppliers, the latest sign of supply chain conditions normalizing back to pre-COVID levels. WSJ

- NVDA delivered another BIG beat and guide above, with Data Center once again serving as the key growth driver. Overwhelming consensus heading into the print was that we were going to get another BEAT & FADE (similar to what we got the last 2 qtrs)) Over the past 4 sessions, NVDA traded down -9% with the desk noting material derisking in NVDA & its AI / Momentum peer group… so, in retrospect, it seems like the “beat & fade” reaction may have been PULLED FORWARD. GS GBM

Earnings

- NVIDIA Corp (NVDA) – Q4 2024 (USD): Adj. EPS 5.16 (exp. 4.64), Revenue 22.1bln (exp. 20.62bln). Q1 25 revenue view 24bln plus or minus 2% (exp. 21.9bln). Revenue breakdown (USD). Data Centre revenue 18.4bln (exp. 17.21bln). Gaming revenue +58% y/y to 2.9bln (exp. 2.72bln). Professional Visualization revenue 463mln (exp. 435.5mln). Automotive revenue -4.4% Y/Y to 281mln (exp. 272.1mln). Other metrics ADJ gross margin 76.7% (exp. 75.4%). R&D expenses +26% Y/Y to USD 2.47bln (exp. 2.43bln). ADJ operating expenses +25% Y/Y to USD 2.21bln (exp. 2.23bln). ADJ operating income USD 14.75bln (exp. 13.14bln). Free cash flow USD 11.22bln (exp. 10.82bln). Commentary Generative AI has “hit the tipping point”. Data Center sales to China declined significantly in Q4 due to US government licensing requirements. Says has gotten requests for information from antitrust regulators in France, EU, UK and China over its sales of GPUs and efforts to allocate supply, while it expects to receive additional requests for information. CEO says demand far exceeds supply for next-generation products and cannot keep up with demand as we ramp. Says China represented mid-single-digit percentage of data centre revenue in Q4 due to USG licensing requirements and sees it to be in a similar range in Q1 (Newswires) Shares +13% in pre-market

- Anglo American (AAL LN) – FY (USD): Revenue 30.7bln (exp. 30.8bln). Adj. Net 2.90bln (exp. 2.81bln). Adj. EBTIDA 9.96bln (exp. 9.76bln). Basic EPS 2.42 (exp. 2.33). Cuts FY dividend to 0.41 (prev. 0.74, -45% Y/Y). COMMENTARY “There is no doubt that while the immediate macro picture presents some challenges for our PGMs and diamonds businesses, the demand trends for metals and minerals have rarely looked better.” “Our updated assessment of global GDP growth and consumer demand were the main factors behind our USD 1.6bln write-down of our book value of De Beers, principally relating to goodwill.” Anglo American secures additional multi-billion tonne high quality iron ore resource at Minas-Rio. Shares +3.4% in European trade

- Rolls Royce (RR/ LN) – FY (GBP): Revenue 16.49bln (exp. 14.82bln). FCF 1.285bln (prev. 505mln). Operating Margin 10.3% (prev. 5.1%). Sees 2024 FCF 1.7-1.9bln (exp. 1.37bln). Co. sees further improvement to all mid-term targets. Shares +7.9% in European trade

- Mercedes-Benz (MBG GY) – Q4 (EUR): Revenue 40.26bln (exp. 38.61bln). Sees 2024 Cars Adj. Return on Sales between 10-12% (exp. 11.3%); Free cash flow of the industrial business seen slightly above the prior-year level. COMMENTARY: Group EBIT is expected to be slightly below the previous year’s level resulting in divisional guidances. Mercedes-Benz Cars will seek to defend and hold pricing at 2023 levels. Index Weightings: DAX 40 (4.01%), Euro Stoxx 50 (1.6%), Stoxx 600 (0.5%) Shares +4.7% in European trade

- AXA (CS FP) – FY23 (EUR): Revenue 102.7bln (exp. 105.5bln), Net 7.19bln (exp. 7.45bln). Co. announces a share buyback of up to EUR 1.6bln. Co. increased main financial targets for 2024-2026. Targeting a total payout ratio of 75%, comprising a 60% dividend payout ratio and an additional 15% from annual share buy-backs. Dividend +16% Y/Y to EUR 1.98/shr. Co. announced a new strategic plan dubbed “Unlock the Future”. (AXA) Index Weightings: CAC 40 (3.3%), Euro Stoxx 50 (1.8%), Stoxx 600 (0.6%) Shares +2.4% in European trade

- Nestle (NESN SW) – FY23 (CHF): Revenue 92bln (exp. 94.04bln). Organic Revenue +7.2% (exp. +7.4%). Dividend 3 (exp. 3.08). Real Internal Growth -0.3% (exp. +0.08%). Sees 2024 organic revenue around +4% (exp. +4.91%). OUTLOOK 2024 outlook: “We expect organic sales growth around 4% and a moderate increase in the underlying trading operating profit margin. Underlying earnings per share in constant currency is expected to increase between 6% and 10%.” 2025 mid-term targets fully confirmed: mid-single-digit organic sales growth and an underlying trading operating profit margin range of 17.5% to 18.5% by 2025. Underlying earnings per share in constant currency to increase between 6% and 10%. COMMENTARY Growth was broad-based across most geographies and categories. Distribution costs as a percentage of sales decreased. (Nestle) Index Weighting: SMI (17.5% – largest), Stoxx 600 (2.8% – second largest) Shares -4% in European trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive amid tailwinds from the tech uplift in US futures following NVIDIA earnings. ASX 200 lagged as participants continued to digest an influx of earnings and after Australia’s Flash Manufacturing PMI returned to contraction territory. Nikkei 225 outperformed amid tech strength and eventually printed fresh intraday record highs above 39,000. KOSPI was marginally higher after the BoK kept rates unchanged and signalled an unlikelihood of a cut soon. Hang Seng and Shanghai Comp. were both firmer albeit with price action in Hong Kong choppy amid US-China chip-related frictions, while the mainland remained afloat after the latest stability efforts by China.

Top Asian News

- China’s Foreign Minister Wang said he feels Europe’s rational perception of China is increasing, believing China’s development is in line with the logic of history and Europe should not be afraid of it or reject it. Wang added that the European side is positive about strengthening China-EU exchanges at all levels and is very enthusiastic about deepening practical cooperation, while he would like to stress to the European side that ‘de-risking’ will not eliminate cooperation and ‘reducing dependence’ will not reduce mutual trust.

- Chinese small banks reportedly cut deposit rates to ease margin pressure, according to China Securities Journal.

- BoK maintained its base rate at 3.5%, as expected, with the decision made unanimously. BoK said it will maintain a restrictive policy stance for a sufficiently long period and will monitor the inflation slowdown, financial stability and economic growth risks, household debt growth, monetary policy operations in major countries and developments in geopolitical risks. BoK also stated that consumption and construction investment to recover at a slower pace, as well as noted that uncertainties to the growth outlook are high. Furthermore, Governor Rhee said five board members said the current interest rate should be maintained at least for the next three months and one board member said the door for a rate cut should be opened for the next three months, while Rhee added that he still doesn’t see much chances of a rate cut in H1 and that most members’ view it is too early to discuss rate cuts.

- Former BoJ policymaker Sakurai says BoJ could end negative rates in March if this year’s pay hikes exceed 4%, although there’s an equal chance it may wait until April, according to Reuters.

- Japanese PM Kishida says need to achieve wage hikes exceeding price increases

European bourses, Stoxx600 (+1.0%) soared at the open, taking lead from strong Nvidia (+13%) earnings, after-hours. Thereafter, in tandem with the softer-than-expected German PMI data, equities came off best levels and have been edging lower since, but remain markedly firmer on the session. European sectors are mixed; Tech is the clear outperformer after strong Nvidia earnings; peers such as ASML (+4.5%), BE Semiconductor (+15.7%, also on strong earnings) gain. Mercedes Benz (+4.9%) is leading the gains in the Autos sector, whilst Nestle (-4.3%) drags down Food Beverage and Tobacco. US Equity Futures (ES +1.0%, NQ +2%, RTY +0.5%) are entirely in the green, with clear outperformance in the tech-heavy NQ, after yet another strong earnings report from Nvidia (+13%).

Top European News

- EU is reportedly poised to release EUR 6.3bln in post-pandemic aid to Poland as early as next week in a major vote of confidence in the new government’s ability to mend ties with Brussels, according to Bloomberg.

- UK Chancellor Hunt is reportedly working on plans for a 99% mortgage scheme, via FT citing officials.

- BoE’s Greene says the tick-up in PMI data offers some grounds for optimism on growth in 2024; wage growth is heading in the right direction; services inflation generally started to ease; says she needs to see more evidence that UK inflation is not entrenched before she votes for a cut

FX

- USD is suffering at the hands of the NVIDIA-inspired jubilant move in the equity complex. DXY has been as low as 103.43 thus far (following French PMIs) before recovering in close proximity to its 200DMA at 103.69.

- An eventful morning for the EUR as strong French PMI metrics sent EUR/USD to a session peak of 1.0888 (50DMA sits at 1.0886) before a soft German manufacturing release sent the pair back to current levels of around 1.0855.

- GBP is benefitting from USD weakness with some two-way price action following mixed PMI metrics. As it stands, Cable is resting on its 50DMA at 1.2675.

- JPY is relatively steady vs. the USD with the pair remaining in consolidation mode after printing a YTD peak last week; trough of the session at 150.02.

- Antipodeans are both notably firmer vs. the USD as risk conditions prove supportive. AUD/USD cleared the 200DMA at 0.6563 and weekly high.

- PBoC set USD/CNY mid-point at 7.1018 vs exp. 7.1854 (prev. 7.1030).

Fixed Income

- USTs are near unchanged on the session as we await Fed speak & weekly US data with Wednesday’s FOMC Minutes release uneventful overall. More pertinently, the 20yr auction was poor, which sparked pressure in Treasuries.

- Bunds were initially hampered by the weak US outing, before then jumping lower on the hot French PMI data. Thereafter, a mixed German PMI release (big misses in Manufacturing & Composite), helped Bunds to rise back above 132.00 from their earlier trough at 131.78.

- Gilt price action moved in tandem with the aforementioned French/German data, before lifting by around 20 ticks after the UK Flash PMIs; currently holds around 97.30, towards the top-end of 96.92-97.49 bounds.

Commodities

- Crude is holding onto overnight gains after risk appetite was bolstered by all-around blockbuster earnings from tech giant Nvidia, with the mood reverberating cross-market. The larger-than-expected build in Private Inventories was ignored. Brent futures hold around USD 83.50/bbl.

- Firm trade across precious metals as a function of the risk-induced softness in the Dollar potentially coupled with some tailwinds from favourable technicals; XAU found support near its 21 DMA (2,024.16/oz) before rising above its 50 DMA (2,032.03/oz).

- Base metals are higher across the board this morning, but to varying degrees, with the complex bolstered by the risk-on sentiment and the weaker Dollar.

- Dubai sets the official crude differential for May at parity to DME Oman.

- German Economy Minster Habeck expects that gas prices will continue to fall.

- US Energy Inventory Data (bbls): Crude +7.2mln (exp. +3.9mln), Gasoline +0.4mln (exp. -2.1mln), Distillate -2.9mln (exp. -1.7mln), Cushing +0.7mln.

Geopolitics: Middle East

- Israeli military sounded sirens in the Red Sea port city of Eilat, warning of possible income aerial threats. It was separately reported that a possible medium-range ballistic missile launched by Iranian-backed Houthis in Yemen was intercepted by Israel’s Arrow air defence system over the Red Sea near Eilat.

- UKMTO has received reports of an incident 70nm south east of Aden, Yemen.

- UKMTO says it has been reported a vessel attack by two missiles, resulting in onboard fire 70NM Southeast of Yemen’s Aden.

- Ambery Saysp Alau-flagged, UK-owned general cargo ship was reportedly targeted with two missiles approx. 63NM Southeast of Aden, Yemen

Geopolitics: Other

- US, Japan and South Korea held a trilateral export control meeting at the US Embassy in Tokyo and agreed to cooperate further on Russia-bound export control and outreach to Southeast Asia, as well as critical tech export control, according to Japan’s Trade Ministry.

- US GOP Rep. Gallagher said during a delegation visit to Taipei that they are there to show bipartisan support for Taiwan and need to be more vigilant than ever to pass on the gift of freedom. Gallagher also stated that the message they want to send is that if China attempts an invasion, that effort would fail, while he added that the US stands with Taiwan, according to Reuters.

- Taiwan’s President Tsai thanked the US for continuing to help Taiwan strengthen its defences and said they will continue to engage with the world, as well as hope to see even more Taiwan-US exchanges this year. It was also reported that Taiwan’s President-elect Lai said they are facing great pressure from China and will continue to enhance defence capabilities, according to Reuters.

- China’s coast guard said it drove away a Philippine Fisheries and Aquatic Resources Bureau vessel that ‘illegally intruded’ into the waters adjacent to Scarborough Shoal, according to state media.

US Event Calendar

- 08:30: Feb. Initial Jobless Claims, est. 216,000, prior 212,000

- Feb. Continuing Claims, est. 1.88m, prior 1.9m

- 08:30: Jan. Chicago Fed Nat Activity Index, est. -0.21, prior -0.15

- 09:45: Feb. S&P Global US Manufacturing PM, est. 50.7, prior 50.7

- Feb. S&P Global US Services PMI, est. 52.3, prior 52.5

- Feb. S&P Global US Composite PMI, est. 51.8, prior 52.0

- 10:00: Jan. Existing Home Sales MoM, est. 4.9%, prior -1.0%

- Jan. Home Resales with Condos, est. 3.97m, prior 3.78m

Central Bank Speakers

- 10:00: Fed’s Jefferson to Give Speech, Q&A

- 15:15: Fed’s Harker Speaks on Economic Outlook

- 17:00: Fed’s Cook Speaks at Macrofinance Conference

- 17:00: Fed’s Kashkari Participates in Panel Discussion on Outlook

- 19:35: Fed’s Waller Speaks on Economic Outlook

DB’s Jim Reid concludes the overnight wrap

Strong guidance from Nvidia last night has given markets another boost this morning, with the stock surging by +9% in after-hours trading. That rally has extended more broadly, as S&P 500 futures are up +0.74%, and overnight the Nikkei surpassed its all-time intraday peak from 1989. So that’s a very big milestone, and it continues the Nikkei’s recent outperformance, having recorded a +16.5% gain over 2024 so far. That follows similar records in Europe yesterday, where both the DAX (+0.29%) and the CAC 40 (+0.22%) closed at all-time highs, and Euro HY spreads also reached their tightest level in over two years. That being said, there were further losses for sovereign bonds, and yields on 10yr Treasuries and bunds both closed at their highest level since November, thanks to hawkish central bank commentary and weak demand at a 20yr Treasury auction.

In terms of those Nvidia results, the company reported $22.1bn of revenue in Q4 (vs $20.4bn analyst expectations), representing a dramatic +265% increase in sales compared to a year earlier. It projected $24bn of revenue for the current quarter (above $21.9bn expectation), with Nvidia’s CEO speaking of a “tipping point” for generative AI. This strong outlook led Nvidia shares to post an impressive +9% gain in after-hours trading, though the magnitude of this move might be seen as par for the course given that, ahead of the release, options were implying a move of more than 10% in Nvidia’s share price today.

Before the release, US equities had actually had a mixed day yesterday, with the S&P 500 trading -0.6% lower less than an hour before the close, before recovering to advance +0.13%. Tech underperformance saw both the NASDAQ (-0.32%) and the Magnificent 7 (-0.31%) post modest declines, and Nvidia (-2.85%) had actually been the worst performer among the Magnificent 7 group. Things looked more promising outside of the big tech names, with 6 5% of S&P 500 companies gaining on the day. Moreover in Europe, the Euro Stoxx 50 (+0.32%) closed at a 23-year high, and both the DAX (+0.29%) and the CAC 40 (+0.22%) closed at an all-time high. The broader STOXX 600 was down -0.17%, but that was in large part due to the weakness among UK equities, where the FTSE 100 was down -0.73%.

On the rates side, a key story yesterday were the FOMC minutes, which reinforced the narrative that the Fed was in no rush to ease policy. According to the minutes, “most participants noted the risks of moving too quickly to ease the stance of policy and emphasized the importance of carefully assessing incoming data in judging whether inflation is moving down sustainably to 2 percent”, while “several participants mentioned the risk that financial conditions were or could become less restrictive than appropriate“. Meanwhile on QT, the minutes confirmed plans to begin in-depth balance sheet discussions at the March meeting, though this came with a view “to guide an eventual decision to slow the pace of runoff”, so not just suggesting that a change on QT is imminent.

The minutes came an hour after a 20yr Treasury auction, where weak demand helped to push up yields further, as the share of indirect bidders fell to its lowest since May 2021. Moreover, there was some hawkish commentary earlier in the day, which further contributed to the bond selloff. For instance, Richmond Fed President Barkin said in an interview (recorded on Tuesday) that “You do worry that when the goods price deflation cycle ends, you’re going to be left with shelter and services higher than you like it”. And over in Europe, the ECB’s Wunsch said “I believe one should not discard a scenario in which monetary policy stays tight for longer than currently expected”.

Collectively, that led investors to dial back their expectations for rate cuts again. In fact, the chance of a rate cut at the Fed’s March meeting was down to just 7%, which is the lowest in over three months. Bear in mind that a cut by March was fully priced at the start of the year, so we’ve seen a significant turnaround in expectations so far this year. And looking further out, the amount of cuts expected by the December meeting was down to just 86.7bps by the close, the lowest in more than three months, and a major decline from the 168bps expected less than six weeks ago.

Given all that, sovereign bond yields ended the day noticeably higher on both sides of the Atlantic. For instance in the US, the 1 0yr Treasury yield (+4.4bps) closed at its highest level since November, at 4.32%. Moreover, there was evidence that the recent increase in rates was filtering through to the real economy, as with 30yr mortgage rates back above 7% for the first time in over two months, according to data from the Mortgage Bankers Association for the week ending February 16. Back in Europe it was a similar story, with pricing of a rate cut by April down to 38%, its lowest in four months, while yields on 10yr bunds were up +7.5bps to 2.45%, also their highest closing level since November.

Overnight in Asia, we’ve seen all the major indices advance, with gains for the Nikkei (+1.91%), the Shanghai Comp (+1.00%), the CSI 300 (+0.73%), the Hang Seng (+0.74%) and the KOSPI (+0.34%). That’s been driven by the technology sector, and tech stocks in the Nikkei have led the index’s advance with a +3.97% gain. Separately, we’ve also seen growing confidence overnight that the Bank of Japan will adjust their ultra-loose monetary policy, as Governor Ueda said he expected the virtuous economic cycle to continue, and pointed out that services prices were continuing to rise. Indeed, yields on 2yr JGBs are currently at their highest level since 2011 overnight, and investors are now pricing in a 78% chance that they’ll deliver a hike by the April meeting.

Otherwise, today will bring the release of the February flash PMIs from around the world, and we’ve already had a few releases overnight. In Japan, the composite PMI fell back to 50.3, down from 51.5 the previous month, but in Australia, the composite PMI was back in expansionary territory at 51.8, marking its highest level in 10 months.

To the day ahead now, and data releases include the flash PMIs for February from Europe and the US, along with the US weekly initial jobless claims and existing home sales for January, as well as the euro area final inflation print for January. From central banks, we’ll get the ECB’s account of their January meeting, and also hear from the Fed’s Jefferson, Harker, Cook, Kashkari and Waller.

Tyler Durden

Thu, 02/22/2024 – 08:20

via ZeroHedge News https://ift.tt/57zAPeZ Tyler Durden