Positioning Is Worrying And Nobody Seems To Care

By Jan-Patrick Barnert and Michael Msika, Bloomberg Markets Live reporters and strategists

The market was braced for Nvidia’s earnings and they lived up to expectations, while the Fed minutes were pretty much a non-event. But the big picture is worrying: positioning is stretched and most investors don’t seem to care.

Some profit taking on tech stocks before the most anticipated earnings release of the season was hardly surprising. But now that Nvidia is out of the way, with the stock gaining 9% in post market trading, the big question is what investors will do about their very stretched equity exposure: build more, hold or start to unwind soon?

So far, portfolio managers have been busy buying into a bull trend perceived to have no ending. The Stoxx 600 is closing in on a record high and overbought levels, while CFTC future net positioning in dollar terms on the S&P 500 reached an all-time high earlier this month.

“Even post Tuesday’s selloff, indications of short-term US equity positioning remain stretched with quant funds, levered upside, momentum and call skew all more than two-thirds of the way to the levels that preceded two of the four largest S&P fragility events since 1928: Feb. 2018’s ‘Vixplosion’ and March 2020’s Covid shock,” say Bank of America derivatives strategists including Vittoria Volta. “With the pressure to chase momentum and fickle liquidity, fragility risks are high, though not extreme.”

That said, the strategists don’t see a bubble forming for the Magnificent 7 as their volatility has been falling, unlike during bubble episodes when price swings became more pronounced in concert with rising prices. “The decoupling between upside and downside vol in these stocks is reminiscent of the 2000s tech bubble, but earnings better meeting price-expectations and the asymmetry in Mag7’s macro reaction function suggests that this trend may be more due to the pain trade still being higher,” they say.

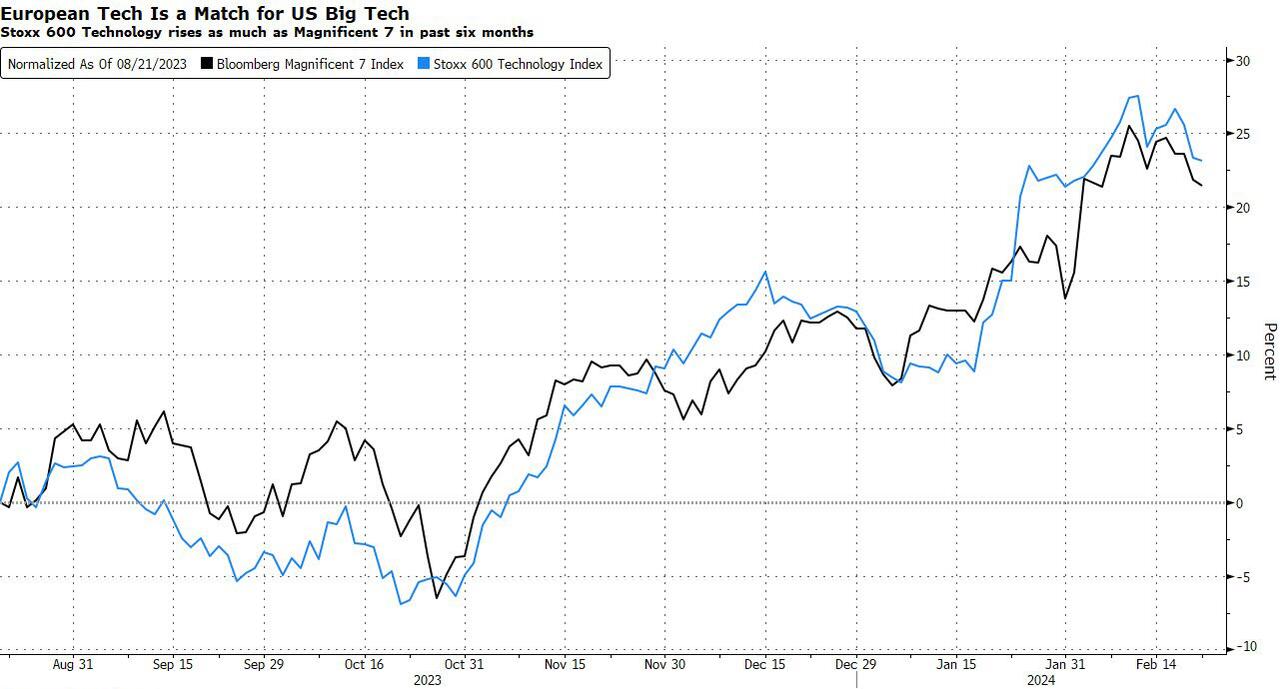

Europe hasn’t been immune to the tech hype — on the contrary. Tech is among the best performing Stoxx 600 sectors this year after a 9.1% surge, while ASML and SAP alone are responsible for a third of the benchmark’s gains and nearly half of the returns in the Euro Stoxx 50. Meanwhile, according to the BofA European fund managers survey, tech is now the most popular industry group, along with insurance. Following a massive surge in exposure last month, a net 32% of BofA’s respondents said they overweight the sector.

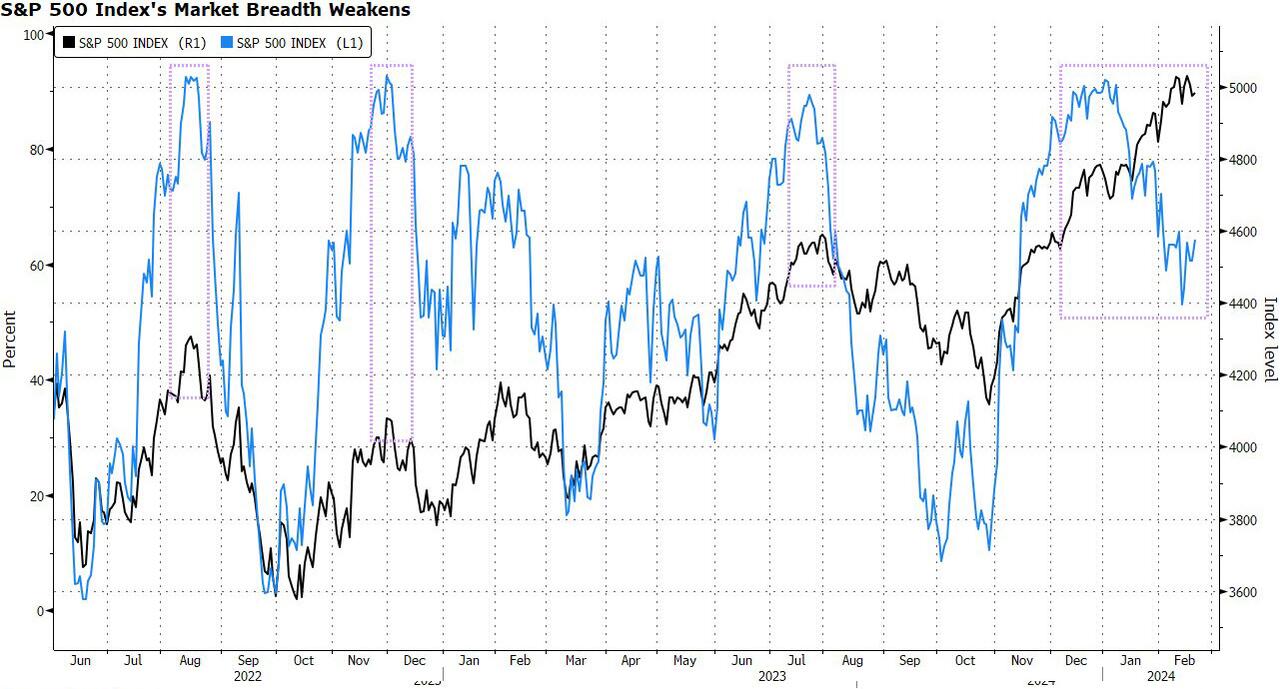

At the same time, tech sector breadth as measured by the short-term indicator of stocks trading above their 50-day moving average has weakened further. The indicator failed to confirm a top in the market as it had done multiple times over the past 18 months and instead decoupled from the wider benchmark as performance has become increasingly concentrated within a handful of stocks. This is most notable in the Nasdaq, where Nvidia and Meta account for almost 70% of this year’s gains.

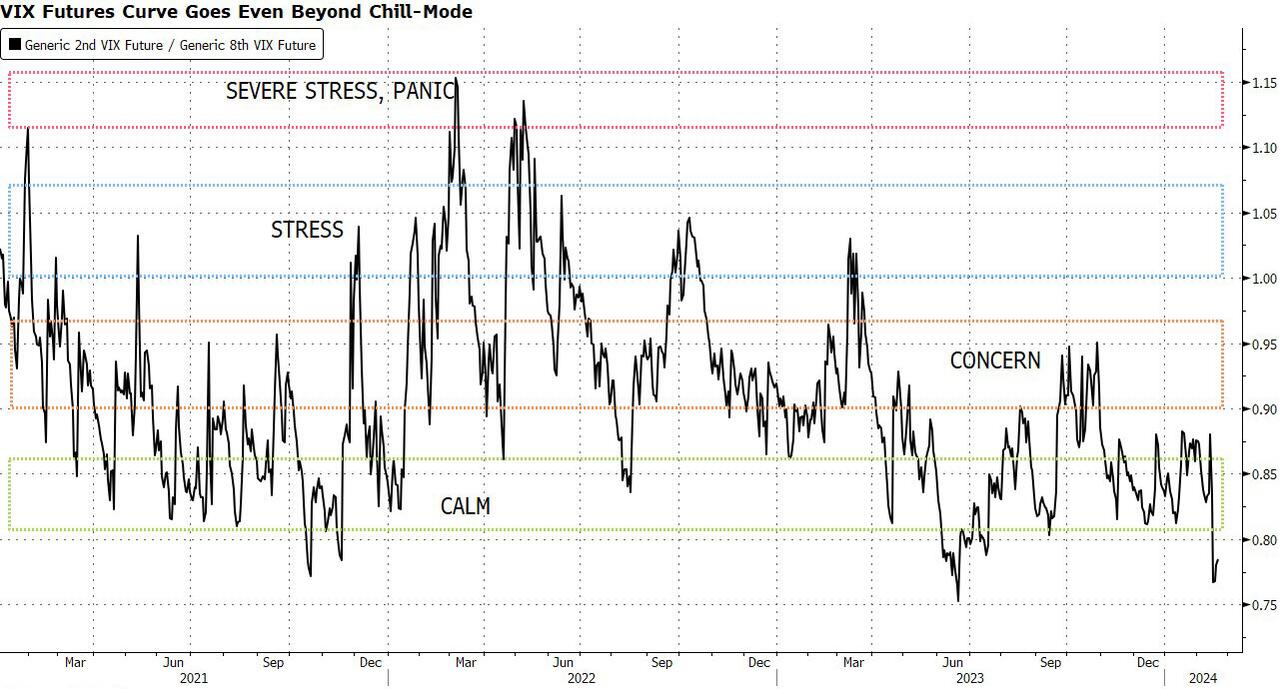

Overall, describing markets as calm sounds increasingly like an understatement — at least when using the favored VIX curve indicator, which has now fallen to the lowest level since 2017. Together with a collapsing skew reading for the wider market and especially for tech stocks, plus a put-call ratio below 0.8, all the signs suggest that just about nobody cares about downside risk at this point.

Nomura cross-asset strategist Charlie McElligott explains it thus: “The key to equities seemingly being able to keep shaking off nascent pullbacks? Well outside of the ongoing ‘AI euphoria’ theme and de-grossing of shorts, which continues powering spectacular rallies in the ‘worst of’ junk companies, it’s been all about the Pavlovian ‘Options Selling’ — flows which continue to suppress volatility.”

And while this low-volatility, high-momentum market environment that’s free of big moves has encouraged almost every systematic investor from vol control to trend followers toward near-maximum exposure, their impact is subdued for the moment. But their positioning could act as a combustive agent if things go wrong.

“Just like gamma exposure, systematic flows aren’t always about direction; sometimes, they can simply act as stabilizing forces in the market,” say Tier1Alpha strategists. “That said, these funds still pose a significant risk to the equities market this week, as even a small uptick in volatility could result in some significant selling.”

“Across sector groups, positioning in mega-cap growth and tech continues to rise and is into the top decile, with net call volume surging to pandemic boom levels this week while flows into tech funds also resumed their strong run,” according to Deutsche Bank strategists Parag Thatte and Bankim Chadha. They add that equity allocations by CTAs rose further last week to hit the 83rd percentile.

Tyler Durden

Thu, 02/22/2024 – 11:55

via ZeroHedge News https://ift.tt/I9Z2y6m Tyler Durden