Investors Finding It Increasingly Pointless To Be Bearish

By Jan-Patrick Barnert and Michael Msika

Investors are finding it increasingly pointless to be bearish as equity markets are about to lock in a fourth consecutive month of gains, the longest streak in Europe since the 2021 pandemic rally.

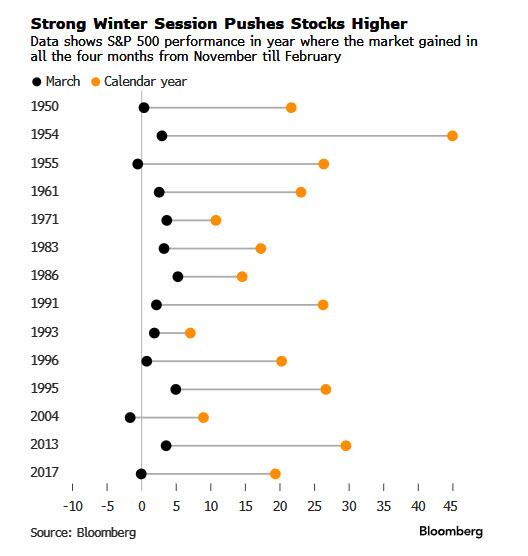

Even February’s performance looks quite impressive, contrary to the usual seasonal pattern of weakness in the second half of the month. Also, number crunching signals good news ahead: when the S&P 500 Index advances during the four winter months, the remaining calendar year’s performance has never been negative, and the year showed average annual gains of 21%.

And then there is the 1995 analogy that the Federal Reserve’s looming interest rate-cutting cycle may again allow the world’s largest economy to grow without stoking price pressures. If history serves as a guide, we could potentially be in for another massive bull ride.

So while keeping one eye on the exit door just in case the overwhelming belief in this rally starts to weaken, more and more bears seem to be giving in now. HSBC strategists this week ended their tactical underweight stance in equities. The bank’s chief multi-asset strategist Max Kettner said that sentiment and positioning have been stretched and remain elevated but that “this isn’t enough to prompt a significant correction in risk assets” without a “clear catalyst.”

And finding a shock event that would reverse the rally — and getting its timing right — is proving elusive. The macro backdrop and corporate earnings look fine, the US election is still a while away and it’s hard to see any candidate saying something so outrageous that it spooks investors. Geopolitics is one risk in investors’ minds, but unless there’s a serious escalation in the Middle-East, markets don’t seem to worry too much. China is busy tackling domestic issues, and while banks’ credit risk is in the spotlight, chances of contagion seem limited at this point.

Some market watchers are noting that the velocity of pushing to new highs is actually a sign of caution. Point taken, yet timing the peak seems almost impossible if looking at the history of the Nasdaq index. Also, the pace of gains is slower than during the Internet bubble.

Volatility is further adding fuel to the market — or at least not holding it back as the crowd of volatility sellers is stacking higher. Nomura strategists said that each month investors are selling $241 million of volatility, which helps compress market swings and keeps risk-on sentiment intact. That comes after $6 billion of inflows into ETFs using derivatives to create extra income over the first two months of the year, according to the bank.

Nomura’s Charlie McElligott said that the current market backdrop has created an environment for volatility sellers to “collect extra yield.” Namely, US stocks that “only go up and simply refuse to pull back due to AI mania and the perception of US economic Goldilocks allowing for a soft-landing” while at the same time investors get the benefits of expected easing by the Fed later in 2024.

The call wall — a significant resistance level for the market, sits just above the current spot price level. But there is very little to suggest this will cause big headaches anytime soon. The short gamma level, together with the CTA sell trigger, stand somewhere around 4,950/4,900 points for the S&P 500 Index. So we would need a sustained 4% move lower before even hitting this level, not to mention any pathway toward bigger declines.

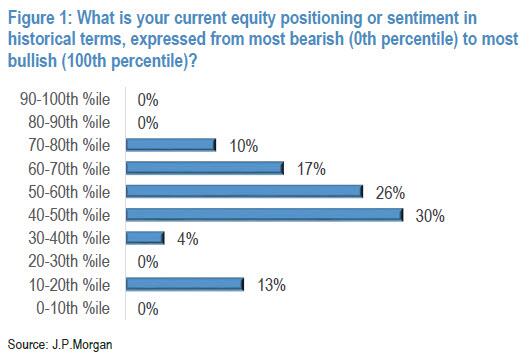

“Investor optimism is high and positioning is elevated, as a Goldilocks outcome or better has become consensus,” according to JPMorgan strategists led by Marko Kolanovic. More than half of the investors in the bank’s latest client survey see their equity positioning in the 40th to 60th percentile based on historical terms and 39% said they are still planning to increase equity exposure.

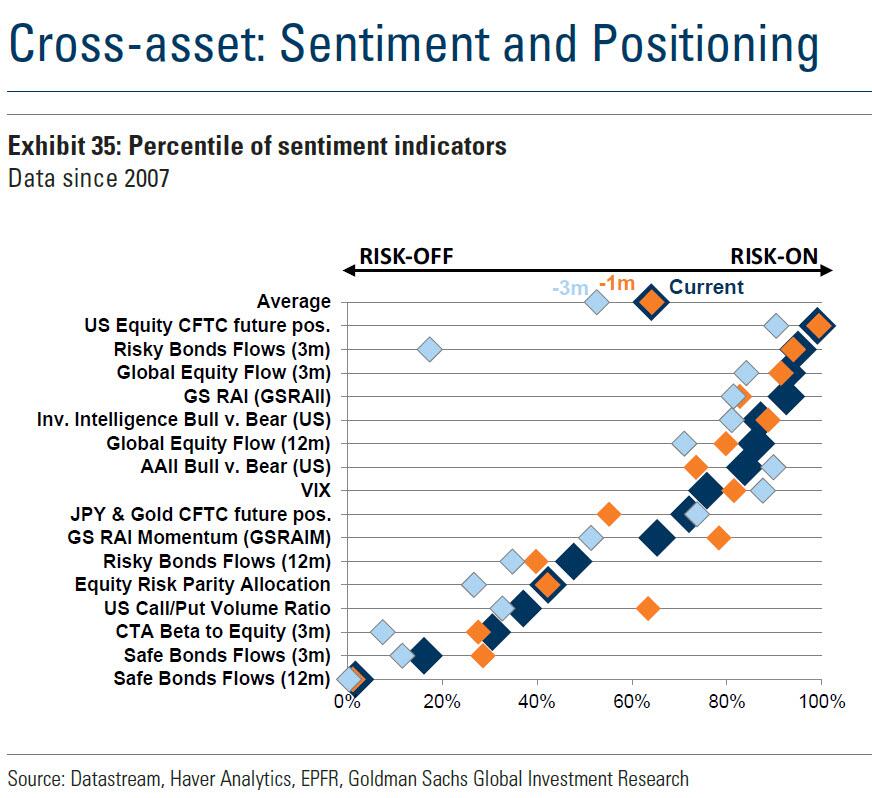

Half of Goldman Sachs’ sentiment indicators are now over the 80th percentile versus their own history — lead by positioning. Flow indicators also improving and even the fact that investors are generally exposed to concentrated positions can be seen as a two-edged sword, according to Goldman strategists including Cecilia Mariotti.

“On one side, this inevitably increases concerns around potential near-term setbacks in case of related shocks,” she wrote. “But on the other side it suggests there is space for bullish sentiment and positioning to be further supported, especially if we start seeing a more meaningful rotation out of cash and into risky assets and laggards within equities.”

Tyler Durden

Thu, 02/29/2024 – 12:40

via ZeroHedge News https://ift.tt/ysmE9WT Tyler Durden