Futures Jump, Bitcoin Rebounds After Tuesday Rout As Attention Turns To Powell Testimony

US stock futures reversed a sharp two-day selloff as traders waited to see if Fed Chair Jerome Powell will continue to push back against the prospect of speedy interest-rate cuts during his testimony to the House Financial Services Committee. As of 8:00am, S&P futures rose 0.3%, while contracts on the Nasdaq 100 added 0.8% as tech names rebounded following Tuesday’s 1.7% drop for the Nasdaq Composite; all of the Mag7 names are higher pre-mkt with additional strength in aemis where AVGO/MRVL are up 2.6% and 3.3% pre-mkt (both report earnings tomorrow). According to JPM, “we appear to be set up for a relief rally but given recent dips being bought and markets higher over the next 2-3 sessions it begs the question of whether yesterday was the pullback.” Bond yields are flat to up 1bp, and the dollar is being sold. The commodity complex is mixed with Energy higher, Metals lower, and Ags mixed. Bitcoin has staged a powerful rebound and recovered most of yesterday’s post-all time high losses. Today’s macro data focus is on Powell’s speech at 10am (Day 1 of 2), ADP (which has not been predictive of NFP), JOLTS, and Beige Book.

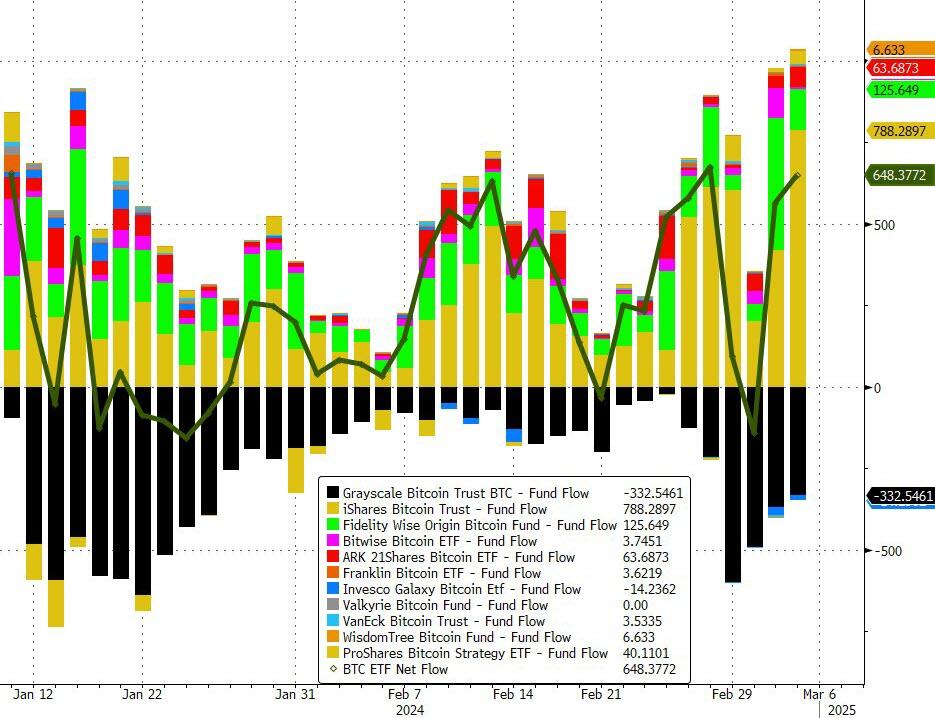

Also of note is that during yesterday’s brutal selling across crypto after bitcoin hit a new all time high, investors were BTFD like crazy with blowout ETF inflows. And just like that, crypto is now a “safe asset.”

In premarket trading, cybersecurity firm CrowdStrike soared after forecast-beating results, lifting in its wake peers Palo Alto Networks and Zscaler. Skincare companies’ shares dropped s after a report detailing how acne products from several brands are alleged to contain elevated levels of benzene, a chemical linked to cancer; Estee Lauder (EL US) -3.6%, Taro Pharmaceutical -3.5%. Cryptocurrency-linked stocks rally as Bitcoin rebounds from a temporary slump. In a volatile session on Tuesday, the cryptocurrency surged to a record for the first time in more than two years, before falling sharply. Among the crypto-linked moves, Cleanspark +6.3%, Cipher Mining +4.2%, Marathon Digital +5.7%, MicroStrategy +11%, Coinbase Global +5.6% and Riot Platforms +6.1%. Chinese e-commerce company JD.com Inc. soared in New York after it announced strong results and a $3 billion buyback. Here are the other notable premarket movers:

- ChargePoint (CHPT US) shares decline 5.0% after the electric-vehicle charging company reported fourth-quarter revenue that missed estimates. Additionally, the company’s first-quarter revenue guidance didn’t meet analyst expectations.

- Couchbase (BASE US) shares jump 8.9% after the infrastructure software company reported fourth-quarter results that beat expectations and gave a first-quarter forecast that is slightly above the analyst consensus.

- CrowdStrike (CRWD US) shares jump 23% after the cybersecurity provider reported fourth-quarter results that were stronger than expected and gave an outlook that is above the analyst consensus. Peers also gain: SentinelOne (S US) +11%, Palo Alto Networks (PANW) +3.4%, Fortinet (FTNT US) +3.3%, Zscaler (ZS US) +4.5%, Okta (OKTA US) +2.6%, Cloudflare (NET US) +3.2%

- Dada (DADA US) ADRs rally 15% after the JD.com unit said it will reverse overstated revenue in some quarters after an independent review found that some online advertising and marketing-services transactions were conducted primarily to meet sales targets; JD.com gained +12%

- Entravision Communications (EVC US) shares tumble 46% after reporting that Meta Platforms plans to wind down its authorized sales partner program, which accounted for about half of Entravision’s revenue last year.

- Nordstrom (JWN US) shares slide 11% after the department-store operator reported fourth-quarter net sales that were short of consensus expectations. Morgan Stanley said the “disappointing” outlook overshadowed beats in earnings per share and revenue.

- PDD Holdings (PDD US) ADRs fall 3.2% underperforming other US-listed Chinese stocks.

- Ross Stores (ROST US) shares drop 2.8% after the discount department store chain issued full-year comparable sales guidance that missed estimates. Jefferies said the guidance came in below their expectations, while TD Cowen noted the conservative outlook left room for a future beat and raise.

In yesterday’s main event outside of markets, Donald Trump and Joe Biden sailed through the Super Tuesday round of primaries, edging closer to a general election rematch in November. There were no surprises there, nor was it a surprise when Nikki Haley announced she is dropping out of the presidential race. If anything, the question is why it took this long.

Attention now turns to Powell’s semiannual testimony before Congress, where he is widely expected to reiterate that the Fed does not see an urgent need for rate cuts, given robust economic data in recent months. A meeting of the European Central Bank is due Thursday, followed by monthly US payrolls data on Friday.

“The market is certainly not expecting a breakthrough from Powell, the ECB or Friday’s job data,” said Francois Rimeu, a strategist at La Francaise Asset Management in Paris. Rimeu predicted this year’s equity gains will extend, with many investors fearful of missing out on the rally. The S&P 500 hasn’t suffered a drop of 2% or more in one day since February 2023, the longest run without such a pullback in six years. “I expect many investors late on the rally will buy the dips along the way,” he said.

European stocks are green and hovering near record levels with the Stoxx 600 up 0.3% as investors await Federal Reserve Chair Jerome Powell’s testimony on Wednesday and the European Central Bank’s meeting later in the week. Real estate and chemicals stocks outperform, while the health care and media sectors lag. Here are the most notable premarket movers:

- D’Ieteren shares rise as much as 6.3% after releasing results. The spotlight is on the Belgian car dealer’s “finally rock solid” free cash flow and strong net position, according to Degroof.

- IMCD shares advance as much as 4.4% after JPMorgan double-upgrades to overweight and calls the Dutch chemicals distributor “one of the best earnings compounders in the sector.”

- IAG shares rise as much as 4.9% after a double-upgrade at JPMorgan to overweight from underweight, as the broker sees investments boosting the airline group’s earnings in the longer term.

- ConvaTec shares rise as much as 7.6% after the company lifted its mid-term sales growth target. Analysts say this demonstrates the company continues to execute its strategy.

- Scor shares gain as much as 7.8% after the insurer delivered a solvency beat and confirmed a dividend in-line with expectations.

- TUI shares rise as much as 6% in London after Morgan Stanley upgrades to overweight from equal-weight, citing a solid travel demand outlook and the tour operator’s “very low” valuation.

- Dassault Aviation shares slide as much as 5.6%, slipping from Tuesday’s record-high close, after the French aircraft maker released an update which analysts describe as “mixed.”

- DHL shares slide as much as 5.5% after the German logistics firm presented weaker-than-expected 4Q earnings, weighed down by its Express and Freight Forwarding divisions.

- Antofagasta shares fall as much as 3.8% after the copper miner was downgraded by both Barclays and RBC Capital Markets.

- Legal & General shares decline as much as 4.9% after full year operating profit at the financial services company missed the average analyst estimate.

- Grifols shares decline as much as 18% after Moody’s placed the company’s rating on review for downgrade and Gotham City Research published new questions on its accounting methods.

- Basic-Fit shares fall as much as 6.4% after a downgrade to equalweight by Barclays, which cited the potential for the gym operator’s German rollout to be more costly than expected.

Earlier in the session, Asian stocks gained as traders continued to digest China’s ambitious 5% growth target announced at a top official meeting, while Chinese tech shares rebounded ahead of key earnings releases. The MSCI Asia Pacific Index erased earlier losses to rise as much as 0.4%. Chinese tech giants such as Alibaba and Tencent were the biggest boosts to the regional gauge, while JD.com surged ahead of its fourth-quarter results. An index of Chinese shares listed in Hong Kong jumped more than 2%, while the onshore CSI 300 Index also edged higher. “Hong Kong’s rebound is led by tech and in particular JD.com. It looks to be related to expectations on its results due today,” said Marvin Chen, a Bloomberg Intelligence strategist. “There could be some short covering in JD.com as well.”

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The yen is up 0.2% but off its best levels having rallied on reports at least one BOJ policymaker will say it’s appropriate to end negative rates at the March meeting. The BOJ is also said to be getting more confident over the strength of wage growth. GBP/USD rises as much as 0.2% to 1.2731, in line with peers; Aussie climbs 0.3%, recovering from an early slip after data showed Australia’s economy slowed in the final three months of last year as elevated interest rates and rising living costs dragged on household spending. Kiwi dollar also recovers from weakness following Reserve Bank of New Zealand chief economist Paul Conway saying the central bank may be able to start cutting interest rates sooner than it currently expects to if the Fed begins easing later this year; Climbs 0.3% to 0.6104 amid broad dollar weakness. USD/JPY declined as much as 0.5% to 149.33 before paring the move.

In rates, treasuries were slightly cheaper across the curve in early US trading amid bigger losses across core European rates. 10-year yields around 4.16% are ~1bp cheaper on the day, bunds and gilts in the sector by an additional 2.5bp and 3.5bp; curve spreads are broadly within 1bp of Tuesday’s closing levels. Gilts underperformed ahead of the UK budget announcement where Chancellor Jeremy Hunt is expected to unveil personal tax cuts. JGBs were hit overnight following report on Mitsubishi UFJ Financial Group Inc.’s view that the BOJ will end negative rates in March. US session includes Fed Chair Powell’s congressional testimony before the House Financial Services Committee along with two peripheral labor-market reports.

In commodities, Oil prices advance, with WTI rising 1% to trade near $78.90. Spot gold is little changed around $2,127. Bitcoin jumps ~5%.

As noted above, Bitcoin climbs firmly above USD 66k after sinking below USD 60k in the prior session, after making ATHs.

US 10-year yields rise 1bps to 4.16%. European stocks are green and hovering near record levels with the Stoxx 600 up 0.3%. S&P futures rise 0.4% while Nasdaq 100 contracts add 0.8%. The Bloomberg Dollar Spot Index falls 0.1%. The yen is up 0.2% but off its best levels having rallied on reports at least one BOJ policymaker will say it’s appropriate to end negative rates at the March meeting. The BOJ is also said to be getting more confident over the strength of wage growth. Oil prices advance, with WTI rising 1% to trade near $78.90. Spot gold is little changed around $2,127. Bitcoin jumps ~5%.

Looking ahead, the US economic data calendar includes February ADP employment change (8:15am), January JOLTS job openings and wholesale inventories (10am). Fed speakers scheduled include Powell (10am New York time, though Fed sometimes releases text at 8:30am), Daly (12pm) and Kashkari (4:15pm); Fed releases Beige book at 2pm.

Market Snapshot

- S&P 500 futures up 0.4% to 5,104.75

- STOXX Europe 600 up 0.3% to 497.95

- MXAP up 0.5% to 175.11

- MXAPJ up 0.6% to 529.11

- Nikkei little changed at 40,090.78

- Topix up 0.4% to 2,730.67

- Hang Seng Index up 1.7% to 16,438.09

- Shanghai Composite down 0.3% to 3,039.93

- Sensex up 0.5% to 74,047.47

- Australia S&P/ASX 200 up 0.1% to 7,733.54

- Kospi down 0.3% to 2,641.49

- German 10Y yield little changed at 2.35%

- Euro up 0.1% to $1.0873

- Brent Futures up 0.8% to $82.69/bbl

- Gold spot down 0.0% to $2,127.53

- U.S. Dollar Index down 0.15% to 103.64

Top Overnight News

- Chinese policymakers held a rare joint news conference to defend the new economic targets for 2024 and ensure that additional tools exist to bolster growth. Nikkei

- China set a bullish target of around 5% growth this year as top leaders try to boost confidence in the world’s second-largest economy. But for analysts, Premier Li Qiang’s lack of details on how to get there was out of step with the nation’s deep challenges. BBG

- The PBOC has room for further cuts to the reserve requirement ratio and will push for financing costs to trend lower, Governor Pan Gongsheng said. That suggests the PBOC will be more active in easing to bolster demand, Mizuho said. China’s 10-year yield slipped. BBG

- South Korea’s headline CPI ticks up to +3.1% in Feb (up from +2.8% in Jan and ahead of the Street’s +3% forecast) while core is unchanged and inline at +2.5%. WSJ

- Some Bank of Japan (BOJ) board members are likely to say that lifting negative interest rates is reasonable at a policy meeting this month, Jiji Press reported on Wednesday without citing sources. If a majority of the nine-member board vote in favor of ending negative rates it would pave the way for the first rate hike since 2007. RTRS

- Biden urges Hamas to agree to a ceasefire, warning of a “very, very dangerous” situation if one isn’t reached by the start of Ramadan on 3/10. SCMP

- “Super Tuesday” saw Trump and Biden dominate their respective parties (although they each lost once, Trump in Vermont and Biden in American Samoa), but with some large warning signs for each (Trump continues to perform poorly with suburban and educated voters while Biden’s “uncommitted” and 3rd-party problem is very real in certain critical swing states). Politico

- Trump met with Elon Musk and a few wealthy GOP donors on Sunday as the former president looks for a major financial influx to bolster his campaign (Musk apparently thinks it’s essential that Biden be defeated in Nov). NYT

- Nikki Haley plans to suspend her Republican presidential primary bid in a speech Wednesday morning. Her decision arrived the day after Super Tuesday, when she won only Vermont among 15 states that held GOP contests. Haley won’t announce an endorsement Wednesday, the people said. She will encourage Donald Trump, who is close to having the delegates needed to win the GOP nomination, to earn the support of Republican and independent voters who backed her. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly choppy with early pressure following the tech-led declines stateside where Apple shares entered into a technical correction following a slump in China iPhone sales. ASX 200 traded rangebound as financials offset the losses in tech, while GDP data was somewhat inconclusive. Nikkei 225 gapped beneath the 40,000 level at the open before recovering the majority of losses. Hang Seng and Shanghai Comp. shrugged off early caution with outperformance in Hong Kong driven by tech and healthcare, while price action in the mainland was more reserved amid US-China frictions and some growth-related pessimism.

Top Asian News

- RBNZ Chief Economist Conway said declines in core inflation are encouraging and rates need to stay restrictive for a sustained period. Conway said the picture for household consumption is soft and household inflation expectations are a risk, while he added the Fed cutting before the RBNZ could lead to weaker inflation.

- Australian Treasurer Chalmers said the economy is not immune to a global downturn and the balance of risks is shifting from inflation to growth, while he expects Q1 2024 GDP to remain weak.

- China’s NPC and CPPCC press conference: Chinese State Planner Head says sees stronger economic growth trend this year; PBoC Governor says there is still room for RRR cuts; Will maintain appropriate increase in money supply. Click here for all commentary.

- Fitch affirms Korea at AA-; outlook stable

European bourses, Stoxx600 (+0.3%) began the session on a mixed footing and trading on either side of the unchanged mark. As the morning progressed, indices moved into the green and currently trades near session highs. European sectors hold a positive tilt; Chemicals is propped up BASF (+2.5), after the Co. announced global price hikes for chemicals. Media is found at the foot of the pile, and Insurance is also found in the red, weighed on by Legal & General (-4.1%), post-earnings. US Equity Futures (ES +0.4%, NQ +0.7%, RTY +0.5%) are in the green, posting gains similar to that seen in Europe. There is some outperformance in the NQ, attempting to pare back some of the significant losses seen in the prior session. In terms of individual movers, CrowdStrike (+24.5%) is higher in the pre-market after beating on its results and raising guidance.

Top European News

- UK Chancellor Hunt said we can now help families with permanent tax cuts and must bring down borrowing so we can start to reduce debt, according to Reuters.

- UK Chancellor Hunt’s expected decision to lower national insurance by 2p has triggered speculation over a potential May election, according to The Telegraph.

- Ukraine is willing to accept restrictions on EU trade as Kyiv seeks to resolve a dispute with Poland but wants the bloc to ban Russian grain imports, according to FT.

- UK Chancellor Hunt will, according to one Cabinet Minister, announce a 2pp cut to National Insurance and a 1pp cut to Income Tax in the budget, via Playbook; subsequently, Times’ Swinford says UK Chancellor Hunt “won’t” reduce income tax by 1p alongside a 2p reduction in national insurance.

- French Finance Minister Le Maire says the 2023 budget deficit will be significantly above target and the EUR 10bln of spending cuts planned for 2024 are “an emergency brake”, via Le Monde.

FX

- USD broadly softer vs. peers with initial JPY strength acting as a drag on the dollar before other peers began to outmuscle the greenback. DXY session low is at 103.58 matching yesterday’s trough.

- EUR is inching gains vs. the USD with a session best of 1.0879 surpassing yesterday’s 1.0876 peak. If this gives way, Feb 22nd high at 1.0888 will come into view, with the psychological 1.09 mark just above.

- GBP is benefitting from the broadly weaker USD with a high watermark of 1.2731 just below yesterday’s 1.2735 peak. Fate for the pair may well today be sealed via the UK budget. If gains extend beyond yesterday’s peak, Feb 2nd high resides at 1.2772; UK Chancellor Hunt expected to cut NI by 2p & possibly Income Tax by 1p.

- JPY gained sharply vs. the USD in early trade following reporting that some policymakers could support hiking rates in March. USD/JPY fell to a low of 149.33 but was unable to crack last week’s trough at 149.20. The pair then retraced much of the move, before slipping once again on yet another BoJ source, though this move was pared and currently holds around 149.80.

- Antipodeans are both firmer vs. the USD and outperforming across the majors. AUD saw mixed GDP data overnight but has been able to climb back onto a 0.65 handle. Weekly high sits just above current levels at 0.6535.

- PBoC set USD/CNY mid-point at 7.1016 vs exp. 7.1939 (prev. 7.1027).

- Turkish central bank said it has taken additional tightening measures to reinforce its commitment to tight policy and adjusted the loan monthly growth limit within the scope of loan growth-based securities maintenance practice, according to Reuters.

Fixed Income

- USTs are lower by a handful of ticks but holding above the 111-00 mark as specific newsflow has been somewhat light. The docket ahead is dominated by Chair Powell who is providing semi-annual testimony to the House today and Senate on Thursday.

- Gilts were pressured after a Politico piece citing a UK Cabinet Source said the Chancellor will cut NI by 2pp (as reported by the Times on Tuesday) and cut Income Tax by 1pp. Gilts will judge the UK budget at 12:30 GMT / 07:30 ET, where the focus will be on whether Hunt has left enough fiscal breathing space and on the Gilt remit. Following additional sources (Times’ Swinford) pushing back on the Income Tax cut benchmarks lifted off lows to around 98.90.

- Bunds are pressured in tandem with Gilt price action and ultimately unreactive to German trade data which saw a record balance and strong export numbers; currently hold around 132.80 with downside of circa. 40 ticks.

Commodities

- Crude is firmer despite a lack of major catalysts but amid a weaker Dollar and following a bullish-leaning private inventory report yesterday; Brent back above USD 82.50/bbl.

- Precious metals are flat/mixed trade and taking a breather from the recent rally despite the weaker Dollar but ahead of risk events; Spot gold trades within a narrow USD 2,123.75-2,131.60/oz parameter after hitting a high of 2,141.88/oz yesterday.

- Base metals trade mostly higher amid the softer Dollar, and possibly coupled with some economic optimism expressed by Chinese officials at the NPC and CPPCC press conference, in which the PBoC Governor also highlighted more room to cut the RRR.

- Saudi Arabia set April Arab light crude OSP to Asia at Oman/Dubai + USD 1.70/bbl and to NW Europe at ICE Brent + USD 0.30/bbl, while it set OSP to US at ASCI + USD 4.75/bbl.

- UBS forecasts spot gold to rise to USD 2250/oz by end-2024

Geopolitics: Middle East

- Hamas senior official said any exchange of prisoners cannot take place except after a ceasefire. Hamas also said that they showed flexibility to try to reach an agreement and will continue negotiating through mediators until they reach an agreement.

- Hezbollah said it targeted a building in the Avivim settlement in Israel with appropriate weapons and achieved a direct hit, according to Al Jazeera.

- US CENTCOM said its forces shot down anti-ship ballistic missiles and three one-way attack unmanned aerial systems launched from Iranian-backed Houthi-controlled areas of Yemen, according to Reuters.

- UKMTO received a report of a merchant vessel being hailed over VHF for approximately 30 minutes, while the vessel was hailed by an entity declaring itself to be the Yemeni Navy and ordered it to alter course, according to Reuters.

- Yemen’s Houthis said they carried out a qualitative military operation in which they targeted two US warship destroyers in the Red Sea.

- UKMTO receives report of an incident 54NM Southwest of Aden, Yemen.

- US Democrats say Rafah invasion “likely” violates President Biden’s requirement that US military aid be used in accordance with international law, according to Axios sources.

Geopolitics: Other

- Russian Foreign Intelligence Service director Naryshkin said French President Macron’s statement about NATO soldiers in Ukraine shows the irresponsibility of European leaders and are pushing the world to a nuclear war, according to TASS.

- US State Department said the US stands with the Philippines following China’s provocative actions against lawful Philippine maritime operations in the South China Sea, while the US condemns China for repeatedly obstructing Philippine vessels’ high seas freedom of navigation, according to Reuters.

- Second drone hit iron ore refinery in Russia’s Kursk region, according to the regional governor; The iron ore refinery in Russia’s Kursk region is working normally after a second drone attack, according to a representative cited by Reuters.

- Russia’s Kremlin says America is fighting against Russia, according to Ria

US Event Calendar

- 08:15: Feb. ADP Employment Change, est. 150,000, prior 107,000

- 10:00: Jan. Wholesale Trade Sales MoM, est. 0.3%, prior 0.7%

- 10:00: Jan. JOLTs Job Openings, est. 8.85m, prior 9.03m

- 10:00: Jan. Wholesale Inventories MoM, est. -0.1%, prior -0.1%

- 14:00: Federal Reserve Releases Beige Book

Central Bank speakers

- 10:00: Fed Chair Powell Testifies Before Congress

- 12:00: Fed’s Daly to Give Keynote Address

- 14:00: Federal Reserve Releases Beige Book

- 16:15: Fed’s Kashkari Speaks at WSJ Event

Tyler Durden

Wed, 03/06/2024 – 08:14

via ZeroHedge News https://ift.tt/uohGI39 Tyler Durden